Financial Operations

606 Revenue Recognition: A Guide for SaaS & Agencies

Master ASC 606 revenue recognition with this guide for SaaS and agencies. Learn the 5-step model, see worked examples, and get an audit-ready checklist.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··25 min readIf your revenue recognition is sloppy, your valuation story is sloppy.

That sounds harsh, but it’s true. Investors don’t just look at growth. They look at whether your growth is real, repeatable, and reported correctly. If your MRR, ARR, deferred revenue, and implementation fees don’t tie back to a defensible 606 revenue recognition policy, your diligence process gets slower, your audit gets uglier, and your credibility drops fast.

This hits hardest in SaaS, agencies, and recurring-service businesses because your contracts rarely fit a simple cash-in, revenue-out model. You bill annually. You bundle onboarding with subscriptions. You add usage fees, discounts, support, and change orders. Then someone exports the contract data into Excel and hopes the schedule works itself out. It won’t.

Why 606 Revenue Recognition Will Make or Break Your Next Funding Round

A funding round can stall on one revenue memo. That is not an exaggeration. Once investors, lenders, or audit teams see that your revenue policy is vague, inconsistent, or trapped in spreadsheets, they stop debating your growth story and start questioning the reliability of your numbers.

Founders often treat ASC 606 as an accounting technicality. It is a valuation issue. If revenue is recognized too early, your ARR, margins, and retention profile look stronger than they are. If revenue is deferred incorrectly, you can undersell the business and create avoidable volatility in board reporting. Either way, diligence gets slower and more expensive.

For SaaS and agency leaders, the core problem is operational. ASC 606 does not fail in theory. It fails in the accounting system. A contract says one thing, the invoice says another, and QuickBooks or NetSuite gets whatever your team could force into the chart of accounts that month. That gap is where diligence problems show up.

If you need a plain-English baseline first, start with this explanation of what ASC 606 revenue recognition means. Then get practical. Your investors will care less about whether your controller can recite the five steps and more about whether your system can produce a defensible revenue schedule by contract, by SKU, and by period.

Why founders should care

Revenue timing changes the story your numbers tell.

A SaaS company that books onboarding fees upfront can make one quarter look great and the next three look soft. An agency that treats a retainer like earned-on-invoice revenue can overstate current performance if the work is delivered across the month. A usage-based contract without a clear estimate policy can turn forecasted revenue into reported revenue too early. Those are not minor accounting misses. They distort the metrics investors use to price risk.

Here is the CEO test. If an investor asks how implementation fees, annual prepaids, usage charges, and contract modifications flow through revenue, your team should answer in two ways. First, with a clear policy. Second, with reports pulled directly from the system.

That is what matters when you are securing your next funding round. Clean ASC 606 treatment gives investors confidence that your ARR bridge, gross margin trend, and deferred revenue balance can survive diligence.

What changed in plain English

ASC 606 replaced a patchwork of old industry rules with one model for recognizing revenue from customer contracts. The accounting rule itself is not the hard part. The hard part is applying it consistently across real contracts that include subscriptions, onboarding, discounts, change orders, retainers, overages, and milestone billing.

For a founder, four questions matter:

- What exactly did we promise the customer?

- What portion of the contract price belongs to each promise?

- When is each promise delivered?

- What should stay in deferred revenue until delivery happens?

If your team cannot answer those questions quickly, with support from QuickBooks or NetSuite rather than a manual spreadsheet, you have a finance infrastructure problem. And finance infrastructure problems become valuation discounts fast.

