Financial Operations

Accounting for Consulting Services: A Founder's Guide

Master accounting for consulting services with our guide on ASC 606, project profitability, and KPIs. Built for founders of growing $500K-$20M service firms.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readThe professional services market was valued at nearly $5.7 trillion in 2018, and the accounting and management consulting segment is projected to reach $0.83 billion in 2026 according to NetSuite's consulting services KPI overview. That growth creates opportunity, but it also punishes sloppy finance.

If you run a consulting firm, agency, or services-heavy SaaS business, accounting isn't just a back-office function. It determines whether you can see margin erosion early, invoice on time, defend your numbers in diligence, and explain performance to investors without hand-waving.

Most founders think they need better bookkeeping. What they need is accounting for consulting services built around projects, labor economics, and revenue timing. Standard small-business books answer one weak question: “Did we make money this month?” Strong services accounting answers the question that matters: “Which clients, projects, and delivery decisions are making us money, and which ones are draining cash?”

Why Standard Bookkeeping Fails Consulting Firms

Generic bookkeeping fails services firms because it treats labor like a monthly expense instead of your core production engine. In a consulting business, your team's time is the inventory. Once a day passes with misallocated hours, unapproved time, or bad project coding, you can't recover that visibility later.

A basic QuickBooks setup usually gives you a clean P&L at the company level. That's useful, but incomplete. If all your revenue sits in one bucket and all payroll sits in another, you can't tell whether Client A is funding growth or whether Client B is consuming senior staff time and crushing margin.

Company profit is not project profit

That distinction matters more as you scale. A firm can show positive net income while hiding significantly unprofitable work inside “good” revenue. That's how founders get blindsided. Revenue grows, the bank account feels tight, and nobody can explain why.

Here's the operational reality:

- Revenue concentration hides weak work when large invoices mask low-margin delivery.

- Payroll timing distorts monthly optics because salaries hit now, while billing may lag.

- Scope creep disappears in generic books when extra hours never get tied back to a client or project.

- Pricing mistakes survive too long because nobody sees margin by service line.

Practical rule: If your financials can't show profitability by client, project, and service line, you're not managing a consulting firm. You're managing a checking account.

Consulting firms need a different accounting lens

Accounting for consulting services has to connect four moving parts. Contract value, labor effort, delivery cost, and invoicing timing. If even one of those sits in a spreadsheet outside your accounting system, your reporting degrades fast.

That's why project-based visibility isn't optional in a growing firm. You need financial statements that tie directly to operational decisions such as staffing, pricing, write-offs, and collections.

A standard setup tells you what happened. A services-focused setup tells you what to fix.

Use this test:

| Standard bookkeeping view | Services accounting view |

|---|---|

| Monthly revenue total | Revenue by client and project |

| Total payroll expense | Direct labor vs overhead labor |

| Accounts receivable balance | AR by project, aging, and billing status |

| Company-wide gross profit | Delivery margin by engagement |

| Bank balance | Bank balance plus unbilled work and deferred obligations |

If you want investor-ready reporting, the process begins here. Investors and buyers don't trust firms that can't reconcile growth to delivery economics. If margin falls, they want to know whether pricing broke, utilization slipped, or project controls failed. Your accounting system should answer that in minutes, not after a week of manual digging.

Building Your Services-Focused Chart of Accounts

Your chart of accounts determines what you can see later. If it's messy, your reporting will stay messy. If it's too generic, every important decision turns into manual analysis.

For a consulting firm, the chart of accounts should stay lean but deliberate. You need enough structure to separate project economics from overhead, without creating a bloated ledger no one maintains consistently. If you need a primer on account structure, start with this guide on what a chart of accounts is.

What to separate from day one

The biggest mistake is mixing direct delivery costs with operating expenses. Billable labor, subcontractors, and software tied directly to client work belong in cost of services. Executive salaries, admin payroll, rent, and general software belong below gross profit.

That separation is what makes project profitability possible.

