Financial Operations

Accounting for Agencies: A Founder's Profit Guide

Master accounting for agencies with our guide on revenue recognition, KPIs, and month-end closing. Build an investor-ready finance function for your agency.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··24 min readAgencies do not fail on accounting because the math is hard. They fail because generic bookkeeping hides the decisions that drive profit. Revenue gets recorded in the wrong period. Retainers get treated like cash receipts instead of earned work. Project margins look healthy until rework, scope creep, and senior team time show up too late to fix them.

For agencies between $500K and $20M, that is not a bookkeeping inconvenience. It is a valuation problem, a cash planning problem, and an audit risk.

Most articles on accounting for agencies stay at the beginner level. They tell you to track expenses, send invoices, and reconcile the bank. That advice is fine for a freelancer. It is weak advice for an agency with retainers, milestone billing, pass-through spend, deferred revenue, and a founder trying to trust the numbers before hiring, borrowing, or preparing for diligence. What you need is an accounting system built for accrual reporting, ASC 606 revenue recognition, and client-level margin analysis, not a generic chart of accounts and a bookkeeper who closes the month whenever they get to it.

If you want a baseline on operational bookkeeping structure, this bookkeeping guide for marketing agencies is a useful starting point. This article goes further. It focuses on the accounting judgments and reporting discipline that turn messy agency financials into investor-ready statements.

That difference matters. If your revenue is recognized too early, profit looks inflated and future months get weaker on paper. If revenue is recognized too late, you understate performance and make planning harder than it needs to be. Either way, bad timing creates bad decisions. You hire too soon, cut spending too late, or price work off distorted margins.

Even categories outside the agency world, such as nonprofit accounting software, show the same pattern. Once revenue rules and reporting obligations get more complex, basic bookkeeping stops being enough.

You need accounting for agencies that answers three questions with precision. Which clients produce margin. Whether your delivery model converts labor into profit. How much cash and earned revenue you can rely on next quarter. Everything else is secondary.

Why Standard Accounting Fails Your Agency

Most bookkeeping setups answer the wrong question.

They tell you whether cash came in and bills went out. They don’t tell you whether Client A is carrying the business while Client B is burning margin through rework, senior team involvement, and underbilled scope. For an agency, that’s the whole game.

The problem starts with the accounting method. Cash basis accounting creates distorted financial statements for agencies and is only workable for very early-stage businesses with simple revenue structures, while accrual accounting gives far better visibility when you have multiple clients, staff, retainers, or project work, as explained in this agency bookkeeping breakdown. If you invoice late in the month, cash basis makes a strong delivery month look weak. If old invoices happen to clear during a slow month, cash basis makes a weak month look profitable.

Your inventory is time

A product company buys inventory, sells units, and tracks margin against physical goods. Your agency sells expertise and labor capacity. That means your direct costs sit inside payroll, contractors, software used for delivery, and the time your team logs against client work.

If your books dump all payroll into one operating expense bucket, you’ve blinded yourself. You can’t separate direct delivery cost from overhead. You can’t calculate delivery margin cleanly. You can’t see which work is worth doing.

Here’s a simple example using worked numbers.

| Scenario | Cash Received This Month | Work Delivered This Month | Direct Delivery Cost This Month | What cash basis suggests | What accrual shows |

|---|---|---|---|---|---|

| Retainer client | $0 | $10,000 | $6,000 | Bad month | Profitable work delivered, invoice still outstanding |

| Project client | $20,000 | $5,000 | $4,500 | Great month | Most cash is unearned, little margin recognized so far |

| Total | $20,000 | $15,000 | $10,500 | “Strong” cash month | Mixed performance with limited earned profit |

Under cash basis, you’d tell yourself the month looked solid because collections were high. Under accrual, you’d see that one client still owes you for profitable work, while another prepaid for work you haven’t fully earned yet.

