Financial Operations

Agency Profits: Accounting for Advertising Agencies 2026

Master accounting for advertising agencies in 2026. Our guide covers revenue recognition, job costing, KPIs, & pass-through costs to boost profitability.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readMost agency founders think accounting tells them whether the business is healthy. It usually doesn't. It tells them whether the bank account survived the month.

That's a dangerous standard in an industry this large and fragmented. IBISWorld projects global advertising-agency revenue at $444.7 billion in 2026, with about 450,000 businesses operating in 2025, and projects revenue growing at a 3.5% CAGR to $529.0 billion through 2030. In a market that big, sloppy finance doesn't get hidden. It gets punished.

Accounting for advertising agencies is not a back-office chore. It is the control system for client profitability, billing discipline, and working capital. If your books can't tell you which accounts make money, where pass-through spend is distorting cash, and whether your team is earning margin before the month is over, you're not running on finance. You're running on instinct.

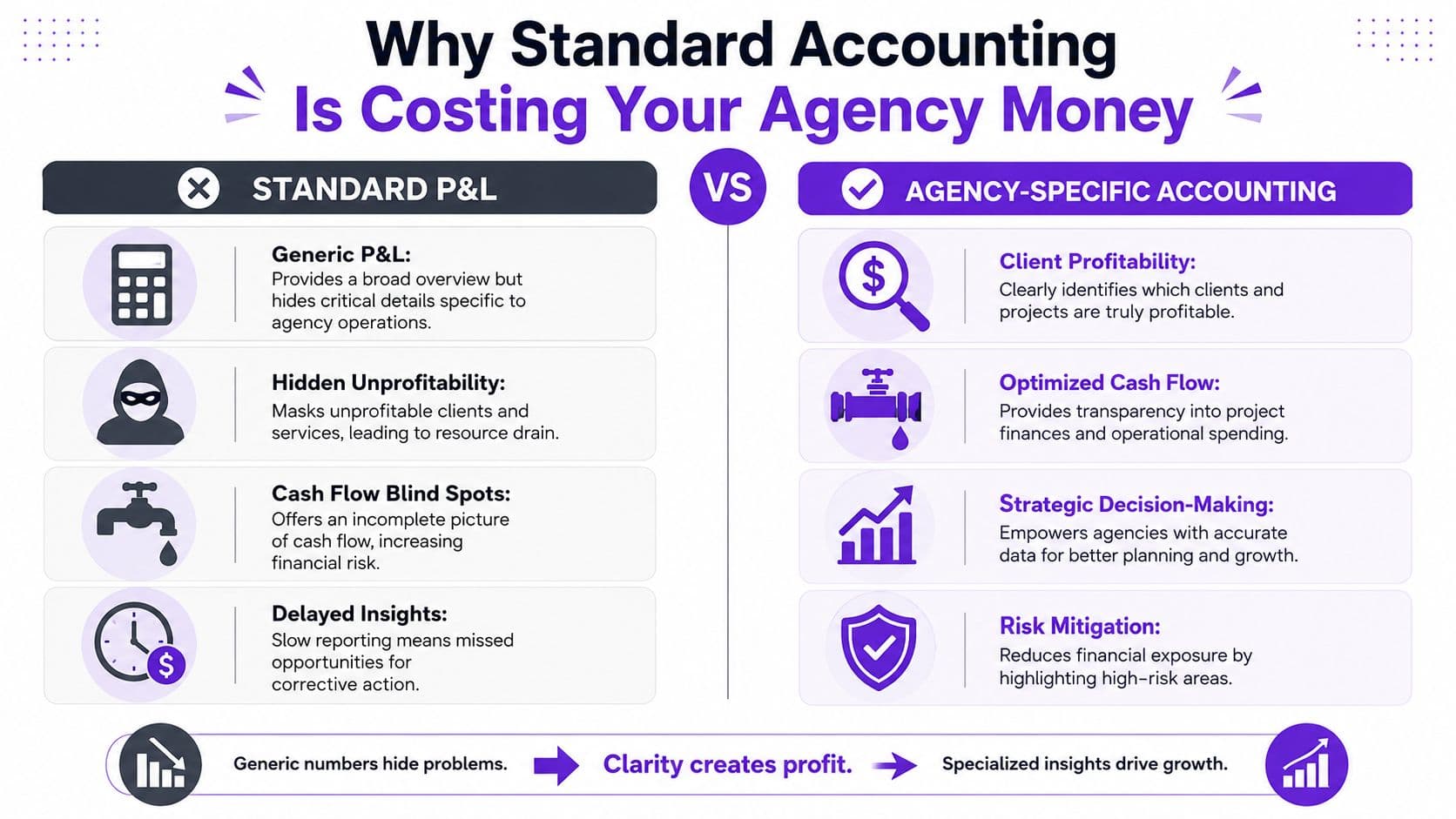

Why Standard Accounting Is Costing Your Agency Money

If you're still running your agency off a standard monthly P&L, you're missing the one thing that matters most. Which clients and projects produce profit.

