Financial Operations

Financial Modeling for Startups: An Investor-Ready Guide

Master financial modeling for startups with our step-by-step guide. Build an investor-ready model covering SaaS/agency revenue, expenses, and cash flow.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readMost startup models fail before investors ever see them. They fail because they are built as presentation decks, not operating systems.

The hard reality is simple. 82% of startups fail primarily because they run out of cash or mismanage cash flow, according to Capidel’s guide to startup financial modeling. If your model does not tell you when cash gets tight, what assumptions drive the shortfall, and what operational changes fix it, it is not a financial model. It is decoration.

For founders between $500K and $20M in revenue, financial modeling for startups should do three jobs at once. It should help you run the business, defend your plan to investors, and expose the mistakes that kill runway. That means a driver-based model, connected financial statements, real scenario planning, and clean treatment of revenue recognition if you sell subscriptions or long-term service contracts.

If you are building from a generic template, stop copying and start thinking like an operator. Investors do not fund spreadsheets. They fund teams that understand what moves revenue, margins, and cash.

Why Your Financial Model Is Your Startup’s Lifeline

A startup dies from lack of cash long before it dies from lack of ambition. That is why financial modeling for startups belongs at the center of your operating rhythm, not buried in a fundraising folder.

A model is not a budget spreadsheet

Most founders start with revenue at the top, expenses underneath, and a hopeful ending. That is not enough.