Practical rule: If your accounting can’t separate invoicing from earning, it can’t support pricing, hiring, or forecasting decisions.

Generic setups miss the agency model

A default QuickBooks or Xero chart of accounts is built for generic small businesses. That structure usually fails agencies because it doesn’t organize revenue and costs by service line, client work, pass-through spend, or delivery labor. That’s why I tell founders to stop copying bookkeeping templates from businesses that sell inventory or simple subscriptions.

If you’re comparing finance tools across business models, even something like this guide to nonprofit accounting software is useful for one reason. It shows how much the chart of accounts and reporting structure need to match the operating model. Agencies need the same kind of intentional setup, just adapted for project delivery and client profitability.

One more mistake founders make. They think “clean books” means reconciled bank accounts. That’s not enough. Clean books for an agency also mean revenue is recognized correctly, delivery costs are coded properly, and client-level reporting ties back to the general ledger. If your current setup doesn’t do that, start with a more agency-specific foundation like this guide on bookkeeping for marketing agencies.

Building Your Agency's Financial Blueprint

A generic chart of accounts is one of the fastest ways to lose control of an agency between $500K and $20M. It hides delivery margin, distorts service-line performance, and leaves you with financials that look tidy but fail under lender, buyer, or audit scrutiny.

Founders usually discover this too late. Revenue looks healthy. Cash feels tight. Hiring decisions get made off topline numbers instead of actual contribution margin.

Your accounting structure needs to mirror how an agency earns, delivers, and bills.

Build the chart of accounts around agency economics

Set up the chart of accounts to separate four things clearly:

- Revenue by contract type so you can compare retainers, fixed-fee projects, and time-and-materials work.

- Direct delivery costs so labor, contractors, and delivery tools sit below the right work.

- Pass-through client spend so media, print, and software rebills do not inflate operating performance.

- Balance sheet timing accounts so prepayments, deposits, and earned but unbilled work do not get buried in revenue.

That structure gives you investor-ready reporting instead of basic bookkeeping. You can calculate Agency Gross Income, gross margin by service line, delivery margin by client, and working capital exposure from unbilled or prepaid work. Those are the numbers that drive pricing, staffing, and cash planning.

Parakeeto’s agency metrics analysis notes that healthy service-based agencies often target gross margins in the 50 to 65 percent range, and that admin expense often lands around 8 to 12 percent of AGI once the books are structured properly for agency reporting. Start with AGI. Then judge the rest of the cost structure against it. Parakeeto’s agency metrics analysis

Recommended agency chart of accounts

| Account Type | Account Name | Example Sub-Accounts |

|---|---|---|

| Revenue | Retainer Revenue | SEO Retainers, Paid Media Retainers, Creative Retainers |

| Revenue | Project Revenue | Website Projects, Brand Strategy Projects, Launch Campaigns |

| Revenue | Time and Materials Revenue | Hourly Strategy, Development Hours, Design Hours |

| Revenue | Other Service Revenue | Audit Fees, Workshops, Consulting |

| Contra / Pass-Through | Client Pass-Through Billings | Media Spend Rebill, Printing Rebill, Software Rebill |

| Cost of Goods Sold | Direct Labor | Strategists, Designers, Account Managers, Developers |

| Cost of Goods Sold | Freelancers and Contractors | Copywriters, Editors, Specialists, Production Support |

| Cost of Goods Sold | Delivery Software | Reporting Tools, Design Tools, PM Tools used in delivery |

| Cost of Goods Sold | Other Delivery Costs | Stock Assets, Project-Specific Licenses, Travel tied to client delivery |

| Balance Sheet | Deferred Revenue | Retainer Prepayments, Project Deposits |

| Balance Sheet | Unbilled Receivables | Earned Not Yet Invoiced |

| Balance Sheet | Prepaid Client Costs | Media Prepayments, Vendor Advances |

| Operating Expenses | Sales and Marketing | Salaries, CRM, Proposal Tools, Lead Gen |

| Operating Expenses | General and Administrative | Accounting, Legal, Insurance, Admin Software |

What this structure lets you see

Assume a client pays you $25,000 in one month. That invoice includes $8,000 of media spend. Your actual service revenue is $17,000. Direct labor tied to the account is $7,000, freelancers are $1,500, and delivery software allocation is $500.

