Financial Operations

Gross Profit Versus Operating Profit: A CEO's Guide

Understand gross profit versus operating profit. Learn the formulas, see SaaS examples, and discover why this matters for fundraising, KPIs, and cash flow.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readA strong gross margin can hide a weak business. That's the trap.

You can report healthy revenue, talk about attractive unit economics, and still run a company that gets less fundable every quarter. The reason is simple. Gross profit and operating profit answer different questions, and founders routinely use the wrong one to judge whether the business is scaling.

That mistake gets expensive fast in SaaS, agencies, and professional services firms. If you classify delivery payroll, onboarding labor, support, or implementation work in the wrong place, your gross margin looks better than reality. Then you hire too fast, price too loosely, and walk into diligence with a P&L an investor or auditor won't trust.

Why This Distinction Determines Your Company's Fate

If your gross margin looks strong but cash keeps tightening, your P&L is telling you something you aren't listening to.

I've seen this pattern over and over. A founder points to gross margin as proof the model works. Meanwhile payroll expands, software spend piles up, leadership adds layers, and operating profit stays thin or negative. The business isn't scaling. It's just producing revenue with attractive direct economics while overhead consumes the rest.

That distinction is not academic. It drives pricing, hiring, fundraising, and audit readiness. Gross profit isolates production efficiency. Operating profit tells you whether the company can support its own operating model. If you confuse the two, you will overestimate how much room you have to spend.

Practical rule: If you're using gross margin alone to justify more headcount, you are making a financing decision with an incomplete metric.

This gets even more dangerous in founder-led businesses between early traction and institutional scrutiny. At that stage, misclassified expenses can make your gross profit look clean while your actual operating performance says the opposite. Investors don't miss that. Neither do auditors. When they start recasting your numbers, they aren't just fixing presentation. They're reassessing risk.

If you're preparing for diligence, you need the same discipline that shows up in a quality of earnings review for founders. Buyers and investors want to know whether your margins are real, repeatable, and supported by defensible accounting.

The blunt version is this. Gross profit can impress. Operating profit determines whether your company deserves confidence.

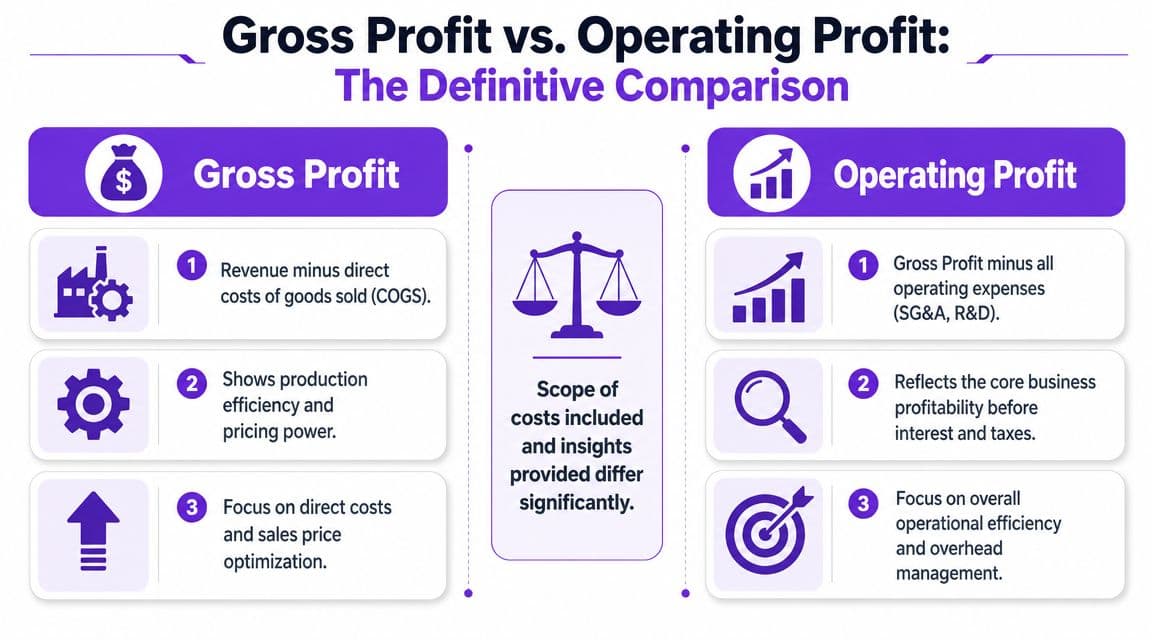

Gross Profit vs Operating Profit The Definitive Comparison

Gross profit and operating profit answer two different questions, and CEOs who blur them make bad scaling decisions.