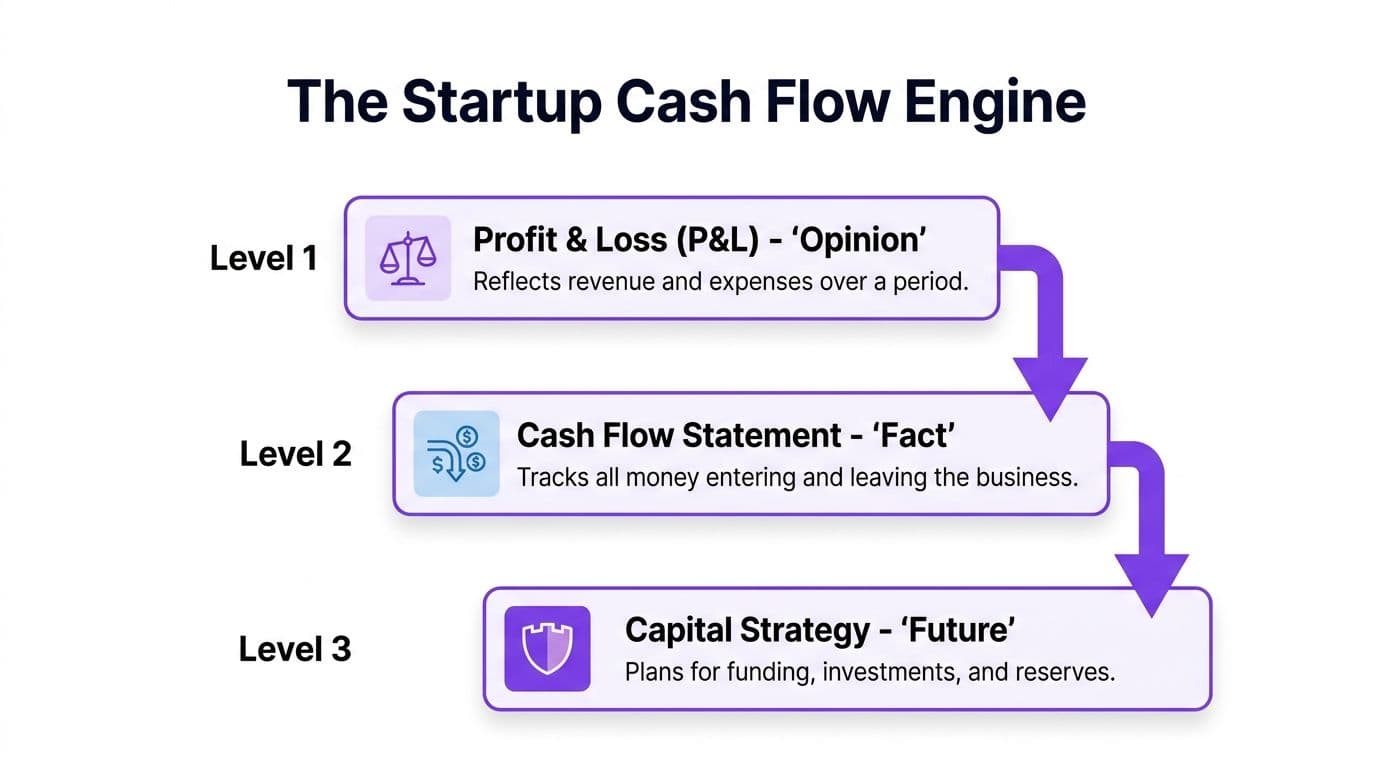

A real model connects three statements:

| Statement | What it tells you | Why it matters |

|---|---|---|

| P&L | Revenue, costs, and profit over time | Shows whether the business model works |

| Balance Sheet | What you own, owe, and retain | Shows financial position, deferred revenue, and funding effects |

| Cash Flow Statement | Actual movement of cash in and out | Shows whether you survive |

If these three statements do not talk to each other, your forecast is unreliable. You can show profit on a P&L and still run out of cash because receivables lag, deferred revenue is mishandled, or hiring outpaces collections.

Investors look for coherence, not optimism

An investor-ready model tells a clean story. The story is not “we are going to grow fast.” The story is “these are the operating drivers, this is how they produce revenue, this is what they cost, this is how cash behaves, and this is when we need capital.”

That is why driver-based forecasts outperform top-down narratives. You need a model that traces results back to real operating inputs such as pipeline conversion, sales capacity, utilization, churn, pricing, collections, and headcount timing.

Practical standard: If you cannot explain every major line item in your model in one sentence, your model is too vague to manage and too weak to fund.

Your model should change how you run the company

A useful model changes decisions now. It tells you whether to slow hiring, tighten collections, change pricing, or raise capital earlier.

It also creates discipline around reporting. For founders who need a stronger planning baseline before building the full model, this startup financial forecasting guide is a good operational complement.

The point is simple. Your model is not an accounting exercise. It is the document that tells you whether your growth plan is financeable.

Laying the Foundation with Assumptions and Drivers

Bad assumptions create fake confidence. Good assumptions create a model you can defend under pressure.

Start with drivers, not outputs

Founders often begin by choosing a revenue target and backfilling the spreadsheet. Investors can spot that immediately.

A solid model starts with the activities that cause revenue:

- Lead generation: Website traffic, outbound volume, referrals, partner-sourced opportunities

- Conversion: Lead-to-demo, demo-to-proposal, proposal-to-close

- Pricing: Contract value, package mix, discounting, expansion

- Retention: Churn, downgrades, renewals

- Delivery capacity: Team utilization, billable hours, account load, implementation bandwidth

These are drivers. Revenue is the result.

For SaaS, investors want driver-based revenue forecasts tied to unit economics, and they watch benchmarks like LTV/CAC above 3:1, monthly churn below 5 to 7 percent for early-stage SaaS, and gross margins of 70 to 80 percent, according to Macabacus on startup financial modeling.

Build your SaaS assumptions from the funnel

Here is the right sequence:

- Start with leads.

- Apply conversion rates.

- Estimate new customers.

- Multiply by average subscription value.

- Adjust for churn and expansion.

That structure gives you a forecast investors can interrogate and still trust.

A simple example:

- Leads = 200

- Lead-to-customer conversion = 5%

- New customers = 10

- Average monthly subscription = $1,000

- New MRR added = $10,000

That example is not complex, but it is defendable. It also lets you test what matters. If conversion weaken...

Unit economics are where optimism gets tested

Founders are exposed when growth lacks sound unit economics. Growth without sound unit economics is just expensive motion.

Jason Lemkin put it clearly at SaaStr: “Unit economics are the truth serum for SaaS businesses. You can have beautiful growth charts and impressive MRR, but if you're spending $15,000 to acquire customers who only generate $12,000 in lifetime value, you are a cash-burning machine.”

