Financial Operations

Fractional Controller Services the Complete CEO's Guide

Explore fractional controller services for businesses earning $500K-$20M. Learn about costs, ROI, deliverables, and how to hire the right finance partner.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readYou don't hire a fractional controller because “finance is important.” You hire one because the numbers have started blocking decisions. Payroll goes out, customers pay, revenue grows, and yet your reporting still feels unstable. You can't tell whether margin slipped because of hiring, pricing, delivery creep, revenue recognition, or plain old bookkeeping errors.

That's the point where basic bookkeeping stops being enough. A full-time controller can cost upwards of $150,000 annually, which is why many growing companies turn to a fractional model instead for the same level of expertise without a full-time executive salary, as noted by Enkel's overview of fractional CFO and controller services. For a business in the $500K to $20M range, that gap matters. You need clean closes, reliable reports, and cash visibility. You don't necessarily need another full-time salary on the org chart.

A good controller doesn't just “keep the books clean.” They build the financial operating system that lets you trust what you're seeing and act on it quickly.

Table of Contents

- When DIY Finance Starts Breaking Your Business

- The Fractional Controller's Core Deliverables

- Controller vs CFO vs Bookkeeper A Clear Comparison

- Who Benefits Most from Fractional Controller Services

- The ROI of a Fractional Controller A Cost-Benefit Analysis

- Your Vendor Selection Checklist

- Your Action Plan for Onboarding and Success

When DIY Finance Starts Breaking Your Business

The first sign usually isn't a compliance issue. It's hesitation.

You're in a leadership meeting and someone asks a basic question. Why did cash drop last month? Are we profitable on that service line? Why doesn't the P&L tie to what we thought happened operationally? Nobody gives a clean answer. Your bookkeeper did the work they were hired to do, but the business has become more complex than transaction entry and month-end categorization.

That's when DIY finance starts creating real business risk. The problem isn't just messy books. The problem is delay. Delay in closing the month. Delay in seeing margin shifts. Delay in catching accrual issues, payroll coding errors, duplicate spend, revenue timing problems, and reconciliation gaps. Delay is expensive because you keep making operating decisions with stale information.

Practical rule: If you trust your bank balance more than your financial statements, you've outgrown basic bookkeeping.

This happens a lot in founder-led businesses. Revenue grows, hiring accelerates, software spend expands, and customer contracts get more nuanced. Suddenly your financial stack needs more than “someone to keep QuickBooks updated.” You need a finance operator who can sit between the details and the decisions.

A full-time in-house controller often isn't the right answer yet. The cost alone filters many businesses out. This breakdown of signs you've outgrown your bookkeeper is useful because it captures the exact inflection point many companies hit before they're ready for a permanent finance leader.

What the failure pattern looks like

A founder usually describes the same cluster of issues:

- Reports arrive late: You get month-end numbers after the next month is already underway.

- Cash feels unpredictable: Revenue is coming in, but timing problems keep surprising you.

- Management reporting is weak: You have a P&L, but no useful explanation behind the changes.

- Board or lender requests create stress: Basic diligence turns into a scramble.

- Your team spends time arguing about numbers: Sales, operations, and finance each have different versions of reality.

The answer isn't more spreadsheet heroics from the CEO. It's structured financial oversight.

