Financial Operations

Auditing a Business: A Founder's Guide for 2026

Auditing a business for the first time? This guide explains audit types, costs, and readiness for SaaS & service firms, ensuring you pass and secure funding.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readMost founders treat an audit like a tax-season ambush. That’s the wrong frame.

A real audit is a credibility event. It tells investors, lenders, acquirers, and your own leadership team that your numbers can survive outside scrutiny. That matters because financial audits are mandatory for all publicly traded companies annually and are often required for private businesses because of investor demands, loans, or a shareholder request above the ownership threshold. They also sit inside a broader risk environment where global fraud losses total $3.7 trillion yearly according to Cocountant’s accounting statistics roundup.

If you run a SaaS company, digital agency, or professional services firm in the $500K to $20M range, auditing a business stops being theoretical fast. The moment you raise capital, add debt, expand headcount, issue equity, or sign larger customers, your books need to hold up. Sloppy bookkeeping stops being an internal annoyance and becomes a deal risk.

My advice is simple. Prepare for an audit before anyone asks for one. If you wait until a lender, investor, or auditor sends the request, you’ve already lost your advantage. You’ll spend more, move slower, and expose weaknesses under pressure.

Why Your First Audit Is a Growth Milestone Not a Burden

The founders who complain the loudest about audits usually have the most to gain from them.

Your first audit forces discipline. It pushes you to clean up revenue recognition, tighten reconciliations, document approvals, separate founder activity from company activity, and build internal controls that a serious buyer or investor expects to see anyway. Those aren’t compliance chores. They’re operating requirements for a company that wants better financing options and cleaner decision-making.

What an audit actually changes

An unaudited P&L is useful for management. An audited set of financials is useful to outsiders.

That distinction matters. Once an independent auditor tests your balances, traces transactions, and evaluates your accounting treatment, your financial statements become more than internal reporting. They become evidence. That changes how a bank underwrites you, how a VC diligences you, and how a buyer evaluates your quality of earnings.

Here’s the practical business impact:

- Fundraising gets sharper: Investors stop wasting time debating whether your revenue schedule is reliable.

- Debt conversations improve: Lenders care about controls, reporting cadence, and repayment visibility.

- Board reporting gets cleaner: You stop arguing about whose spreadsheet is “right.”

- Exit prep starts earlier: Buyers reward companies that don’t require forensic cleanup.

Practical rule: If an audit would expose a weakness, that weakness already exists. The audit didn’t create the problem. It revealed it.

The expensive mistake founders make

Founders think waiting saves money. It doesn’t.

A rushed audit usually means backfilled documentation, late reconciliations, missing contracts, half-baked revenue memos, and a finance team chasing support instead of running the business. Auditors then spend more time resolving preventable issues. You pay for that in fees, internal distraction, and delayed transactions.

Auditing a business should be treated the same way you treat enterprise security or legal diligence. You don’t “get ready” after the request. You operate in a ready state.

Understanding the Three Types of Business Audits

Founders lose time and valuation when they treat every audit like the same event. They are not the same event. Each audit type answers to a different audience, tests different risks, and drives a different business outcome.

Get this distinction right early. It changes how you staff finance, document decisions, and prepare for growth.

Financial statement audit

This is the audit that affects capital.

An independent CPA firm examines whether your financial statements are fairly presented under the accounting standard you use, usually GAAP. The firm will test revenue recognition, expenses, balance sheet accounts, estimates, close procedures, and the support behind material transactions. The question is simple: can a third party rely on these numbers to make a financing or acquisition decision?

For SaaS and service firms, this audit does more than satisfy a request. It strengthens your fundraising story, shortens diligence, and reduces the discount buyers apply when they expect accounting cleanup after a deal.

Typical triggers include:

- Equity financing: Investors want audited financials before a round or as a post-close requirement.

- Debt underwriting: Banks and credit funds want outside assurance before they extend capital.

- Board and shareholder expectations: More discerning stakeholders want reported results tested, not asserted.

- Transaction prep: A sale process moves faster when your statements already stand up to scrutiny.

If you expect to raise capital in the next 12 to 24 months, start building the control environment now. Strong financial controls for growing businesses reduce audit friction and make your numbers more credible long before the auditors arrive.

Tax audit

This audit is about whether you reported taxes correctly and kept the records to prove it.

The reviewer is a taxing authority, usually the IRS or a state agency. The focus is narrower than a financial statement audit but often more painful operationally. Auditors look at income reporting, deductions, payroll tax treatment, owner pay, contractor classification, sales tax exposure, and the support behind positions taken on the return.

