Financial Operations

Your Revenue Numbers Are Wrong, and It’s Destroying Your Valuation

Unsure what is ASC 606 revenue recognition? This guide explains the 5 steps with SaaS examples to get your financials investor-ready. Avoid common pitfalls.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readAs a founder or CEO, you believe your revenue numbers are accurate. But there's a strong chance they're not, and this single mistake is quietly killing your company’s valuation.

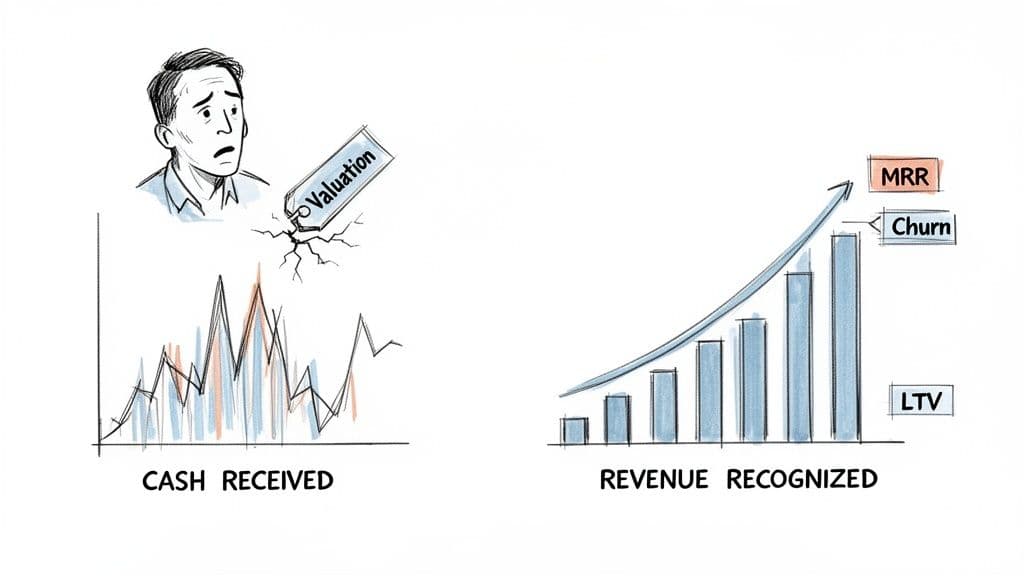

The problem is deceptively simple: you book revenue when cash lands in your bank account. It feels intuitive, but it creates volatile, unreliable financial reports that can kill a funding round or an acquisition before it even starts. Investors don't use your cash numbers; they use ASC 606, and you must too.

Why Your Revenue Approach Is Costing You

If you're running a SaaS, digital agency, or professional services firm between $500K and $20M in revenue, the biggest threat to your valuation isn't your product or your team—it's your books. Investors and acquirers don't care about your cash-basis revenue; they evaluate your business using ASC 606 revenue recognition, the official standard under US GAAP.

Getting this wrong makes your growth look erratic and completely undermines trust in your financial discipline. A messy P&L is one of the fastest ways to get a "no" from a serious investor.

ASC 606 isn't just an arcane accounting rule; it's a strategic necessity. It forces you to recognize revenue as you earn it by delivering your service, not when you get paid. For a SaaS company, this means recognizing a $12,000 annual subscription as $1,000 per month, not as a single lump sum when the payment clears.

"Many founders treat accounting as a backward-looking compliance task. That's a huge mistake. Investor-grade financials built on ASC 606 are a forward-looking strategic asset that tells a clear, defensible story of your company's health and scalability." — Ben Murray, The SaaS CFO

This shift from cash-based to accrual-based recognition has a massive impact on the metrics that actually matter:

- Monthly Recurring Revenue (MRR): It becomes a stable, predictable measure of growth, completely free from the noise of annual prepayments and lumpy cash collections.