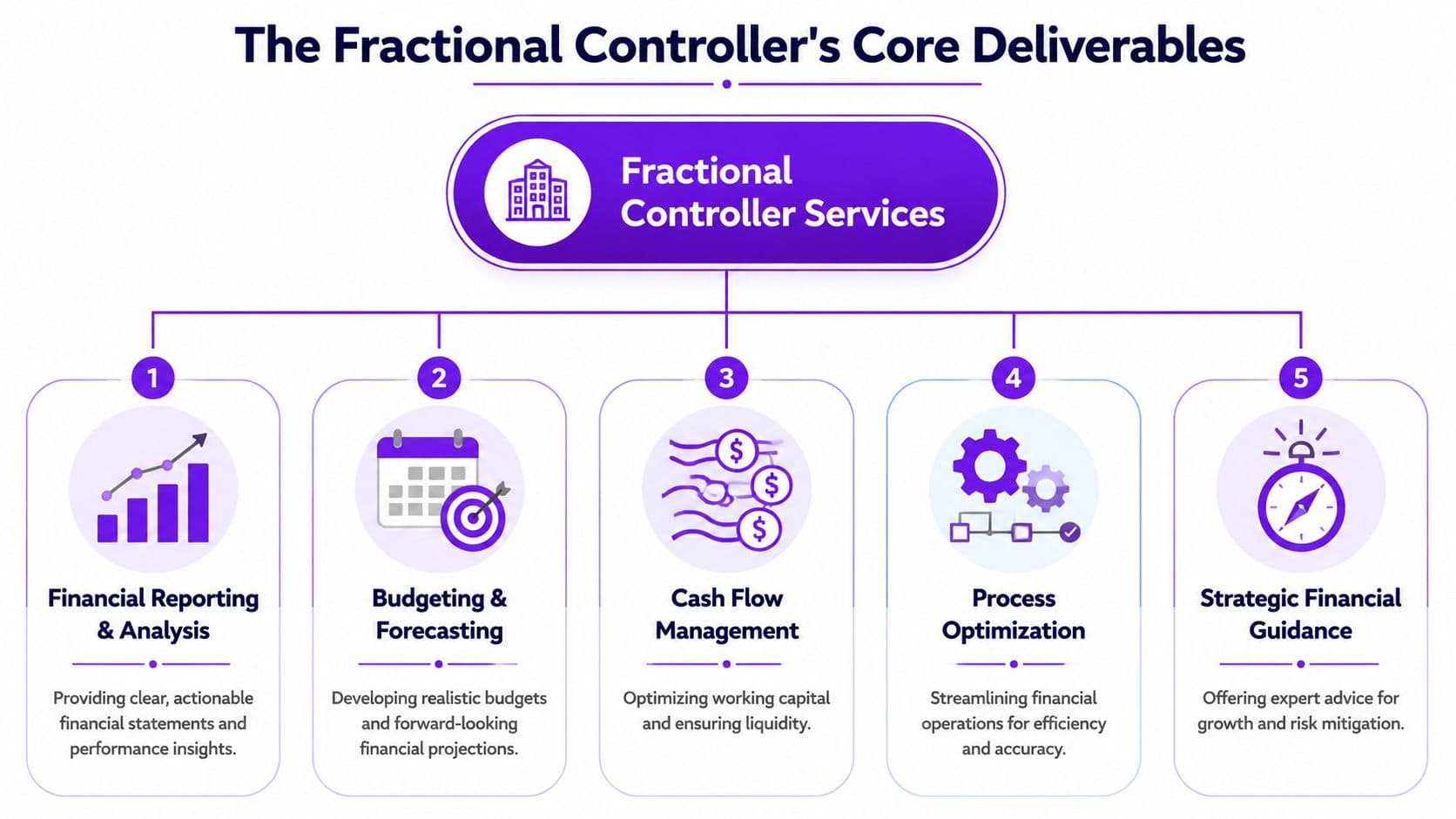

The Fractional Controller's Core Deliverables

A fractional controller earns their keep by turning accounting output into management infrastructure. The role sits between bookkeeping and CFO-level strategy. The controller owns the close, reporting, reconciliations, cash tracking, budget oversight, and process improvements that make financial data timely and usable, as described in Rework Capital's explanation of fractional controller services.

Close process and reporting discipline

The first deliverable is a controlled month-end close. That means the bank accounts reconcile, credit cards reconcile, payroll entries post correctly, accounts receivable and accounts payable are reviewed, and the general ledger reflects what happened.

Without that, every report built afterward is shaky.

The second deliverable is management reporting. Not just a P&L export. You should expect:

- A clean profit and loss statement: Organized to show how the business runs

- A balance sheet you can defend: Not a dumping ground for unreconciled accounts

- A cash flow view: So you can connect accounting profit to liquidity

- Variance analysis: Clear commentary on what changed and why

If you're preparing for fundraising, lending, acquisition review, or partner reporting, a controller also helps you produce the supporting schedules behind the statements. That's where a practical resource like this financial due diligence checklist becomes useful. It shows the level of documentation outside parties usually expect long before a founder thinks they need it.