Gross profit shows whether you deliver your product or service at a profit. Operating profit shows whether the company, as built, can carry its own weight. That difference matters most in SaaS and service firms, where one classification decision can inflate gross margin, depress OpEx, and make your business look stronger than it is during fundraising.

According to Indeed's explanation of gross, net, and operating profit, gross profit is revenue minus cost of goods sold. Operating profit is gross profit minus operating expenses. The math is simple. The judgment behind the math is where companies get into trouble.

Gross Profit vs Operating Profit at a Glance

| Attribute | Gross Profit | Operating Profit |

|---|---|---|

| Core formula | Revenue minus COGS | Gross profit minus operating expenses |

| Primary purpose | Measures delivery efficiency | Measures whether the operating model produces earnings |

| Includes | Revenue and direct costs required to serve customers | Gross profit after sales, admin, management, and support overhead |

| Excludes | SG&A, rent, admin salaries, most overhead, interest, taxes | Interest and taxes |

| Best use | Pricing decisions, service mix analysis, direct cost control | Fundraising, board reporting, hiring pace, scalability analysis |

| Key question answered | Are customer engagements profitable to deliver? | Can this company scale without burning capital? |

What belongs in each bucket

In this regard, SaaS and service firms distort the picture.

For SaaS, COGS often includes customer-specific hosting, third-party usage fees tied to delivery, implementation labor required to onboard the customer, and support labor when support is part of the contracted service. Operating expenses include sales commissions, marketing, executive payroll, finance, HR, recruiting, office costs, and general software subscriptions that support the company rather than customer delivery.

For agencies and professional services firms, billable delivery labor usually sits in COGS. So do contractor costs tied to client work and delivery software used only to serve clients. Account management that is not billable, sales salaries, leadership compensation, internal operations staff, and back-office systems belong in operating expenses.

If your team needs a cleaner framework for the top half of the P&L, use this guide on how to calculate gross margin accurately.

Why misclassification changes the story

Take a SaaS company with $4 million in revenue. If true COGS is $1.6 million, gross profit is $2.4 million and gross margin is 60%. If the company pushes $300,000 of implementation payroll into OpEx instead of COGS, gross profit jumps to $2.7 million and gross margin rises to 67.5%.

Nothing improved. Delivery got no cheaper. The accounting got looser.

That matters in a fundraise. Investors use gross margin to judge efficiency, but they use operating profit to judge whether future scale will require more capital. If your gross margin looks elite because onboarding labor, support labor, or client-specific infrastructure is sitting below the line, a serious investor will recast the numbers. Once they do, valuation pressure follows.

The same problem shows up in audits and diligence. Weak COGS policy signals weak financial controls. If your SaaS business cannot defend why implementation payroll is in OpEx while customer success handles required delivery tasks, or if your agency books too much billable labor below gross profit, reviewers will question the rest of the P&L too.

The CEO view

Gross profit is the cleaner operating lens for pricing and delivery decisions. Operating profit is the harder truth.

A company with strong gross margins and weak operating profit may still have a good business. A company with inflated gross margins caused by bad classification has a reporting problem, a credibility problem, and usually a valuation problem. CEOs should treat that as a control failure, not a formatting issue.