- Customer Lifetime Value (LTV): It's calculated using correctly recognized revenue, giving you a true picture of long-term customer profitability.

- Churn: Your revenue churn calculations become far more accurate because they’re based on consistent monthly revenue streams, not cash timing.

Common Misconception: "We're too small for this."

This is the most common and dangerous objection we hear. Founders of sub-$20M businesses often believe ASC 606 compliance is only for large, public companies. This is false. If you plan to raise capital, seek debt financing, or sell your company, your financials will be audited against GAAP standards.

Failing to adopt ASC 606 creates enormous business risk. When you enter due diligence, investors will immediately force a restatement of your financials. The result is almost always a lower valuation, damaged credibility, and a painful, drawn-out closing process. In a competitive M&A market, buyers often won't even bother—they’ll just walk away.

Getting it right provides a clear, defensible picture of your company’s performance. It smooths your revenue, validates your metrics, and proves you have the financial discipline required to scale. This isn't just about compliance—it's about maximizing your valuation and ensuring you're ready for your next big move.

Understanding ASC 606 and Why It Matters Now

Think of ASC 606 as the universal translator for revenue. It’s the accounting rule that forces you to shift your mindset from "when did we get the cash?" to "when did we actually earn the money by delivering value?" This isn't just a technical update for accountants; it’s a critical standard for any founder who wants to build a fundable, scalable business.

Before ASC 606, the rules were a mess of inconsistent, industry-specific guidelines. An investor couldn't reliably compare a SaaS company in Boston to a digital agency in Austin. The new standard wiped that ambiguity away, replacing it with a single, five-step model that puts everyone on a level playing field.

A Principles-Based Framework for Clarity

When ASC 606 went into effect for private companies on January 1, 2019, it fundamentally changed the game. The new framework is built on a simple principle: you identify the specific promises you've made to your customer (your performance obligations) and only recognize revenue as you fulfill those promises.

This isn't just theory. According to a PwC survey, 79% of companies found that implementing ASC 606 led to higher quality revenue data and better business insights. For you, this has direct implications.

Let's say a customer pays you $24,000 upfront for an annual software subscription. You can no longer book all $24,000 as revenue the day the cash lands in your bank account. Instead, you must recognize it as $2,000 each month as you deliver the software service over the year. This approach smooths out your reported revenue and paints a much more accurate picture of your company’s actual performance.

Why This Matters to You as a Founder

If you have any plans to raise money, get a bank loan, or sell your company, adopting ASC 606 isn't optional. It's the gold standard for financial reporting, and it's the first thing sophisticated investors and acquirers look for.

Getting it right does two crucial things for you:

- It ensures your financial metrics are accurate and defensible, especially key SaaS indicators like monthly recurring revenue (MRR). Investors will grill you on this.

- It signals financial discipline and operational maturity. It shows you run a tight ship, building trust with the very people who will be scrutinizing your books during due diligence.

Ignoring this standard means your financial statements aren't just incorrect—they're a major liability. Having to go back and fix years of improper revenue recognition is a painful and expensive fire drill that can put deals at risk. For a detailed walkthrough of how these principles apply to subscription models, check out this guide to revenue recognition in the software industry. Getting this right from the start ensures your financial story is told correctly.

The Five-Step Revenue Recognition Model in Action

ASC 606 gets rid of the old, inconsistent mess of industry-specific rules and replaces them with a single, clear framework. This isn't just academic theory; it's a five-step model that forces you to connect your revenue directly to the value you deliver to customers. Think of it less like accounting rules and more like a universal recipe for proving how and when you earn your money.

The big shift? It moves your thinking from the old way—"book revenue when cash hits the bank"—to the modern, correct standard: recognize revenue when it is earned.

This principles-based approach means more comparable and trustworthy financials. And in the world of fundraising and M&A, trust and comparability are what drive higher valuations.

So let’s walk through what these five steps actually look like in practice for your business.