Your reporting should show:

- Gross Revenue: $25,000

- Less Pass-Through Expenses: $8,000

- Agency Gross Income: $17,000

- Direct Delivery Cost: $9,000

- Gross Profit: $8,000

- Gross Margin on AGI basis: $8,000 ÷ $17,000 = 47.1%

That client is not nearly as strong as the topline suggests.

This is the mistake I see constantly. A founder looks at a $25,000 account and assumes it supports another hire. The AGI view shows a different reality. After delivery costs, there is not much room for overhead, mistakes, or scope creep. If you price, staff, or forecast off gross billings, you will overhire and compress profit.

Build for decisions, not bookkeeping cleanup

A strong agency chart of accounts should answer specific management questions every month:

- Which service lines produce the highest AGI?

- Which clients consume the most delivery labor relative to revenue?

- How much of billed revenue is still deferred or unearned?

- How much work is completed but not yet invoiced?

- Are sales, admin, and delivery costs in line with target margin?

If your books cannot answer those questions, they are not finished.

A founder planning headcount or changing service mix also needs the accounting structure tied to forward-looking scenarios. A practical next step is building a model that uses AGI, labor capacity, and target margin assumptions together. This guide to financial modeling for startup hiring and scenario planning is a useful place to start.

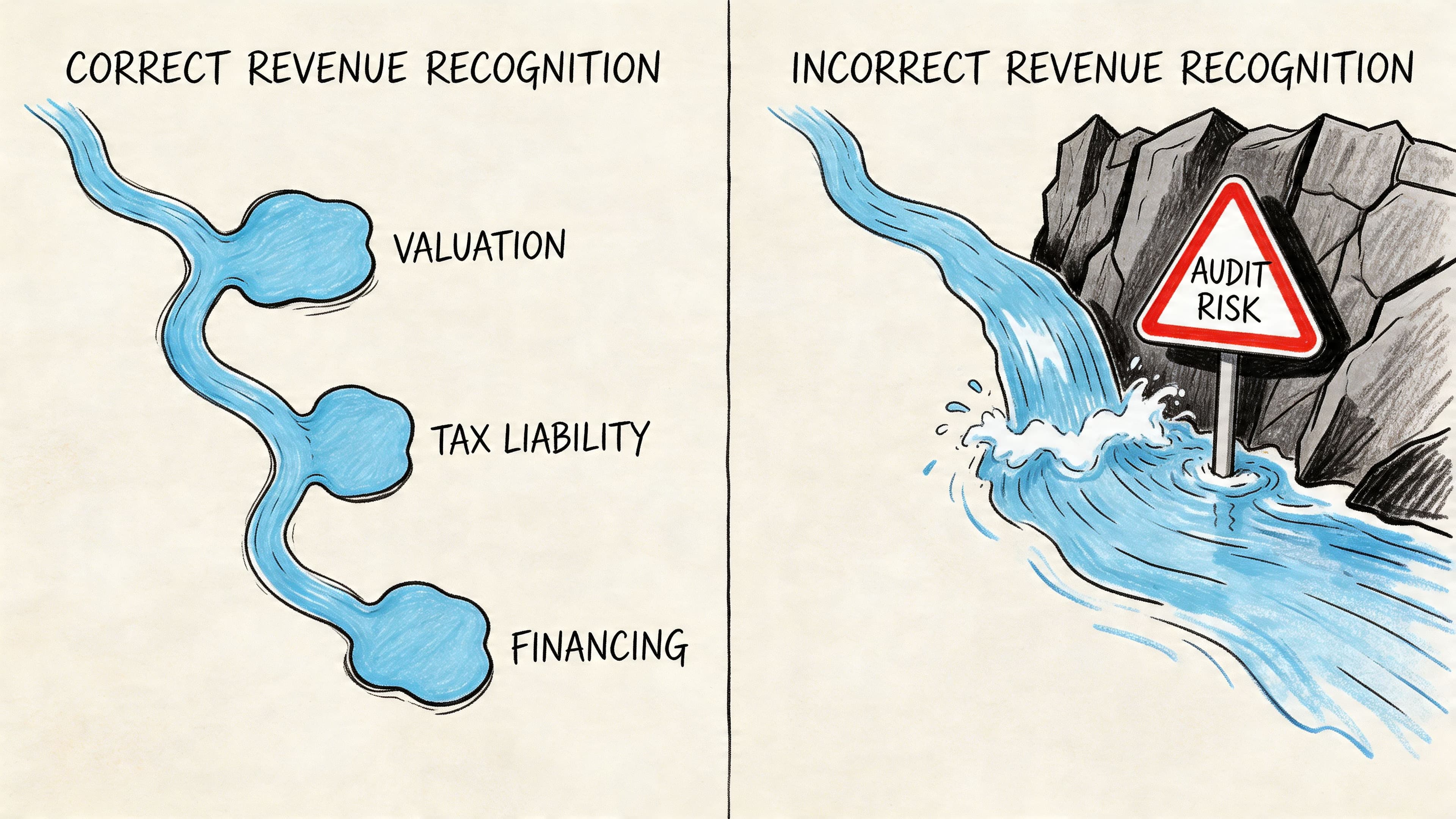

How to Recognize Revenue Correctly and Avoid Audit Risk

Revenue recognition errors are one of the fastest ways to make an agency look more profitable than it is. Then the correction hits. EBITDA drops, deferred revenue jumps, and any lender, buyer, or audit team starts asking harder questions.

Generic bookkeeping often stops being enough for agencies. Agencies between $500K and $20M usually have retainers, deposits, milestone billing, scope changes, contractor-heavy delivery, and partial-month work. If your books still treat invoicing as revenue, your financials are not decision-ready and they are definitely not diligence-ready.