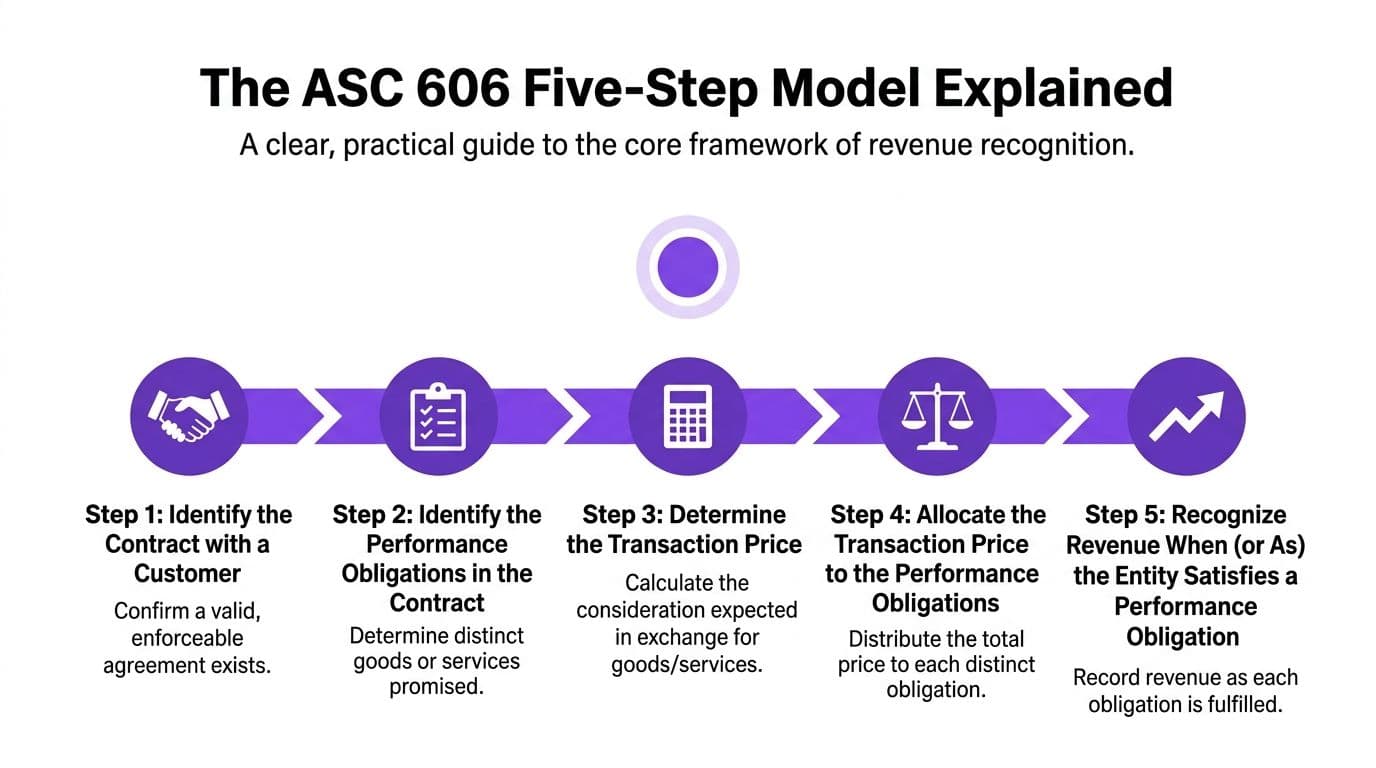

The ASC 606 Five-Step Model Explained

ASC 606 isn’t complicated because the model is unclear. It’s complicated because real contracts are messy. The framework itself is straightforward.

If you want a plain-language primer before you operationalize it, this overview of what ASC 606 revenue recognition means is a useful starting point.

Step 1 Identify the contract

You need a valid agreement with enforceable rights and payment terms. That can be a signed MSA, order form, SOW, or recurring subscription agreement. If collectibility is questionable or the arrangement isn’t clearly enforceable, you don’t have a normal starting point for revenue recognition.

For a digital agency, this often means separating a vague “we’ll help with growth” proposal from an actual contract with scope, fees, and approval terms. For SaaS, it usually means the executed order form and the governing subscription terms.

Step 2 Identify the performance obligations

A performance obligation is a distinct promise to deliver a good or service. Many companies become lax in this area, prompting auditors to investigate closely.

If you sell a website redesign plus ongoing hosting, those may be separate promises. If you sell SaaS access plus a meaningful implementation project, you need to decide whether the implementation is distinct or whether it’s part of a combined promise.

