Financial Operations

Mastering Finance and Accounts Outsourcing for CEOs

CEOs, navigate finance and accounts outsourcing. Learn models, ROI, security, and vendor selection for your business. Get the complete guide.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readYou’re doing revenue. You’re paying people. You’re buying software. You’re probably making decent gross margin. And yet when you ask a basic question like “What can I safely spend next quarter?” or “Which clients are profitable?” the answers come late, half-complete, or not at all.

That’s the point where finance stops being admin and starts becoming a bottleneck.

For a founder running a business around $5M, finance and accounts outsourcing isn’t about dumping bookkeeping on someone else. It’s about getting a finance function that produces numbers you can trust, fast enough to use. If your books are late, your reconciliations are messy, or your reporting changes every month depending on who touched the spreadsheet, you don’t have a finance system. You have a reporting ritual.

When Your Financials Create More Questions Than Answers

You know the pattern. Revenue looks healthy. Cash feels tighter than it should. Payroll goes out. Tax deadlines get handled. But every management decision still feels harder than necessary because the numbers don’t line up cleanly.

That’s why finance and accounts outsourcing has become a strategic category, not a back-office niche. The market was valued at USD 70.19 billion in 2025 and is projected to reach USD 142.66 billion by 2033, growing at a 9.3% CAGR, according to Grand View Research’s finance and accounting outsourcing market analysis. Businesses are not buying outsourced accounting because it sounds efficient. They’re buying control.

What founders usually get wrong

Most founders wait too long.

They assume a part-time bookkeeper, a tax CPA, and a few internal spreadsheets are “good enough” until they hit a bigger milestone. Fundraising. A bank review. A board deck. An acquisition conversation. Then they discover the historical data is inconsistent, deferred revenue isn’t handled properly, payroll entries are off, or key balance sheet accounts haven’t been reconciled in months.

Practical rule: If your P&L needs explanation every month, the issue isn’t the report. The issue is the process behind it.

For a business in the $500K to $20M range, the hidden liability isn’t usually fraud or some dramatic collapse. It’s slower decisions, weaker pricing choices, poor cash planning, and time wasted debating numbers nobody fully trusts.

What outsourcing should actually fix

A real outsourced finance function should give you:

- Timely close so you can act on current data, not last month’s guess

- Clean reconciliations so balance sheet numbers are defensible

- Consistent reporting across revenue, margin, cash, and operating expenses

- Decision support for hiring, pricing, forecasting, and fundraising

If your underlying data is already messy, you may need QuickBooks cleanup services for historical errors and reconciliations before anything else. That’s not a side issue. It’s the foundation.

The Four Models of Finance Outsourcing

“Outsourcing” is too broad to be useful. You need to know what job you’re hiring for.

Some providers record transactions. Some own close and controls. Some help you make strategic decisions. Some only fix one urgent problem. If you buy the wrong model, you either overpay or stay under-supported.

Finance outsourcing service models compared

| Service Model | Best For | Core Services | Strategic Impact |

|---|---|---|---|

| Bookkeeping-as-a-Service | Early-stage companies with simple operations and weak monthly discipline | Transaction coding, bank reconciliations, AP/AR support, monthly books | Gives you cleaner history |

| Outsourced Controller | Businesses with growing complexity and reporting needs | Month-end close, accruals, reconciliations, management reporting, process controls | Gives you reliable monthly reporting |

| Fractional Virtual CFO | Founders making capital allocation, hiring, pricing, or fundraising decisions | Forecasting, board reporting, KPI design, scenario planning, strategic finance support | Helps you decide what to do next |

| One-off Project Work | Companies with a specific finance problem | Cleanup, cash flow build, system migration, audit prep, rev rec remediation | Fixes a defined bottleneck |

Bookkeeping records the past

Bookkeeping-as-a-Service is the minimum viable layer. It matters, but don’t confuse it with finance leadership.

If your need is simple transaction capture, vendor bills, expense categorization, and monthly reconciliations, this model is enough for now. It’s useful when your business is still operationally straightforward and the main problem is backlog.

What it won’t do is tell you whether your service lines are profitable, whether your hiring plan is affordable, or whether your cash forecast is realistic.