The ASC 606 Five-Step Model

| Step | Objective | Common Pitfall for Your Business |

|---|---|---|

| 1. Identify the Contract | Confirm a legitimate, enforceable agreement exists with a customer. | Mistaking a non-binding "letter of intent" or a verbal agreement for a valid contract. |

| 2. Identify Performance Obligations | Break down the contract into all the distinct promises you've made to deliver. | Lumping multiple distinct services (e.g., software access, setup, and training) into one "bundle," which distorts revenue timing. |

| 3. Determine the Transaction Price | Calculate the total money you truly expect to receive, accounting for variables. | Ignoring variable consideration like performance bonuses, usage fees, or potential refunds, which overstates the transaction price. |

| 4. Allocate the Price | Assign a portion of the total price to each distinct promise based on its fair value. | Allocating the price based on what's convenient instead of the item's standalone selling price (SSP). |

| 5. Recognize Revenue | Book revenue only as you fulfill each specific promise to the customer. | Recognizing all revenue upfront for a 12-month contract instead of recognizing it monthly as the service is delivered. |

Now, let's unpack each of those steps with real-world examples.

Step 1: Identify the Contract with a Customer

First, you need a real contract. This is any agreement that creates enforceable rights and obligations—it can be a formal written document, a click-through agreement, or even an established business practice.

For a SaaS company, it's the subscription agreement. For an agency, it's the signed Statement of Work (SOW). The key is that the contract must have commercial substance, and it must be probable that you’ll collect the payment. You can't recognize revenue from a deal with a customer who clearly has no ability or intention to pay.

Step 2: Identify the Performance Obligations

Next, you must look at that contract and itemize every distinct promise you've made. Each one is a performance obligation. A promise is "distinct" if the customer can benefit from it on its own or with other readily available resources.

This is where many companies stumble. You have to unbundle your offering.

- SaaS Example: A $25,000 annual contract isn't just one thing. It might include two distinct performance obligations: (1) ongoing access to the software platform for $24,000 and (2) a one-time $1,000 implementation service. The software and the setup are separate promises.

- Agency Example: A $60,000 website project might have three performance obligations: (1) delivering a brand strategy guide, (2) building the website, and (3) providing three months of post-launch support.

Incorrectly bundling services is a huge mistake. It completely distorts the timing of your revenue and gives investors a false picture of your performance.

Step 3: Determine the Transaction Price

The transaction price is what you actually expect to get paid. This sounds simple, but it’s more than just the number on the invoice. You must account for variable consideration—things like discounts, rebates, performance bonuses, or usage-based fees.

You must make a reasonable estimate of these variables and factor them into the total price from day one. For instance, if you offer a 10% discount for early payment on a $50,000 contract and expect the client to take it, your transaction price is $45,000, not $50,000. If your pricing is based on usage, you have to forecast that usage to land on the price.

Step 4: Allocate the Price to Performance Obligations

With your total transaction price determined, you now must spread that money across each of the separate performance obligations you identified in Step 2. This allocation isn't arbitrary; it must be based on each item's standalone selling price (SSP)—the price you'd charge for it separately.

Let's go back to our SaaS example: a $25,000 annual contract that includes software access ($24,000 SSP) and a one-time implementation service ($1,000 SSP). The allocation is straightforward. You’d allocate $24,000 to the software and $1,000 to the implementation. If you don't have an SSP, you have to estimate it using a consistent methodology, like a cost-plus-margin approach.

Step 5: Recognize Revenue When You Satisfy Performance Obligations

Finally, the payoff. You can recognize revenue only as (or when) you satisfy a performance obligation by transferring control to the customer. This can happen in two ways:

- Over Time: For services delivered continuously, you recognize the revenue evenly over the service period. A $24,000 annual SaaS license is a perfect example; you’d recognize $2,000 in revenue each month for 12 months. The nuances here are critical, which we cover in our guide to revenue recognition in the software industry.