A simple non-SaaS example helps:

| Contract item | Distinct obligation | Typical recognition pattern |

|---|---|---|

| Custom website build | Usually yes | As work is performed if progress is measurable, or at completion if not |

| Monthly hosting | Yes | Over time |

| One-time training session | Usually yes | When delivered |

Step 3 Determine the transaction price

This is the amount you expect to receive. Not just the list price. The actual economics.

That includes fixed fees and any variable consideration such as usage fees, discounts, credits, rebates, or performance-based amounts. If part of the deal depends on future behavior, you estimate it and apply a constraint so you don’t overstate revenue.

Revenue recognition under 606 is about earned economics, not billing mechanics.

A practical website-agency example:

- Fixed build fee for the project

- Monthly maintenance retainer

- Bonus fee if launch happens by a certain date

The fixed build fee is easy. The bonus fee is variable. You don’t book it just because sales says it’s “very likely.”

Step 4 Allocate the transaction price

If one contract includes multiple obligations, you allocate the total consideration across them based on standalone selling price, often called SSP.

That means you don’t dump the whole contract value into the first deliverable. You split the economics across what you promised.

A founder mistake I see all the time is treating upfront cash collection as proof that the upfront work earned most of the revenue. It doesn’t. Billing terms and revenue recognition are not the same thing.

Step 5 Recognize revenue when or as you satisfy the obligation

This is the final step, and it’s where your income statement changes.

You recognize revenue either:

- Over time, as the customer receives the benefit, or

- At a point in time, when control transfers

For SaaS subscriptions, the customer benefits continuously as they access the platform, so over-time recognition is usually the answer. For a one-time training workshop, revenue is usually recognized when the session is delivered.

A simple worked example

Assume your agency signs a contract for:

- Website build for $12,000

- Hosting for $12,000 over 12 months

Total contract value is $24,000.

If the build and hosting are distinct obligations and the SSPs match the contract prices, you allocate:

- $12,000 to build

- $12,000 to hosting

If the website is delivered at launch, you recognize the build revenue when that obligation is satisfied. Hosting is recognized ratably over the year at $1,000 per month.

That’s the core of 606 revenue recognition. Figure out what you sold, determine the true contract value, split it logically, and recognize it when earned.

Applying ASC 606 to SaaS and Agency Contracts

This section is where finance teams either prove they understand the contract or expose that they are still booking off invoices.

SaaS and agency agreements rarely sell one clean thing. They mix subscription access, onboarding, implementation, support, usage, prepaid retainers, milestones, and mid-contract changes. If your team treats that mix as one billing stream, revenue is wrong. Wrong revenue means weak board reporting, lower confidence in your numbers, and more friction in diligence.

For SaaS companies, the operational problem is usually system design. Billing may sit in Stripe or Chargebee, cash lands in the bank, product usage lives in the app database, and revenue is posted in QuickBooks or NetSuite. If those systems are not tied together, your close depends on spreadsheet patches. That breaks fast at scale. A cleaner accounting setup for SaaS companies gives finance a defensible path from contract to journal entry. Teams trying to shortcut that process with trends like Vibe Accounting usually end up with books that look polished but fail under audit.

SaaS example with setup fees and annual billing

Start with a common SaaS contract:

- Annual subscription fee of $120,000

- Setup fee of $10,000

If the setup work does not transfer a distinct standalone benefit to the customer, do not recognize it upfront. In plain English, if the customer bought the platform and setup only helps them get on the platform, the economics belong with the subscription.

The accounting result is usually simple:

- Total consideration = $130,000

- Revenue recognized over the service term

For a one-year term, that is often:

- $130,000 / 12 = about $10,833 per month

That treatment matters for valuation. Front-loading setup revenue flatters early months, then leaves weaker later periods. Investors notice the pattern quickly, especially when deferred revenue and ARR disclosures do not line up. According to Stripe’s ASC 606 guide, 70% of SaaS revenue is ratable under ASC 606, and misallocating bundled obligations like setup fees can inflate early-period earnings by 25%.