Controller support builds financial discipline

The outsourced controller model is where most $5M businesses should start looking seriously.

This role closes the books properly. It handles accruals, ties out the balance sheet, improves reporting quality, and gives you a stable monthly reporting package. If your current setup produces noisy numbers, this is usually the missing layer. A good controller doesn’t just report results. They make the accounting structure dependable.

If you’re weighing whether this should sit in-house or outside the company, read this in-house vs outsourced controller decision guide for growing companies.

A fractional CFO changes the conversation

A virtual CFO should not be doing basic bookkeeping.

A good fractional CFO translates numbers into action. Should you hire two account managers this quarter or wait? Can you afford a pricing experiment? What happens to runway if receivables slip? How should you explain margin compression to investors or lenders? That’s the work.

You hire a bookkeeper to classify activity. You hire a controller to validate it. You hire a CFO to help you act on it.

Project work solves narrow problems

Sometimes you don’t need an ongoing engagement yet. You need a finance project.

Common examples include:

- Historical cleanup when prior books are unreliable

- Cash flow forecasting before a financing decision

- Revenue recognition remediation for SaaS or contract-heavy services

- System integration work across QuickBooks, Stripe, Shopify, Gusto, or NetSuite

Project work is valuable when the pain is concentrated. But if your business has recurring monthly complexity, projects alone won’t solve the operating problem.