That quote should sit next to your model.

If you need a deeper operating framework for this layer, this explanation of unit economics is worth using alongside your forecast build.

Key discipline: Every growth assumption should have a matching cost assumption. More leads usually mean more marketing spend. More customers usually mean more support, implementation, or onboarding load.

Agency and services models need different drivers

Agencies and professional services firms make a common mistake. They copy SaaS logic and forget that delivery capacity drives revenue.

Your core drivers usually look more like this:

| Driver | Why it matters | Common failure |

|---|---|---|

| Utilization | Determines how much of team capacity is billable | Hiring ahead of demand |

| Average bill rate | Drives gross margin and positioning | Underpricing senior work |

| Client mix | Retainers are steadier than project work | Overreliance on one-off projects |

| Collection timing | Cash inflow depends on invoicing discipline | Letting receivables drift |

If you run a service business, model capacity before you model growth. Revenue does not happen because you want it. It happens because the team can deliver it at an acceptable margin.

Use assumptions you can update monthly

The best model is not the most complex one. It is the one you can revise quickly when reality changes.

Color-code inputs. Keep assumptions in one place. Separate historicals from forecast periods. Build formulas that flow from operational reality, not investor wishful thinking.

If your assumptions live in your head, your model is broken.

Building Your Revenue and Expense Schedules

Investors stop trusting a model the moment revenue and expenses look smoothed, averaged, or disconnected from how the business operates.

This section is where a startup model either becomes decision-grade or turns into fundraising theater.

Build SaaS revenue from MRR movements, then separate bookings from recognized revenue

For SaaS, start with an MRR bridge. Do not start with an annual growth rate and work backward. Investors want to see the mechanics of growth.

A clean monthly structure looks like this:

| SaaS revenue driver | Example input |

|---|---|

| Beginning MRR | $80,000 |

| New MRR | $12,000 |

| Expansion MRR | $4,000 |

| Churned MRR | ($5,000) |

| Ending MRR | $91,000 |

Then carry ending MRR into the next month.

Here is the calculation:

- Beginning MRR = $80,000

- New customers = 8

- Average new subscription = $1,500

- New MRR = 8 × $1,500 = $12,000

- Expansion from current accounts = $4,000

- Churned revenue = $5,000

- Ending MRR = $80,000 + $12,000 + $4,000 - $5,000 = $91,000

That implies ARR of $1,092,000 based on ending MRR.

Good founders stop there. Strong founders add the second layer investors care about: bookings, billings, recognized revenue, and cash. If those four lines are merged into one, your SaaS model will fail diligence.

Model agency revenue from delivery capacity, not optimism

Agency and services businesses need a different revenue spine. Your top line is constrained by labor capacity, utilization, pricing, and contract mix.

Use a capacity-based build:

- Team member monthly capacity = 160 hours

- Utilization = 75%

- Billable hours = 120

- Average bill rate = $150

- Monthly revenue per billable team member = $18,000

Multiply that by delivery headcount. Then adjust for management time, ramp time for new hires, write-offs, discounts, and any pass-through revenue.

That last part matters. Pass-through revenue can inflate the top line while doing very little for gross profit. If your agency model does not isolate it, your margins will look healthier than they are.

Retainers should be modeled separately from project work. They behave differently, renew differently, and create different cash timing.

ASC 606 belongs inside the schedule, not in a footnote

Generic startup templates usually gloss over revenue recognition. That is a mistake.

If you sell annual SaaS contracts, multi-month retainers, implementation packages, or milestone-based work, ASC 606 changes the shape of your model. You need separate lines for contract value, invoicing, cash collection, recognized revenue, and deferred revenue. That is what investors expect when they review a model for a software or hybrid software-services company.

A simple SaaS example makes the point.

Assume a customer prepays $24,000 for a two-year contract.

- Cash received upfront: $24,000

- Recognized monthly revenue: $1,000

- Deferred revenue at contract start: $24,000

- After one month, recognized revenue is $1,000 and deferred revenue is $23,000

If you record the full $24,000 as current revenue, your P&L is wrong, your MRR is overstated, and your balance sheet no longer reconciles. A serious investor or lender will catch that quickly.