SaaS example with usage-based pricing

Now add variable pricing:

- Fixed two-year subscription of $200,000

- Usage fee of $0.08 per API call

You cannot book expected usage for the next 24 months and call it revenue. You need an estimate for variable consideration, and that estimate has to be constrained so you do not recognize revenue that is likely to reverse later. Then you update it as actual usage comes in.

The fixed subscription would usually be recognized over the contract term, or about $8,333 per month across 24 months. Usage revenue should be tied to actual activity and the contract terms, not to a sales forecast sitting in a pipeline report.

That is the CFO point. Product data is now accounting data. If finance cannot trace billed usage to recognized revenue, deferred balances, and contract support, your revenue memo is weak and your fundraising deck is exposed.

Agency example with retainers and milestones

Agency contracts create a different failure mode. The team invoices a deposit or a monthly retainer and books revenue the same day.

That is lazy accounting.

A monthly retainer is usually recognized over the service period. If the client prepays on the first of the month, you still earn the revenue as the month passes.

Milestone projects require more judgment. Some milestones represent real transfer of value. Others are just billing checkpoints written to manage cash flow. Revenue follows performance, not the invoice schedule.

Here is the practical treatment:

| Contract type | Billing pattern | Better 606 treatment |

|---|---|---|

| Monthly retainer | Invoice at start of month | Recognize over the service month |

| Fixed-fee website build | Deposit, progress invoice, final invoice | Recognize based on actual transfer of control or measured progress |

| Strategy workshop | Invoice upfront | Recognize when workshop is delivered |

| Hosting plus support | Annual prepay | Defer and recognize over time |

If you run an agency and want cleaner margins, cleaner month-end reporting, and fewer diligence questions, separate billing operations from revenue policy. They are not the same function.

Contract modifications matter more than founders expect

Upsells, downgrades, paused work, term extensions, and scope changes are accounting events. They change the revenue schedule. They can also change deferred revenue, contract assets, and the pattern of recognition.

A SaaS customer adding seats mid-term may require a prospective update to the recognition schedule. An agency change order can create a new performance obligation or modify an existing one. If your rule is "just add another invoice," your books will drift away from the contract.

That drift gets expensive during an audit or funding round because finance then has to rebuild history deal by deal.

What auditors want to see

Auditors want a system, not a story.

They usually ask for:

- Contract inventory tied to signed agreements

- Documented performance obligations

- Standalone selling price support for bundles

- Revenue schedules tied to the general ledger

- Deferred revenue roll-forward

- Support for variable consideration estimates

- Documented treatment of amendments, renewals, and upsells

This short explainer is worth watching if you want a quick operational view before rebuilding your process:

If your current process depends on invoice dates, payment receipts, and manual spreadsheet overrides, you are not applying ASC 606 in a way investors or auditors will trust. You are running a temporary workaround. That is fine at $500,000 in revenue. It is a real problem when you are raising capital, preparing for audit, or trying to defend valuation.

Sample Journal Entries and Accounting System Setups

Most founders don’t need more theory. They need to know what is recorded in their books.

Here’s the basic rule. Cash collection does not equal revenue. Under 606 revenue recognition, upfront billing usually creates a liability first, then revenue gets recognized as you perform.

If you need a refresher on how revenue flows through the chart of accounts, this plain-English guide to the general ledger and how it works helps connect the journal entries to the financial statements.

Sample journal entries for a prepaid SaaS contract

Assume a 12-month, $12,000 SaaS contract billed and collected upfront. The customer gets platform access evenly over the year.

Sample ASC 606 Journal Entries for a 12-Month, $12,000 SaaS Contract

| Date | Account | Debit | Credit |

|---|---|---|---|

| Contract start | Cash | $12,000 | |

| Contract start | Deferred revenue | $12,000 | |

| End of month 1 | Deferred revenue | $1,000 | |

| End of month 1 | SaaS revenue | $1,000 | |

| End of month 2 | Deferred revenue | $1,000 | |

| End of month 2 | SaaS revenue | $1,000 |

That pattern continues monthly until the deferred revenue balance is fully recognized by the end of the term.