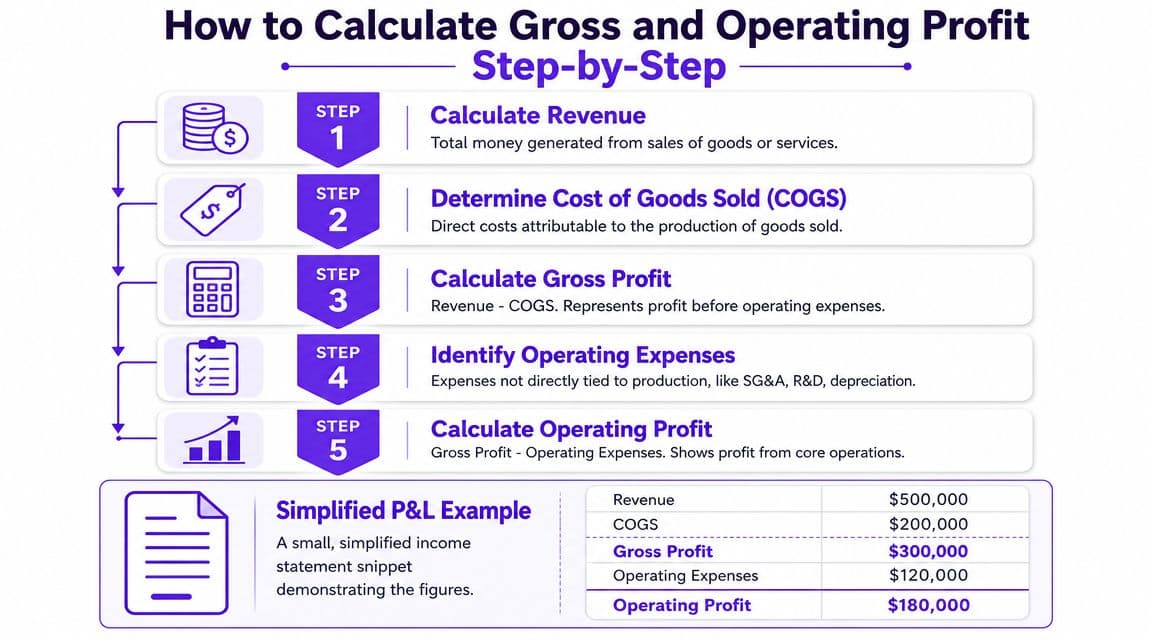

How to Calculate Gross and Operating Profit Step-by-Step

Let's make this concrete.

The mechanics are simple when the classifications are right. They become misleading when they aren't. Start with revenue, subtract COGS to get gross profit, then subtract operating expenses to get operating profit.

A basic reference point helps. In Bookipi's operating income versus gross profit example, a company with $150,000 in revenue and $90,000 in COGS has $60,000 in gross profit. If it then incurs $25,000 in operating expenses, operating profit drops to $35,000. That one example captures the entire issue. Delivery can be profitable while the full operation is less so.

SaaS example with classification discipline

Suppose your SaaS P&L starts with subscription and implementation revenue.

Use this sequence:

- Record total revenue for the period.

- Subtract direct delivery costs that exist because customers are being served.

- Review what's left as gross profit.

- Subtract the costs of running the rest of the company.

- Land on operating profit.

A practical SaaS classification checklist:

- COGS items: Customer-specific hosting usage, third-party data passed through service delivery, implementation labor tied to onboarding, support payroll when support is part of delivering the contracted service.

- Operating expense items: Sales commissions administration, executive salaries, finance and HR payroll, general software tools, office costs, recruiting, brand marketing.

If you need a refresher on the margin math itself, use this guide on how to calculate gross margin.

Later in the close process, review any employee whose time splits across functions. A support lead who spends part of the month resolving customer delivery issues and part managing internal processes shouldn't sit lazily in one bucket forever. Build a documented allocation policy and update it when the role changes.

Here's a visual walkthrough of the flow from revenue to operating profit:

Agency example with billable labor

Agencies usually make this harder than it needs to be.

If an employee's work is billable or directly tied to client production, that cost typically belongs in COGS. Think designers, developers, media buyers executing campaigns, and contractors assigned to delivery. If the work is managerial, administrative, or related to winning future business, it belongs in operating expenses.

Use this review table during month-end close:

| Expense item | Likely treatment | Why it matters |

|---|---|---|

| Billable project labor | COGS | It reflects the direct cost to deliver client work |

| Freelancer tied to a live engagement | COGS | It's customer-serving production cost |

| Agency owner doing sales and leadership | Operating expense | That's part of running and growing the firm |

| Proposal team or biz dev staff | Operating expense | They support selling, not current delivery |

| Internal QA not tied to a client contract | Operating expense | It supports operations broadly |

If your agency reports a fantastic gross margin because most delivery payroll sits in operating expenses, your gross margin isn't a metric. It's a filing preference.

The point of the exercise isn't cosmetic accuracy. It's decision accuracy. Once the classifications are right, your pricing, staffing, and client profitability analysis become much more credible.

