Financial Operations

A Founder's Guide to Accounting for SaaS: Investor-Ready Financials

Master accounting for SaaS with this guide on ASC 606, deferred revenue, and key metrics. Build investor-ready financials and drive scalable growth.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readSaaS accounting isn't just regular accounting with a different name. It’s a completely different way of thinking about your finances, built specifically for the subscription model. Unlike a business that sells a product once, you deliver value over time—and your accounting must reflect that reality by recognizing revenue as you earn it, not just when cash hits the bank.

This accrual-based approach is the only way to get a true, investor-ready picture of your company's health.

Why Your SaaS Financials Are Probably Lying to You

If you're a founder, CEO, or finance leader at a SaaS company between $500K and $20M in Annual Recurring Revenue (ARR), there's a good chance your financial statements are giving you a dangerously misleading view of your business. This isn't a simple bookkeeping mistake. It's a strategic blind spot that quietly sabotages your growth.

Standard accounting methods were never designed for subscriptions. When you log a $12,000 annual contract payment as instant revenue in the month you receive it, your books are flat-out lying to you.

The Cash-Basis Trap: A Common Misconception

Many early-stage companies fall into the cash-basis accounting trap, where revenue gets recorded the moment money lands in your bank account. It feels simple, but for a SaaS business, it's a disaster waiting to happen. It paints a volatile and completely unreliable picture of your performance, making it impossible to see your actual growth trajectory.

"A quick, accurate month-end close isn’t just about reporting history. It's about providing the leadership team with the 'receipts'—the verified data—they need to make confident decisions for the next month, not the last one." — Ben Murray, The SaaS CFO

Investors demand financials that prove your business model works, and cash-basis accounting fails that test every single time. A big influx of annual prepayments can make one month look incredibly profitable, while the next looks weak—even if your underlying recurring revenue is growing steadily.

Warning Signs: The Dangers of Inaccurate Financials

This disconnect creates serious problems you cannot afford to ignore:

| Red Flag | Business Impact |

|---|---|

| Fundraising Roadblocks | Sophisticated investors will immediately distrust cash-basis financials. They'll demand a complete restatement of your books, which delays—or even kills—your deal. |

| Flawed Valuations | You can't calculate a credible valuation without proper revenue recognition. It’s like trying to measure a building with a rubber band. |

| Poor Decision-Making | How can you make smart calls on hiring, marketing spend, or product development when your core financial data is unreliable? You can't. |

Your Next Step: Shifting to an Investor-Ready Model

The only way forward is to move to accrual-basis accounting under ASC 606 standards. Think of this not as a chore for compliance, but as a strategic move to tell an accurate and compelling story about your growth. Accrual accounting matches revenue to the period in which you earn it, not when you collect the cash. This creates a smooth, predictable revenue stream on your Profit & Loss (P&L) statement that actually reflects the health of your subscription base.

Making this shift turns your finance function from a reactive cost center into a proactive tool for growth. You get the clarity you need not just for investors, but for your own strategic planning. For a deeper dive, check out our guide on how to prepare financial statements that investors trust. Your journey to scalable growth starts with honest, accurate accounting.

Mastering ASC 606 and Deferred Revenue

ASC 606 isn't just an accounting rule—it's the bedrock of credible financial storytelling for any SaaS company. It stops you from making the classic, fatal mistake of booking a full year's contract value the day cash hits your bank account. Doing that creates a wildly misleading and volatile picture of your company’s health.

The core principle is simple: you recognize revenue as you actually deliver your service over time. This is the essence of accrual accounting for subscriptions. It’s non-negotiable for any SaaS business that wants to attract investors, pass an audit, or get a clear view of its own performance.

From A Lumpy Cash Spike To Smooth, Predictable Growth

Let's walk through a real-world example. Imagine a customer signs a $12,000 annual contract and pays you the full amount upfront on January 1st.

Under the wrong (cash-basis) method, your books would show a massive $12,000 revenue spike in January and $0 for the next 11 months. This is a mirage. It tells you nothing about your sustainable performance.

