Financial Operations

How to Improve Cash Flow: A Founder's Playbook for Scaling Companies

Learn how to improve cash flow with our founder's playbook. Get actionable strategies on collections, billing, and forecasting for SaaS and service firms.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··22 min readYou can improve your cash flow in only three ways: accelerate cash inflows, delay cash outflows, and increase the amount of cash your operations generate. This isn't just about tweaking a few numbers. It's about getting paid faster, being smart about when you pay your own bills, and fine-tuning your pricing and costs. For founders of fast-growing businesses, mastering this isn't just good financial hygiene—it’s a survival skill.

Your Revenue Is Growing But Your Bank Account Is Not

It’s one of the most frustrating feelings for a founder: you're hitting record sales, but you're still scrambling to make payroll. If your business is pulling in between $500K and $20M in revenue and this sounds familiar, do not panic. It’s not a sign that you’re failing; it’s a sign your financial operations haven't kept up with your sales growth.

More revenue does not magically fix cash problems. It magnifies them.

The current economy makes this even harder. Leaders are feeling an unprecedented cash flow crunch. Only 30% of small business owners report profitability above their expectations for 2025, a massive drop from 57% the year before. This squeeze is pushing far too many founders toward high-risk loans with punishing interest rates just to stay afloat.

This guide is a direct, no-fluff playbook built for founders of SaaS, digital agencies, and professional services firms. We’ll show you the specific tactics that create breathing room and fuel actual growth. To even begin, you have to know where your money is going, which starts with knowing how to properly categorize your bank statements.

For quick cash flow improvements, focus on these three core areas. We will detail specific tactics for each in the following sections.

| Lever | Area of Impact | Potential Speed to Cash |

|---|---|---|

| Accelerate Inflows | Getting paid faster by customers | 1-2 weeks |

| Delay Outflows | Extending payment terms with suppliers | 2-4 weeks |

| Increase Operational Cash | Optimizing pricing and cutting waste | 4-8 weeks |

This table shows the immediate levers you can pull, but we’re going to go much deeper.

Instead of generic advice, we’ll focus on:

- Immediate tactical wins to get cash in the door now.

- Operational changes that build a resilient financial foundation for the long haul.

- Strategic forecasting to turn cash flow from a constant worry into a strategic asset.

This guide will break down the most common cash flow problems in small businesses and give you an actionable plan to build a company where your bank account finally reflects your success.

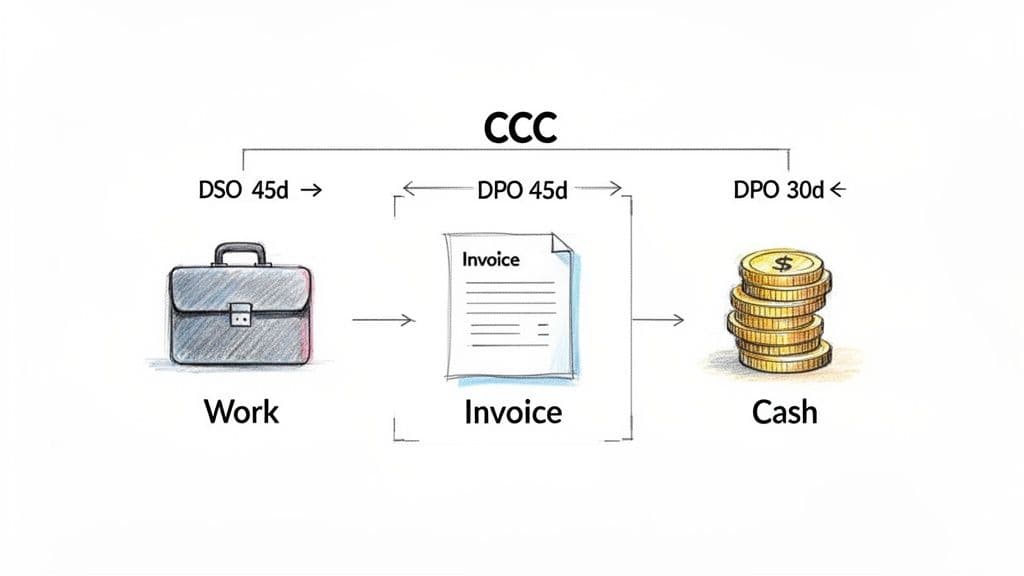

Secure Quick Wins by Shortening Your Cash Conversion Cycle

The fastest way to improve your cash flow isn't complex financial engineering—it's getting paid faster. The time lag between when you do the work and when the cash actually hits your bank is a silent business killer. This gap is your Cash Conversion Cycle (CCC), and making it shorter is the single most powerful lever you can pull for immediate impact.