Most bookkeeping setups were built for businesses that buy inventory, sell products, and collect cash in a fairly linear way. Agencies don't work like that. You sell time, strategy, creative output, and campaign execution. You also carry pass-through costs, uneven labor utilization, and billing timing that can make a “profitable” month look healthy while specific client work is steadily draining cash.

The hard evidence is straightforward. HubSpot's 2024 Agency Growth Report says agencies using project-level financial tracking report 32% higher overall profit margins than peers using standard bookkeeping. That gap exists because project-level tracking exposes bad pricing, scope creep, and unprofitable client relationships before they become permanent.

What standard bookkeeping hides

A generic P&L usually lumps together revenue, payroll, software, contractors, and overhead. That gives you a company-wide summary, but it does not answer the operational questions that drive agency economics.

- Client-level margin: You need to know whether Client A is funding growth or consuming your best team at weak margins.

- Service-line performance: SEO, paid media, branding, web development, and production rarely carry the same economics.

- Timing distortions: An invoice sent this month may reflect work done across several months.

- Pass-through noise: Media spend can make top-line revenue look bigger while contributing little or no real margin.

Practical rule: If your accounting can't show gross margin by client, it can't guide pricing, staffing, or account management.

The false comfort of a clean monthly P&L

Founders often say, “My books are clean. My CPA reviews them.” That's not the same as having useful management accounting.

Tax-ready books are about compliance. Agency-ready books are about decisions.

Here's the distinction:

| View | What it tells you | What it misses |

|---|---|---|

| Standard bookkeeping | Whether income exceeded expenses overall | Which clients, projects, or retainers drove the result |

| Agency-specific accounting | Profitability by client, project, and service line | Much less, if built correctly |

If you want a plain-English explanation of what weak finance processes cost, read this breakdown on the cost of poor accounting decisions.

Your agency does not need more reports. It needs sharper reports. The goal is to stop asking, “Did we make money?” and start asking, “Where did we make money, where did we lose it, and what changes this month?”

Building Your Agency's Financial Blueprint

Agency accounting has always required two systems, not one. A historical accounting guide for advertising agencies explains the long-standing split between general accounting for financial reports and cost accounting for client profitability, and stresses that systems should prevent agencies from financing client advertising with their own cash. That old logic still applies because your agency still has the same two jobs. Report the business accurately, and protect margin and cash at the client level.

A generic chart of accounts won't do that. You need a structure that reflects how an agency earns, spends, bills, and carries risk.

Build the chart around decisions

Your chart of accounts should answer real management questions:

- Are retainers more profitable than project work?

- How much direct labor are you consuming to serve each client?

- How much of your expenses are true delivery costs versus overhead?

- Are you holding client money separately from operating cash?

- Are contractors helping margin or masking staffing problems?

If your current structure can't answer those questions, rebuild it.

For a deeper framework, this guide on what a chart of accounts should do for growing businesses is worth reviewing before you touch QuickBooks or Xero.

Sample Agency Chart of Accounts Partial

| Account Type | Account Name | Purpose |

|---|---|---|

| Revenue | Retainer Revenue | Tracks recurring client service fees |

| Revenue | Project Revenue | Separates one-time scoped work from recurring work |

| Revenue | Commission or Markup Revenue | Isolates agency earnings on managed spend or vendor activity |

| Cost of Goods Sold | Direct Labor | Captures employee time spent delivering client work |

| Cost of Goods Sold | Freelancers and Contractors | Tracks outsourced delivery costs tied to client work |

| Cost of Goods Sold | Media or Production Pass-Through Costs | Separates reimbursable or managed spend from agency margin |

| Operating Expenses | Sales and Marketing | Keeps internal growth costs out of delivery margin |

| Operating Expenses | Admin and G&A | Captures leadership, finance, office, software, and support overhead |

| Other Current Liability | Client Funds Held | Records client cash the agency holds but hasn't earned |

| Other Current Asset | Unbilled WIP | Tracks work performed but not yet invoiced |

| Accounts Receivable | Trade Receivables | Tracks standard client invoices due |

| Bank | Client Trust or Clearing Account | Segregates client-funded spend from operating cash |

The accounts most agencies get wrong

The biggest mistakes are structural.