Here's a practical starting point.

| Account Type | Specific Accounts |

|---|---|

| Revenue | Consulting Revenue Fixed Fee, Consulting Revenue Time and Materials, Retainer Revenue, Pass-Through Revenue |

| Cost of Services | Direct Labor Client Delivery, Subcontractor Costs, Project Software, Client Travel Reimbursable or Non-Reimbursable |

| Operating Expenses | Admin Payroll, Sales and Marketing, Rent, Insurance, Recruiting, General Software, Founder Compensation |

| Assets | Cash, Accounts Receivable, Unbilled Revenue, Prepaids |

| Liabilities | Accounts Payable, Accrued Expenses, Deferred Revenue, Payroll Liabilities |

| Equity | Owner Contributions, Distributions, Retained Earnings |

Why accrual accounting is non-negotiable

Cash-basis books are fine for very small operators who only care about taxes and bank balance. That isn't your situation if you're trying to scale, raise capital, or manage delivery.

Accrual accounting matches revenue and expenses to the period when the work happens. That matters in consulting because the invoice date and the delivery date are often different. If you bill a deposit upfront, cash comes in before you've earned the revenue. If you complete work before invoicing, you've earned revenue before cash arrives.

Without accrual accounting, your P&L lies at exactly the moments when you most need clarity.

The chart of accounts should match how you sell

Your account structure should reflect your actual business model, not accounting textbook categories.

For example:

- Fixed-fee projects need separate revenue tracking because margin risk sits in delivery efficiency.

- Time-and-materials work needs clean ties between hours, billing rates, and recognized revenue.

- Retainers should stand apart because they affect forecasting and capacity planning differently.

- Pass-through costs need visibility so they don't inflate apparent delivery performance.

Keep the chart tight. Complexity belongs in classes, customers, projects, and departments inside QuickBooks, Xero, or NetSuite. It does not belong in an endless list of duplicate GL accounts.

A clean chart of accounts gives you the raw material for every other system. Revenue recognition, project P&Ls, month-end close, and board reporting all depend on it.

Mastering Revenue Recognition with ASC 606

If you're still recognizing revenue when you send an invoice, you're reporting your billing process, not your business performance.

ASC 606 requires you to recognize revenue when you satisfy performance obligations. In consulting, that often means recognizing revenue over time as work is performed. NetSuite notes that consulting firms commonly use an input method based on hours worked, and that firms automating this process reduce billing discrepancies by 30% while avoiding the 15% to 20% overstatement of revenue common with manual WIP tracking in their analysis of consulting firms in this guide to accounting for consultants.

If you want a deeper implementation view, this overview of ASC 606 revenue recognition is a useful companion.

The five-step logic in plain English

ASC 606 sounds technical, but the business logic is straightforward.

-

Identify the contract

You need a real agreement with scope, payment terms, and enforceable rights. -

Identify the performance obligations Determine what you've promised to deliver.

-

Determine the transaction price

Set the total amount you expect to earn. -

Allocate the price if needed

If the contract includes multiple obligations, assign value across them. -

Recognize revenue when the work is satisfied

For many consulting projects, that means recognizing revenue over time based on labor progress.

Worked example for a fixed-fee consulting project

Assume you sign a $60,000 fixed-fee engagement over three months. Your team estimates 300 total hours to complete the project.

Under the input method, revenue recognized equals:

Hours completed / Total estimated hours × Contract value

Now assume your team logs:

- Month 1: 90 hours

- Month 2: 120 hours

- Month 3: 90 hours

That gives you:

| Month | Hours completed | Cumulative completion | Revenue recognized that month |

|---|---|---|---|

| Month 1 | 90 | 30% | $18,000 |

| Month 2 | 120 | 70% cumulative | $24,000 |

| Month 3 | 90 | 100% cumulative | $18,000 |

If you invoiced $20,000 upfront at kickoff, you still would not recognize $20,000 immediately just because cash hit the bank. In Month 1, you would recognize only $18,000 if that's the portion earned through delivery.