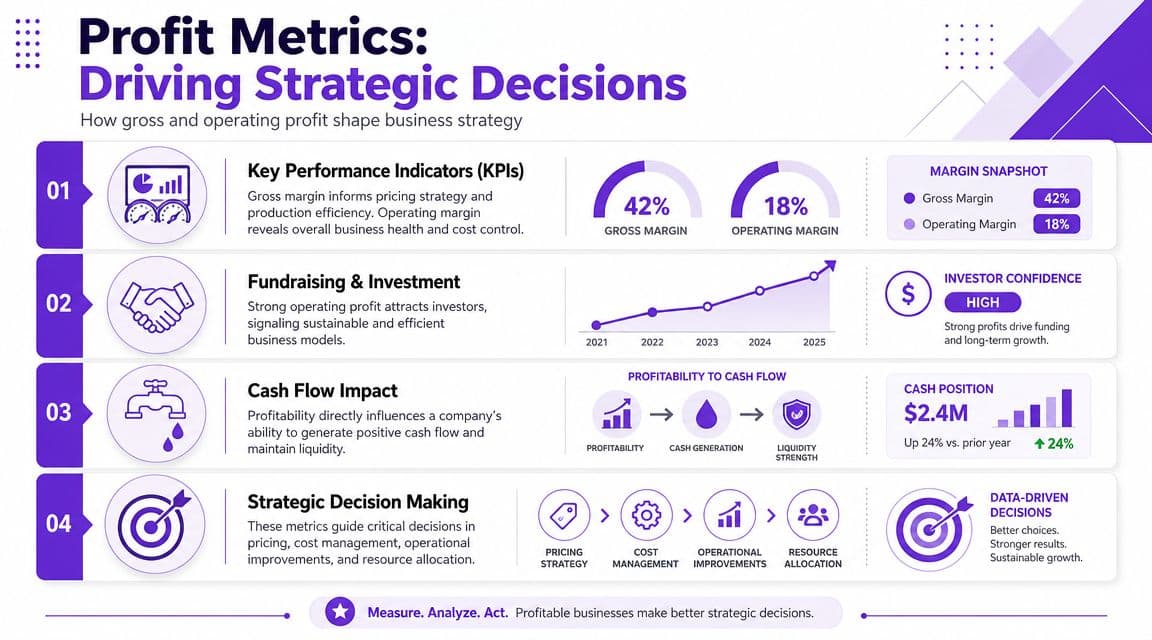

The Strategic Implications for KPIs Fundraising and Cash Flow

Misstate gross profit and you will misprice the business, misread burn, and walk into fundraising with numbers that do not survive diligence.

A SaaS company can show an attractive gross margin on paper while hiding implementation payroll, customer support, and onboarding labor in operating expenses. A services firm can do the same by parking billable labor below gross profit. The result is the same. You look more scalable than you are, and that mistake gets expensive fast when investors recast the model.

The spread tells the story

Gross profit answers one question. Can you deliver the product or service efficiently?

Operating profit answers the one that matters in a boardroom. After payroll, systems, management, and go-to-market spend, is there an actual business here?

Use a simple example. A SaaS company reports $5 million in revenue and claims 80% gross margin, so gross profit is $4 million. During diligence, investors find $900,000 of implementation and support payroll sitting in OpEx even though those teams are required to deliver the service. Reclassify that cost into COGS and gross margin drops to 62%. Nothing changed economically, but the valuation discussion just did. The company no longer looks like a high-efficiency software model. It looks like a software business with a heavy service layer.

That change hits more than optics. It changes CAC payback assumptions, margin benchmarks, headcount planning, and the credibility of every forecast tied to future scale.

What this means in diligence

Experienced investors and buyers usually test four things first:

- Margin integrity: Do your COGS policies match how the business delivers revenue?

- Scalability: Does revenue growth improve operating profit, or does every new dollar require more hidden service labor?

- Cash needs: How much outside capital will the business need if the true cost structure is higher than reported?

- Audit readiness: Can management explain classifications consistently under scrutiny, especially in SaaS and ASC 606-sensitive service models?

If those answers are weak, they will recast your statements before they price the deal. That usually means a lower valuation, a harder raise, or both.

This is why clean classification work is not a bookkeeping exercise. It is deal preparation. Founders who wait until a financing process starts are already late, which is why reading about hiring a fractional CFO for startups is often a practical first step before serious fundraising.