What non-compliant books usually look like

A lot of small teams book this instead:

| Event | Debit | Credit |

|---|---|---|

| Cash collected | Cash $12,000 | Revenue $12,000 |

That entry is simple. It’s also wrong if the service hasn’t been delivered yet.

Reality check: Your bank account measures cash. Your income statement measures performance.

How to set this up in QuickBooks, Xero, and NetSuite

The accounting logic is universal. The software execution isn’t.

QuickBooks Online and QuickBooks Online Advanced

QuickBooks can handle deferred revenue, but it won’t save you from a bad contract analysis. You still need:

- A consistent contract review process before invoices are posted

- A deferred revenue liability account mapped correctly

- Monthly recurring journal entries or a recognition schedule

- Clear linkage between invoices, services periods, and revenue release

For a simple annual prepaid subscription, QuickBooks can work if volume is low and someone owns the schedule. Once you add setup fees, usage-based pricing, or contract modifications, manual QuickBooks workflows get fragile quickly.

Xero

Xero is fine for clean, simple recurring contracts. It gets painful when you need contract-level allocation logic, amendment tracking, or audit-ready support for standalone selling price. At that point, teams often export data to spreadsheets, which creates version-control problems immediately.

NetSuite

NetSuite is stronger for multi-element arrangements, recurring schedules, and more formal revenue automation. It’s the better fit when you have:

- Multiple entities

- Higher contract volume

- SaaS deals with bundled services

- A real audit or institutional diligence process

The catch is implementation discipline. NetSuite’s module won’t fix undefined performance obligations or sloppy SSP policies. It just automates whatever logic you feed it.

My recommendation by stage

| Your situation | Better approach |

|---|---|

| Simple recurring billing, low contract complexity | QuickBooks with a documented monthly deferred revenue schedule |

| Mixed retainers, projects, and annual prepaids | QuickBooks or Xero plus a formal contract review workflow |

| Multi-year SaaS contracts, usage fees, frequent amendments | NetSuite or a dedicated revenue tool tied to your GL |

| Heavy spreadsheet dependency | Rebuild the workflow before adding volume |

If your finance stack still depends on tribal knowledge and month-end heroics, study how teams are approaching Vibe Accounting. The useful takeaway isn’t style. It’s that modern finance functions need systems that are fast, readable, and operator-friendly. Revenue recognition is no exception.

Common ASC 606 Pitfalls That Trigger Audits

Revenue mistakes rarely start with exotic accounting. They start with ordinary deals, booked the wrong way, month after month, until an auditor or investor asks for support and the team has none.

That is why ASC 606 issues show up so often in diligence. Buyers and auditors are not hunting for trivia. They are testing whether your finance function can explain how revenue moves from contract to system to general ledger. If that chain breaks, they question the numbers, the controls, and management judgment.

If you want a better sense of how these issues surface in diligence, review this guide on what auditors examine when auditing a business.

Red flags an auditor will question

Setup fees recognized upfront without a distinct benefit

Founders hear, “We did the onboarding work in month one, so book the fee in month one.” That logic fails under ASC 606 if the customer cannot benefit from that setup on its own.

For a SaaS company, implementation, onboarding, and data migration often support the subscription rather than stand alone as a separate deliverable. For an agency, a kickoff or strategy fee may still be part of a broader retainer relationship. If the setup work is not distinct, recognize it over the same period as the related service. Booking it all upfront inflates early revenue and drags future periods down.

SSP that nobody can defend

A lot of companies allocate contract value across software, onboarding, training, and managed services using numbers pulled from memory. That is not a policy. It is improvisation.

You need a repeatable standalone selling price method that your team can explain without confusion. In practice, that means using actual pricing data, approved ranges, or a documented estimation approach. If your controller, auditor, and CFO would each allocate the same deal differently, your policy is weak and your revenue schedule is exposed.

Contract modifications handled outside the accounting system

This is one of the biggest real-world failures I see. Sales executes an upsell. Customer success agrees to a downgrade. Someone extends the term by email. Finance finds out later, usually during close.