The same issue shows up in agencies. If you invoice an upfront strategy fee, collect a retainer before work is delivered, or bill against milestones, cash does not equal revenue. Build the schedule so the accounting treatment is visible month by month.

One warning sign is obvious. If bookings, billings, recognized revenue, and cash all rise in perfect sync, the model is probably wrong.

Benchmark the output, but do not reverse-engineer the answer

Founders often force their model to hit “good” SaaS metrics. Investors can tell.

Use benchmark ranges as a reasonableness check after the schedule is built:

| Metric | Seed Stage (<$1M ARR) | Series A ($1M - $5M ARR) | Growth Stage ($5M+ ARR) | |---|---|---| | LTV/CAC | Work toward above 3:1 | Above 3:1 is expected | Sustain above 3:1 while scaling | | Monthly churn | Keep below 5-7% for early-stage SaaS | Tighten retention as cohorts mature | Demonstrate durable retention | | Gross margin | Move toward 70-80% | 70-80% signals scalability | Protect margin during expansion |

If your model only “works” because churn is unrealistically low or CAC stays flat while growth accelerates, fix the operating assumptions. Do not polish the output.

Build expenses from hiring plans, vendor logic, and margin reality

The expense schedule needs the same level of detail as revenue.

Start with payroll. Build it by role, start date, base salary, payroll taxes, commissions, bonuses, and benefits. A single annual salary bucket spread evenly across the year is not acceptable. Hiring timing drives burn, cash runway, and execution risk. It also drives dilution once you connect this model to your financing plan and cap table.

Then build the rest of the cost base:

| Expense area | What to model |

|---|---|

| Payroll | Role, start month, salary, payroll taxes, benefits |

| Marketing | Channel spend tied to pipeline or lead assumptions |

| Software | Per-seat tools and fixed platform costs |

| G&A | Insurance, legal, accounting, rent, admin costs |

| Cost of service or support | Delivery labor, contractors, onboarding, hosting |

Tie each line to an operating driver. Sales commissions should follow bookings. Hosting should track usage or customer count. Software seats should rise with headcount. Contractor spend should flex with delivery load, not grow by a flat percentage every year.

For founders refining the top-line build, this sales projections template for growing companies is a useful cross-check for how revenue assumptions should flow into the rest of the model.

Make the schedules answer investor questions fast

A good schedule does more than total up revenue and expenses. It explains what has to go right.

You should be able to answer these questions in seconds:

- Which revenue line drives growth: new logos, expansion, retainers, or project work?

- How much recognized revenue is backed by deferred revenue?

- Which hires are ahead of demand, and which are triggered by demand?

- What happens to gross margin if utilization drops or churn rises?

- How does a slower collection cycle change operating cash needs?

- How much extra capital will you need, and how much dilution follows if the hiring plan stays fixed while revenue slips?

That last question gets ignored in generic templates. It should not. A model that connects revenue timing, expense timing, ASC 606 treatment, and financing impact gives founders a much clearer view of what growth costs.

If your schedule cannot answer those questions, rebuild it before you show it to a board, lender, or investor.

Forecasting Cash Flow and Your Capital Strategy

Cash shortfalls kill startups faster than weak margins. Your model needs to show the exact month cash gets tight, why it happens, and what financing decision fixes it.

The cash flow statement turns a growth plan into an operating reality. It forces your revenue timing, expense timing, collections, payables, financing, and ASC 606 treatment to reconcile with the bank balance.

Why net income is not cash

Founders who only manage the P&L often get surprised here.

A startup can post healthy recognized revenue and still run into a cash crunch because profit and cash move on different schedules. That gap gets wider in SaaS and agency models, where billing terms, implementation work, retainers, annual prepayments, and deferred revenue all distort the timing.

Cash changes for a few predictable reasons:

- Receivables delays: Revenue is recognized before the customer pays.

- Deferred revenue: Cash is collected before revenue is recognized under ASC 606.

- Non-cash items: Depreciation, amortization, and stock-based compensation affect profit without changing cash.