First, founders bury direct labor inside payroll overhead. That kills visibility. Delivery payroll belongs in cost of goods sold when employees are doing client work.

Second, they mix pass-through spend with agency revenue. That inflates top-line numbers and obscures actual margin.

Third, they skip client-funds liability accounts. If you hold client media money, your books should show that you are holding it, not earning it.

Your accounting software should mirror how the agency operates. If the books don't distinguish labor, pass-throughs, WIP, and client funds, the reporting will always be late and misleading.

If you're cleaning up system design, it helps to connect project and operational data cleanly. For agencies using QuickBooks and delivery tooling together, a practical reference is how Angelwood integrates with QuickBooks, because the integration question is usually where good account design either gets reinforced or broken.

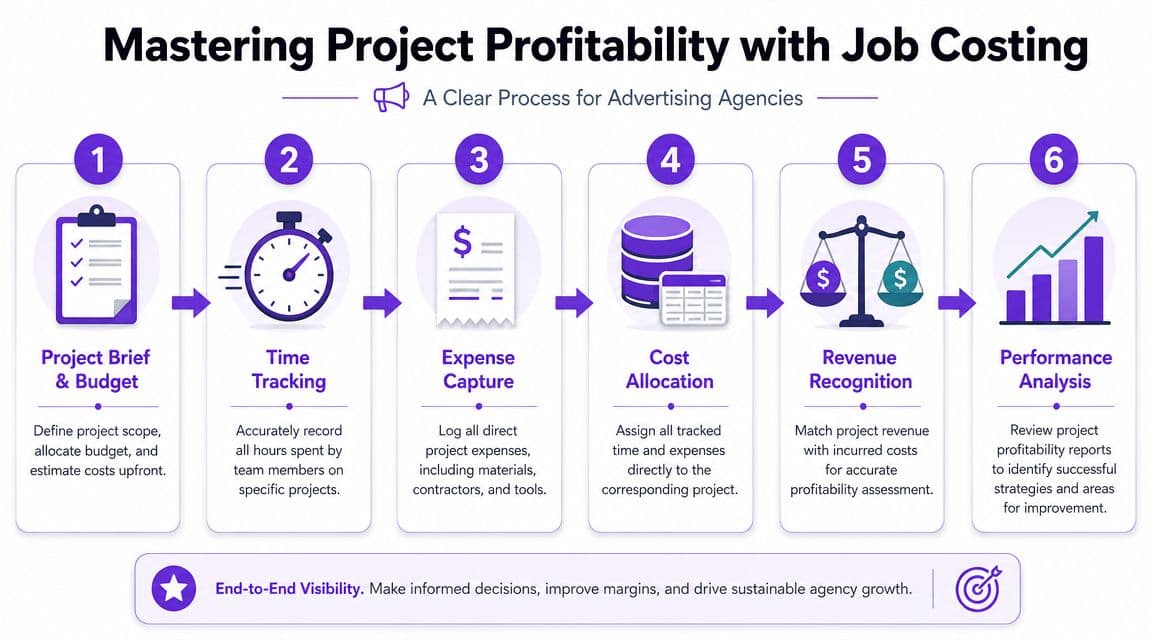

Mastering Project Profitability with Job Costing

Job costing is where agency accounting becomes useful. Without it, your P&L is a history report. With it, finance becomes operational.

Under ASC 606, agencies using accrual accounting must recognize revenue when services are transferred, not when invoices go out or cash comes in. For multi-month campaigns, that usually means recognizing revenue over time based on progress. If you ignore that, your monthly margin reporting is distorted from the start.

What job costing must include

A real job-costing system for an agency assigns each of these to the client and project:

- Recognized revenue tied to delivery progress

- Direct labor cost for employee time spent

- Contractor cost attached to the project

- Direct tools or production costs when they exist

- Gross margin by project, not just by month

Most agencies track time poorly, then wonder why profitability feels mysterious. Time is your inventory. If your team doesn't code time to clients and projects accurately, every margin number becomes suspect.