ASC 606 does not forgive side agreements or scattered approvals. Amendments change transaction price, performance obligations, timing, or all three. If modifications live in Salesforce notes, inbox threads, or unsigned PDFs instead of QuickBooks or NetSuite workflows, your revenue schedule is already unreliable.

Variable consideration booked like a forecast

Usage fees, overages, performance bonuses, and success fees cause trouble because operators blur forecasting with accounting.

A forecast belongs in the board deck. Recognized revenue belongs in the books only when your method is supportable and properly constrained. SaaS companies get this wrong with consumption pricing. Agencies get it wrong with media rebates, commissions, and performance-based fees. If finance cannot show the rule for what gets recognized now versus later, expect an audit comment.

If sales assumptions drive revenue recognition, but accounting has no memo, no approval trail, and no system rule, you have a controls failure.

Spreadsheet dependence creates audit risk fast

Spreadsheets are not the problem by themselves. Uncontrolled spreadsheets are.

A manual revenue file usually fails in three places. The contract data is incomplete. The logic changes without review. The resulting journal entries do not tie cleanly to deferred revenue and recognized revenue by customer or contract. QuickBooks teams feel this first because they often bolt revenue schedules onto billing reports. NetSuite teams can create the same mess if they automate bad contract data.

Auditors care about the math, but they also care about evidence. Who changed the file? Which contract version did they use? Where is the approval? If your answer is “ask Sarah, she knows the sheet,” your process is not audit-ready.

Other warning signs

- Deferred revenue does not reconcile to contract schedules. That usually means someone is posting top-side fixes after the fact.

- Executed contracts are stored in multiple places. Finance cannot apply a consistent policy if it cannot find the final agreement.

- Revenue treatment changes by deal owner. Two similar contracts should not produce different answers because different people reviewed them.

- The revenue policy lives in tribal knowledge. If one controller departure can break the close, the control never existed.

- Materiality is used as a shortcut. Small errors repeated across contracts become a pattern, and patterns attract scrutiny.

The fix is operational

Stop treating ASC 606 as a memo-writing exercise. Treat it like a revenue operations workflow that feeds your accounting system correctly.

For SaaS and agency companies, the fix is straightforward:

- Centralize signed contracts and amendments before month-end close

- Map each contract type to clear performance obligations

- Write an SSP policy your team can effectively apply

- Set rules for setup fees, usage fees, renewals, and modifications

- Tie every revenue schedule to the GL and deferred revenue rollforward

- Review non-standard deals before revenue is posted, not after

That is the actual standard. Not theory. Execution.

Companies that handle this well protect valuation, shorten diligence, and avoid ugly cleanup work right before a fundraise.

Your ASC 606 Migration Checklist and Timeline

A bad ASC 606 rollout does not fail in the policy memo. It fails in the close process, the contract handoff, and the audit binder you cannot support under pressure.

If you are six months from a fundraise, audit, or lender review, the clock is already running. Fixing revenue recognition after diligence starts burns leadership time, delays financial delivery, and gives investors a reason to discount your numbers. That is avoidable.

If your historical books are messy, clean that up first. A policy will not save bad source data. If you need to repair the underlying records before building compliant schedules, start with this guide to QuickBooks cleanup services for messy historical books.

Six months before audit or fundraising

Start with scope, ownership, and system reality.

Do not begin in Excel. Begin with the contracts you sell and the accounting system you use, whether that is QuickBooks today or NetSuite after the next round.

- Inventory every live contract type: SaaS subscriptions, implementation packages, onboarding fees, agency retainers, project SOWs, usage pricing, renewals, discounts, and amendment forms.

- Group contracts by accounting outcome: Standard monthly SaaS should not sit in the same bucket as a custom agency engagement with milestones and overages.

- Write a usable revenue policy: Define performance obligations, variable consideration, SSP, contract modifications, and the trigger for revenue recognition in plain language your team can apply.

- Assign one process owner: The controller, CFO, or outsourced finance lead owns the decision. Sales, legal, and client success contribute inputs. They do not make revenue policy.

- Decide where schedules will live: QuickBooks usually needs a controlled external schedule. NetSuite can handle more natively, but only if the contract setup is clean.