Cash forecasting that you can actually use

Cash flow forecasting is where a strong controller becomes immediately valuable to a CEO. Most businesses don't fail because the P&L looks bad. They fail because cash timing surprises them.

A simple 13-week cash flow forecast gives you a forward view of liquidity. It doesn't need to be fancy. It needs to be updated, grounded in real collections and payment timing, and tied to operating decisions.

Sample 13-Week Cash Flow Forecast Calculation

| Week | Beginning Cash | Cash In (A/R, Sales) | Cash Out (Payroll, Rent, A/P) | Ending Cash |

|---|---|---|---|---|

| Week 1 | $85,000 | $22,000 | $31,000 | $76,000 |

| Week 2 | $76,000 | $18,000 | $27,000 | $67,000 |

| Week 3 | $67,000 | $40,000 | $29,000 | $78,000 |

| Week 4 | $78,000 | $24,000 | $33,000 | $69,000 |

In this example, the math is simple. Ending Cash = Beginning Cash + Cash In - Cash Out. But the insight matters more than the arithmetic. Week 2 shows tightening liquidity. Week 3 only improves because collections spike. If those receivables slip, your cash position changes immediately.

A forecast is only useful if someone owns the assumptions behind collections, payroll timing, vendor payments, and deferred expenses.

For founders who want a more detailed explanation of where this work sits operationally, what a controller actually does is a good companion read.

Controls systems and technical accounting

A fractional controller also improves the machinery behind the numbers.

Independent advisory guidance notes that fractional controllers often implement scalable systems connecting finance, sales, payroll, and CRM tools, while improving reporting accuracy and compliance discipline. The same guidance says these arrangements can reduce the cost of full-time finance leadership by an estimated 40% to 60%, according to Optima Office's review of fractional controller support.

That work usually includes:

- System integration: Connecting tools like QuickBooks, Xero, NetSuite, Stripe, Gusto, Shopify, HubSpot, or Salesforce so data moves cleanly

- Control design: Setting approval flows, close checklists, and reconciliation procedures

- Technical accounting: Handling issues like deferred revenue, prepaid expenses, accruals, and contract timing correctly

- Bookkeeping oversight: Making sure day-to-day entry supports decision-grade reporting rather than just tax prep

This is the part many founders underestimate. Better reporting doesn't come from prettier dashboards. It comes from disciplined accounting underneath them.

Controller vs CFO vs Bookkeeper A Clear Comparison

Most finance hiring mistakes come from role confusion. Founders hire too junior, then wonder why nobody fixes reporting. Or they hire too senior, then pay strategy rates for cleanup work that should have been solved first.

The cleanest way to think about it is this. A bookkeeper records the past. A controller manages the present. A CFO shapes the future.

Finance Roles at a Glance

| Role | Focus | Key Tasks | Typical Full-Time Cost |

|---|---|---|---|

| Bookkeeper | Transaction accuracy | Categorizing expenses, invoicing, bill pay, routine entries, bank and card posting | Varies by market and scope |

| Controller | Financial control and reporting | Month-end close, reconciliations, reporting, cash tracking, controls, budget oversight, bookkeeping supervision | Full-time controller roles can cost upwards of $150,000 annually, as noted earlier |

| CFO | Strategic finance leadership | Capital planning, board communication, fundraising support, scenario modeling, financing strategy, long-range planning | Often higher than controller compensation |

That distinction matters operationally.

A bookkeeper can keep your records current. They usually won't redesign the close process, review the integrity of the balance sheet, or establish reporting standards for leadership. A CFO can set direction, but if the underlying accounting is weak, the strategy rests on bad inputs.

That leaves the controller as the missing layer in a lot of growing businesses. If you want a practical breakdown of the handoff point, when to hire a bookkeeper, controller, or CFO lays out the progression clearly.