For founders, the core issue is discipline. Sloppy books, mixed personal spending, weak payroll processes, and inconsistent entity treatment turn a tax review into a cash drain. You are not just arguing over compliance. You are risking penalties, interest, and management distraction at the exact moment the business should be focused on customers and margin.

Internal audit

Internal audit is management's pressure test.

In a smaller company, this usually does not mean a formal department. It means a structured review of the systems behind the numbers: approvals, reconciliations, revenue workflows, contract storage, access controls, and month-end close discipline. You can run that review through your internal finance lead or an outside advisor with audit experience.

This is the audit type that creates the most strategic value because it gives you time to fix weaknesses before they affect financing, tax exposure, or a sale process. For a SaaS company, that may mean cleaning up deferred revenue support and user access controls. For a service firm, it may mean tightening time tracking, project profitability reporting, and cutoff procedures.

| Audit type | Main trigger | Primary objective |

|---|---|---|

| Financial statement audit | Investor, lender, board, or transaction request | Prove financial statements are reliable for external decision-makers |

| Tax audit | IRS or state inquiry | Verify tax filings, classifications, and supporting records |

| Internal audit | Leadership decision | Find control gaps early and improve reporting quality |

Founders should treat these audits as three different business tools. Financial audits improve credibility with capital providers. Tax audits test compliance discipline. Internal audits help you fix the systems that determine whether the company can scale cleanly.

The Five Areas Auditors Scrutinize Most

Auditors don’t look everywhere with equal intensity. They go where errors, fraud risk, and judgment are concentrated. In founder-led companies, that usually means a small group of recurring problem areas.

Bank and account reconciliations

If your cash doesn’t tie, nothing else matters.

Auditors start with reconciliations because they reveal whether your month-end close is real or cosmetic. Every bank account, credit card, loan balance, payment processor, payroll clearing account, and merchant balance should reconcile to the general ledger. If Stripe says one thing and QuickBooks says another, you’ve got a control problem.

Common audit failures here include:

- Stale reconciling items: Old deposits in transit and uncleared checks with no real explanation.

- Manual journal plug entries: Entries posted to “force” a tie-out.

- Unreconciled processor balances: Stripe, Shopify, Square, or PayPal activity not matching the ledger.

- Loan accounts booked from guesses: Interest, principal, and fees all mashed together.

A founder should ask one direct question: can your controller produce a reconciliation package for every balance sheet account without improvising?

Revenue recognition under ASC 606

At this point, many SaaS companies break.

According to BPM’s technical accounting guide, non-compliance with ASC 606 drives 70% to 80% of technical accounting adjustments during audits. Misallocation can extend audit timelines by 4 to 6 weeks and increase fees by 25% to 40%.

That’s not abstract. It hits companies with subscriptions, implementation fees, onboarding work, usage-based billing, annual prepayments, discounts, credits, and contract modifications.

Worked example for a SaaS contract

Assume you sell this annual contract:

| Item | Contract amount |

|---|---|

| Annual software subscription | $24,000 |

| One-time implementation service | $6,000 |

| Total contract value | $30,000 |

Now assume the implementation work does not create a separate standalone deliverable for the customer and is required to enable the subscription. In that case, you generally don’t book the full $6,000 upfront just because you invoiced it on day one. You assess the performance obligations and allocate revenue accordingly.

If the total arrangement is recognized over a 12-month service period, a simplified allocation would look like this:

- Monthly revenue recognized = $30,000 ÷ 12 = $2,500 per month

- Revenue recognized in month 1 = $2,500

- Deferred revenue after month 1 = $27,500

The wrong treatment is what many DIY setups do:

- Book implementation fee upfront = $6,000

- Book first month of subscription = $2,000

- Total month 1 revenue booked incorrectly = $8,000

That creates an immediate overstatement of $5,500 in month 1 compared with the simplified straight-line pattern above. Then the rest of the year is distorted. Your monthly MRR reporting gets noisy, your deferred revenue roll-forward breaks, and your audit turns into a technical accounting cleanup project.

If your contracts have bundles, usage fees, credits, or midterm upgrades, get your policy documented and tested. Don’t guess. If you need a practical breakdown of the controls that support this, review financial controls for growing businesses.

“The PBC list is where weak finance teams get exposed. If you can’t provide complete, organized support quickly, the audit drags and confidence drops.”

Former Big 4 auditor

Internal controls

Auditors pay attention to who can do what.

A founder-led company often has one person approving bills, entering them, paying them, reconciling the account, and posting journal entries. That’s efficient until it isn’t. Auditors want to know whether your process can prevent or detect mistakes and inappropriate activity.