Three months before audit or fundraising

Now convert policy into a workflow your team can repeat every month.

A finance team should be able to take a signed contract, review it once, post it correctly, and reproduce the answer on demand. If that is not true, you do not have an ASC 606 process. You have a set of opinions.

Build a contract review checklist

Every new contract and amendment should answer these questions before revenue is posted:

| Question | Why it matters |

|---|---|

| What did the customer actually buy? | Identifies performance obligations |

| Are any fees variable, usage-based, or contingent? | Affects transaction price and constraints |

| Are multiple services bundled into one price? | Drives SSP allocation |

| Is recognition over time or at a point in time? | Sets the revenue pattern |

| Did the contract modify an existing arrangement? | May change future recognition and deferred revenue treatment |

Test your policy on real contracts

Use actual signed deals, not hypothetical examples from an accounting memo.

Test at least one contract from each major revenue stream. For a SaaS company, that usually means annual prepaid subscriptions, onboarding packages, mid-term seat expansions, and usage-based billing. For an agency, test monthly retainers, fixed-fee projects, milestone billing, and change orders.

Look for the deals that usually break the process:

- Setup and onboarding fees

- Annual prepayments

- Usage-based pricing

- Milestone or deliverable-based projects

- Upsells, downgrades, and renewals with changed terms

If your policy only works for the easiest deals, it is not ready.

One month before audit or fundraising

At this point, theory is over. You need support that ties cleanly from contract to schedule to general ledger to financial statements.

- Finalize contract-level revenue schedules: Each material contract should show booking date, term, allocations, revenue by month, and deferred revenue balance.

- Tie schedules to the GL: Deferred revenue, recognized revenue, and any contract assets must reconcile exactly.

- Centralize support: Keep signed agreements, amendments, memos, calculations, and approvals in one controlled folder or system.

- Review reporting outputs: Your monthly financial package should present revenue consistently across the P&L, balance sheet, and board materials.

- Run a dry diligence request: Ask someone outside the day-to-day close to pull support for a sample contract. If it takes an hour, your process is still weak.

What to stop doing now

These habits create cleanup work, audit comments, and credibility problems.

- Stop booking cash receipts to revenue unless performance is complete

- Stop using invoice dates as your recognition rule

- Stop tracking the actual schedule in one person's spreadsheet

- Stop approving custom sales terms without finance review

- Stop treating amendments as minor admin work

- Stop assuming your accounting system is right because the invoice posted correctly

A rollout sequence that works

Use this order.

- Clean historical books if the base data is unreliable

- Inventory and group contract types

- Write the policy for real deal terms, not textbook examples

- Test actual contracts across each revenue stream

- Build schedules that tie to the GL

- Configure QuickBooks or NetSuite around the policy

- Train sales, finance, and operations on approval rules

- Run the monthly close the same way every time

The common mistake is buying software first and deciding the accounting later. Reverse that. First define how your SaaS subscriptions, agency retainers, setup fees, and contract changes should be recognized. Then configure the system to produce that answer consistently. That is what makes diligence easier, audits cleaner, and your revenue story more credible in a funding round.

Turn Compliance into a Strategic Advantage

Good 606 revenue recognition does more than satisfy auditors. It sharpens how you run the company.

When revenue is tied to actual performance obligations, your MRR and ARR become more credible. Your deferred revenue tells a clearer story. Your board reporting gets cleaner. Your fundraising narrative gets tighter because investors can trust the timing and quality of your earnings.

You also get better operating visibility. You can see which contracts create predictable recurring revenue, which deal structures distort margins, and where sales is introducing accounting complexity that finance needs to price or control. That’s useful long before an audit starts.

Clean revenue recognition doesn’t lower ambition. It makes your growth story believable.

If your current process depends on spreadsheets, invoice dates, or unwritten judgment calls, fix it before your next audit or financing event. The best time to clean up 606 revenue recognition is before someone else asks for the backup.

If you want help getting your revenue recognition audit-ready, Jumpstart Partners works with SaaS, agencies, and service businesses to clean up books, implement ASC 606 workflows, and produce investor-ready financials without the usual month-end chaos.