The rule you need to follow

Under ASC 606, revenue is recognized when you satisfy a performance obligation. That means when the work is delivered based on the contract terms.

For agencies, the failure points are predictable:

| Revenue model | What founders book | What you should book |

|---|---|---|

| Monthly retainers | Full invoice to revenue on send date | Revenue over the service period |

| Time and materials | Revenue when billed | Revenue as hours are delivered |

| Fixed-fee milestone projects | Deposits and milestone invoices to revenue immediately | Revenue when each performance obligation is satisfied |

If your contract language is sloppy, your accounting will be sloppy too. You need clear deliverables, clear acceptance points, and a documented basis for how revenue moves from deferred to earned.

Worked example with a $50,000 project

Use a simple website engagement.

You sign a $50,000 contract with three milestones:

- Deposit at kickoff: $20,000

- Design approval milestone: $15,000

- Launch milestone: $15,000

Assume the contract states these are three distinct performance obligations. The client pays the $20,000 deposit before the first milestone is completed.

Step 1: Record the deposit as a liability

Cash received is not earned revenue if the related work is still outstanding.

Journal entry at cash receipt

- Debit Cash: $20,000

- Credit Deferred Revenue: $20,000

That deferred revenue balance matters. It tells you how much client work you still owe.

Step 2: Recognize revenue when the first milestone is complete

You complete the kickoff deliverable and the first performance obligation is satisfied. Now you can move the amount from the balance sheet to the P&L.

Journal entry when milestone one is completed

- Debit Deferred Revenue: $20,000

- Credit Project Revenue: $20,000

That is the point where revenue is earned.

