Financial Operations

Deferred Revenue: The SaaS Founder's Guide to Unlocking Growth

Unsure what is deferred revenue? This guide explains how to account for it, its impact on your financials, and why it's a key metric for investors.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readDeferred revenue is one of the most powerful—and most misunderstood—metrics on your company's balance sheet. In short, it’s the cash you’ve collected for a service or product you have not yet delivered. It’s a liability because it represents a promise you still have to fulfill, but for founders of growing SaaS and service businesses, it's also your single best indicator of future growth.

Stop Misreading Your Revenue and Stalling Your Growth

Confusing the cash in your bank account with the revenue you’ve actually earned is a dangerous mistake that distorts your financial reality, leads to poor strategic decisions, and makes savvy investors skeptical. For SaaS companies, digital agencies, and professional services firms that bill upfront, mastering this concept isn't just an accounting checkbox—it's non-negotiable for building a predictable, scalable business.

Let’s use a simple example. A new customer signs up on January 1st and pays you $12,000 upfront for an annual software subscription. Your bank account is $12,000 richer, which is fantastic for your cash flow. But you haven't earned that money yet. According to Generally Accepted Accounting Principles (GAAP), you only earn it as you deliver the service—in this case, $1,000 each month over the next year.

The initial $12,000 you collected goes onto your balance sheet as a deferred revenue liability. Every month, you’ll move $1,000 from that liability account over to your income statement as earned revenue.

Why This Distinction Matters

The gap between a cash receipt and earned revenue is fundamental to understanding your company's true financial health. Misinterpreting a high deferred revenue balance can lead to disaster, while understanding it unlocks strategic advantages.

"A growing deferred revenue balance is one of the clearest signs of a healthy subscription business. It's tangible proof that customers are committing to you for the long term, effectively funding your future growth." - David Kellogg, former CEO of Host Analytics

This table clarifies the critical distinction between cash received from a customer and the revenue your business has actually earned.

| Concept | Cash Inflow | Earned Revenue |

|---|---|---|

| When It's Recorded | The moment a customer pays you. | As you deliver the product or service over time. |

| Financial Statement | Affects the Statement of Cash Flows. | Affects the Profit & Loss (P&L) Statement. |

| What It Represents | A promise to deliver future value. | The value you have successfully delivered. |

| Example (SaaS) | A $12,000 annual payment received on Jan 1st. | $1,000 recognized each month from Jan to Dec. |

Properly tracking deferred revenue helps you:

- Forecast Accurately: It transforms unpredictable cash spikes into a smooth, predictable revenue stream—the bedrock of solid budgeting and strategic planning.

- Impress Investors: Experienced investors scrutinize your deferred revenue balance. They see it as tangible proof of future performance and strong customer loyalty.

- Maintain Compliance: Correct revenue recognition is a core requirement of accounting standards like ASC 606, which governs how companies handle contracts with customers.

According to OpenView's 2023 SaaS Benchmarks report, top-performing SaaS companies consistently show a high ratio of deferred revenue to total ARR, often exceeding 50%. This indicates a strong preference for annual upfront payments, which is a sign of a healthy, mature sales motion.

Ultimately, misreading your revenue isn't just an accounting slip-up; it's a strategic blind spot. A huge part of this is building a product that people stick with, so implementing strategies to reduce customer churn is paramount for protecting and growing that future revenue balance. For a deeper dive into how this metric fits with others, check out our guide on ARR vs. MRR.

How to Calculate Deferred Revenue: A Practical SaaS Example

Theory is one thing, but watching the numbers move is what makes the concept click. Let's walk through a real-world SaaS scenario to see exactly how deferred revenue flows through your financial statements.