- At a Point in Time: For promises fulfilled all at once, you recognize the revenue when the work is complete and delivered. In our example, you’d recognize the full $1,000 for the implementation service the moment it's finished and the customer has accepted it.

ASC 606 Revenue Recognition Examples and Calculations

Theory only gets you so far. The real impact of ASC 606 clicks when you see the numbers in action. The most important lesson is simple but revolutionary for many businesses: your bank balance is not your revenue.

Let’s break down two common scenarios—one for a SaaS company and one for a professional services firm—and compare the old, cash-based method with the correct ASC 606 approach.

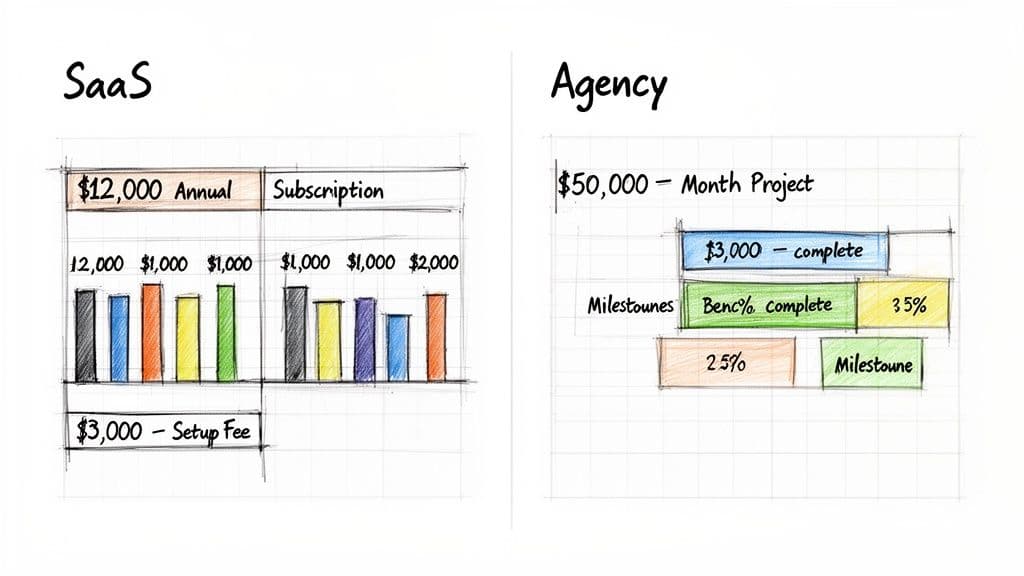

SaaS Example: Annual Contract with Setup Fee

Imagine your SaaS company signs a new customer on January 1st. They pay $15,000 upfront.

- Annual Software Subscription: $12,000

- One-Time Setup Fee: $3,000 (delivered in January)

The Wrong Way (Cash Basis): You’d book $15,000 in revenue for January because that’s when the cash landed. Your P&L shows a massive revenue spike in Month 1, followed by eleven months of zero revenue from this client. This volatility makes your growth look erratic and unreliable.

The Correct Way (ASC 606): You must break the contract into its distinct performance obligations and recognize revenue as you deliver value.

- Setup Fee Revenue: The setup is a distinct service delivered "at a point in time." You recognize the full $3,000 in January when the work is completed.

- Subscription Revenue: The $12,000 software license is delivered "over time." You must recognize it evenly, booking $1,000 per month ($12,000 / 12 months).

The cash you received but haven't earned sits on your balance sheet as a liability called deferred revenue. Our guide on what is deferred revenue breaks down exactly how to manage this.

| Month | Incorrect Revenue (Cash) | Correct Revenue (ASC 606) | Calculation (ASC 606) |

|---|---|---|---|

| Jan | $15,000 | $4,000 | $3,000 (Setup) + $1,000 (Subscription) |

| Feb | $0 | $1,000 | $1,000 (Subscription) |

| Mar | $0 | $1,000 | $1,000 (Subscription) |

| ... (Apr-Dec) | $0 | $1,000/mo | $1,000 (Subscription) |

| Total Year 1 | $15,000 | $15,000 |

While the annual total is the same, the ASC 606 method smooths your recurring revenue, giving investors a stable, predictable picture of your business's true health.