With ASC 606, you get it right. You only recognize $1,000 in revenue each month over the 12-month contract. The rest of the cash you've collected but haven't yet earned sits on your balance sheet as a liability called Deferred Revenue.

A Common Misconception: Deferred Revenue isn't a debt in the traditional sense; it's a promise. It represents the future service you are contractually obligated to provide, and it's one of the best indicators of a healthy SaaS business.

This evolution from simple cash tracking to sophisticated accrual models is exactly why modern accounting standards were created. They provide a true, forward-looking view of business health for complex models like SaaS.

This shift is precisely what ASC 606 delivers—moving from just recording transactions to showing the underlying momentum of your business.

The Deferred Revenue Waterfall In Action

Let's see how that $12,000 annual contract actually plays out on your books month-by-month. Notice how the Deferred Revenue balance starts high and is methodically "drawn down" each month as you earn the revenue.

This table shows the monthly accounting for a single annual contract paid upfront.

| Month | Cash Collected | Revenue Recognized | Deferred Revenue Balance |

|---|---|---|---|

| Jan | $12,000 | $1,000 | $11,000 |

| Feb | $0 | $1,000 | $10,000 |

| Mar | $0 | $1,000 | $9,000 |

| Apr | $0 | $1,000 | $8,000 |

| May | $0 | $1,000 | $7,000 |

| Jun | $0 | $1,000 | $6,000 |

| Jul | $0 | $1,000 | $5,000 |

| Aug | $0 | $1,000 | $4,000 |

| Sep | $0 | $1,000 | $3,000 |

| Oct | $0 | $1,000 | $2,000 |

| Nov | $0 | $1,000 | $1,000 |

| Dec | $0 | $1,000 | $0 |

This method creates a smooth, predictable income statement and a balance sheet that clearly reveals your pipeline of future, contracted revenue.

Why Investors Scrutinize Deferred Revenue

New founders sometimes panic when they see a large liability on their balance sheet. But in SaaS, a big and growing deferred revenue balance is a powerful sign of health and momentum.

Investors look for a rising deferred revenue balance for three key reasons:

- It Validates Sales Performance: A growing balance is hard proof that your sales team is closing deals and bringing in cash. It's a leading indicator of growth.

- It Predicts Future Revenue: This isn't speculative—it's contracted revenue that will hit your P&L in the coming months, giving your financial forecasts real credibility.

- It Signals Customer Stickiness: A high deferred revenue balance, especially from annual prepayments, shows you have a committed customer base that's locked in for the long haul.

Actionable Next Step: Review your balance sheet. Is your deferred revenue balance tracked accurately and growing? If not, this is your first priority. You can use our checklist for auditors and investors to see exactly how this concept is tested during due diligence.