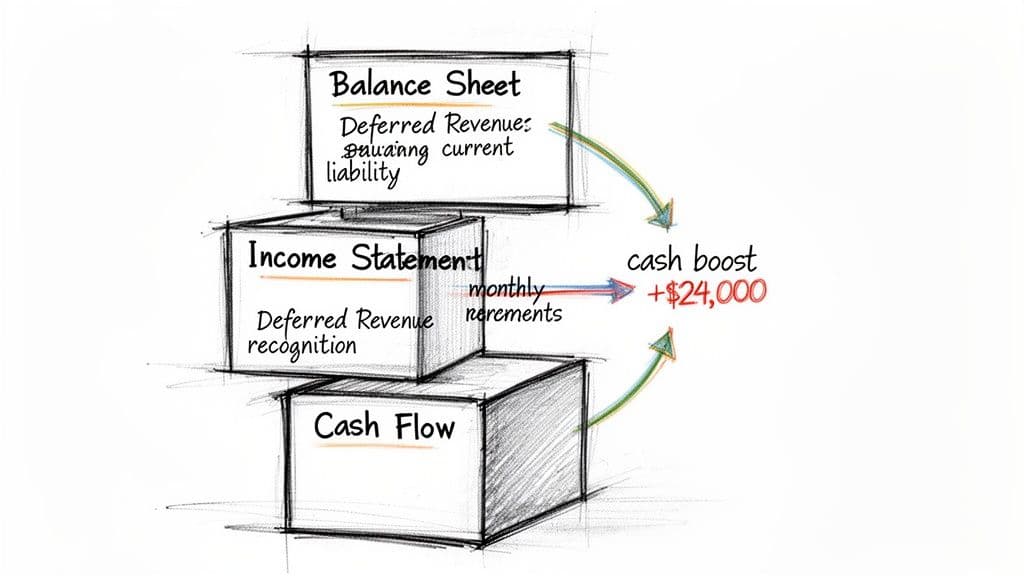

Imagine your SaaS company lands a new client on a $24,000 annual contract. They pay the full amount upfront on January 1st. That single transaction kicks off a series of accounting entries that unfold over the entire year.

The diagram above nails the core lifecycle: cash comes in, you hold it as a liability (because you owe a service), and then you recognize it piece by piece as you deliver on that promise.

Step 1: The Initial Journal Entry on January 1st

The second that $24,000 payment hits your bank, it must be recorded. Since you haven't delivered any service yet, none of it is revenue. Instead, you'll make two entries that only affect your balance sheet.

Here’s the journal entry:

- Debit (Increase) Cash: Your cash account jumps by $24,000. This shows up immediately on your Statement of Cash Flows.

- Credit (Increase) Deferred Revenue: You create a liability called Deferred Revenue for the same $24,000. This line item on your balance sheet acknowledges that you owe your new client a full year of service.

At this stage, your Profit & Loss (P&L) statement is completely untouched. You haven't "earned" a single dollar of revenue from this deal yet.

Step 2: Monthly Revenue Recognition

As your team delivers the software month after month, you fulfill one-twelfth of your obligation to the client. This means you can finally start recognizing a portion of that deferred revenue as earned revenue.

The calculation is simple:

$24,000 (Total Contract Value) / 12 months = $2,000 per month

On January 31st (and at the end of every following month), you’ll make this adjusting journal entry:

- Debit (Decrease) Deferred Revenue: You reduce your deferred revenue liability by $2,000.

- Credit (Increase) Earned Revenue: You increase your earned revenue on the P&L by $2,000.

You repeat this exact process every single month. Here’s how the deferred revenue balance shrinks over the first quarter as you earn it.

| Date | Transaction | Earned Revenue (P&L) | Deferred Revenue (Balance Sheet) |

|---|---|---|---|

| Jan 1 | Initial Payment | $0 | $24,000 |

| Jan 31 | Month 1 Recognition | +$2,000 | $22,000 |

| Feb 28 | Month 2 Recognition | +$2,000 | $20,000 |

| Mar 31 | Month 3 Recognition | +$2,000 | $18,000 |

By December 31st, you will have recognized the full $24,000 as revenue, and your deferred revenue balance for this contract will be back to $0. This methodical process ensures your revenue figures are accurate and reflect the true performance of your business. For a deeper dive into the official rules, check out our guide on SaaS revenue recognition under ASC 606.

The Impact of Deferred Revenue on Your Financials

Deferred revenue doesn’t live in a vacuum—it actively shapes your three core financial statements. For founders and finance leaders, understanding its ripple effects is critical. It’s the connection between the cash you collect today and the performance you report tomorrow, and both investors and auditors will scrutinize how well you manage it.

The Balance Sheet: Your Promise to Customers

First up is the Balance Sheet. When a customer pays you upfront, that cash creates a liability: deferred revenue.

It's classified as a current liability because it represents a short-term obligation you must fulfill, typically within the next 12 months. Think of it as a formal IOU to your customers. A rising deferred revenue balance is a healthy sign, showing strong sales and a growing pipeline of future work.

The Income Statement: Where Revenue is Earned

Next is the Income Statement, or Profit & Loss (P&L). The full deferred revenue balance never appears here. Instead, only the portion you actually earn each month gets recognized.

Following our $24,000 annual contract example, only $2,000 hits your P&L each month as earned revenue. This methodical process aligns your revenue with the actual delivery of your service—a core principle of the ASC 606 revenue recognition standard. This is what smooths out your top-line revenue, turning lumpy annual payments into the predictable monthly income streams that investors love to see.