Step 3: Bill and recognize the second milestone correctly

You reach design approval and issue the $15,000 invoice. If the milestone has already been satisfied, recognize the revenue at that point.

Journal entry at billing and recognition

- Debit Accounts Receivable: $15,000

- Credit Project Revenue: $15,000

If billing happens before delivery, the credit goes to Deferred Revenue first. Then it moves to revenue once the work is complete.

Step 4: Recognize the final milestone at launch

At launch, you invoice the last $15,000 and recognize it once the final deliverable is complete.

Total recognized revenue reaches $50,000 only after all three obligations are satisfied.

What the wrong method does to your numbers

The bad version is common:

- Collect $20,000 deposit and book revenue immediately

- Invoice $15,000 at design approval and book revenue immediately

- Invoice $15,000 at launch and book revenue immediately

That approach distorts the month the deposit lands. It usually overstates profit early, understates liabilities, and gives you fake margin in the periods where the work has not been delivered yet.

Then management uses those bad numbers to make real decisions. Founders hire too early. Pricing looks healthier than it is. Client profitability gets overstated. Forecasts become fiction.

Prepaid cash is a contract liability until your team earns it.

Retainers are where agencies slip most often

Retainers look simple, which is why agencies get them wrong.

If you invoice a monthly retainer in advance, recognize revenue across the service month. If the client prepays quarterly, spread it across the quarter as services are delivered. If work is paused, delayed, or materially reduced, your revenue timing may need to change with it. For agencies cleaning up this process, this guide to agency retainer accounting and recurring revenue tracking is a useful operating reference.

A short explainer helps if your team needs a visual on the concept:

The audit risk is not theoretical

Revenue recognition problems usually surface during one of four events:

- A bank asks for accrual-basis financials

- A buyer starts quality of earnings work

- An auditor tests contract timing

- Your own controller tries to explain why cash, revenue, and gross margin do not line up

At that point, cleanup is expensive. You have to rebuild contract schedules, restate prior months, and explain why management was using the wrong numbers. The work is tedious, but the bigger problem is credibility. Once a diligence team finds revenue timing errors, they start questioning everything else.

Common objections that do not hold up

- “We’re too small for ASC 606.” If you use deposits, retainers, milestone billing, or advance invoices, size is not the issue. Contract structure is.

- “Cash basis is simpler.” Simple is fine for tax prep. It is weak for margin analysis, forecasting, and lender or investor reporting.

- “Our CPA handles this at year-end.” Year-end cleanup does not fix eleven months of bad decisions.

Get this right and your P&L starts reflecting actual delivery performance. Get it wrong and every metric built on revenue, gross margin, utilization, client profitability, forecast accuracy, becomes less reliable. That is why agencies that want investor-ready financials have to move past basic bookkeeping and treat revenue recognition as an operating system, not a tax afterthought.