How to diagnose which role you need

You probably need a bookkeeper if your issue is basic transaction hygiene. Bills aren't entered on time, invoices are inconsistent, and accounts haven't been maintained.

You probably need a controller if your issue is trust. The reports exist, but they're late, hard to explain, or full of unreconciled balances. You need someone to own the monthly close and turn accounting into management information.

You probably need a CFO if your issue is direction. The numbers are reliable, but you need help with pricing strategy, capital structure, fundraising, debt, expansion planning, or board-level decisions.

The wrong finance hire usually looks “capable” in interviews. The problem shows up later when the work they're best at doesn't match the problem you actually need solved.

Who Benefits Most from Fractional Controller Services

Companies usually become good candidates for fractional controller support at a specific financial inflection point. In my experience, the trigger is less about industry and more about volume, reporting complexity, and the cost of getting the numbers wrong. A common band is roughly $3 million to $15 million in revenue, where the business has outgrown basic bookkeeping, but a full-time senior finance hire still feels expensive relative to need.

The better question is not, “What kind of company uses a fractional controller?” It is, “What conditions make the hire pay for itself?”

Three trigger points show up repeatedly:

- Monthly close drifts past 10 to 15 business days

- Cash flow surprises leadership despite stable revenue

- Margin by customer, product, or service line is unclear

Once those issues show up together, the cost of delay rises fast. For a practical framework, this controller services ROI analysis breaks down the financial case in more detail.

SaaS and recurring revenue businesses

SaaS finance gets complicated earlier than founders expect. Deferred revenue, annual contracts, implementation fees, usage-based billing, credits, and commission treatment can all distort reported performance if the accounting is loose.

That matters because small classification errors can lead to bad operating decisions. If gross margin is overstated by even a few points, you may keep spending on acquisition channels that do not earn back their cost. If churn reporting excludes downgrades or delayed cancellations, the board sees a healthier business than the one finance is funding.

“Unit economics are the truth serum for SaaS businesses. You can have beautiful growth charts and impressive MRR, but if you're spending $15,000 to acquire customers who only generate $12,000 in lifetime value, you have a leaky bucket, not a business.” Jason Lemkin, Founder of SaaStr, quoted in Jumpstart Partners' piece on SaaS unit economics

A fractional controller helps clean up the underlying accounting so MRR, deferred revenue, gross margin, and cohort reporting hold up under scrutiny. That is often the difference between a useful board deck and a polished guess.

Agencies and professional services firms

Service businesses usually hit the wall through margin confusion, not revenue shortfall. The top line can look healthy while profits stay inconsistent because utilization, write-offs, scope creep, contractor mix, and owner compensation are not being tracked in a disciplined way.

I see the fastest ROI here.

If an agency is doing $5 million in annual revenue and improves net margin by just 2 points after fixing project costing and pricing discipline, that is $100,000 in annual profit. A fractional controller engagement often costs far less than that. The economics are not hard to justify when the reporting starts showing which clients create profit and which consume senior team time.

Strong controller support helps answer questions such as:

- Which accounts produce healthy contribution margin

- Whether new hires are increasing delivery capacity or just adding overhead

- Whether billing rates cover fully loaded labor cost

- Whether collections delays are creating avoidable borrowing or cash strain

If leadership cannot explain why one month generated cash and the next did not, despite similar revenue, the accounting layer usually needs attention.

Ecommerce, PE-backed, and nonprofit organizations

These groups need stronger control earlier than they often plan for, but for different reasons.

Ecommerce companies deal with timing and reconciliation risk. Inventory movements, returns, merchant fees, channel mix, and payout timing can make gross margin look better or worse than reality. When Shopify, Amazon, Stripe, and the general ledger do not reconcile cleanly, leadership loses confidence in both margin and cash forecasts.

PE-backed companies need reporting that survives diligence. Lenders, investors, and board members will ask for support schedules, consistent close procedures, and clean balance sheet detail. A fractional controller can build that reporting discipline before a financing process, covenant review, or sale process exposes the gaps.

Nonprofits have a different pressure set. Fund restrictions, grant compliance, board packets, and audit readiness require more than transaction entry. They require accurate classification, documentation, and repeatable reporting processes.