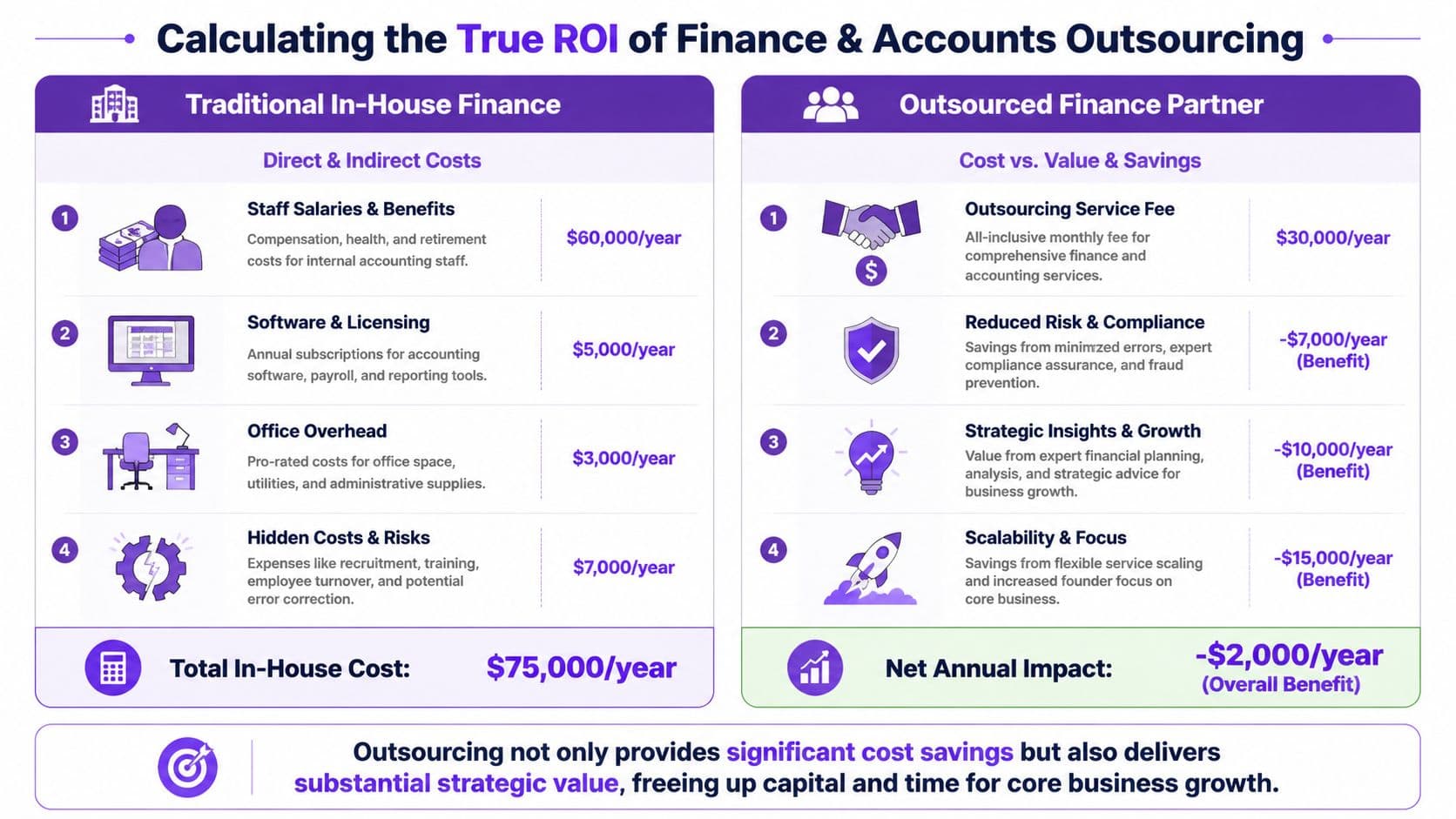

Calculating the True ROI of Outsourcing

Most ROI conversations about outsourcing are shallow. They compare one salary to one monthly fee and stop there. That overlooks the full economic picture.

The full return comes from four places: lower operating cost, corrected historical errors, faster decision cycles, and less founder time spent babysitting finance.

Start with direct cost

Use a simple worked example.

Assume you’re considering an in-house controller at $120,000. If you compare that to an outsourced arrangement costing $5,000 per month, the annual outsourced spend is:

- $5,000 x 12 = $60,000

Direct annual difference:

- $120,000 in-house cost

- $60,000 outsourced cost

- $60,000 direct savings

That’s the obvious part. It’s not the whole case, but it matters because it creates budget room for better systems and higher-level support.

Add the hidden error correction value

Most founders often underestimate the upside.

According to Insignia Resource’s accounting outsourcing statistics roundup, providers report finding significant onboarding issues, and Jumpstart Partners reports an average of over $47,000 in issues per new client. If your books have been managed reactively, that number should get your attention.

Now add that into the same ROI math.

- Direct annual savings from outsourcing = $60,000

- Historical errors identified and corrected = $47,000

- Total first-year financial impact = $107,000

That does not mean every dollar drops straight to profit. Some issues are timing errors, some are classification fixes, some are tax or revenue recognition exposures. But they all affect decision quality and risk.

Count the speed-to-close value

Here’s the operational side.

If your current close takes 20 days and a modern outsourced provider gets you to 5 days or fewer, you gain 15 days of earlier visibility each month. Over a year, that’s:

- 15 days x 12 months = 180 days

You are effectively operating with current financial visibility 180 days earlier per year.

That’s not a soft benefit. It changes hiring timing, pricing reviews, cash planning, and collections pressure. You’ll stop making decisions based on old information.

Owner test: Ask yourself how many decisions you delayed this year because the numbers weren’t ready. That delay has a cost, even if it never shows up as a line item.

Build a practical ROI worksheet

Use this framework:

| ROI Component | Worked Example |

|---|---|

| In-house finance cost | $120,000 |

| Outsourced annual fee | $60,000 |

| Direct savings | $60,000 |

| Historical errors found during onboarding | $47,000 |

| First-year measurable impact | $107,000 |

If you want to pressure-test the numbers for your own business, this controller services ROI analysis resource is the kind of framework you should use internally.

The point is simple. Don’t evaluate finance and accounts outsourcing as labor arbitrage. Evaluate it as a combination of cost control, cleanup, speed, and reduced decision risk.

Security Compliance and Your Tech Stack

The biggest reason founders hesitate to outsource finance isn’t cost. It’s trust.

You’re handing over payroll data, revenue data, customer billing data, bank activity, tax records, and often investor reporting. If the provider treats security like a sales checkbox, walk away.

Security is not optional

For regulated industries such as SaaS under ASC 606, finance, and healthcare, domain expertise matters, but security matters just as much. Mordor Intelligence’s market analysis on finance and accounting outsourcing notes that data-privacy regulations and cyber-risk are the top risks associated with outsourcing, which is why SOC 2 Type II and documented internal controls are critical.