Your CCC is the number of days it takes to turn your investments in services (your team's time and effort) into cash. For service and SaaS businesses, we zoom in on two key components: Days Sales Outstanding (DSO) and Days Payable Outstanding (DPO). The game is simple: shrink your DSO and strategically stretch your DPO.

Slash Your Days Sales Outstanding (DSO)

Days Sales Outstanding (DSO) is the average number of days it takes you to collect payment after a sale. A high DSO means your customers are using you as their free bank. Your cash is sitting in their accounts, not yours, and you're the one funding their operations. According to OpenView's 2024 SaaS Benchmarks, best-in-class companies maintain a DSO under 45 days, while the average hovers around 62 days.

Let's look at a digital agency with $2.4 million in annual revenue, or $200,000 a month. If your average DSO is 60 days, you have roughly $400,000 tied up in accounts receivable at any given moment. That's cash you've earned but cannot use.

Now, watch what happens when you cut that DSO from 60 to 45 days with a more disciplined collections process.

- Daily Revenue: $2,400,000 / 365 days = $6,575 per day

- DSO Reduction: 60 days - 45 days = 15 days

- Cash Unlocked: 15 days * $6,575/day = $98,625

Just by collecting cash 15 days faster, you inject nearly $100,000 of non-dilutive cash straight back into your business. That’s real money you can put toward payroll, a new marketing campaign, or critical growth initiatives. We have an entire playbook on what is accounts receivable management that dives deep into building this process.

Red Flags: Warning Signs of a Cash-Draining Client

Not all revenue is created equal. You must spot problem clients before they do real damage to your cash flow.

Keep an eye out for these red flags:

- Consistent Late Payments: A client who is always 15-30 days past due is not just disorganized; they are showing you a pattern.

- Disputing Every Invoice: Nitpicking minor details on every single bill is often a tactic to stall payment.

- Going Silent: If a client suddenly becomes unresponsive after an invoice is sent, it's time for immediate, direct follow-up.

- Requesting Extended Terms After the Fact: Asking for Net 60 or Net 90 after the work is already done puts you in an impossible position.

If you spot these patterns, tighten your credit policies for that client. This means requiring upfront deposits, switching to milestone-based billing, or, in some cases, having the courage to fire them if their payment habits do not improve.

Strategically Manage Your Days Payable Outstanding (DPO)

While shrinking DSO is all about getting cash in the door faster, managing Days Payable Outstanding (DPO) is about intelligently timing your cash outflows. Let me be clear: this does not mean you stop paying your bills. It means negotiating favorable terms with vendors and using payment schedules to your strategic advantage.

One quick win here often lies in your back-office operations. Simple accounts payable process improvement can shorten processing times and give you better control over payment timing, which directly impacts your cash conversion cycle.

For SaaS businesses, top-tier vendors often operate on standard Net 30 terms. According to OpenView's 2024 SaaS Benchmarks, a healthy DPO for a software company usually falls between 30 and 45 days. Pushing it much further can damage crucial relationships with your suppliers.

Focus your energy on negotiating with non-critical vendors. Can you consolidate smaller software subscriptions onto a single corporate credit card that gives you a 30-day float? Can you ask your office supply vendor for Net 45 terms? These small adjustments add up, giving you valuable breathing room in your cash position.

Optimize Your Pricing and Billing for Predictable Revenue

Your pricing and billing strategy is not an administrative chore—it's one of the most powerful, and most overlooked, levers for fixing your cash flow. If you are not strategic, you are not just billing clients; you are involuntarily financing their operations.

For a services firm, this is the all-too-familiar pain of finishing a massive project and then waiting 30, 60, or even 90 days to see a single dollar. For a SaaS company, it's about breaking the exhausting month-to-month cash flow cycle and building a truly predictable revenue base.