Worked example for a $50,000 project

Assume you signed a fixed-fee campaign project for $50,000. The project runs across two months.

You estimate total delivery effort at 400 hours. By the end of Month 1, the team has completed 160 hours of the work. That means the project is 40% complete based on labor progress.

Under over-time revenue recognition, you would recognize:

- Total contract value: $50,000

- Percent complete in Month 1: 40%

- Revenue recognized in Month 1: $20,000

Now assign direct costs incurred in Month 1:

- Employee labor cost on the project: $9,600

- Freelance design support: $3,000

- Direct production expense: $1,400

Total direct project cost in Month 1:

- $9,600 + $3,000 + $1,400 = $14,000

Month 1 gross margin on the project:

- Revenue recognized: $20,000

- Direct cost: $14,000

- Gross margin dollars: $6,000

- Gross margin percentage: $6,000 ÷ $20,000 = 30%

That is the number you should manage from. Not the invoice amount. Not the cash received. The recognized revenue matched to actual delivery cost.

Why invoicing and profitability are not the same

Let's say you invoiced the client $25,000 upfront at kickoff.

If you treated that full invoice as Month 1 revenue, your books would show:

- Revenue: $25,000

- Direct costs: $14,000

- Gross margin: $11,000

- Gross margin percentage: 44%

That looks far better than reality. But it's wrong for management purposes if only 40% of the work has been delivered. This is why founders think a project is fine until Month 2 exposes the overrun.

For a more complete operating framework, this guide to project accounting for agencies that want better profitability tracking gives the reporting structure I recommend.

A short explainer on the mechanics can help your team align on process:

A simple review cadence that works

You don't need a giant finance stack. You need discipline.

Review project economics every week using these questions:

| Question | What you're checking | What to do if it's off |

|---|---|---|

| Is recognized revenue aligned with progress? | Whether revenue is overstated or lagging | Adjust revenue schedules and WIP |

| Is labor burn ahead of budget? | Whether scope or efficiency is slipping | Re-scope, re-staff, or issue change order |

| Are contractor costs expanding? | Whether outsourced support is eating margin | Approve spend before work starts |

| Is gross margin acceptable? | Whether the project is worth continuing as priced | Raise fees, change scope, or exit the work |

The management standard I'd enforce

Job costing is not optional once you have multiple active clients and mixed delivery teams. If a PM can't tell you current budget burn, finance can't protect margin.

That's why I push agencies to use tighter operating controls, including better cost monitoring in project delivery. If you want a practical operations-side resource, WeekBlast for better cost control is useful because finance problems often start as delivery discipline problems.

The point of job costing isn't prettier reporting. It's catching margin failure while you still have time to fix pricing, staffing, or scope.