The Cash Flow Statement: The Immediate Benefit

Finally, the Statement of Cash Flows tells the story of your liquidity. The moment that $24,000 annual payment lands in your bank, it immediately boosts your Cash from Operating Activities.

This upfront cash is a massive strategic advantage. According to a survey on The Kaplan Group's website, 93% of businesses experience revenue loss from late payments. The upfront cash from annual contracts sidesteps this problem, allowing you to invest in growth using your customers' own funds and reducing the need for external financing.

This table summarizes how deferred revenue interacts with each financial statement, offering a clear reference for you and your finance team.

| Financial Statement | How Deferred Revenue Appears | Business Implication |

|---|---|---|

| Balance Sheet | Appears as a current liability, representing your obligation to deliver future services. | A growing balance indicates strong sales momentum and a healthy pipeline of future revenue. |

| Income Statement | The total balance does not appear. Only the monthly earned portion is recognized as revenue. | Creates a smooth, predictable revenue stream that reflects true business performance over time. |

| Cash Flow Statement | The full upfront payment is recorded as cash from operations upon receipt. | Provides immediate working capital to fund growth, hiring, and product development. |

To ensure all your statements are accurate and connected, you might find value in our detailed guide on how to prepare financial statements.

Using Deferred Revenue as a Strategic Growth Metric

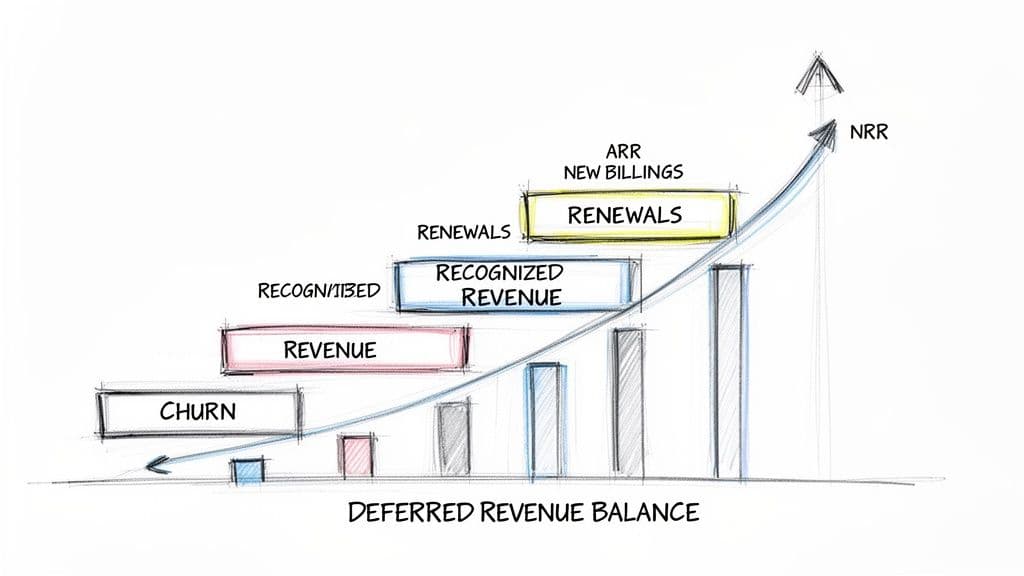

Stop thinking of deferred revenue as just an accounting liability. For any SaaS or service-based business, it's one of the most powerful leading indicators of future growth. A steadily climbing deferred revenue balance is hard proof of strong new sales, successful renewals, and happy customers—all before a single dollar hits your P&L.

Investors understand this. They don't just see a liability; they see a backlog of guaranteed future performance. When you learn to analyze this metric correctly, you stop simply reporting numbers and start telling a compelling story about your company's momentum.

Unlocking Insights with the Deferred Revenue Waterfall

The best way to see what's really going on is with a deferred revenue waterfall. This is a month-over-month report that tracks the flow of cash from new billings into your deferred revenue account, and then how it trickles out into recognized revenue over time. This analysis shows you precisely how prepayments turn into earned income, revealing deep insights into your contract health and business velocity.

Your waterfall should answer a few critical questions at a glance:

- Momentum: Is our deferred revenue balance growing, shrinking, or flat? Growth is what you want to see.

- Sales Performance: How much did new bookings and renewals add to the balance this period?

- Churn Impact: How much did we lose from customers churning or downgrading their plans?