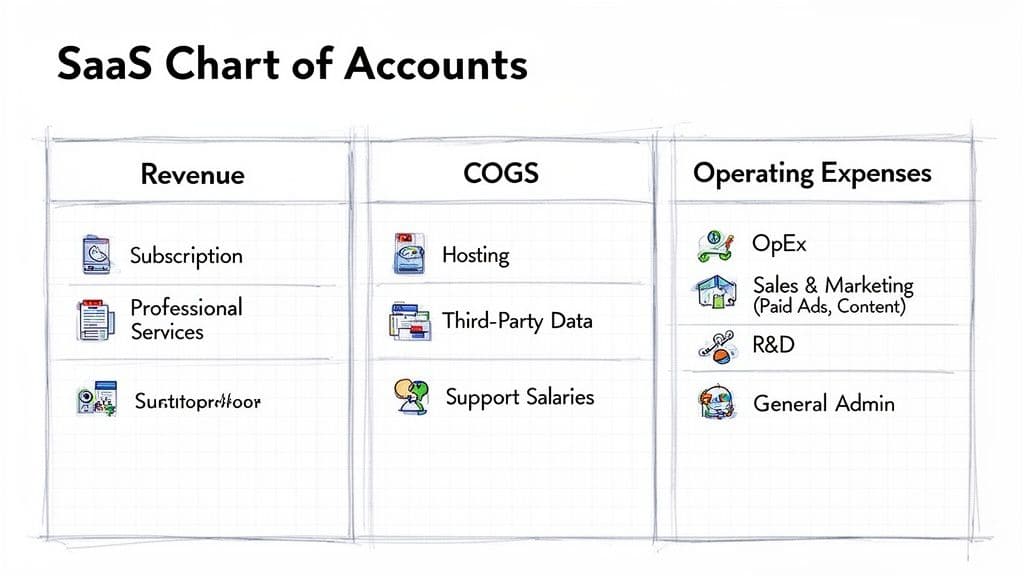

Building a SaaS-Ready Chart of Accounts

Think of your Chart of Accounts (COA) as the index for your company's financial story. If you're running a SaaS business using the generic COA template from QuickBooks or Xero, you’re trying to index a complex novel with categories meant for a children's picture book. It won't work.

A generic COA leaves you with a mess of useless, jumbled data. It mashes critical costs together, making it impossible to calculate the SaaS metrics that investors and your own leadership team need to make smart decisions. A proper, SaaS-ready COA, on the other hand, is built to give you an x-ray view of your business's financial health.

Differentiating Your Revenue Streams

First, you must stop thinking of "revenue" as a single number. A functional SaaS COA requires separate accounts to track each distinct way you make money. This isn't just for neatness; it's fundamental to understanding your business model and true profitability.

At a minimum, you need to break out:

- Subscription Revenue: The lifeblood of your company—recurring income from your core software.

- Professional Services Revenue: One-time fees for implementation, setup, training, or custom development.

- Usage/Overage Revenue: Revenue from any consumption-based component of your pricing.

Lumping these together is a huge mistake. It completely hides the profitability of your core subscription product. Investors want to see high-margin, repeatable subscription revenue, not a top line propped up by low-margin, one-off services.

Cost of Goods Sold The SaaS Way

In the SaaS world, Cost of Goods Sold (COGS)—often called Cost of Revenue (COR)—isn't about physical products. It represents the direct costs you incur to deliver your service and support your paying customers. Getting this category right is non-negotiable for calculating your gross margin.

Your SaaS COGS should include specific accounts for:

- Hosting Costs: What you pay for services like AWS, Google Cloud, or Azure.

- Third-Party Data & APIs: Fees for essential software you integrate, like a mapping API or data enrichment tools.

- Customer Support Salaries & Software: The payroll and software expenses for your frontline support team.

- Capitalized Software Development: Building a robust SaaS COA means you need to get this right. Having clear CapEx and OpEx distinctions is critical for accurate financial reporting and tax planning.

Deconstructing Operating Expenses for ROI

Finally, your Operating Expenses (OpEx) must be structured to measure the return on your growth investments. A single "Marketing Expense" account is a massive red flag for any savvy investor because it makes calculating your Customer Acquisition Cost (CAC) impossible.

You need to break down your Sales & Marketing spend into granular accounts like:

- Paid Advertising: Separate accounts for Google Ads, LinkedIn Ads, etc.

- Content & SEO: Track costs for writers, tools, and any agency partners.

- Sales Commissions: Isolate the variable compensation tied directly to closing deals.

- Sales & Marketing Salaries: The fixed payroll cost of your growth teams.

This level of detail is the only way to see which acquisition channels are actually working and calculate a true, defensible CAC. Without it, you’re flying blind and burning cash.

Actionable Next Step: If your current COA looks more like a generic template than this SaaS-specific structure, it's a clear sign that a professional cleanup is overdue. Fixing these foundational issues is the first step toward building an investor-ready finance function, which our team can tackle with a dedicated QuickBooks cleanup services project.

The SaaS Metrics That Actually Matter to Investors

Investors don't fund stories; they fund predictable, efficient growth. While your GAAP-compliant financials are the ticket to the game, the real conversation—the one that determines your valuation—is all about a specific set of SaaS metrics.

If you can't speak this language fluently, you're dead in the water. Getting your Key Performance Indicators (KPIs) wrong is a faster way to get a "no" from a VC than almost any other mistake. These aren't just internal benchmarks; they are the universal yardstick investors use to decide if your company is a healthy, scalable machine or a cash-burning engine about to seize up.