What hits the books

At contract signing, when the upfront invoice goes out:

- Debit Accounts Receivable $20,000

- Credit Deferred Revenue $20,000

When cash is collected:

- Debit Cash $20,000

- Credit Accounts Receivable $20,000

At the end of Month 1, once $18,000 has been earned:

- Debit Deferred Revenue $18,000

- Credit Consulting Revenue $18,000

If, later in the project, earned revenue exceeds invoiced amounts, the excess sits in Unbilled Revenue until you invoice it.

That distinction matters:

| Term | What it means | Why founders should care |

|---|---|---|

| Deferred Revenue | Cash collected before work is earned | Cash is strong, but revenue isn't earned yet |

| Unbilled Revenue | Work delivered before invoicing | You've created value, but haven't converted it to AR yet |

| Recognized Revenue | Revenue earned under ASC 606 | This is what belongs on the P&L |

Revenue timing affects more than compliance. It shapes lender confidence, investor trust, and how credible your growth story looks under diligence.

Common misconception founders need to drop

The biggest misconception is “we got paid, so it's revenue.” It isn't. Cash collection and revenue recognition are related, but they are not the same event.

The second mistake is relying on manual WIP spreadsheets. Once your delivery team logs time in one system, PMs review scope in another, and finance updates revenue in a third spreadsheet, errors become predictable. That's when overstatement happens, billing drifts, and audit support turns painful.

If you want clean financials, tie approved time entries directly to project budgets and recognition rules. That turns ASC 606 from a compliance burden into a management tool.