That should shape your buying criteria immediately.

Ask for:

- SOC 2 Type II evidence or equivalent control documentation

- Role-based access controls across banking, payroll, and accounting systems

- Approval workflows for payables, payroll changes, and user permissions

- Documented internal controls for reconciliations, close, and reporting review

If you want a broader view of how security controls tie into business risk, Understanding compliance risks and ROI gives a useful non-finance lens that most founders should read.

Your provider should improve your stack, not complicate it

A modern outsourced finance team should act like the hub of your finance data, not another layer of manual work.

That means connecting your accounting system to the tools that already run your business:

- QuickBooks, Xero, or NetSuite for core accounting

- Stripe, Shopify, and Square for payments and sales channels

- Gusto and BambooHR for payroll and people data

When those systems don’t talk cleanly, your team wastes time on exports, spreadsheet tie-outs, and duplicate entry. A competent provider closes those gaps and gives you one reliable reporting flow.

If your “finance process” depends on one employee remembering which CSV to download, your process is fragile.

Compliance and automation should work together

A good provider doesn’t ask you to choose between control and speed.

You want documented review processes, but you also want automation in reconciliations, reporting, and recurring workflows. Those things belong together. If a firm can’t explain how it handles both, they’re not ready for a growth-stage client.

If you’re still relying on a patchwork setup, this overview of startup bookkeeping services and modern finance support is the right baseline for what a properly integrated operation should cover.