Connecting Deferred Revenue to Key SaaS Metrics

Deferred revenue doesn't live in a vacuum. Its true power comes from connecting it to other vital metrics that paint a complete picture of your company's health. Understanding its place among other 6 key metrics for SaaS businesses is what separates good operators from great ones.

Here’s how it intersects with two of the most critical:

- Annual Recurring Revenue (ARR): Your deferred revenue balance is a direct reflection of your ARR and billing cycles. A high deferred revenue figure relative to your ARR is a great sign—it means you have a healthy number of customers paying annually upfront, which is fantastic for cash flow.

- Net Revenue Retention (NRR): A stable or growing deferred revenue balance goes hand-in-hand with strong NRR. When customers renew and expand their contracts (upsells), they add to your deferred revenue, signaling that they're happy and your product is sticky.

"Your deferred revenue balance is the single best predictor of your next 12 months of revenue. If it’s growing, your business has a strong pulse. If it’s shrinking, you need to find out why—fast." - Mark G. B. CPA, Strategic Finance Advisor

This interconnected view is exactly what sophisticated investors want to see. It shows you have a deep, fundamental understanding of your business drivers.

Benchmarking Your Performance

So, how does your deferred revenue stack up? While every business is different, industry benchmarks provide a useful yardstick. As you scale and successfully push for more annual contracts, your deferred revenue-to-ARR ratio should climb significantly.

SaaS Deferred Revenue Benchmarks as a Percentage of ARR (Source: OpenView SaaS Benchmarks)

| Company Stage (Revenue) | Typical Deferred Revenue (% of ARR) | Primary Driver |

|---|---|---|

| Early Stage (<$5M) | 10% - 25% | Primarily monthly billing cycles |

| Growth Stage ($5M - $25M) | 25% - 40% | Mix of monthly and annual contracts |

| Scale-Up ($25M - $100M) | 40% - 60% | Strong push for annual prepayments |

| Enterprise (>$100M) | 60%+ | Multi-year contracts, enterprise sales motion |

As your company matures, your ability to secure longer-term, prepaid contracts increases, directly boosting the deferred revenue balance and strengthening your financial foundation. For more insights into the metrics that matter most, see our guide on the most essential SaaS financial metrics.

Red Flags: Common Deferred Revenue Mistakes That Kill Deals

Getting deferred revenue wrong isn't just a back-office accounting task—it’s a critical failure that can make or break your next funding round or acquisition. The smallest error sends a clear signal to investors and buyers: your financial house is not in order. Get this wrong, and you risk a collapsed deal or a painful hit to your company’s valuation.

Mistake 1: Booking Multi-Year Deals as Immediate Revenue

It’s incredibly tempting to book a two-year, $100,000 contract as revenue the day it's signed. This is the most dangerous mistake you can make. It wildly overstates your performance and creates a completely distorted financial picture that violates the core principles of accrual accounting.

- The Fix: Record the full $100,000 as a deferred revenue liability on your balance sheet. Then, recognize the revenue evenly over the 24-month contract term—that's $4,166.67 per month. This reflects your true performance and builds a predictable, defensible revenue stream.

Mistake 2: Using Messy Spreadsheets to Track Everything

When you only have a few contracts, a spreadsheet seems fine. As you scale, managing deferred revenue waterfalls in Excel becomes a recipe for disaster. Manual data entry, broken formulas, and version control nightmares introduce a huge risk of human error that poisons your financial reports.

"A messy deferred revenue schedule is a massive red flag in due diligence. It tells a buyer that you lack scalable financial processes, which immediately makes them question the reliability of all your numbers." – M&A Advisor for SaaS Companies

- The Fix: Invest in real accounting software with a dedicated revenue recognition module (like QuickBooks Online Advanced or NetSuite) as early as you can. Automation ensures accuracy, provides a clean audit trail, and grows with your business.

Mistake 3: Forgetting ASC 606 Performance Obligations

The ASC 606 standard requires you to identify and account for separate performance obligations within a single deal. A $50,000 contract might include $40,000 for software access, $5,000 for a one-time implementation fee, and $5,000 for premium support.

- The Fix: Break down every contract into its distinct deliverables. Assign a standalone selling price to each component and recognize the revenue only as each specific obligation is fulfilled. Lumping them together is non-compliant and will fail an audit.

Mistake 4: Misclassifying Deferred Revenue During M&A

When you’re selling your company, buyers may try to reframe your deferred revenue as a "debt-like" item, arguing that because they have to spend resources to service those prepaid contracts, the value of that future work should be deducted from your purchase price.