The Core Metrics Driving Valuation

Dozens of metrics exist, but during due diligence, only a handful truly carry weight. They connect your daily operations directly to your financial future.

Here are the essentials you absolutely must master:

- Annual Recurring Revenue (ARR): The predictable revenue from your active subscriptions, normalized to a one-year period. It’s the single most important top-line metric. We cover the finer points in our complete guide to calculating Annual Recurring Revenue.

- Customer Acquisition Cost (CAC): Your total sales and marketing spend—salaries, ads, commissions, everything—divided by the number of new customers acquired in that period. It's the price you pay to win a new logo.

- Customer Lifetime Value (LTV): This metric forecasts the total revenue you'll generate from an average customer before they churn. It’s the long-term payoff for acquiring that customer.

These three don't live in isolation. Massive ARR growth is exciting, but if it comes from a sky-high CAC and customers who churn out in six months, investors will see a leaky bucket, not a rocket ship.

From Metrics to Ratios: Where the Real Story Is

Knowing your individual KPIs is just step one. The real magic happens when you combine them into ratios that reveal the health of your business model.

LTV to CAC Ratio

This is it. If you only track one ratio, make it this one. It compares the lifetime value of a customer to what you spent to acquire them, answering the most critical question: is your growth profitable?

Worked Example: LTV:CAC Calculation

- Calculate LTV: Your average customer pays $500/month (ARPA), and your monthly churn rate is 2%. Your LTV is $500 / 0.02 = $25,000.

- Calculate CAC: You spent $100,000 on sales and marketing last quarter and signed 10 new customers. Your CAC is $100,000 / 10 = $10,000.

- Find the Ratio: Your LTV to CAC ratio is $25,000 : $10,000, or 2.5:1.

So, is 2.5:1 good? According to OpenView's 2024 SaaS Benchmarks, a ratio of 3:1 is the baseline for "healthy." Anything less is a major red flag. Best-in-class companies push this to 5:1 or higher, proving they have an incredibly efficient growth engine.

CAC Payback Period

This metric tells you exactly how many months it takes to earn back the cash you spent to land a new customer. The shorter the payback, the more cash-efficient your growth is. For most VC-backed SaaS companies, a payback period of under 12 months is the gold standard.

Retention: The Ultimate Proof of Product-Market Fit

Efficiently acquiring customers is great, but investors need to know they'll stick around. This is where retention metrics steal the show.

| Metric | What It Measures | Industry Benchmark (SMB SaaS) |

|---|---|---|

| Gross Revenue Retention (GRR) | Your ability to retain customers, ignoring expansion. It isolates the impact of churn and downgrades. | > 90% is considered strong. |

| Net Revenue Retention (NRR) | The "holy grail." Measures revenue from existing customers, including expansion from upsells. | > 100% means you grow without new customers. Top-tier SaaS is 120%+. |

The entire practice of accounting for SaaS is built on mastering these numbers. With early-stage SaaS firms losing 5-7% of their customers every month, as highlighted in recent SaaS statistics, flying blind without these KPIs isn't just risky—it's a recipe for failure.

Actionable Next Step: Create a simple dashboard to track ARR, CAC, LTV, and NRR monthly. If you can't calculate these numbers from your current accounting system, your financial data isn't actionable.