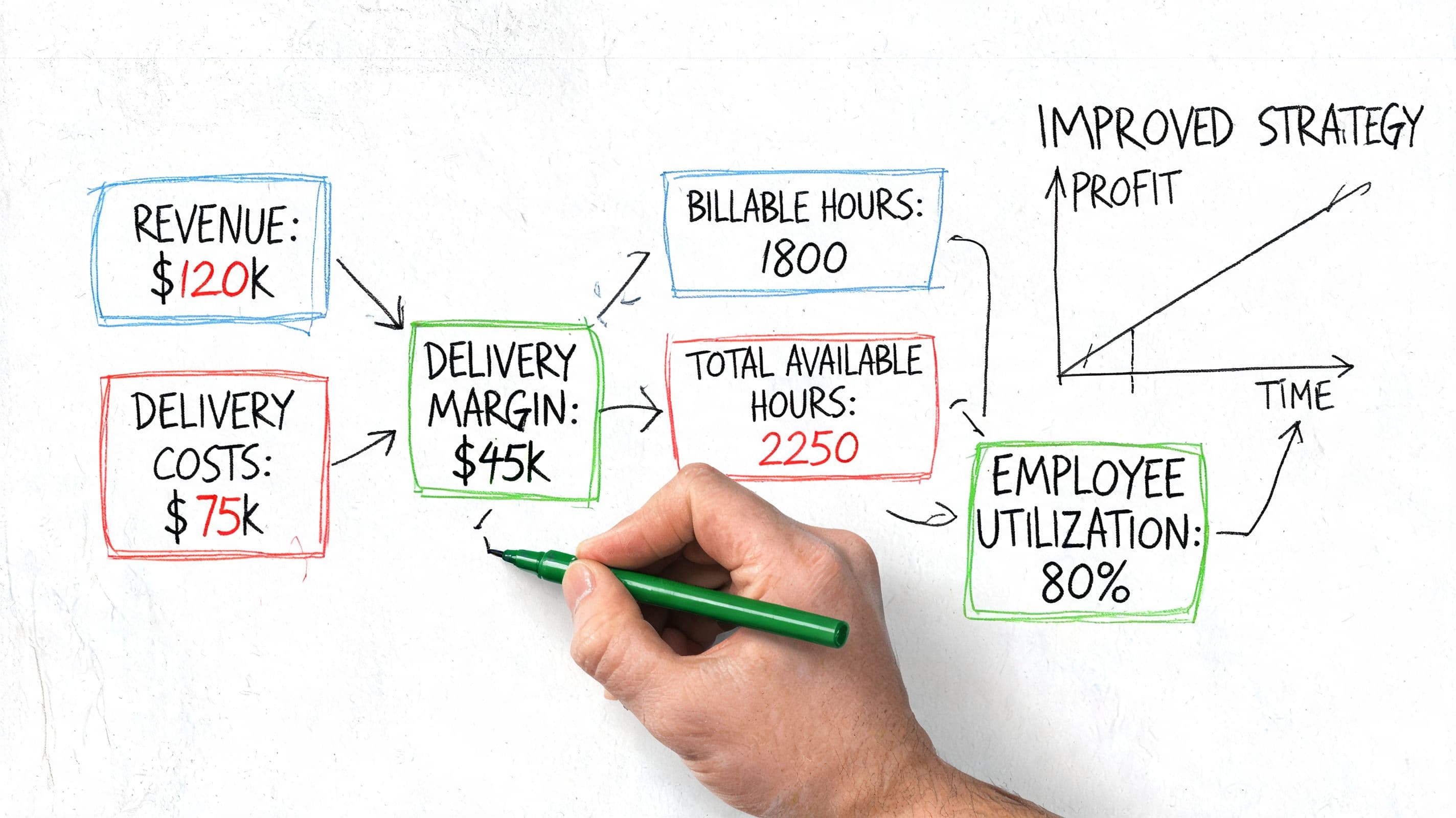

How to Calculate and Improve Project Profitability

Project profitability is where accounting becomes strategy. This is the number set that tells you whether growth is healthy or just expensive.

The core KPI is Delivery Margin, calculated as (Revenue - Direct Costs) / Revenue. According to SMLS Advisors' accounting guidance for consultants, a healthy delivery margin typically falls between 60% and 70%.

If your projects consistently land below that range, you don't have a bookkeeping problem. You have a pricing, staffing, or scope-control problem.

A sample project P&L

Let's use a simple project example.

Assume a client project generates $60,000 in revenue. Direct costs tied to delivery are:

- Direct labor: $18,000

- Subcontractor cost: $4,000

- Project software and direct expenses: $2,000

Total direct costs = $24,000

Delivery Margin =

($60,000 - $24,000) / $60,000 = 60%

That project sits at the low end of the healthy range.

| Project P&L line | Amount |

|---|---|

| Revenue | $60,000 |

| Direct labor | $18,000 |

| Subcontractors | $4,000 |

| Project software and direct expenses | $2,000 |

| Total direct costs | $24,000 |

| Delivery margin | 60% |

That's the baseline. If the same project had run $6,000 over in direct labor because scope expanded and nobody approved a change order, total direct costs become $30,000. Delivery Margin falls to 50%. The client still sees a successful engagement. Your P&L does not.

If you need a simple framework to calculate your cost of sales, use that before you debate pricing. A lot of firms skip straight to rate changes without first identifying what belongs in direct delivery cost.

Delivery margin is only one lens

Strong operators pair delivery margin with two practical checks.

First, employee utilization. If expensive delivery staff spend too much time on internal work, margin erodes even when pricing looks fine.

Second, effective billable rate. This tells you whether realized revenue per hour matches the rate assumptions built into your pricing model.

You don't need a complicated dashboard to start. You need consistent project coding, approved timesheets, and direct costs booked to the right job.

Founders often celebrate top-line growth while project economics quietly deteriorate. Revenue is not proof of profit. Margin is.

For a deeper client-level framework, this guide to agency profitability and true client ROI shows how to connect account performance to actual economics.

Red flags that deserve immediate action

When these show up, don't wait until quarter-end.

- Margin compression on your biggest accounts. Large clients can hide weak pricing because absolute revenue looks impressive.

- Repeated write-offs after invoice review. That usually means poor scope control or weak budget discipline.

- Senior team members doing junior work. Your cost base rises while the client price stays fixed.