Professional Services Example: Project-Based Work

Now let's look at a digital agency that signs a $50,000, three-month website redesign project. The payment schedule is 50% upfront and 50% on completion.

The Wrong Way (Cash Basis): You’d recognize $25,000 in Month 1 when the deposit hits and another $25,000 in Month 3 upon final payment. Your books show lumpy revenue that completely misrepresents when your team actually did the work.

The Correct Way (ASC 606): You must recognize revenue based on the progress toward completing your performance obligation—in this case, building the website. A common way to measure this is the percentage of completion method, based on hours worked. Assume a total project budget of 100 hours.

| Month | Hours Worked | % of Project Complete | Recognized Revenue |

|---|---|---|---|

| Month 1 | 30 hours | 30% | $50,000 × 30% = $15,000 |

| Month 2 | 50 hours | 50% | $50,000 × 50% = $25,000 |

| Month 3 | 20 hours | 20% | $50,000 × 20% = $10,000 |

| Total | 100 hours | 100% | $50,000 |

This method perfectly aligns your recognized revenue with your agency's actual delivery of services each month, giving you a true picture of monthly profitability and resource utilization.

Red Flags: Common ASC 606 Mistakes to Avoid

Adopting ASC 606 isn’t a one-time project. The standard demands constant judgment, and one wrong step can throw your financials into disarray, spook investors, and lead to painful audit findings. The trick is to spot these problems internally before an auditor or investor does.

Here are the most common red flags we see and what you should do instead.

Red Flag 1: Misidentifying Performance Obligations

The most frequent error is bundling distinct services together. You look at a single contract price and think it represents a single service, but ASC 606 forces you to unbundle every specific promise.

- The Mistake: Your contracts lump software access, a one-time setup fee, and ongoing technical support into a single line item. You then recognize that entire contract value evenly over the subscription term.

- What to Do Instead: Treat each of those promises as a separate performance obligation. A one-time setup fee is a distinct service; its revenue should be recognized when the setup is complete, not spread out. Unbundling is the key to getting the timing right.

Red Flag 2: Incorrectly Allocating the Transaction Price

Even if you identify the performance obligations correctly, you can still stumble by misallocating the total contract price. The price must be divided up based on the standalone selling price (SSP) of each component—what you would charge for each item if you sold it separately.

- The Mistake: You allocate the price based on what looks convenient or helps you hit an internal target, such as assigning a nominal $1 value to a setup fee to push more revenue into the recurring software subscription.

- What to Do Instead: You need to establish and document a clear, defensible basis for each item's SSP. If you don't sell something on its own, you must estimate its fair value using a consistent method, like a cost-plus-margin analysis. This gives you a solid foundation that will stand up to scrutiny.

Red Flag 3: Expensing Sales Commissions Upfront

This one trips up a lot of founders. The common mistake is to expense all sales commissions the moment they're paid out. But under ASC 340-40 (the companion guide to ASC 606), commissions paid to acquire a contract must be capitalized and then amortized over the period you expect to benefit from that contract (i.e., the customer lifetime).

- The Mistake: Your P&L shows a huge, lumpy sales commission expense in the month a big deal closes, distorting your profitability.

- What to Do Instead: Treat commissions as a contract asset on your balance sheet. Then, you amortize that asset over the expected customer life, matching the expense to the revenue it helped generate. According to OpenView's 2024 SaaS Benchmarks, the median customer lifetime for scaling SaaS is 3-5 years, providing a solid benchmark for your amortization period.

Your Action Plan for ASC 606 Compliance

Knowing the five steps is one thing. Building a system that produces audit-ready financials every single month is another. This isn't about turning you into an accountant. It's about creating a scalable, repeatable process that stands up to scrutiny from investors, auditors, or potential buyers.