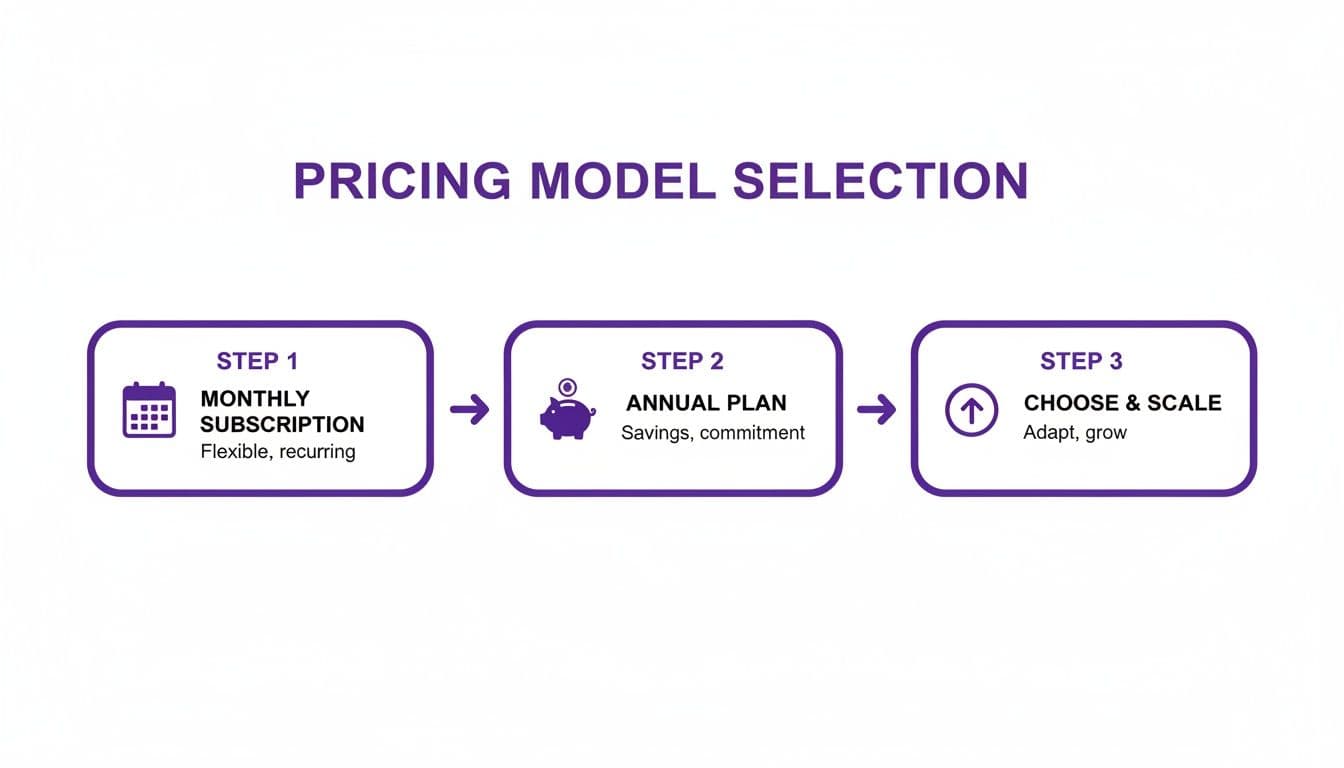

The Cash Flow Power of Annual Plans

For any SaaS company, the fastest way to inject cash into the business is by shifting customers from monthly to annual contracts. The impact is immediate. While your recognized revenue for accounting purposes stays the same month to month, the upfront cash fundamentally changes your working capital.

Let's run the numbers. Say you have a $1,000 per month SaaS plan.

| Billing Cadence | Monthly Cash Flow (First Month) | Annual Cash Flow (First Month) |

|---|---|---|

| Cash In | $1,000 | $12,000 |

| Recognized Revenue | $1,000 | $1,000 |

Just by switching one customer to an annual plan, you pull an extra $11,000 in cash into your bank account on day one. Now, imagine converting just 20% of your 100 customers to annual plans. That’s $220,000 in immediate cash (20 customers x $11,000) you can use to fund growth, hire that key engineer, or build a buffer.

You can learn more about how this impacts your financial reporting by reading our guide on annual recurring revenue.

Customers will ask why they should pay upfront. You need a confident, value-first answer ready.

- Script: "We offer an annual plan for a couple of key reasons. First, you get a 15% discount, so you're locking in significant savings over the year. Second, it simplifies budgeting and billing for your team with just one invoice instead of twelve. For us, it allows us to invest more aggressively in our product roadmap, which means you see new features and improvements much faster."