- Projects with lots of unbilled hours. Teams are working, but finance can't monetize the effort cleanly.

- Profitability debates that rely on opinions. If account managers and finance produce different numbers, your system design is broken.

Here's a useful training resource to align operations and finance on the same metrics before you change process:

What to do when a project is underperforming

Don't jump to layoffs or price hikes first. Diagnose the actual cause.

| Problem | Likely root cause | Best response |

|---|---|---|

| Margin below target from kickoff | Underpricing | Rebuild pricing model and minimum deal thresholds |

| Margin declines mid-project | Scope creep | Tighten change-order approvals |

| Good revenue, weak cash | Slow invoicing or collections | Fix approval-to-invoice workflow |

| Strong utilization, weak margin | Wrong staff mix | Reassign delivery layers and reduce senior over-service |

The goal isn't perfect project performance. The goal is catching deterioration while you still have options.

Optimizing Invoicing and Cash Flow

Profit on the P&L doesn't fund payroll. Cash does. That's why invoicing design matters as much as pricing.

Most consulting firms don't have a revenue problem. They have a cash conversion problem. Work gets done, hours sit unapproved, invoices go out late, and collections start even later. By the time cash lands, you've already paid salaries tied to that work.

Pick an invoicing model that matches delivery reality

Different billing models create different cash patterns.

| Billing model | Cash flow profile | Operational burden | Best fit |

|---|---|---|---|

| Fixed fee | Predictable if invoiced on milestones or upfront | Requires strong scope control | Defined deliverables |

| Time and materials | More responsive to actual effort | Requires disciplined time tracking | Variable-scope work |

| Retainer | Smoothest cadence | Requires careful expectation management | Ongoing advisory or embedded support |

Fixed-fee work gives cleaner forecasting, but it punishes poor delivery discipline. Time-and-materials is fairer when scope changes, but only if time entry approval is fast and reliable. Retainers improve planning, but they can hide over-servicing if you don't review effort against the agreement.

Follow the dollar through the system

In a healthy process, the flow looks like this:

- Time and direct costs are recorded to the project.

- Finance reviews what has been earned and what can be billed.

- Unbilled work moves to an invoice.

- The invoice moves into accounts receivable.

- Cash is collected and matched cleanly.

Every delay in that chain creates a financing burden on your business.

If you want to tighten collections discipline, this overview of accounts receivable management covers the operational side well.

Common objections that hurt cash flow

Founders often resist tighter billing because they think it creates client friction. Usually, the opposite is true. Clients dislike surprise invoices and vague backup. They don't object to timely, accurate invoices tied to approved work.

The other bad assumption is that invoicing once a month is “cleaner.” It's only cleaner for your team if your clients are effectively financing your delivery costs. That's a poor trade.

If your team logs time daily but invoices monthly after a long approval delay, you've built a working-capital gap into the business by choice.

Use these rules:

- Invoice from approved time, not estimated memory

- Bill deposits or kickoff amounts on fixed-fee work

- Set milestone invoices where delivery value is obvious

- Push disputed items into a fast review loop, not a month-end pile

- Make one person accountable for invoice release timing

A consulting firm with solid margins can still run short on cash. Usually the culprit isn't profitability. It's lag.