- Financing activity: Debt and equity increase cash without appearing in operating revenue.

If your model stops at the income statement, it misses the question investors care about. How much cash does growth consume before it starts to fund itself?

Build the operating cash view before the full statement

Start with net income. Then adjust for non-cash items and working capital.

For a simple monthly example:

- Net income of $10,000

- Accounts receivable increase of $15,000

- Deferred revenue increase of $8,000

Operating cash flow is not $10,000. The AR build uses cash. The deferred revenue balance adds cash. The result depends on collection timing and contract structure, not just on reported profit.

That is why a long-range model is not enough. Pair it with a weekly cash tool. A 13-week cash flow forecast for startup cash planning gives you the operating view you need when payroll, vendor payments, and customer collections start slipping against plan.

Operator rule: Review cash weekly when hiring is ramping, collections are stretching, or large annual contracts are distorting recognized revenue versus cash received.

A short explainer on this relationship is worth watching before you finalize your build:

Burn rate and runway shape your fundraising options

Your capital plan should produce two outputs every month:

- Burn rate

- Runway

Do not bury them on a summary tab. Put them in plain view.

A basic runway calculation looks like this:

- Cash on hand = $1,200,000

- Monthly burn = $100,000

- Runway = 12 months

That number drives your negotiating position with investors. If runway drops below the time required to hit the next meaningful milestone, product launch, revenue scale, margin improvement, or a clean retention story, you are raising from weakness.

Use gross burn and net burn. Gross burn tells you how expensive the operating machine is. Net burn shows how quickly cash leaves after revenue collections. Investors will ask for both, and they should.

Model financing and dilution in the same file

Many founders treat fundraising as a single line item called “cash in.” That is amateur modeling.

Your model should connect the raise to ownership, timing, and future runway in one place. At minimum, include:

- Pre-money and post-money ownership

- New shares issued

- Option pool expansion

- Founder dilution

- Cash added from the round

- Runway extension after the raise

This matters even more in SaaS and agency businesses with uneven cash conversion. A company can look healthy on recognized revenue, close a round, and still create a weak financing outcome because the raise came too late, priced too low, or assumed a hiring plan the cash profile cannot support.

Build the cap table directly into the cash model. Then test the raise against milestone timing. If the company needs another round before reaching the next investor-proof stage, the dilution math is already telling you the strategy is wrong.

Some teams use Excel. Others use equity software. The tool does not matter. The link between cash planning, ASC 606 revenue timing, and cap table impact does.

One option for teams that need the accounting, close process, and model maintenance aligned is Jumpstart Partners, which provides outsourced controller support, investor-ready reporting, and cash flow visibility for businesses in the $500K to $20M range. That is useful when fundraising, revenue recognition, and operational reporting all need to connect cleanly.

Your model should answer one blunt question without cleanup or interpretation: on the current plan, when does cash hit zero? That date should set your fundraising timeline.

Validating Your Model with Scenarios and KPIs

A startup that misses plan by a few points on conversion, churn, or collections can burn months of runway without changing its headline growth story. That is why scenario testing matters. It shows whether the business still works when the assumptions investors will challenge start to move.

Pick the few variables that matter

Build three cases. Base, upside, and downside.

Anything more usually hides the answer instead of improving it. The point is to pressure-test the handful of drivers that can change cash, growth quality, and fundraising timing.

For most startups, those drivers are:

| Scenario driver | Why it matters |

|---|---|

| Sales conversion | Changes new customer volume and pipeline efficiency |

| Churn or retention | Reshapes recurring revenue and lifetime value |

| Hiring pace | Pulls payroll, onboarding costs, and burn forward |

| Collections timing | Changes cash arrival even when booked revenue looks strong |

| Gross margin | Determines whether growth improves cash generation or increases strain |

For SaaS, test new bookings, retention, expansion, and implementation timing. Then check how ASC 606 changes the pattern of recognized revenue versus billed cash. A business can post stable revenue while collections soften or deferred revenue reverses. Investors will catch that mismatch quickly.