Key control areas include:

- Approval workflows: Who approves bills, refunds, payroll changes, and journal entries

- Segregation of duties: Whether one person can initiate and complete a transaction alone

- System access: Admin rights in QuickBooks, NetSuite, Stripe, Gusto, and banking platforms

- Close review: Evidence that someone reviews the month-end package

A weak control environment doesn’t guarantee a bad opinion, but it does increase testing and scrutiny.

This walkthrough is useful if your team needs a visual explanation of what auditors look for in practice.

Payroll and equity

Payroll is one of the easiest places to make expensive mistakes.

Auditors will compare payroll registers, tax filings, employee agreements, bonus approvals, and general ledger postings. They’ll also examine equity grants, option approvals, and how stock compensation was handled if it applies to your business.

The trouble spots are predictable:

- Contractor versus employee misclassification

- Payroll liabilities not tied to filings

- Bonuses accrued without support

- Equity grants missing board approval or valuation support

If you issue equity and don’t maintain a clean cap table with documentation, expect friction.

Accounts payable and accounts receivable

AP and AR tell auditors whether your books reflect reality or wishful thinking.

On the payable side, auditors test vendor support, approval evidence, timing of accruals, and duplicate or unusual payments. On the receivable side, they care about collectability, aging quality, credit memos, write-offs, and whether revenue was booked ahead of substance.

Red flags auditors notice fast

- Customers with old open invoices and no collection plan

- Large manual write-offs posted near period end

- Vendor bills recorded without contracts or invoices

- Round-dollar accruals with no support

- Payments to unfamiliar vendors

If you’re auditing a business that runs on subscriptions or retainers, these five areas decide whether the audit is smooth or painful.

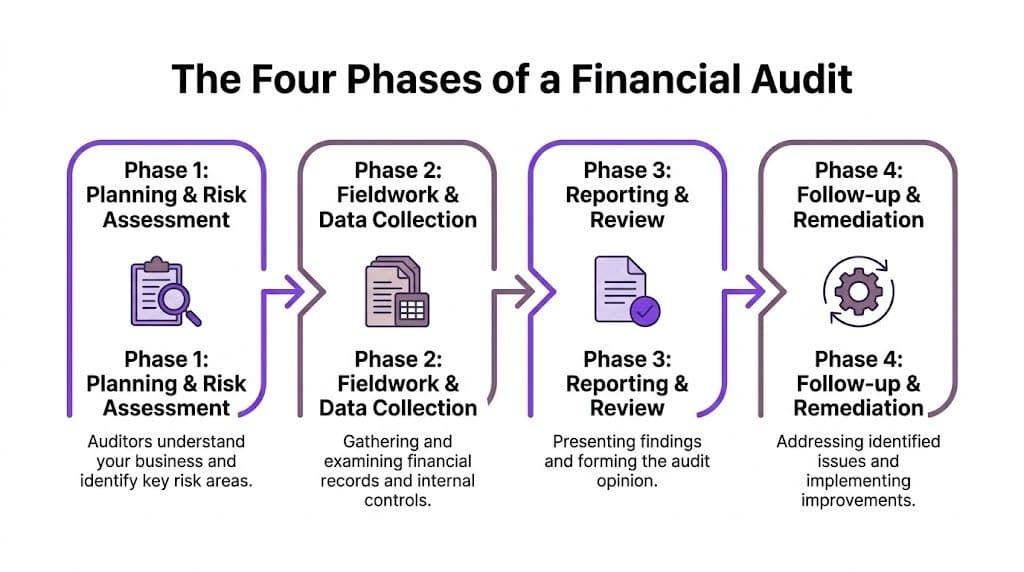

The Four Phases of a Financial Audit

An audit feels chaotic only when you don’t understand the sequence. In reality, it’s a structured project with predictable phases, deadlines, and deliverables.

Planning and risk assessment

Auditors learn how your business works and decide where the risk sits.

They’ll ask about your revenue model, customer contracts, systems, ownership structure, debt, payroll, tax filings, related-party transactions, and significant changes during the year. Then they issue the PBC list, short for “Provided by Client.” That list is the operational heartbeat of the audit. It includes bank statements, reconciliations, contracts, invoices, payroll reports, board minutes, equity records, and policy documentation.

Your job in this phase is to be organized, fast, and consistent. If you need a more tactical prep guide, use this audit preparation checklist.

Fieldwork and data collection

This is the part founders usually call “the audit,” but it’s only one stage.

Auditors start testing balances and transactions. They select samples, inspect documentation, send confirmations if needed, review reconciliations, evaluate controls, and ask follow-up questions. If your books are tight, this phase is mostly project management. If your books are messy, this phase becomes archaeology.