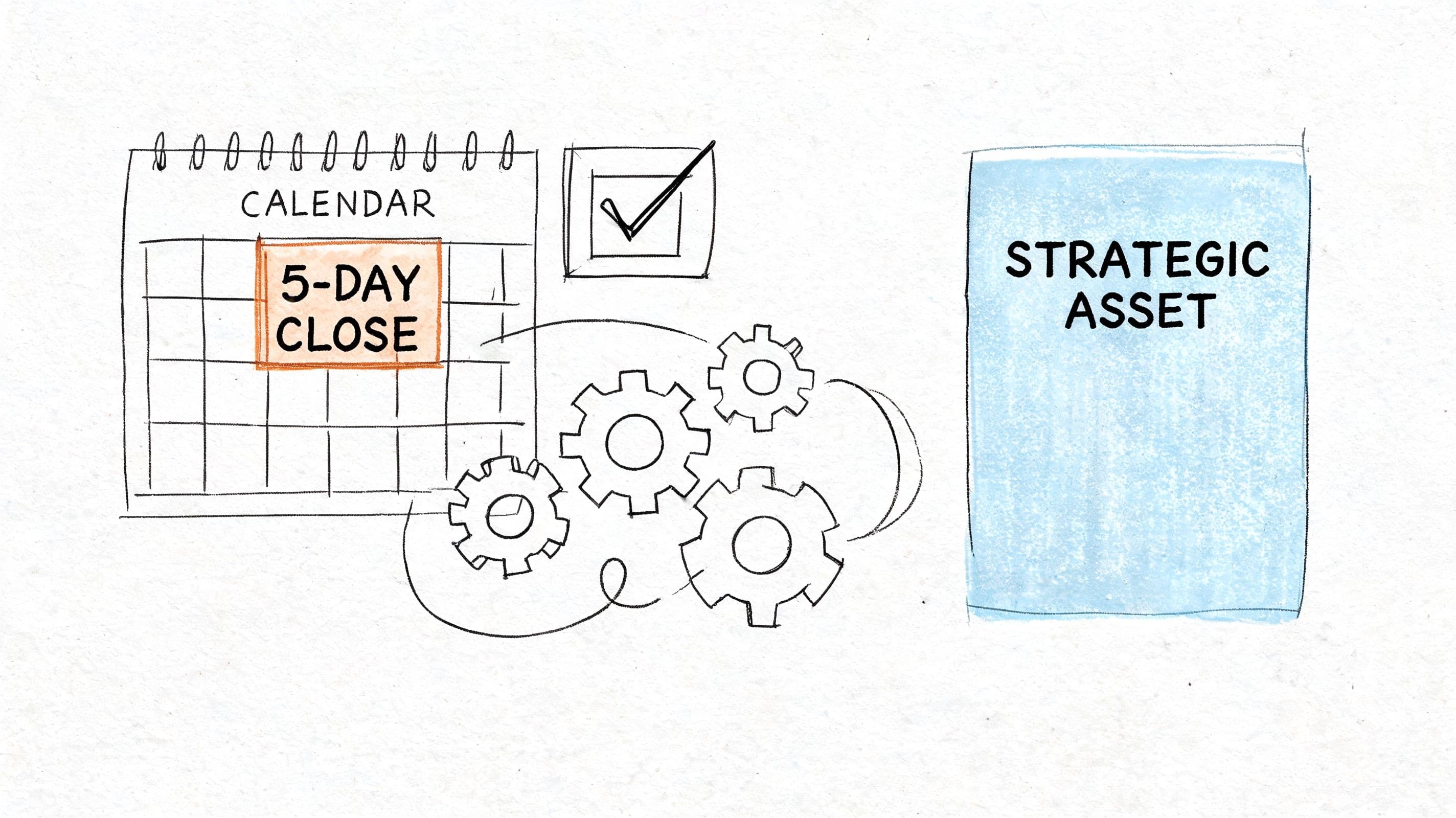

The 5-Day Month-End Close for Consulting Firms

A messy close tells you your operating system is weak. A fast close tells you finance and delivery are speaking the same language.

For a consulting firm, the close has one job. Convert operational activity into reliable financials quickly enough that leadership can still act on them. If you're waiting weeks for project numbers, the data is already stale.

If your process is still chaotic, this checklist of month-end close best practices is the right place to tighten controls.

What has to happen during close

The close shouldn't rely on heroics. It should follow a fixed sequence.

| Close step | Why it matters |

|---|---|

| Lock timesheets and project coding | Prevents late changes from distorting labor reporting |

| Review unbilled work | Captures earned revenue not yet invoiced |

| Update deferred revenue balances | Keeps deposits from inflating earned revenue |

| Reconcile direct costs by project | Protects delivery margin accuracy |

| Reconcile bank, AR, and AP | Anchors the financial statements to reality |

| Produce management reporting package | Turns accounting output into decisions |

What belongs in the reporting package

Don't stop at the three statements. Founders need operating visibility, not just GAAP output.