The common thread is simple. Fractional controller services make the most sense when bad financial reporting has become expensive, but a full-time controller still does not pencil out.

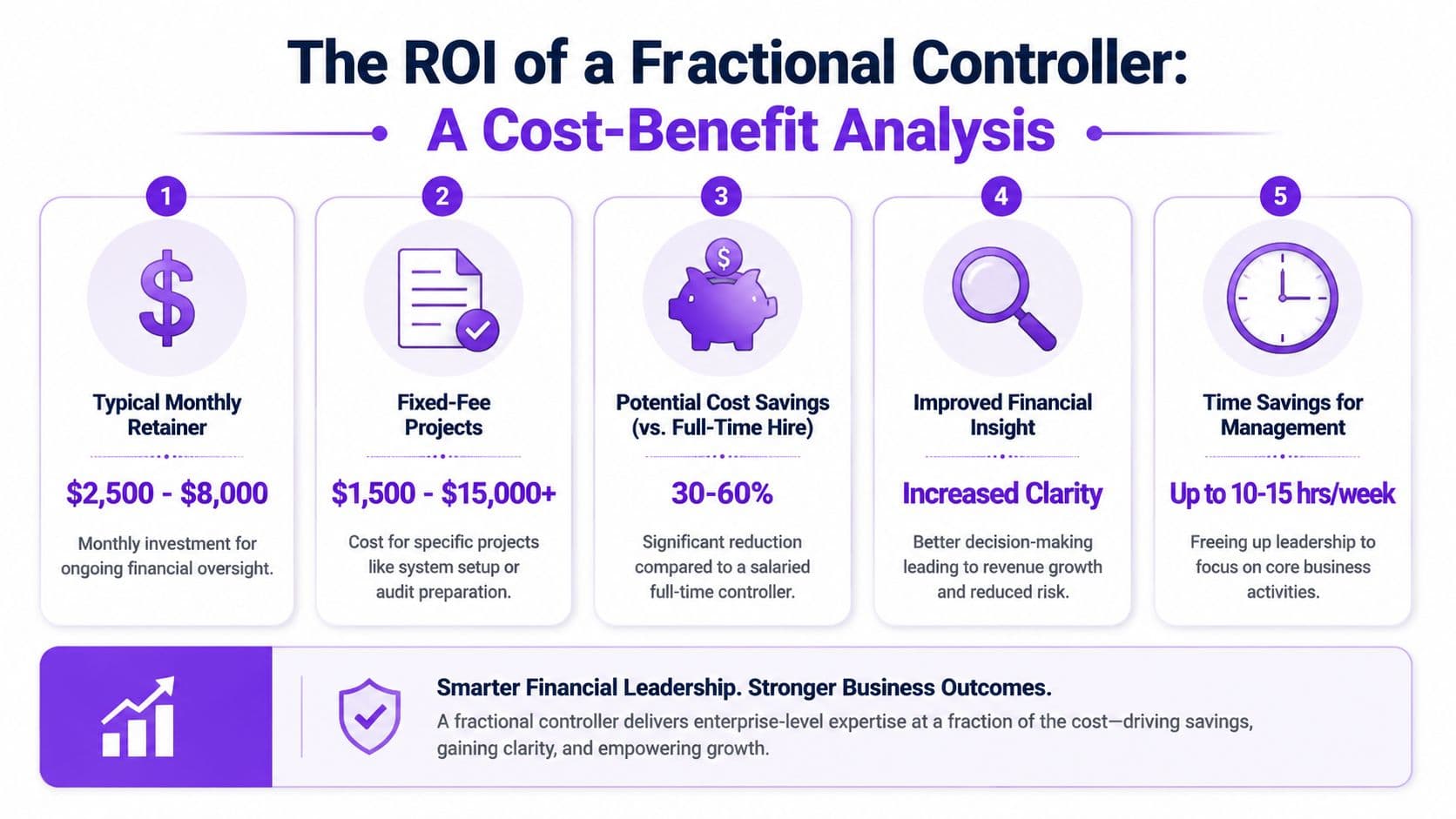

The ROI of a Fractional Controller A Cost-Benefit Analysis

A controller hire starts to pay for itself faster than many CEOs expect. The clearest cases show up when reporting delays, billing leakage, and leadership time waste are already costing more each quarter than a part-time controller engagement.