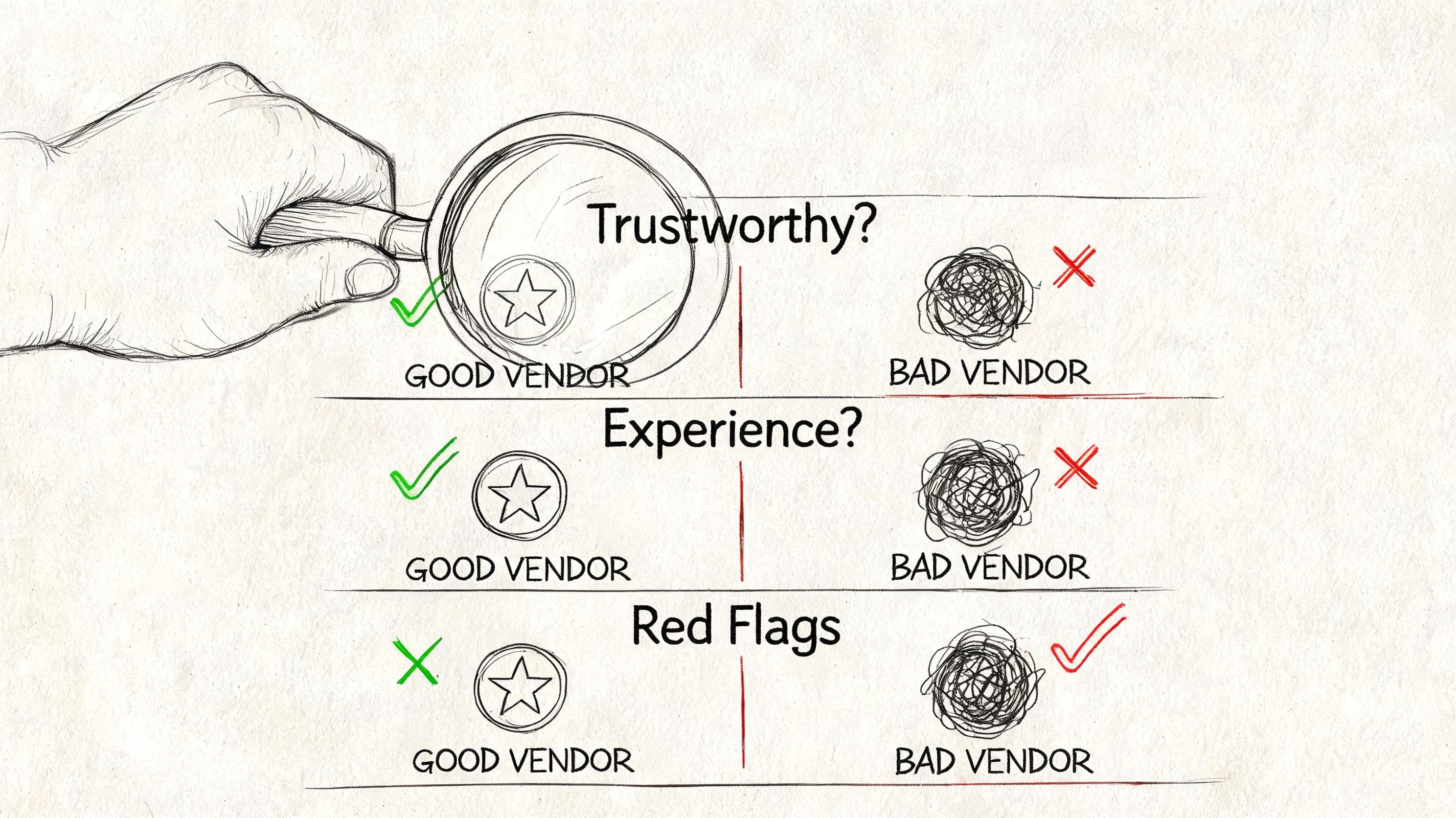

How to Choose a Vendor and Red Flags to Avoid

It is the 12th of the month. You still do not trust last month’s numbers, payroll is waiting on approval, and a lender or investor asks for clean financials by Friday.

That is the true vendor test.

A finance outsourcing firm should do more than keep books current. It should reduce correction work, shorten close, and give you investor-ready reporting without a scramble. If a provider cannot show how it improves those three outcomes, you are buying labor, not finance leadership.

What to score in a vendor review

Start with capacity and hiring depth. According to CFO.com’s coverage of the Personiv CFO Pulse Survey, 90% of CFOs who outsource report they can easily find qualified accountants, while 100% of non-outsourcing peers struggle with staffing. Access to talent matters, but staffing alone is not the win. The key question is whether that talent produces faster closes, fewer errors, and cleaner reporting for decisions.

Use a scorecard. Make each firm earn the work.

-

Industry fit

Ask for examples from businesses like yours. SaaS revenue recognition, agency project accounting, and e-commerce inventory each break in different places. A firm that treats them the same will miss issues that later require cleanup. -

Team structure

Get the org chart for your account. You need to know who does transaction work, who reviews it, who owns the close, and who answers when something goes wrong. If accountability is blurry in the sales process, it will be worse after you sign. -

Close process and speed

Ask how many business days they need to close the month, what is included in that close, and what would delay it. A fast close is not cosmetic. It gives you time to correct course while the month still matters. -

Error correction approach

Ask how they diagnose bad books, rebuild reconciliations, and quantify prior-period issues. Hidden errors destroy ROI because you pay twice. First for bad work, then for cleanup. -

Reporting quality

Request a sample monthly reporting pack, cash flow forecast, and board or lender package. If the output is thin, late, or hard to read, your decisions will be slow and your investor conversations weaker. -

Control environment

Ask who approves payroll, who releases payments, how access is reviewed, and how changes are documented. Payroll and payables fraud usually slips through weak process, not weak software. Benely's payroll fraud prevention guide is a useful checklist to compare against a vendor’s control setup.

Questions worth asking on the first call

Ask these directly, then listen for specifics instead of polished answers:

- How do you handle onboarding when prior books are wrong, and how do you separate cleanup from ongoing work?

- What does your month-end close checklist include, and what is your target close timeline?

- Who reviews the work before reports reach me, and what happens if that reviewer finds errors?

- Can you show me a sample cash flow forecast, management report, and investor or lender package?

- How do you handle approvals for payroll, vendor payments, and changes to bank access?

- What is your process if my accounting setup is not audit-ready or not accrual-ready?

- How do you measure success in the first 90 days besides getting transactions booked?

That last question matters. A serious provider will talk about close speed, reconciliation coverage, reporting accuracy, and decision-useful output. A weak one will talk about hours worked.

Red flags that should kill the deal

Some red flags are obvious. Others look harmless until they cost you a quarter.