Stop Being a Bank for Your Service Clients

For digital agencies and professional services firms, the real cash flow killer is project-based billing that leaves you completely exposed. If you only invoice when a project is "done," you are funding 100% of the project costs—your team's salaries, your overhead, everything—for months at a time. This model is a recipe for disaster.

It's time to realign your billing structure with your service delivery.

- Upfront Deposits: Require a 25-50% deposit before a single minute of work begins. This confirms the client is serious and immediately covers your initial mobilization costs.

- Milestone Billing: Break large projects into distinct phases. Tie payments to the completion of each milestone. This way, you get paid as you deliver value, not months after the fact.

- Retainer Models: For any ongoing work, move clients to a retainer model. They pay a fixed fee each month, creating predictable, recurring revenue that smooths out the lumpy cash flow of project work.

Shifting your billing model is not asking for a favor; it’s about aligning payment with the value you’re creating. Have confidence in that conversation.

"Pricing is the exchange rate on the value you create. If you only talk about your time and costs, you're anchoring the conversation to the wrong things. Frame every billing discussion around the outcome and ROI you deliver for the client, and value-based pricing becomes a natural conversation." — Kyle Brennan, Founder of Brennan Growth Advisors

Actionable Next Step: Pull up the agreements for your top five clients right now. Find the three biggest opportunities to implement these changes—whether it’s pitching an annual plan to a monthly SaaS user or proposing a retainer to a major project client. This exercise alone can uncover tens of thousands of dollars in cash flow you’re leaving on the table.

Build a 13-Week Cash Flow Forecast to See the Future

If you feel like you’re constantly firefighting cash problems, it’s because you are looking in the rearview mirror. To move from reactive panic to proactive strategy, you need to see what’s coming. The single most powerful tool for this is the 13-week cash flow forecast.

This is not an abstract accounting exercise. Think of it as your business’s financial radar, letting you spot cash crunches months—not days—away. It's a simple, week-by-week map of every dollar coming in and every dollar going out.

Forget the intimidating software. At its heart, a 13-week forecast is a powerful log of expected cash movements that gives you a real-time pulse on your financial health.

The Anatomy of a 13-Week Forecast

Your first forecast starts with a basic structure tracking all cash movements for the next quarter. You'll organize it into two main buckets: cash inflows and cash outflows.

Cash Inflows:

- Customer Collections: Use your AR aging report to project when existing invoices will actually get paid. Be honest here—if a client always pays 15 days late, your forecast must reflect that reality.

- New Sales: Look at your sales pipeline and project when newly closed deals will turn into cash in the bank.

- Other Income: Do not forget other cash sources like financing draws, asset sales, or tax refunds.

Cash Outflows:

- Payroll & Benefits: This is almost always your largest and most predictable expense.

- Rent & Utilities: These fixed costs are easy to forecast.

- Software Subscriptions: Map out every recurring SaaS payment.

- Taxes: Factor in payroll taxes, sales tax, and any quarterly income tax payments.

- Vendor Payments: Your AP aging report is your guide for scheduling payments.

- Loan Payments & CapEx: Debt service and one-time large purchases have to be in here.

Seeing it all laid out week-by-week immediately flags future cash deficits. This gives you the breathing room to act before you're in a crisis, turning the finance function from a reactive cost center into a strategic partner.

The Non-Negotiable Starting Point

Your forecast is only as strong as its foundation. You must begin with a perfectly reconciled opening cash balance. If you’re off by even a few thousand dollars in Week 1, that error will cascade through the entire model, making your projections dangerously useless.

This is exactly where most founders get tripped up. Nailing the opening balance means pulling detailed, accurate accounts receivable and accounts payable aging reports and reconciling them against your current cash position.

"A forecast without a reconciled opening balance isn't a forecast—it's a guess. Garbage in, garbage out. The discipline of reconciling your cash every week is what separates businesses that control their destiny from those that are controlled by it." — Jonathan Wu, CPA, Partner at Jumpstart Partners

Stress-Testing Your Business with Scenarios

This is where your forecast evolves from a static report into a dynamic strategic tool. Once you have a baseline, you can start running "what-if" scenarios to see how resilient your business really is.

- Scenario 1: The Late-Paying Whale: What happens if your largest client pays 30 days late? Plug that assumption into the model and watch what it does to your ending cash balance. Do you dip below your minimum operating cash level?

- Scenario 2: The Lost Deal: That big Q3 deal you’re banking on—what if it slips to Q4, or you lose it entirely? Remove that inflow from the forecast. Can you still cover payroll?