Use this table as your roadmap to move from theory to execution.

| Step | Action Item | Why It's Critical |

|---|---|---|

| 1. Draft Policy | Create a formal Revenue Recognition Policy document. It must outline your judgments on performance obligations, SSPs, and variable consideration. | This is the first document an auditor will ask for. It creates consistency and proves you have a systematic approach. |

| 2. Deconstruct Contracts | Systematically review your standard agreements to identify and list every distinct performance obligation (e.g., software, setup, support). | This is the only way to correctly unbundle your services and get your revenue timing right from the start. |

| 3. Map Systems | Map the data flow between your CRM (e.g., Salesforce), payment processor (e.g., Stripe), and accounting software (e.g., QuickBooks, NetSuite). | Spreadsheets won't scale. Automation is key to accuracy and efficiency. For more on this, see Mastering Revenue Recognition with Stripe. |

| 4. Set Up Entries | Configure the specific journal entries for deferred revenue, monthly revenue recognition, and commission capitalization/amortization. | This is the technical backbone of compliance, ensuring your balance sheet and P&L are always in sync with ASC 606 rules. |

| 5. Build Controls | Establish a formal review and approval process for any new or non-standard contracts that come through the door. | Compliance isn't a one-time project. Strong controls prevent new contracts from breaking your carefully built system. |

This whole process can feel overwhelming. The goal is to move from manual, error-prone accounting to a system that builds trust and supports your growth. You’re building a financial engine, not just ticking a compliance box.

Frequently Asked Questions About ASC 606

Even with a solid game plan, you likely still have questions about what ASC 606 really means for your business. Here are the answers to the questions we get asked the most.

How Does ASC 606 Affect SaaS Metrics Like MRR and ARR?

This is a huge one for any subscription business. Think of ASC 606 as a filter that makes your Monthly Recurring Revenue (MRR) and Annual Recurring Revenue (ARR) more accurate and—most importantly—defensible. It smooths out the financial lumps you get from annual prepayments or uneven cash collection.

The standard forces you to separate true, recurring software revenue from one-time fees like setup or implementation. This gives investors a crystal-clear, stable view of your contractual recurring revenue. That’s the number they really care about when they’re trying to figure out how healthy and scalable your company is.

Do We Really Need to Comply If We Are a Small Company?

Yes. Absolutely. If you have any plans to raise money, get a serious bank loan, or sell your company, your financials are going under a microscope. Investors and lenders live in a world governed by Generally Accepted Accounting Principles (GAAP), and that means ASC 606 compliance is non-negotiable.

"A common misconception among early-stage founders is that GAAP compliance is something you can 'bolt on' later. The reality is that waiting creates a massive financial and operational debt that you'll be forced to pay down during the most critical moments of your company's life—like a funding round or acquisition. Start clean, stay clean." — Scott Orn, Managing Partner at Kruze Consulting

Getting it right early on saves you from the nightmare of a costly, time-consuming restatement of your historical financials right when a high-stakes deal is on the line.

Can My Bookkeeper Handle This Implementation?

Probably not. And that's no knock on your bookkeeper. Basic bookkeeping is usually about cash-basis accounting—tracking money as it comes in and goes out. That’s a fundamentally different skillset than what ASC 606 requires.

Proper implementation demands deep expertise in accrual accounting. It means making complex judgments about performance obligations and contract allocations, plus having the technical chops to map and integrate financial systems. This is controller-level or fractional CFO work, plain and simple. You need that expertise to get it right and keep it right, especially as your contracts get more complex.

Navigating ASC 606 is a major project, but you don’t have to tackle it alone. If this action plan shines a light on gaps in your current process, we can help. Jumpstart Partners specializes in implementing these audit-ready ASC 606 workflows to deliver the investor-grade financials you need to scale.

Schedule a free consultation today to assess your current process and build your roadmap for compliance.