Experienced investors do not reward adjusted storytelling. They reward margin definitions that hold up in diligence, audits, and board reviews.

Cash flow follows operating truth

Cash problems usually show up after classification mistakes, not before.

Here is the pattern. A company reports strong gross margin, hires ahead of plan, signs a bigger office lease, adds software, and builds a sales team around a margin profile that was never real. Then cash starts disappearing because the delivery engine was more labor-heavy than management admitted. For SaaS firms, misclassifying onboarding, support, and implementation can create this exact trap. For service firms, burying direct client labor in OpEx does the same thing.

A disciplined cash flow forecasting process forces you to model the business with an accurate cost structure, not the flattering one. That is how you decide whether you can afford headcount growth, whether pricing needs to move, and whether a fundraise is being used to scale or solely to cover a margin problem.

Use gross profit to judge delivery economics. Use operating profit to decide whether the company can grow without breaking itself.

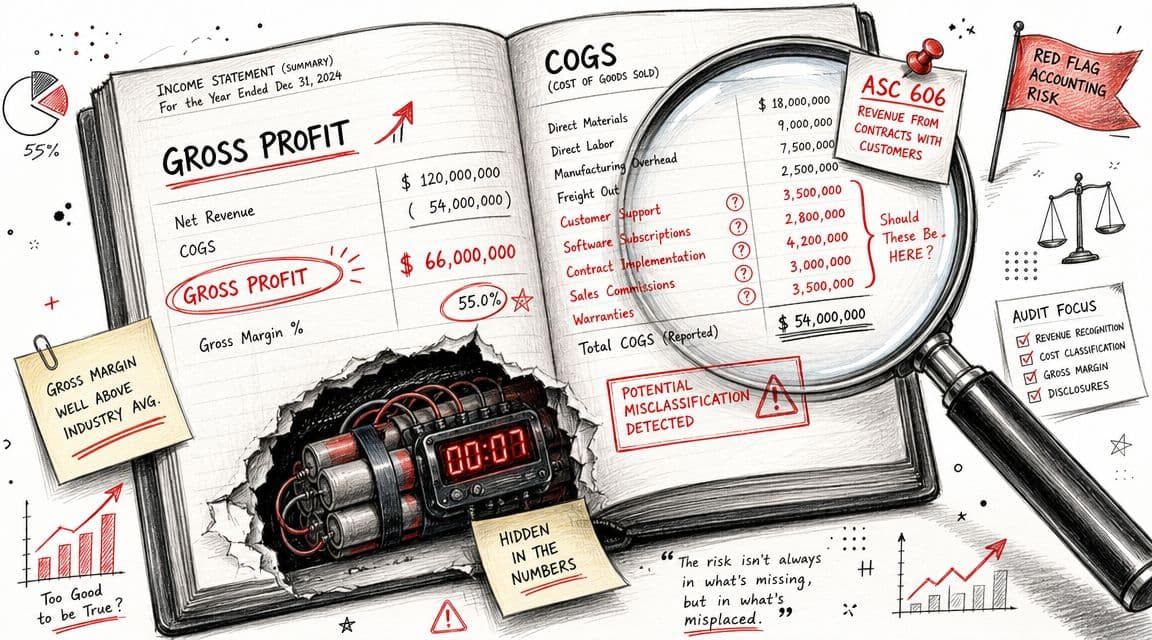

Common COGS Misclassifications and ASC 606 Red Flags

Most margin problems in growing SaaS and service firms aren't economic first. They're classification problems first.

That matters because a sloppy chart of accounts creates fake confidence. Once diligence starts, those choices become red flags.

The usual offenders

These are the line items I would challenge immediately in a SaaS or service business:

- Implementation teams parked in OpEx: If onboarding is required to deliver the contract, that labor often belongs in COGS.

- Customer support fully treated as G&A: If support is part of the promised service, pushing it below gross profit overstates gross margin.

- Billable employees classified as admin payroll: Agencies do this constantly, especially when staff wear multiple hats.

- Project contractors buried in miscellaneous expense: Direct delivery cost belongs where the delivery cost belongs.

- Account managers mislabeled without role review: If they retain and serve current client work rather than sell new business, the classification deserves scrutiny.

What investors and auditors notice

They notice inconsistency first.

If your gross margin improves suddenly with no pricing change, no delivery automation, and no vendor savings, someone reviewing the file will ask what moved. If the answer is "we changed how we book payroll," you've just signaled that your historic trend line isn't comparable.