- Scenario 3: The Annual Discount Push: What if your campaign to convert 20% of your monthly SaaS customers to annual plans succeeds next month? Model that huge cash influx and see how it transforms your runway.

Visualizing the impact of different billing cadences is one of the most powerful ways to truly understand the levers you can pull to manage cash.

By simulating these possibilities, you prepare for them. Maybe it means proactively drawing on a line of credit, launching a targeted collections campaign, or holding off on a non-essential hire. You’re no longer just reacting to surprises; you’re making data-driven decisions. To really nail this, check out our complete guide on building a 13-week cash flow forecast.

Actionable Next Step: Make this a weekly ritual. Every Monday, your finance leader must update the forecast with last week's actual numbers, analyze any differences, and add a new "Week 13" to the end. This continuous loop makes your predictions more accurate over time and embeds proactive cash management right into the DNA of your company.

Your 90-Day Cash Flow Implementation Plan

All the strategies we've covered are powerful, but they are just theory without execution. Let's turn that knowledge into a concrete, 90-day roadmap your team can follow to drive real, measurable improvement in your cash position.

This is not about trying to fix everything at once. It's about building momentum through focused, 30-day sprints. Each block targets specific, high-impact activities that will deliver tangible results, giving your growth plans the rock-solid cash foundation they need to succeed.

Days 1-30: Score Quick Wins and Build Momentum

The first month is all about stopping the bleeding and getting immediate visibility. The goal is to plug the most obvious leaks and get a crystal-clear picture of your cash reality. These are actions you can start today and see results from within a few weeks.

Your priorities for the first 30 days are:

- Hunt down your overdue cash. Run a detailed AR aging report and immediately zero in on every invoice more than 30 days past due. This becomes your collections war room list.

- Focus on the biggest impact first. Do not get paralyzed by the entire list. Pick your top five overdue accounts by dollar amount and start a disciplined, daily follow-up process. Get that money in the door.

- Put reminders on autopilot. Set up automated invoice reminders in your accounting software. A simple cadence—like 7 days before the due date, on the due date, and 7 days after—offloads a massive amount of manual work and speeds up payments.

Days 31-60: Shore Up Your Operations

With some quick wins secured, the next 30 days are about fixing the operational weaknesses that created cash gaps in the first place. You’ll shift from playing reactive defense with collections to building proactive, resilient financial processes.

This is where you embed better habits into your day-to-day operations:

- Rewrite your payment terms. Pull the contracts for your five largest clients. Where can you move from billing after the fact to getting paid upfront? Look for opportunities to require deposits or switch to milestone-based payments.

- Build your first 13-week forecast. Using the principles we covered, build your version 1.0 forecast. It will not be perfect, but it will be a powerful tool for making smarter decisions. Our guide on cash flow forecasting best practices can walk you through the process step-by-step.

- Flex your negotiating muscle. Find one non-critical vendor and negotiate a payment term extension from Net 30 to Net 45. It’s a small win, but it builds your team's confidence for bigger negotiations down the road.

Days 61-90: Move to Strategic Optimization

In the final 30 days, you shift from defense to offense. You will use the data and stability you have created to make strategic moves that fundamentally improve your business's ability to generate and hold onto cash. This is where you directly connect financial operations to your growth strategy.

During this final sprint, you will:

- Conduct a full pricing and packaging review. Go through your service offerings and SaaS plans with a fine-tooth comb. Where are the opportunities to push for annual subscriptions, implement value-based retainers, or simply increase prices?

- Start modeling the future. Use your 13-week forecast to model best-case, worst-case, and most-likely scenarios for the next quarter. This transforms strategic planning from a gut-feel exercise into a data-driven conversation with your leadership team.

Your 90-Day Cash Flow Improvement Checklist

Turning a plan into reality requires a clear, actionable checklist. Use this table to guide your team over the next three months, ensuring you stay focused on the key actions that will drive real change in your cash position.