The business case is rarely just lower payroll. It is improved financial visibility that changes operating decisions before mistakes turn into write-downs, cash squeezes, or expensive cleanup work. For a company between roughly $2 million and $20 million in revenue, that usually matters more than the title itself.

What you are buying

You are paying for a stronger accounting layer that produces usable numbers on time and gives management a cleaner basis for decisions.

That return usually shows up in four places:

- Faster decision-making: leadership gets financials soon enough to act on them

- Lower error cost: reconciliations and review procedures catch misstatements earlier

- Better cash control: receivables, payables, and timing gaps become visible before they create strain

- Recovered executive time: the CEO, founder, or COO spends less time sorting out accounting noise

The gains are not always evenly distributed. A SaaS company may see the payoff first in deferred revenue accuracy and cleaner board reporting. An agency may see it in job profitability and fewer billing misses. An ecommerce business may see it in inventory, payout, and merchant fee reconciliation that stops gross margin from drifting away from reality.

If you want to pressure-test the numbers before talking to providers, run a simple controller services ROI analysis for growing companies.

This short video gives a useful overview of how finance support affects operating decisions:

A simple ROI framework with worked examples

Start with costs you can verify from your own business. That produces a stronger decision than generic claims about efficiency.

Worked example 1

Assume a full-time controller would cost $150,000 per year in salary, payroll taxes, and benefits. A fractional controller engagement at $4,000 to $7,000 per month costs $48,000 to $84,000 annually. The direct savings range is $66,000 to $102,000 per year.

That is the easy part of the math.

The harder part, and usually the bigger part, is whether the business is already losing money because the accounting function is late, inconsistent, or too shallow.

Worked example 2

Assume the company invoices $500,000 per month and weak follow-up or poor billing controls delay collection by just 10 days on 15% of invoices. That is about $75,000 of cash arriving late each month. If the business is relying on a line of credit at 10% interest, the financing cost is modest on paper, but the operating impact is not. Late cash can force slower hiring, delayed vendor payments, or founder intervention every month.

A controller does not solve collections alone, but a good one creates the reporting discipline that shows where invoices stall, who owns follow-up, and which customers are becoming a pattern.

Worked example 3

Use leadership time as a line item. If a CEO and COO together spend 12 hours a month reviewing questionable financials, answering lender questions, and chasing missing balance sheet support, that is 144 hours a year. At a blended executive cost of $150 to $250 per hour, that is $21,600 to $36,000 in annual management time spent on work that should be handled inside the finance function.

That cost is often hidden, so it gets ignored.

Worked example 4

Now add one preventable reporting error. A missed accrual, an unreconciled payroll liability, or a revenue classification problem can easily create a five-figure cleanup with your CPA firm, plus internal rework. One cleanup project a year can erase much of the perceived savings from waiting too long.

Trigger points that usually justify the spend

The best time to hire is not “when finance feels messy.” It is when the mess has become measurable.

A fractional controller usually makes financial sense when several of these conditions are true at the same time:

- Monthly close regularly runs past 15 business days

- Leadership does not trust the P&L without extra explanation

- Balance sheet accounts stay unreconciled for more than one close cycle

- Cash swings are hard to explain from operations alone

- Billing errors or delayed invoicing are affecting collections

- Board, lender, audit, or tax requests trigger scramble mode

- The CEO or founder is still the backstop for reporting accuracy

At that point, the question is less about affordability and more about how much bad information is already costing the business.

Common objections and the trade-off

“We're too small” can be true at $500,000 in revenue with simple operations. It is usually false at $5 million in revenue with multiple departments, financing needs, or recurring revenue complexity.

“We already have a bookkeeper” is not a rebuttal. It means transaction processing is covered. It does not mean the company has ownership of the close, reconciliations, accruals, reporting package, or control issues.