A well-run management team does three things here:

- Assigns one owner for auditor communication.

- Tracks open items in a shared request list.

- Answers with support, not explanations alone.

| Phase | What auditors do | What you need ready |

|---|---|---|

| Planning | Scope the engagement and identify risks | Org details, policies, prior financials, contracts |

| Fieldwork | Test transactions, balances, and controls | Reconciliations, support files, schedules, approvals |

| Reporting | Draft findings and opinion | Final responses, proposed adjustments review |

| Follow-up | Confirm remediation on open issues | Updated processes and corrected records |

Management rule: Never answer an audit question from memory when a report, contract, or reconciliation can answer it better.

Reporting and review

Once testing wraps, auditors evaluate unresolved items and draft their opinion.

If they propose adjustments, your team needs to review them quickly and understand what caused them. Some are straightforward posting corrections. Others reveal a policy issue, especially around revenue, accruals, or classifications. The reporting phase is also where tone matters. Defensive leadership teams slow everything down. Responsive teams get to completion faster.

Follow-up and remediation

A lot of companies think the audit ends when the report is issued. That’s backward.

The useful part comes after. Any control gap, documentation weakness, or process failure should feed directly into your close process for the next period. If the audit found recurring issues, fix the workflow, not just the entry.

A business becomes audit-ready. Not because one audit succeeded, but because the next one requires less effort.

Common Audit Pitfalls and Their Staggering Costs

Founders rarely lose time and money because an auditor asked hard questions. They lose it because weak finance habits sat untouched until an outside party forced the issue.

That cost goes well beyond audit fees. A messy audit can delay a fundraise, weaken buyer confidence in diligence, trigger lender questions, and force leadership to spend weeks defending numbers instead of running the business. For SaaS and service firms, that is a growth problem.

The red flags that keep showing up

The same failures appear in companies that outgrow founder-led finance:

- DIY bookkeeping that lasted too long: The books worked at an early stage and fail once billing, payroll, accruals, and cash movement get more complicated.

- Missing support for key transactions: Contracts, invoices, approvals, or reconciliations are incomplete or scattered across inboxes and drives.

- Worker classification errors: Contractors are treated like employees, or employees are pushed into contractor status without support.

- Commingled spending: Founder purchases, reimbursements, and business expenses run through the same cards and accounts.

- Revenue tracked in spreadsheets instead of a policy-driven process: SaaS companies quickly encounter trouble with this approach, especially with implementation fees, usage billing, renewals, and bundled services.

If you recognize your company in that list, fix it now. Delay gets expensive.

The tangible costs of common audit pitfalls

| Pitfall | Direct consequence | Business cost |

|---|---|---|

| DIY bookkeeping with unreconciled accounts | Auditors expand testing and send repeated support requests | Higher audit fees, longer close cycles, and leadership time pulled into cleanup |

| Revenue recognition errors | Proposed adjustments, policy challenges, and delayed sign-off | Slower fundraising, weaker diligence posture, and lower confidence in forecast quality |

| Poor documentation for expenses or accruals | Balances cannot be supported cleanly | More audit scrutiny, more back-and-forth, and greater risk of tax and reporting issues |

| Commingled founder spending | Reclassification work and possible tax exposure | Extra cleanup, credibility damage, and preventable friction with auditors and investors |

| Weak internal controls | Auditors rely less on your process and test more transactions directly | More disruption across finance and operations, plus a slower path to a clean opinion |

Revenue recognition deserves special attention because it shapes valuation, not just compliance. If your contracts include onboarding, implementation, retainers, milestones, or variable fees, get your policy aligned before fieldwork starts. A plain-English guide to ASC 606 revenue recognition is a good starting point.

Bank reconciliations create another common failure point. If cash does not tie out cleanly every month, auditors stop trusting the rest of the file. Using automated bank reconciliation software can reduce manual matching errors and give your team a cleaner audit trail.

Weak books become a financing problem, a tax problem, and a credibility problem.

Objections I hear, and why they fail

“We’re too small for this to matter.”

Smaller companies usually have fewer controls, less segregation of duties, and more exceptions approved by the founder. That makes the audit harder, not easier. Buyers and investors know it.

“Our CPA will clean it up at year-end.”

Year-end cleanup does not build a reliable finance function. It produces rework. Auditors want support, consistency, and a repeatable close process.

“We haven’t had an issue yet.”

That only means no independent party has tested the numbers hard enough. Audit problems stay hidden until they hit cash, taxes, debt covenants, or diligence.

A clean audit does more than avoid trouble. It proves your company can scale with discipline, which is exactly what investors, lenders, and acquirers pay for.