For agencies, pressure-test utilization, billable rates, client concentration, and payment terms. Agency models fail when founders forecast recognized revenue cleanly but ignore how slow-paying clients distort cash.

Watch for the mistakes that kill credibility

Weak models usually fail in predictable ways. Founders overstate how quickly demand converts. They keep assumptions flat as the company scales. They treat revenue as cash. They ignore contract structure, deferred revenue, and collections timing until the runway suddenly shortens.

Those are operating mistakes, not spreadsheet mistakes.

Red flags

- Top-down market capture: The model starts with market size instead of sales capacity, deal flow, and conversion.

- No balance sheet logic: Accounts receivable, deferred revenue, prepaid expenses, and accrued liabilities do not move with growth.

- Static operating assumptions: Conversion, retention, utilization, and gross margin stay unrealistically steady at every scale.

- No true downside case: The plan only holds if hiring lands on time, sales efficiency improves, and churn stays contained.

- KPI clutter: The dashboard tracks activity but misses efficiency, cash durability, and revenue quality.

If one assumption changes, the impact should flow through revenue, expenses, cash, and runway in the same model.

That standard matters even more if you are fundraising. Investors do not want a forecast that only explains the upside. They want to see what breaks, when it breaks, and whether management understands the fix. Use a short financial due diligence checklist for startup fundraising and reporting to test whether the model holds up under scrutiny.

Build a one-page dashboard investors can scan quickly

Your KPI page should translate the model into operating signal. It should not read like a monthly close package.

For SaaS, track:

- MRR and ARR trend

- Gross and net revenue retention

- CAC payback

- LTV/CAC

- Gross margin

- Burn multiple

- Runway

For agencies and services firms, track:

- Monthly revenue trend

- Gross margin by service line

- Utilization

- Average bill rate

- DSO or collections timing

- Backlog or contracted revenue

- Runway or liquidity

Keep the dashboard tied to the model. If churn worsens, net revenue retention should move. If enterprise deals close with annual prepayments, deferred revenue and cash should move. If hiring ramps ahead of delivery capacity in an agency, utilization and margin should show the hit.

That is what makes the model credible. The KPIs do not sit beside the forecast. They prove the forecast is built on operating reality.

From Model to Action Your Path to Investor Readiness

A startup model is only valuable if you use it to make decisions. That means updating it, reconciling it to actuals, and forcing tradeoffs through it before the market forces them on you.

What you should do next

Start with the basics and do them well:

- Build a driver-based forecast tied to how your business sells and delivers.

- Connect the P&L, balance sheet, and cash flow statement.

- Model revenue recognition correctly if you have subscriptions, retainers, or multi-period contracts.

- Add scenarios that test the assumptions most likely to fail.

- Track a short KPI dashboard that management and investors can read in minutes.

If you are preparing for diligence, board review, or fundraising, your next step is not more spreadsheet tabs. It is cleanup.

Use a checklist. Reconcile historicals. Check deferred revenue. Review collections timing. Make sure the cap table and cash model agree. If you need a structured place to start, this financial due diligence checklist is the right next document to work through.

Common objection you should ignore

A lot of founders say they are too early for a real model.

That is backward.

Early-stage companies need stronger modeling because small mistakes hit cash faster, hiring decisions are less forgiving, and investor confidence is more sensitive to inconsistency. You do not need a huge finance team. You need a disciplined model and someone accountable for keeping it honest.

What investor-ready looks like

Investor-ready does not mean polished charts and aggressive revenue ramps.

It means your model can answer hard questions without collapsing:

- Why will churn stay inside your expected range?

- What happens to cash if hiring starts earlier?

- How does deferred revenue move if customers prepay?

- When does the business need new capital?

- What milestone does the next round fund?

If you cannot answer those questions clearly, fix the model before you start the roadshow.

A good financial model gets you funded. A disciplined modeling process helps you stay alive long enough to deserve the funding.

If you want help turning your forecast into an investor-ready operating model, talk to Jumpstart Partners. Their team supports SaaS, agencies, and other growing businesses with controller services, ASC 606 workflows, cash flow reporting, and investor-ready financials so founders can spend less time fixing spreadsheets and more time managing growth.