A useful monthly package for accounting for consulting services should include:

- P&L by month and year-to-date

- Balance sheet with commentary on unbilled and deferred balances

- Cash flow summary

- Project profitability by client or engagement

- AR aging with owner by account

- Brief narrative on margin movement and billing issues

The real advantage of a fast close

A fast close improves management behavior. Teams stop debating stale numbers and start fixing current issues.

Here's the difference in practice:

- A slow close tells you in retrospect that margins were weak.

- A fast close tells you quickly enough to adjust staffing, invoice timing, or project controls in the current month.

Close speed is not vanity. It determines how long bad assumptions survive inside the business.

If you want investor-ready reporting, enforce deadlines on timesheets, invoice approvals, and accrual reviews. Finance can't close fast if operations is casual.

Choosing Your Tech Stack or Outsourced Partner

A bad finance stack does more than slow down bookkeeping. It distorts utilization, hides project margin problems, delays invoices, and makes revenue quality look weaker in diligence.

Spreadsheets fail consulting firms once delivery volume rises and billing rules get less uniform. If time tracking sits in one system, invoicing lives in another, and ASC 606 adjustments happen in a manual month-end file, you lose control of the numbers that drive cash flow. Founders feel that failure in slow collections, surprise margin compression, and board meetings spent arguing over which report is right.

You have two workable options. Build a services-focused finance stack with clear ownership, or hire an outsourced team that already knows how consulting economics flow through the books.

The DIY stack

Build internally if you have someone who can design the process and enforce it across delivery, finance, and payroll. Software does not fix sloppy inputs.

At minimum, your stack should include:

- Accounting system such as QuickBooks Online, Xero, or NetSuite

- Time tracking tied to clients, projects, phases, and service lines

- Project or PSA system for budgets, staffing plans, and delivery oversight

- Payroll system that maps labor cleanly to departments or project cost buckets

- Reporting layer that shows project margin, unbilled revenue, deferred revenue, AR aging, and cash visibility

Choose tools based on reporting outcomes, not feature lists. If the stack cannot show earned but unbilled revenue, actual labor cost by project, and margin by engagement manager without spreadsheet repair, it is not good enough for a growing consulting firm.

When outsourcing makes more sense

Outsource once finance complexity starts affecting decisions. That point usually arrives before founders expect it.

Bring in outside support when these conditions show up:

- You are heading into fundraising, lender diligence, or an audit

- Revenue recognition depends on project status, milestones, retainers, or prepaid blocks

- Project profitability reports arrive late or change after close

- Invoice approvals bottleneck with founders because the underlying numbers are not trusted

- The team can produce statements, but cannot explain margin shifts, cash conversion, or unbilled balances clearly

An outsourced controller team can usually fix this faster than a piecemeal hiring plan. The right partner sets policy, cleans up the chart of accounts, aligns systems, and turns month-end output into operating metrics management can use.

Jumpstart Partners is one example of that model. It provides outsourced controller and bookkeeping support for growing businesses using platforms like QuickBooks, Xero, and NetSuite. That approach makes sense when you need better project accounting and a faster close before you are ready to build a full internal finance bench.

Make the decision based on economics. If bad reporting causes delayed billing, missed scope creep, or weak margin visibility, the finance function is already costing you money. Fix it before diligence starts, while you still have time to improve cash flow, clean up revenue quality, and present a stronger operating story to investors.

If your firm is growing and your accounting still can't show project margin, unbilled revenue, and a reliable close without manual cleanup, it's time to fix the system. Jumpstart Partners helps services businesses build investor-ready financials, improve cash visibility, and run accounting like an operating function instead of an afterthought.