“We'll wait until we hire a CFO” often creates a more expensive problem. Without a controller layer, the CFO spends time cleaning up numbers instead of helping with pricing, capital planning, or strategic decisions.

One provider option in this market is Jumpstart Partners, which offers outsourced controller support for growing businesses and project-based work such as cash flow planning and cleanup. The useful test is straightforward. Can the provider shorten the close, improve balance sheet accuracy, clarify ownership, and give management numbers it can use with confidence?

Your Vendor Selection Checklist

Most buyers focus too much on credentials and too little on operating fit. The right provider should make your finance function more dependable within the first closing cycle, not just sound polished in a sales call.

What to verify before you sign

Use this checklist in interviews and proposal reviews.

- Industry pattern recognition: Ask whether they've handled your business model before. SaaS revenue timing, agency utilization, ecommerce reconciliation, and nonprofit fund tracking all create different accounting problems.

- Tech stack fluency: They should be comfortable with your accounting system and adjacent tools. That often means QuickBooks, Xero, NetSuite, Stripe, Shopify, Gusto, payroll systems, and CRM integrations.

- Scope clarity: Ask exactly who owns the close checklist, reconciliations, reporting package, budgeting support, and communication with your bookkeeper or outside CPA.

- Security and access controls: You're granting access to banking data, payroll, customer billing, and financial statements. Ask how permissions are managed, how files are shared, and how offboarding works.

- Team depth: A single excellent operator can be great until they disappear during close week. A team-based model usually handles continuity better.

- Communication rhythm: You want a defined cadence for close updates, review calls, cash forecast refreshes, and escalation when something breaks.

If you're evaluating outsourced finance support more broadly, this overview of finance and accounts outsourcing is a useful benchmark for comparing models.

Red flags that should stop the process

Some warning signs should end the conversation quickly.

Red Flags

- Vague deliverables: If they can't describe what your monthly output will include, expect confusion later.

- No balance sheet discipline: Any provider who talks only about the P&L is skipping the foundation.

- Tool ignorance: If they don't understand the systems feeding your ledger, reporting problems will keep repeating.

- Founder dependency: If their model relies on you to explain every account each month, they aren't building a process.

- No handoff structure: You need clarity on how they work with your tax CPA, payroll provider, and internal operations lead.

- Reactive posture: If they only “fix issues when they appear,” you're buying cleanup, not control.

A good vendor doesn't just answer finance questions. They reduce the number of questions that recur each month.

Your Action Plan for Onboarding and Success

The best onboarding plans are operational, not ceremonial. You don't need a long kickoff deck. You need access, ownership, cleanup priorities, and a timeline to first reliable reporting.

The first 90 days

Weeks 1-2 should focus on data access and diagnosis. Your controller needs entry to the accounting platform, bank feeds, payroll system, billing tools, loan records, and prior financial statements. They should also review your chart of accounts, close process, outstanding reconciliations, and reporting needs.

Weeks 3-4 are for cleanup and control design. That usually includes reconciling major balance sheet accounts, correcting coding issues, documenting recurring journal entries, and setting a close checklist with owners and deadlines.

Month 2 should produce the first dependable reporting cycle. That means a closed month, reviewed statements, cash visibility, and commentary on key variances. If that doesn't happen, something is off in scope, data access, or execution.

What success should look like

By Month 3, you should expect a stable routine.

That usually includes:

- A repeatable close cadence: Everyone knows what happens and when

- Financial statements you trust: Not perfect forever, but controlled and explainable

- Forward cash visibility: Enough to make hiring, spending, and payment decisions with less guesswork

- Better management conversations: Less debate over the numbers, more discussion about action

If you're evaluating whether your business is at that trigger point, start with your last three closes. Were they timely? Did the balance sheet reconcile cleanly? Could you explain margin and cash movement without rebuilding the file from scratch? If the answer is no, the business case is already there.

If your team has outgrown bookkeeping but doesn't need a full-time controller yet, Jumpstart Partners can help you assess the gap, clean up the close process, and put reliable reporting and cash visibility in place. A short consultation is usually enough to determine whether you need ongoing controller support or a targeted cleanup project first.