-

Hourly billing for routine monthly work

That model rewards drift, not discipline. For recurring bookkeeping, close, and reporting, you want defined deliverables and clear ownership. -

No named account lead

Shared inboxes and rotating staff create missed context. You need one person accountable for deadlines, quality, and escalation. -

No sample reporting

If they cannot show the product, do not buy the promise. -

Vague cleanup language

If your books need repair and the answer is “we’ll sort it out during onboarding,” expect overruns, delays, and ugly surprises in the first close. -

No clear review layer

Bookkeeping without controller review is how hidden errors survive for months. -

No explanation of how they support investor or lender requests

You may not need a board deck today. You will still need clean, credible numbers on short notice. A provider that cannot produce them raises your financing risk. -

Security claims with no process behind them

“We take security seriously” means nothing. Ask who can approve payments, who can change payroll details, and how access is removed.

This short video is worth watching before you sign with anyone:

Choose the firm that can explain, in plain English, how it will shorten close, catch errors early, and deliver investor-ready financials without fire drills. That is where the ROI shows up.

Real-World Results from Outsourced Finance

Most founders don’t need another abstract argument. They need to know what changes in practice.

The SaaS scale-up

A SaaS company has recurring revenue, but the founder still waits too long to see clean MRR, churn, and expense trends. Marketing spend decisions happen in a fog because the numbers land too late.

An outsourced finance team shortens close, ties billing data back to the general ledger, and standardizes reporting. Now the founder sees current subscription performance early enough to adjust spend this month, not next month. The value isn’t bookkeeping. The value is faster capital allocation.

The agency turnaround

A digital agency thinks it has a sales problem. It doesn’t. It has a pricing and delivery problem.

Once controller-level reporting is in place, client profitability becomes visible. A few accounts that look large on revenue turn out to be weak on margin because delivery hours are too high and change orders are poorly tracked. The fix is not “work harder.” It’s repricing, tighter scope control, and changing which work the agency says yes to.

Better finance doesn’t just tell you what happened. It tells you what to stop doing.

The e-commerce cash squeeze

An e-commerce brand is growing, but cash feels tight every time inventory orders hit. Revenue is up, yet operating pressure keeps rising.

Outsourced finance proves its worth. The team builds a short-term cash view, aligns payout timing from sales channels with payroll and vendor obligations, and gives the founder a clearer purchase plan. The immediate result is less guesswork. The strategic result is fewer avoidable cash crunches during growth.

Across all three examples, the pattern is the same. Better finance and accounts outsourcing gives you usable numbers, cleaner controls, and faster decisions. That’s what you’re buying.

Your Step-by-Step Transition Checklist

The transition doesn’t need to be messy. It needs to be structured.

Strategic CFO’s overview of outsourced accounting and FP&A in 2025 notes that modern providers use end-to-end automation, AI-driven forecasting, and intelligent automation that can shorten closing cycles to 5 days or fewer. That only happens when onboarding is disciplined.

What to do first

-

Define the business problem

Decide whether your main issue is late close, messy historical books, weak cash visibility, or lack of strategic reporting. -

Gather system access and documents

Pull your accounting files, bank access structure, payroll records, prior financials, tax filings, and key contracts into one place. -

Identify cleanup needs

Be honest about what’s broken. Unreconciled bank accounts, bad revenue coding, and missing accruals should be surfaced early.

What the provider should handle next

- System mapping between accounting, payments, payroll, and HR tools

- Close process design with responsibilities, review steps, and deadlines

- Reporting package setup for P&L, balance sheet, cash flow, and KPIs

- Control design for approvals, access, and reconciliations

If you want a practical starting point, use this month-end close checklist template for growing businesses to compare your current process against what a real close should include.

What success looks like in the first month

You should expect:

- cleaner reconciliations

- a defined close calendar

- fewer spreadsheet workarounds

- reports that tie out consistently

- clear ownership for open issues

If you don’t get those basics quickly, the transition is off track.

If your current financials are late, noisy, or dependent on founder intervention, it’s time to fix the system instead of tolerating it. Jumpstart Partners works with growing businesses that need outsourced controller and bookkeeping support, faster close, and investor-ready reporting. If you want a clear view of what needs cleanup, what can be automated, and what level of finance support fits your business, book a consultation and get specific about the next step.