They also notice policies that exist only in someone's head. If no one can explain why one support salary sits in COGS and another sits in OpEx, the financials aren't investor-ready.

Warning sign: If your controller, founder, and CPA would classify the same role three different ways, your margin reporting isn't defensible.

ASC 606 adds another layer

Revenue recognition and cost classification can collide in messy ways.

If you have implementation fees, bundled services, or fulfillment activities tied to contracts, you need a documented approach that aligns revenue treatment with the economics of delivery. A loose setup undercuts audit readiness fast. This overview of ASC 606 revenue recognition is a practical place to start if your contracts include onboarding, setup, or multi-element arrangements.

The core principle is simple. You don't get investor-grade margins from optimistic labeling. You get them from consistent policy, documented judgments, and close procedures that hold up under review.

Actionable Controls to Optimize Both Profit Margins

Bad margin controls do more than blur reporting. They make you price the wrong work, hire too early, and walk into fundraising with numbers you cannot defend.

Treat gross profit and operating profit as two separate management systems. Gross profit controls how efficiently you deliver. Operating profit controls how much company infrastructure the business can support. If you run a SaaS or services company and mix implementation labor, support payroll, hosting, customer success, and sales ops in the wrong buckets, both signals break.

Controls that improve gross profit

Start with the costs tied directly to delivery.

For SaaS, that usually means hosting, third-party infrastructure, implementation labor, and any support or success work required to fulfill the contract. For service firms, it means billable payroll, subcontractors, project-specific software, and reimbursable pass-through costs. If those items sit below the line in OpEx, gross margin looks stronger than reality. That leads to underpricing, weak renewal strategy, and ugly diligence questions later.

Use these controls:

- Review delivery cost at the customer or project level: Tag direct labor, software usage, and subcontractor spend to the account that consumed it. If a client generates $120,000 in annual revenue but needs $75,000 of delivery cost, your margin problem is not theoretical.

- Set a written COGS policy by role: Decide which roles belong in COGS based on actual delivery work, not titles. An implementation manager who spends 80 percent of time onboarding customers belongs in COGS. A sales enablement manager does not.

- Reclassify mixed roles monthly: SaaS companies often misclassify technical support, onboarding, and customer success because those teams wear multiple hats. Split time by function when the role materially supports both delivery and overhead.

- Audit vendor leakage: Review cloud spend, contractor invoices, data tools, and partner fees. If direct delivery cost rises faster than pricing, gross profit will compress whether you notice it or not.

Channel businesses need the same discipline. Operators trying to grow my profit on Amazon still need a clean split between direct fulfillment cost and operating overhead before any margin analysis is useful.

Controls that improve operating profit

Once direct costs are clean, fix the overhead engine.

A company can post healthy gross margins and still run out of cash because OpEx grows without control. That happens all the time in founder-led SaaS firms. Revenue grows, gross margin looks attractive, then headcount, software, and admin costs pile up faster than the business can absorb them.

| Control | Why it matters |

|---|---|

| Headcount approval tied to forecast | Stops overhead hires from outrunning realistic revenue |

| Department budget ownership | Forces managers to own spend instead of sending everything to finance |

| Monthly variance review | Catches margin erosion before it becomes a cash problem |

| Software stack cleanup | Cuts duplicate tools that quietly inflate operating expense |

| Close checklist with role allocation review | Prevents recurring COGS versus OpEx errors |

One control matters more than it sounds. Review payroll mapping every month. In SaaS and services, payroll is usually the biggest source of margin distortion. One reclass from OpEx to COGS can drop gross margin enough to change how an investor views scalability.

Build the process before diligence starts. A documented financial controls framework for growing businesses gives your team a repeatable way to close the books, apply classification rules, and explain margin trends under scrutiny.

Your next move should be specific:

- Audit every payroll role against a written COGS versus OpEx policy.

- Rebuild the P&L so direct delivery costs sit above gross profit.

- Review gross profit by customer, service line, product, or contract type.

- Forecast operating profit monthly with hiring and software spend included.

- Fix classification issues before fundraising, lender review, or audit fieldwork begins.

If your financials do not clearly separate gross profit from operating profit, Jumpstart Partners can help you rebuild the P&L, tighten classifications, and produce reporting that supports pricing, fundraising, and audit readiness.