- The Fix: Work with your financial advisor to frame deferred revenue as what it truly is: a powerful asset. It represents a pipeline of guaranteed future revenue from a committed customer base. Having a clean and detailed financial due diligence checklist helps you organize the data you need to confidently defend your valuation.

Automate Revenue Recognition and Get Investor Ready

If you're still wrestling with deferred revenue in a spreadsheet, you're not just wasting time—you're exposing your business to serious, unnecessary risk. Manual tracking is slow, riddled with human error, and completely lacks the audit trail that investors and auditors demand. A single broken formula can send a shockwave through your entire financial model, leading to a crisis of confidence during due diligence.

Your Actionable Next Steps

- Assess Your Current Process: Are you using spreadsheets to track deferred revenue? If you have more than 20 contracts, it's time to upgrade.

- Evaluate Accounting Software: Research platforms like QuickBooks Online Advanced or NetSuite that have built-in revenue recognition modules compliant with ASC 606.

- Get Expert Guidance: Software is only a tool. Partner with a financial expert who can implement the right system, build compliant workflows, and transform your data into strategic insights.

An experienced financial partner will help you:

- Implement the Right System: We'll help you choose and configure the accounting software that fits your business model.

- Build Compliant Workflows: We design and implement ASC 606-compliant processes for identifying performance obligations and recognizing revenue correctly.

- Deliver Strategic Insights: We analyze your deferred revenue trends, forecast future performance, and build financial models that withstand intense investor scrutiny.

Get Investor-Ready Financials with a 5-Day Close

For founders heading into a funding round or an audit, having clean, accurate, and timely financials isn't optional—it’s table stakes. At Jumpstart Partners, we don’t just manage your books; we build the financial infrastructure you need to scale with total confidence.

"A fast, accurate month-end close isn’t a 'nice-to-have'—it’s the heartbeat of a well-run company. It gives you the real-time data needed to make quick, informed decisions and provides the proof of operational excellence that investors demand." - CPA & Outsourced Controller

We specialize in putting these systems into action. We’ll migrate you from messy spreadsheets to a robust accounting platform, build out your ASC 606-compliant workflows, and deliver a guaranteed 5-day month-end close. The result is a set of investor-ready financials you can trust, no questions asked.

Ready to get your deferred revenue under control and unlock your company’s true potential? Book a consultation with Jumpstart Partners today.

Common Questions About Deferred Revenue

Applying these concepts to your own business always brings up a few specific questions. Here are the most common misconceptions and questions we hear from founders.

Is Deferred Revenue the Same as Unearned Revenue?

Yes, they’re identical. Deferred revenue and unearned revenue are two names for the same accounting concept: cash you’ve received for a product or service you haven't delivered yet. It's always a liability on your balance sheet because it represents an obligation to your customer.

How Does ASC 606 Change How We Calculate Deferred Revenue?

ASC 606 forces you to get much more specific by breaking down your customer contracts into distinct performance obligations. You can only recognize revenue as each individual promise is fulfilled.

For a $30,000 annual SaaS deal, you must unbundle it:

- $24,000 for software access (recognized monthly over the year).

- $4,000 for a one-time implementation service (recognized only when setup is complete).

- $2,000 for premium support (recognized monthly over the year).

You have to track, defer, and recognize revenue for each component on its own schedule. This complexity makes manual spreadsheets completely unmanageable.

Misconception: "Deferred revenue is just an accounting problem."

This is false. A growing deferred revenue balance is one of the most powerful signals of a healthy, scalable business. It's not just an accounting line item; it tells a story about your future growth and momentum.

When investors see your deferred revenue climbing, it proves three things they love:

- Guaranteed Future Revenue: You have a strong, predictable pipeline of income already locked in.

- Strong Product-Market Fit: Customers believe in your value enough to pay you upfront.

- Healthy Cash Flow: You’re collecting cash ahead of service delivery, which funds growth without needing to raise more capital.

Put simply, it's one of the clearest signs that you're building a top-tier subscription business.

Can Deferred Revenue Ever Be a Negative Number?

No, that’s not possible. Deferred revenue represents cash you've already been paid for work you still owe. The balance can be zero or positive, but it can never go below zero. If you ever see a negative number in your deferred revenue account, it’s a red flag that points to a serious error in your bookkeeping.

Managing deferred revenue correctly is non-negotiable if you want to scale your business and impress investors. At Jumpstart Partners, we put the systems and expertise in place to ensure your financials are always audit- and investor-ready. Book a consultation today to get complete confidence in your numbers.