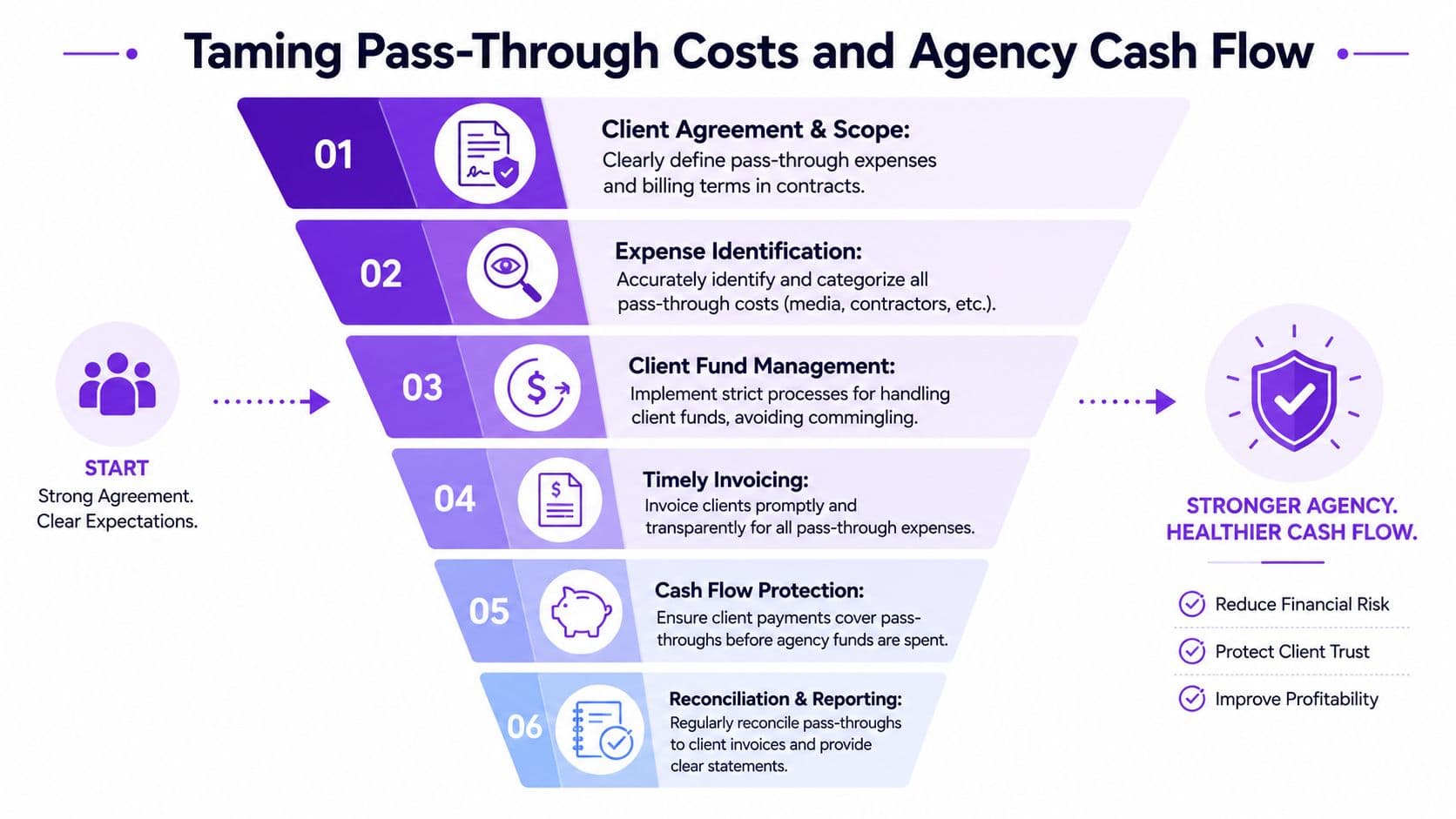

Taming Pass-Through Costs and Agency Cash Flow

Most agencies don't get into trouble because revenue is too low. They get into trouble because cash timing is sloppy, especially around media spend, contractors, and other pass-through costs.

One guide notes that unbilled services can represent 15% to 30% of monthly revenue for project-based firms, and that uneven payment timing for pass-through costs can put real strain on working capital. If you're fronting ad spend before collecting from the client, you are financing someone else's business with your balance sheet.

Stop commingling client money

If clients pre-fund media, production, or platform spend, keep that money out of your operating account. Use a separate bank account, clearing account, or dedicated card structure tied to your accounting workflow.

That does three things:

- Protects operating cash so payroll isn't competing with client spend

- Improves reconciliation because deposits and disbursements have a clean audit trail

- Reduces disputes because you can show exactly what was received, spent, and still held

The workflow I recommend

| Step | Control | Why it matters |

|---|---|---|

| Contract setup | Define pass-through billing terms and prepayment requirements | Prevents ambiguity before spend starts |

| Client funding | Collect funds before vendor payment when possible | Keeps the agency from floating spend |

| Cash segregation | Hold client money in a separate account or clearing structure | Avoids commingling |

| Spend authorization | Require approved budget before release | Stops account teams from improvising with cash |

| Reconciliation | Match vendor charges, client invoices, and held funds every month | Catches timing gaps fast |

The mistake founders rationalize

A founder says, “We know the client will pay. We've worked with them for years.”

That isn't a control. That's optimism.

If a client delays reimbursement and you've already paid Meta, Google, creators, publishers, or production vendors, your agency just became a lender. You took balance sheet risk without charging for it.

Cash discipline matters most with good clients. Bad clients expose weak controls fast. Good clients hide weak controls until the gap gets large.

Fix the cash-conversion gap

Use these rules:

- Invoice pass-throughs early: Don't wait until month-end if spend is accumulating quickly.

- Shorten the billing cycle: Weekly billing for large media or production activity is often cleaner than monthly billing.

- Track unbilled WIP every week: Don't let completed work sit off-invoice.

- Tie account management to collections: Client service shouldn't be separated from cash accountability.