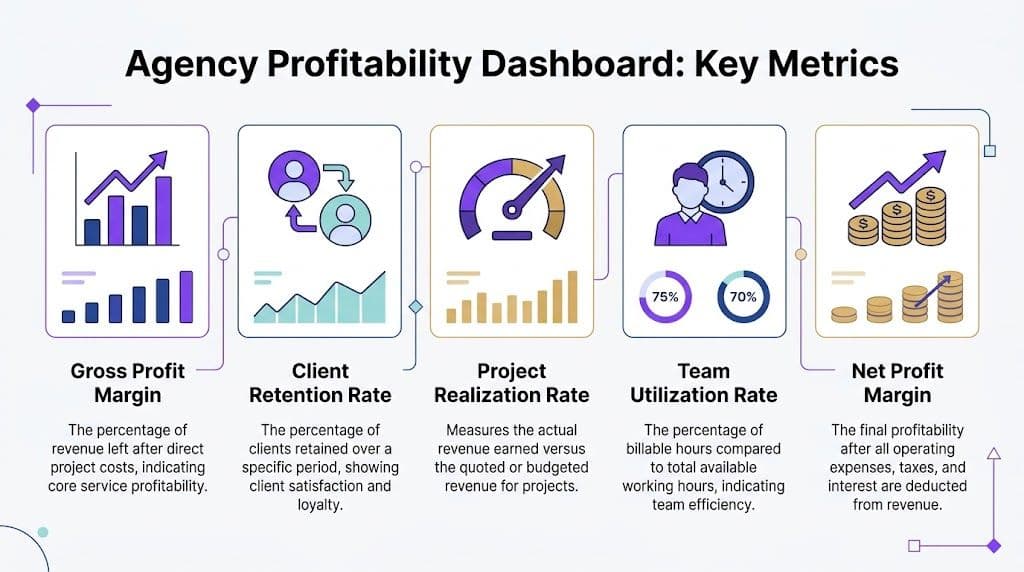

Your Agency's Profitability Dashboard What to Track

Agencies do not lose profit in one dramatic mistake. They lose it in small misses across pricing, staffing, scope control, and collections. If your dashboard does not expose those leaks quickly, it is decoration.

You need a short list of metrics that ties delivery performance to financial results. For agencies between $500K and $20M, the dashboard should answer five questions: What revenue is actually yours to keep? Are projects producing enough gross profit? Is team capacity being used well? Are you billing what you worked? Are clients paying on time?

Start with AGI and gross margin

Founders often look at top-line revenue first. That is a mistake. If a large share of that revenue passes straight through to media, freelancers, print, or production, it tells you very little about the strength of the agency.

Start with AGI, or adjusted gross income. Calculate it as gross revenue minus pass-through expenses. AGI is the revenue pool available to cover payroll, overhead, and profit. Without it, your margin analysis is distorted and your revenue-per-employee number is inflated.

Then track gross margin against AGI or service revenue, using the same method every month. The exact formula matters less than consistency, but the discipline matters a lot. If direct labor, contractor costs, and delivery software are not classified cleanly, your margin report will look stable right up until cash gets tight.

A simple example makes the point.

A project bills $30,000. Direct labor is $12,000. Contractor support is $2,500. Project-specific software and tools add $500. Gross profit is $15,000. Gross margin is 50%.

If unplanned revisions add another $4,000 of labor, gross profit drops to $11,000 and gross margin falls to 36.7%. Same client. Same invoice. Bad delivery economics.

Track the operating metrics that explain margin movement

Gross margin is an output. You need the inputs behind it.

Two of the most useful are utilization and realization. Function Point explains these benchmarks in its profitability reporting guide for agencies, including the commonly cited target ranges of 70 to 80 percent utilization and 80 to 90 percent realization for healthy agencies. Those ranges are not academic. Miss them for a few months and margin compression shows up fast.

Use this dashboard structure:

| KPI | How to calculate it | Why it matters |

|---|---|---|

| AGI | Gross Revenue minus Pass-Through Expenses | Shows the revenue that actually funds payroll, overhead, and profit |

| Gross Margin | Gross Profit divided by Revenue or AGI, whichever basis you use consistently | Tests whether delivery is producing enough profit before overhead |

| Utilization Rate | Billable Hours divided by Total Available Hours | Shows whether paid capacity is being converted into client work |

| Realization Rate | Billable Amount Invoiced divided by Billable Amount at Standard Rates, or billable hours invoiced divided by billable hours worked if that is how you price | Exposes write-downs, weak scoping, discounting, and over-servicing |

| AR Aging Review | Review aging buckets weekly | Flags collection risk before it turns into a payroll problem |

Read the metrics together, not in isolation

One metric rarely tells the truth on its own.

High utilization and low realization usually means your team is working hard on underpriced or poorly scoped accounts. Good gross margin with weak collections means the service model works, but billing and follow-up are lagging. Strong AGI with disappointing net income usually points to overhead creep, not a sales problem.