| Timeframe | Key Action | Objective |

|---|---|---|

| Days 1-10 | Run AR Aging Report & Target Top 5 Overdue Accounts | Immediately identify and begin collecting on largest overdue invoices. |

| Days 10-20 | Automate Invoice Reminders | Systematize collections follow-up to reduce manual effort and speed up payments. |

| Days 20-30 | Hold First Weekly Cash Huddle | Establish a rhythm of reviewing cash inflows, outflows, and AR aging with the team. |

| Days 31-45 | Review Top 5 Client Contracts for Payment Terms | Identify opportunities to switch from arrears to upfront or milestone payments. |

| Days 45-60 | Build and Review First 13-Week Cash Flow Forecast | Gain forward-looking visibility into your cash position to make proactive decisions. |

| Days 61-75 | Perform Full Pricing & Packaging Review | Identify opportunities to increase prices, push annuals, or improve margins. |

| Days 75-90 | Model Financial Scenarios with Leadership Team | Use your forecast to stress-test your strategy and plan for different outcomes. |

This 90-day plan is not a one-time fix; it's a system for building continuous improvement into your financial operations. By following these steps, you will create the stability and visibility you need to grow confidently.

Frequently Asked Questions About Cash Flow Management

As founders and finance leaders start to scale, we see the same cash flow questions pop up again and again. Here are the direct answers to the questions we hear most, designed to clear up common misconceptions and give you a clear path forward.

What is the difference between cash flow and profit?

Profit is an accounting concept; cash is what you use to pay your bills. You cannot make payroll or keep the lights on with paper profits.

Your income statement shows profit—it’s your revenue minus expenses. But it includes non-cash items like depreciation and, more importantly, it recognizes revenue when it's earned, not when the payment actually lands in your bank account.

Cash flow is the literal movement of money into and out of your business. A company can look highly profitable on its P&L but go bankrupt because its clients pay too slowly. That’s a classic case of negative cash flow killing a "profitable" business. Getting this distinction right is fundamental to your survival.

How often should I review my cash flow forecast?

For any business in the $500K to $20M range, your 13-week cash flow forecast is not a static budget you set once a year. It's a living, breathing document that has to be reviewed and updated weekly.

Every week, you must run this simple but critical process:

- Drop in your actual cash inflows and outflows, replacing the numbers you forecasted for the previous week.

- Analyze the variances. Where were you right, and where were you wrong? Why?

- Add a new "Week 13" to the end of your forecast using your updated assumptions.

This rolling process creates a powerful feedback loop. Your forecast gets smarter and more accurate over time, letting you spot potential cash shortfalls months in advance, not days. This is how you shift from reactive fire-fighting to proactive financial strategy.

My team is at capacity. How can we implement this?

This is the most common—and most valid—objection we hear from lean, growing companies. The answer is simple: do not try to do everything at once. Overloading your team is a surefire way to guarantee nothing gets done. Focus on the highest-impact, lowest-effort moves first. The 90-day plan in this guide was designed specifically for this reality.

"The bottleneck in improving cash flow is almost never a lack of knowledge. It's a lack of execution capacity and clean data. Start with one thing—usually collections—and build from there. Success breeds momentum." — Jonathan Wu, CPA, Partner at Jumpstart Partners

Instead of trying to overhaul the entire company, start small and build momentum.

- Task one person with collections. For the next 30 days, their only job is to chase down your top five overdue accounts.

- Start with a simple forecast. Your first 13-week model does not need to be perfect. A basic spreadsheet tracking major cash movements is infinitely better than having nothing at all.

- Acknowledge the data problem. Often, the real issue is not capacity, but messy books that make any kind of forecasting impossible. That’s a clear signal it might be time to bring in an outsourced partner to clean up your data and handle the modeling, freeing up your team to focus on growth.

When should I consider a line of credit?

The absolute best time to secure a line of credit is when you do not need it. Banks are eager to lend to healthy, organized businesses; they run from companies that are already in the middle of a cash crisis.

Think of a line of credit as a strategic tool, not a Band-Aid for a broken business model. Its purpose is to bridge temporary, predictable cash gaps—like covering payroll while you wait for a large client check to clear—not to finance ongoing losses.

Before you even think about talking to a lender, you must have a reliable 13-week cash flow forecast in hand. It proves you understand your capital needs, have a plan to repay the funds, and are a low-risk borrower. Walking into a bank with a detailed forecast instantly boosts your credibility and dramatically increases your chances of getting approved. It shows you know exactly how to improve cash flow and are just looking for a tool to manage its timing.

This playbook provides the roadmap, but execution is everything. The team at Jumpstart Partners specializes in implementing these systems for growing businesses like yours, delivering a 5-day month-end close and the cash flow visibility you need to scale confidently.

Stop guessing and start forecasting. Schedule a consultation with Jumpstart Partners today to build a financial foundation that supports your ambition.