How Outsourced Finance Turns Audit Prep into a System

You do not solve audit readiness with a heroic quarter-end scramble. You solve it with a repeatable finance system.

That means monthly reconciliations completed on time, revenue schedules tied to executed contracts, payroll and equity records maintained as events happen, and close documentation stored where someone else can inspect it without guessing. Once that system is in place, auditing a business becomes validation instead of emergency repair.

What changes when the system is built properly

Modern audit prep is increasingly driven by data analytics, not just manual sampling. According to the Journal of Accountancy’s coverage of audit data analytics and visualization, ADA allows 100% transaction population testing instead of 5% to 10% sampling and cuts anomaly detection time by 60% to 75%. The same source notes that SOC 2 Type II providers can deliver 99.8% accuracy guarantees by integrating systems such as QuickBooks and NetSuite.

That matters because your systems leave trails. If your general ledger, bank feeds, payroll platform, billing system, and merchant processor don’t align, auditors and investors will see the inconsistency quickly.

A better setup usually includes:

- Integrated source systems: QuickBooks, Xero, NetSuite, Stripe, Shopify, Gusto, and BambooHR feeding a consistent close process

- Documented close routines: Reconciliations, review signoffs, revenue schedules, and variance analysis completed monthly

- Exception-based review: Teams focus on anomalies instead of re-checking clean transactions

- Secure control environment: Permissions, approvals, and audit trails are visible and reviewable

If bank recs are still manual and painful, a practical resource on automated bank reconciliation software can help you evaluate workflow options before those bottlenecks spill into audit season.

Why outsourced finance works better than ad hoc cleanup

A good outsourced finance function doesn’t just “help with the audit.” It builds the machinery that makes the audit easier every month.

That includes policy design, monthly close discipline, reconciliations, reporting packages, and technical accounting support where revenue recognition or equity treatment gets complicated. It also gives founders something they rarely have internally at this stage: a finance operator who knows what an auditor will ask before the question lands.

If you’re evaluating models, compare them against a real operating standard, not just hourly bookkeeping help. This guide to outsourced controller services is a useful starting point.

The best audit prep is boring. Clean reconciliations. Clear approvals. Current schedules. Organized support. That’s what lets leadership stay focused on the business instead of babysitting the audit.

Your Audit Readiness Checklist and Next Steps

At this point, you don’t need more theory. You need a diagnosis.

Quick self-assessment

Answer each question with yes or no.

- Books closed on time: Are your monthly books closed consistently with reconciled cash, cards, loans, payroll, and merchant balances?

- Revenue policy documented: Do you have a written approach for subscriptions, setup fees, bundled services, credits, and contract changes?

- Contracts organized: Can your team pull signed customer agreements and amendments quickly?

- Expense support complete: Does every significant transaction have invoice, approval, and business-purpose support?

- Payroll documented: Can you tie payroll entries to payroll reports and tax filings?

- Equity records maintained: Do you have board approvals, grant documentation, and a current cap table where relevant?

- Internal controls visible: Are approvals, access rights, and review steps defined rather than informal?

- Audit trail clean: Could an outsider follow a transaction from source document to ledger to financial statement without hand-holding?

How to read your result

| Your answers | What it means | What to do now |

|---|---|---|

| Mostly yes | You’re in decent shape | Run a mock audit request list and tighten weak spots |

| Mixed | You have avoidable audit risk | Clean up revenue, reconciliations, and documentation before year-end |

| Mostly no | You are not audit-ready | Treat this as an urgent finance rebuild, not a bookkeeping task |

A lot of founders also miss the control side of readiness. If customer contracts, financial systems, and access controls are all part of how your business operates, security and audit readiness overlap. A practical outside reference is this SOC 2 readiness assessment, especially if customers or investors are starting to ask harder diligence questions.

The next moves I recommend

- Run a PBC simulation. Ask your finance team to assemble the core audit support package now.

- Review revenue recognition manually. Pull a sample of contracts and confirm the accounting treatment matches the terms.

- Test your close process. Look for stale reconciling items, unsupported journal entries, and balances that rely on spreadsheet patches.

- Fix documentation habits. No invoice, no approval, no posting. That should be the standard.

- Use a formal checklist. Start with this checklist for auditors and build your internal readiness review around it.

If your audit readiness depends on one employee remembering where files live, you are not audit-ready.

An audit is a forcing function. Use it before someone else does.

If your books aren’t audit-ready and you know it, get help before the pressure arrives. Jumpstart Partners helps SaaS companies, agencies, and growing businesses build investor-ready financials, tighter controls, and a finance system that can stand up to audit scrutiny.