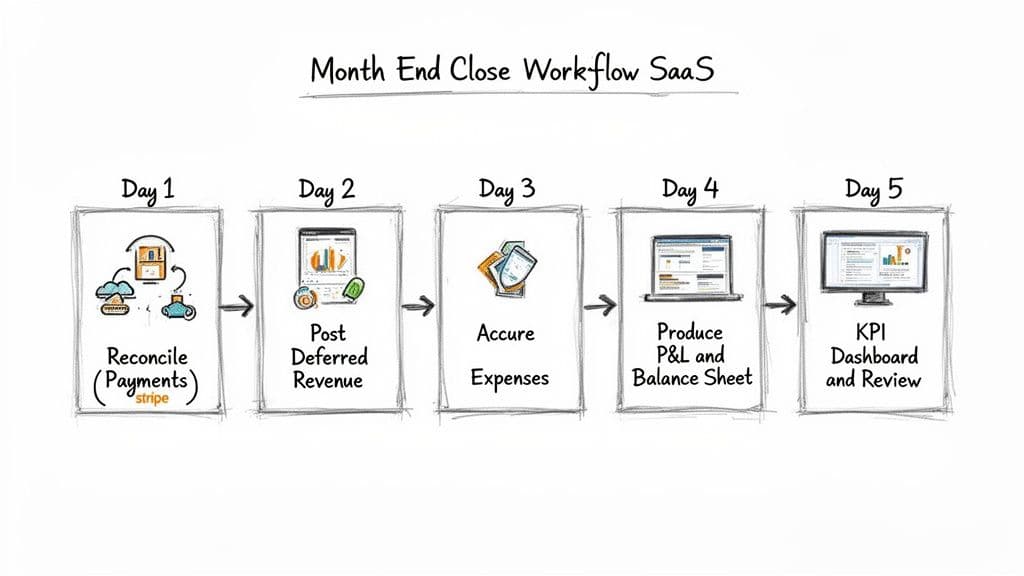

How to Achieve a 5-Day Month-End Close

A slow, agonizing month-end close is a sure sign of a broken accounting system. If closing your books drags on for weeks, you're steering your company by looking in the rearview mirror—making decisions based on stale data. For a modern SaaS business, the gold standard is a fast, predictable 5-day close.

Anything longer is a strategic liability. A chaotic close means your revenue recognition is probably a manual mess, your expenses are recorded incorrectly, and you have zero real-time visibility into the SaaS metrics that drive your valuation. This isn't just an accounting headache; it's a growth bottleneck.

The 5-Day SaaS Close Playbook

A streamlined close isn't a monthly fire drill; it's a smooth, repeatable process. The key is moving away from manual spreadsheet jockeying and toward a systemized, automated workflow. Here’s the day-by-day playbook we implement for SaaS companies.

| Day | Key Actions |

|---|---|

| Day 1 | Lock Down Cash and Revenue: Reconcile all bank, credit card, and payment processor accounts (Stripe, Square, etc.). |

| Day 2 | Post Core SaaS Entries: Post the deferred revenue journal entry to recognize earned revenue and record expense accruals for unbilled invoices. |

| Day 3 | Finalize Payroll and Prepaids: Record the payroll journal entry from your provider (Gusto), accrue sales commissions, and post amortization/depreciation. |

| Days 4-5 | Deliver Insights: Produce core financial statements, update your KPI dashboard (ARR, LTV, CAC, NRR), and deliver high-level analysis. |

Moving From Manual Chaos to Automated Clarity

Let’s be clear: this 5-day timeline is flat-out impossible with a manual, spreadsheet-heavy process. The only way to get there is through automation.

Integrating your core systems—your accounting platform (QuickBooks, Xero, or NetSuite) with your payment processor, payroll provider, and CRM—eliminates the soul-crushing data entry that causes delays and costly errors. This systematic approach is the foundation of a scalable SaaS company.

Actionable Next Step: Check out our guide on month-end close best practices to map out your own close calendar. If your close takes longer than a week, it’s a red flag that your systems need an overhaul.

Your Roadmap to Investor-Ready Financials

Knowing what ASC 606 is and being able to produce investor-ready financials are two very different things. The first is theory; the second is where you build real enterprise value. Getting there requires a clear, actionable plan to transition from messy, manual bookkeeping to a professional, scalable finance function.

We guide companies through a proven, three-phase approach to transform their financials from a liability into a strategic asset.

Phase 1: Assessment and Cleanup

The first step is a frank diagnosis of your current financial state. This isn’t just about finding typos. It’s a deep dive to find the systemic issues—the historical errors in revenue recognition, haphazard expense categorization, and messy balance sheet accounts that are quietly eroding trust in your numbers.

We start by establishing a clean, accurate starting point. Correcting past mistakes ensures your future reporting is built on a solid foundation, not on flawed historical data that will get you grilled in due diligence.

Phase 2: System Implementation

With a clean slate, we can build a system that’s actually designed for a subscription business. This phase is all about implementing the right structure and technology to handle your growth instead of slowing it down.