Investor-ready financials distinguish themselves from basic bookkeeping. A bookkeeper can tell you what happened in the general ledger. A controller should tell you why margin moved, which accounts caused it, and whether the problem sits in pricing, staffing, delivery, or cash conversion.

Disconnected systems make that impossible. If time tracking, project data, payroll, and invoicing do not agree, your dashboard will produce false confidence. Reconciliation is not clerical work. It is control. Teams that want tighter reporting often pair their dashboard process with automated bank reconciliation software so cash activity matches the books faster and exceptions get reviewed while they still matter.

If you want a practical model for presenting these numbers to leadership each month, use this guide to financial dashboards for CEOs and KPI tracking.

A weekly dashboard that is actually useful

Keep the operating review tight and decision-oriented:

- Client profitability: Which accounts dropped below target margin, and why?

- Capacity: Which teams are underloaded, and which are headed toward burnout or overruns?

- Realization: Where are write-offs, unapproved scope increases, and budget overruns accumulating?

- Collections: Which invoices need action this week to protect near-term cash?

- Trend view: Which metric has moved for three straight weeks and now needs a management decision?

That is enough. If a metric does not change a staffing move, pricing decision, client conversation, or cash action, it does not belong on the dashboard.

The 5-Day Month-End Close A Repeatable Process

Agencies that close the books late make decisions with stale numbers. That is how margin slips, payroll surprises hit cash, and founders miss revenue recognition errors that should have been caught days earlier.

A five-day close is the standard you should run. Not because it looks disciplined, but because agencies between $500K and $20M do not have the luxury of waiting two or three weeks to understand what happened last month. Client concentration and delayed collections can change your cash position fast. If your close drags, you will spot the problem after it has already affected hiring, vendor payments, or owner distributions.

The close process that works

Run the same cadence every month.

| Day | Primary focus | Output |

|---|---|---|

| Day 1 | Reconcile bank and credit card activity | Cash position confirmed |

| Day 2 | Post payroll accruals, contractor costs, and major vendor accruals | Direct costs captured in the correct period |

| Day 3 | Update deferred revenue and unbilled receivables schedules | Revenue tied to work performed |

| Day 4 | Review AR aging and AP obligations | Collection actions and cash timing decisions |

| Day 5 | Finalize P&L, balance sheet, and cash forecast | Management-ready reporting package |

That sequence matters. Cash first. Cutoff second. Revenue recognition third. Collections and forward cash view last.

What each day should include

- Reconcile cash first: If cash is wrong, the rest of the close is unreliable. High-volume teams often use automated bank reconciliation software to clear routine transactions quickly and isolate exceptions for review.

- Accrue what was incurred: Payroll, contractor work, media passthroughs, and major software costs belong in the month they were incurred. If you wait for bills to arrive, your project margins will be wrong.

- Update revenue schedules: Basic bookkeeping often proves inadequate for agencies regarding revenue schedules. Retainers, prepaid work, milestone billing, and unbilled work-in-process require a monthly ASC 606 review. Revenue should match performance, not invoice timing.

- Review AR with ownership: Aging reports do not collect cash. Assign every overdue invoice to an owner, set follow-up dates, and escalate disputed balances immediately.

- Build the forward cash view: Every close should update a rolling 13-week cash forecast so you can see pressure points before they become operating problems.

A fast close is a control system. It catches miscodings, missed accruals, duplicate expenses, revenue cut-off errors, and collection risk while the facts are still fresh.

Warning signs your close is broken

Use this checklist:

- You are still posting prior-month expenses after reports are issued

- Deferred revenue and unbilled revenue have not been updated this month

- Finance and project teams report different revenue totals

- AR aging exists, but no one owns collection follow-up

- The cash forecast is manually rebuilt from scratch every month

- Your P&L is final, but balance sheet accounts have not been reconciled

Those are not minor process gaps. They are control failures that produce unreliable financials.