- Review liquidity separately from profitability: A profitable month can still create a cash squeeze.

If your agency needs a stronger operating playbook for collections and working capital, this article on how agencies can improve cash flow with better finance controls is a solid next read.

The KPIs That Actually Drive Agency Growth

Most agency dashboards are cluttered. They report activity instead of economics.

You don't need dozens of metrics. You need a handful that force action. The best KPI set for accounting for advertising agencies answers four questions: Are you pricing work correctly, delivering efficiently, collecting cash fast enough, and building stable revenue?

“The target billable gross margin for a healthy agency should be 50% or higher. Anything below that indicates issues with pricing, efficiency, or scope creep that need immediate attention.” Jonathan Andrus, CEO of Contax Inc.

The KPI set I'd put on every founder dashboard

| KPI | What it tells you | How to use it |

|---|---|---|

| Gross margin by client | Whether each account is worth keeping | Reprice, re-scope, or exit bad-fit clients |

| Gross margin by service line | Which offerings deserve more sales effort | Shift demand toward higher-quality revenue |

| Retainer revenue trend | Whether recurring work is stabilizing the business | Monitor concentration and renewal health |

| Unbilled WIP | Whether delivery is outrunning billing | Tighten invoicing and PM handoff |

| Accounts receivable aging | Whether revenue is converting into cash | Escalate collections early |

| Utilization by delivery team | Whether staffing matches demand | Fix underuse or overloading before hiring |

A worked KPI example

Suppose one client generated $20,000 of recognized revenue this month and required $8,000 of direct labor plus $2,000 of contractor support.

Gross margin dollars:

- $20,000 - $8,000 - $2,000 = $10,000

Gross margin percentage:

- $10,000 ÷ $20,000 = 50%

That client is sitting on the benchmark Jonathan Andrus calls healthy. If another client at the same revenue level produces materially less margin because revisions never stop or account management hours are bloated, the issue isn't revenue. It's delivery economics.

Don't ignore channel-specific metrics

If influencer work is part of your service mix, finance should sit next to campaign measurement, not apart from it. A practical companion resource is this list of essential influencer marketing metrics, because channel reporting should tie back to contract structure, effort, and margin.

The KPI rule is simple. Every metric on your dashboard must have an owner and a decision attached to it. If nobody acts on it, remove it.

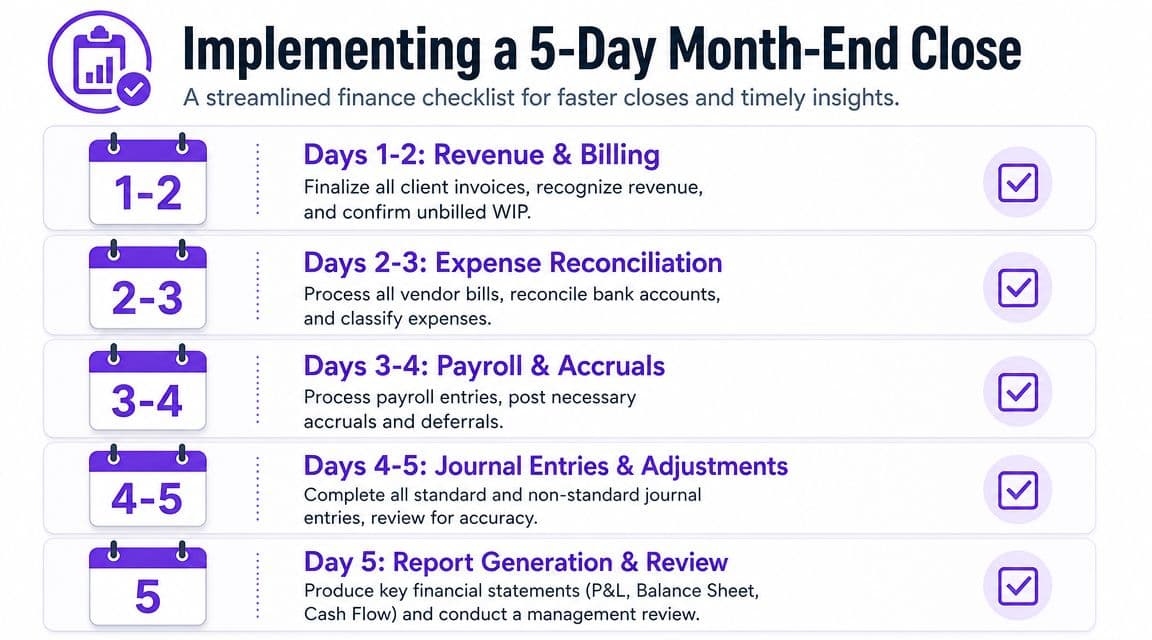

Implementing a 5-Day Month-End Close

If you're getting financials three weeks after month-end, they are too late to manage the current month. At that point, accounting becomes documentation, not control.