- SaaS COA Setup: We implement the SaaS-specific Chart of Accounts, properly separating subscription revenue from one-time services and breaking down costs for a clear view of your margins.

- Tech Stack Integration: We connect your core systems—QuickBooks, Xero, or NetSuite with payment processors like Stripe and your payroll provider—to automate data flow and finally kill manual entry errors.

- Define the Close Process: We formalize your month-end close with a detailed checklist. The goal is a repeatable, efficient process that delivers accurate financial statements within five business days, every single month.

Phase 3: Strategic Outsourcing

Once your systems are solid, the focus shifts from just bookkeeping to generating strategic insight. This is where we start producing the monthly KPI dashboards with the metrics investors actually care about, like the LTV:CAC ratio and Net Revenue Retention.

This is also the stage where you decide if your internal team has the capacity and expertise to manage this new, higher-level function, or if it’s time to partner with an expert.

To truly ensure your roadmap to investor-ready financials is solid, understanding and addressing compliance is critical. A key part of this is learning about What Is SOC Compliance: A Practical Guide to demonstrate operational integrity.

Common SaaS Accounting Questions

As you scale, you’ll run into the same handful of critical accounting questions that every SaaS founder faces. Here are the straight answers we give when we see these issues in the wild—getting them right is the difference between being fundable and being forced to restate your financials.

What’s the Single Biggest Mistake Early-Stage SaaS Companies Make?

Hands down, the biggest error is sticking with cash-basis accounting for too long. It feels simple, which is why founders love it. But it gives you a dangerously warped view of your business's health.

When you sign a $12,000 annual contract and get the cash upfront, cash-basis accounting tells you that you made $12,000 that day. Your books look amazing for a month, then terrible for the next eleven. Investors see this lumpy, misleading revenue and will immediately distrust your numbers. They'll force you to restate everything, a painful process that can delay or even kill a deal.

The only acceptable method is accrual-basis accounting under ASC 606. This standard requires you to recognize revenue as you deliver the service—in this case, $1,000 per month for 12 months. It's non-negotiable for building a scalable, fundable SaaS company.

Do I Really Need a Special Chart of Accounts?

Yes, absolutely. A generic QuickBooks template wasn't built for a subscription model, and it will fail you. It won’t properly separate critical revenue streams (like Subscription vs. Professional Services) and it mashes together key cost categories.

This makes it impossible to calculate the SaaS metrics that matter, like Gross Margin and Customer Acquisition Cost (CAC). A SaaS-specific Chart of Accounts is the blueprint for actionable financial reporting. It’s what gives you the granular data needed to understand your performance and tell a compelling story to investors.

"AI has become what it should’ve been all along: an economic engine for software incumbents. Now, investors want to see the receipts." — Ben Murray, The SaaS CFO

Your financials are those receipts. They must be clear, accurate, and defensible.

When Should I Switch From QuickBooks/Xero to NetSuite?

This is a classic scaling question, and the answer isn't a specific revenue number—it’s about a complexity threshold. You’ve outgrown QuickBooks or Xero when the pain of managing your current system outweighs the cost of upgrading.

That tipping point usually happens when:

- Manual work becomes overwhelming: Your finance team spends more time exporting data to spreadsheets for revenue recognition or metric calculations than they do analyzing what the numbers actually mean.

- You need multi-entity consolidation: You're operating in multiple countries with different currencies and need to roll up your financials without a week of spreadsheet gymnastics.

- Advanced compliance becomes a requirement: You’re prepping for an IPO or need the robust controls for SOX compliance that entry-level systems like QuickBooks simply can't provide.

For most businesses under $20M in ARR, a properly configured QuickBooks or Xero, integrated with the right tools, is more than enough. The key is building a great system around it, not just jumping to a more expensive platform like NetSuite before you're ready.

If you’re wrestling with a slow month-end close, messy books, or metrics you can’t trust, you have already outgrown your current system. Jumpstart Partners specializes in building the exact investor-ready accounting systems growing SaaS companies need. Let's talk about how we can give you the financial clarity to scale with confidence. Schedule your consultation.