If you want a cleaner structure for task ownership, deadlines, and review checkpoints, use this monthly close process framework for agencies.

Signs You've Outgrown In-House Bookkeeping

Agencies do not break financially all at once. They drift into bad reporting as complexity outruns the person entering transactions.

Once you move past basic monthly bookkeeping, the core issue is not effort. It is fit. An in-house bookkeeper can keep the ledger current and still leave you with the wrong answers for a service business that bills through retainers, milestones, prepaid work, media pass-through, contractor costs, and changing scopes. For agencies between $500K and $20M, that gap matters. This is the range where generic bookkeeping stops producing decision-ready numbers and starts creating rework, margin confusion, and audit exposure.

A practical sign is transaction load. As firms scale, monthly transaction counts rise sharply, especially once payroll, AP, contractor payments, software subscriptions, reimbursable spend, and client billing all stack up. Industry operators have documented agency finance systems expanding from roughly 100 monthly transactions at smaller firms to more than 2,000 at larger ones, as outlined in this agency accounting operations review. At that volume, a basic bookkeeper usually becomes a bottleneck.

Red flags founders should take seriously

You have outgrown in-house bookkeeping if any of these show up consistently:

- Your financials arrive after the decisions are already made: Late reports do not help you price work, control hiring, or manage cash. They only confirm what already happened.

- Project profitability lives outside the accounting system: If margin depends on spreadsheet stitching, you do not have a finance system. You have a manual workaround.

- Time tracking, payroll, and invoicing do not tie together: That creates missed billings, understated delivery costs, and false confidence in account profitability.

- Revenue recognition depends on memory: If retainers, deposits, prepaid work, and milestone invoices are handled differently each month, your revenue numbers are unreliable.

- You are still translating the numbers for your own finance staff: Founder interpretation is a control failure. Finance should explain the business back to you, not the other way around.

What a stronger finance setup should give you

A real finance function does more than code transactions.

It should give you clean monthly reporting, revenue recognition that matches how work is delivered, and client economics you can trust. It should also give you a balance sheet that is reviewed, not ignored while everyone stares at the P&L.

| Capability | What it means in practice |

|---|---|

| Accurate monthly close | You get timely P&L, balance sheet, and cash reporting |

| Revenue recognition discipline | Retainers, deposits, and milestones are booked correctly |

| Project and client visibility | Margin reporting ties to time, labor, and invoicing data |

| Cash forecasting | You can see risks before they hit payroll timing |

| Controller-level insight | Someone explains the numbers and pushes decisions forward |

That last point matters most. Bookkeeping records activity. Controller oversight catches misstatements, defines policy, and turns reports into operating decisions.

The common founder mistake

Founders often say, “We’re not big enough for a controller.”

That framing costs money. You do not buy controller support for status. You buy it to protect margin, shorten the close, fix revenue recognition, and get numbers you can use in lender, buyer, or investor conversations.

If your agency has multiple service lines, meaningful payroll, project-based delivery, contractor dependence, or plans to raise capital, transaction entry is not enough. You need financials built for agency economics, not generic small-business bookkeeping.

How to choose an outsourced partner

Start with three filters.

- Agency-specific expertise: They should understand AGI, pass-through spend, utilization, realization, unbilled work, and deferred revenue.

- System fluency: They should know the tools already running your operation, including your accounting platform, payroll system, time tracker, and project management stack.

- Controller capability: Reporting alone is insufficient. You need someone who can define close procedures, review reconciliations, enforce revenue policy, and explain the financial consequences of what changed.

Outsourced controller support is often the right next step. Firms such as Jumpstart Partners provide bookkeeping and controller services for agencies in the $500K to $20M range, including faster close cycles, cash visibility, and ASC 606-oriented reporting workflows. That is the level of finance support growing agencies usually need.

Upgrade the finance function before reporting failures start shaping strategy.