A five-day close is realistic for agencies if the workflow is standardized, ownership is clear, and project review happens before the books are finalized. Founders usually overcomplicate things. They think a fast close requires enterprise software. It doesn't. It requires a calendar, a checklist, and zero tolerance for lingering reconciliations.

The five-day workflow

| Day | Primary focus | Deliverable |

|---|---|---|

| Day 1 | Categorize transactions and reconcile cash | Clean bank and card activity |

| Day 2 | Record payroll, AP, and routine accruals | Updated expense base |

| Day 3 | Review project status and revenue recognition | Accurate WIP and earned revenue |

| Day 4 | Review draft financials and investigate anomalies | Corrected P&L and balance sheet |

| Day 5 | Finalize reports and hold management review | Decision-ready monthly package |

Where agencies usually get stuck

The bottleneck is rarely bookkeeping. It's missing operational inputs.

Project managers don't finalize status. Team leads approve time late. Vendor bills arrive after the close starts. Founders change classifications while reviewing draft statements. The result is the same every time. Finance waits on operations, then everyone complains that reporting is late.

Use a locked process instead:

- Cut off time entry quickly: Don't let labor reporting drift.

- Require PM signoff on project status: Revenue recognition depends on delivery progress.

- Accrue known costs even if bills haven't landed: Waiting for paperwork slows the close and weakens accuracy.

- Review exceptions, not every line item: Leadership should focus on unusual swings and margin changes.

What management should review on Day 5

Your review meeting should answer these points:

- Which clients or projects missed expected gross margin?

- What work was delivered but not yet billed?

- Did pass-through activity create any cash exposure?

- Are receivables aging in a way that needs founder involvement?

- What decisions need to happen this week on pricing, staffing, or collections?

A fast close is not about speed for its own sake. It gives leadership timely numbers while they can still change the outcome of the current month.

If you want a stronger operating checklist, this resource on month-end close best practices for growing finance teams is useful. Firms like Jumpstart Partners also provide outsourced controller support for agencies that need help building a repeatable close process tied to accruals, reconciliations, and management reporting.

Avoiding Costly Mistakes and Becoming Audit-Ready

Most agency finance problems are visible long before they become serious. Founders just normalize them.

Red flags you should treat seriously

- You don't know client-level gross margin. That means pricing and staffing decisions are happening blind.

- Client money touches the operating account. That creates custody risk and muddies reconciliations.

- Revenue follows invoices instead of delivery. That distorts monthly performance.

- Scope creep is discussed but not documented financially. Your team is doing unpaid work and calling it client service.

- Contractor costs are rising without project-level review. Margin can erode when outside support becomes the default.

- Month-end close depends on one person remembering everything. That's not a process. That's a failure waiting to happen.

Audit-ready doesn't just mean audit-ready

Strong accounting records help in more situations than formal audits. They matter when a lender asks for clean statements, when an investor asks how recurring revenue converts to cash, when a buyer reviews client concentration and margin quality, or when your own leadership team needs confidence in pricing decisions.

Audit-ready agencies do a few things consistently:

| Area | Audit-ready standard |

|---|---|

| Revenue | Clear support for how and when revenue was recognized |

| Costs | Direct costs tied to projects and clients |

| Cash | Reconciled balances and clean segregation of client funds |

| Contracts | Signed terms that support billing and pass-through treatment |

| Close process | Repeatable monthly checklist with approvals and support |

If you recognized your agency in the red flags above, fix the system now, not after a cash crunch, diligence request, or ugly client dispute. Clean books are useful. Decision-grade books are better. That's what lets you protect margin, stop financing clients, and run the agency with confidence.

If you need help building that system, Jumpstart Partners works with growing agencies on outsourced controller and bookkeeping support, including accrual-based reporting, month-end close discipline, and cash flow visibility. If your current books are technically accurate but operationally useless, that's the right time to bring in specialized help.