Financial Operations

Accounting for Marketing Agencies: A Founder's Guide

Master accounting for marketing agencies. This guide covers job costing, revenue recognition, KPIs, and software for founders to drive profitability.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readYour agency can post solid top-line revenue and still be badly under-managed. The reason is simple. Standard bookkeeping hides agency economics. It records cash, invoices, and expenses, but it doesn't show which clients earn money, which engagements burn hours, and where your margin disappears.

That failure is expensive. Marketing agencies lose an average of 10-15% of annual revenue through unbilled hours and poor time tracking, and agencies that review time entries against billing each month typically recover $47K+ in missed margin per client annually, according to Basta CPA's analysis of accounting mistakes in marketing agencies.

If you're serious about accounting for marketing agencies, stop treating finance as compliance work. It's an operating system. You need clean revenue recognition, client-level job costing, a chart of accounts built for agency work, and a dashboard that tells you when profit is slipping before your bank account does.

Why Your Agency Is Leaking Profit (And How to Stop It)

Your bank balance is not a performance metric. It's a lagging snapshot.

Agencies fail financially in predictable ways because they use generic bookkeeping built for simple businesses. But your business isn't simple. Your inventory is team time. Your cost of goods sold often includes labor, freelancers, software tied to client work, and pass-through spend. If you don't track those costs by client and project, you're guessing at profitability.

What standard bookkeeping misses

A typical bookkeeper will tell you whether revenue went up and whether expenses stayed within range. That's not enough.

You need answers to harder questions:

- Which clients produce healthy gross margin: Not just who pays the biggest retainer.

- Which projects absorb extra hours: Scope creep doesn't show up clearly in a generic P&L.

- Which service lines are underpriced: Strategy, creative, paid media, SEO, and production rarely carry the same economics.

- Where the month broke down: Poor invoicing discipline, weak time capture, and misclassified costs all distort results.

Practical rule: If you can't pull a client-level margin report from your accounting stack, you don't know your agency's real profitability.

The fix starts with operational discipline, not more reports. Tie timesheets to clients. Allocate direct costs correctly. Review billable hours against contracts every month. Then compare actual performance against plan. If you need a simple framework for that review cadence, this guide to budget variance for founders is useful because it shows how to spot where actual results drift from budget before those gaps become chronic.

The real issue is visibility

Founders often assume their problem is pricing. Sometimes it is. More often, the core problem is that nobody can see margin erosion until months later.

You don't need prettier financials. You need accounting for marketing agencies that surfaces the leaks fast enough to act. That means client-level reporting, disciplined billing controls, and month-end reviews that connect hours worked to revenue earned.

Build a Chart of Accounts That Tells You the Truth

Your chart of accounts is either a decision tool or a dumping ground. Most agencies use the second version.

A generic chart of accounts lumps all revenue into one bucket and all subcontractors, software, and labor into broad expense categories. That produces financial statements, but it doesn't produce insight. You can't tell whether retainers outperform project work. You can't isolate direct delivery costs from overhead. And you can't calculate true gross margin with confidence.

Stop using a generic structure

Your chart of accounts should reflect how your agency earns money and how work gets delivered.

Here's the difference.

| Structure | Bad generic version | Good agency-specific version |

|---|---|---|

| Revenue | One “Service Revenue” account | Separate accounts for retainer revenue, project revenue, and performance-based or commission revenue |

| Cost of Goods Sold | One “Subcontractors” line and maybe “Payroll” in operating expenses | Direct labor, freelancer costs, subcontractors, client-specific software, media or pass-through costs |

| Operating Expenses | Mixed admin and delivery costs | Clear overhead categories such as sales and marketing, general software, rent, admin payroll |

| Reporting value | Tells you total company profit | Tells you service mix, gross margin quality, and where delivery costs are rising |

A practical chart of accounts blueprint

Set up your revenue accounts around the three common agency models described in NetSuite's overview of accounting for marketing agencies: retainers, project-based fees, and performance-based compensation.

Use separate accounts such as:

- Retainer revenue: Monthly recurring client work

- Project revenue: One-time campaigns, builds, launches, audits

- Performance or commission revenue: Affiliate, revenue share, or outcome-based fees

Then build cost accounts that mirror delivery reality:

- Direct labor: Team time spent on client work

- Freelancers and subcontractors: External specialists tied to delivery

- Client software and tools: Platform subscriptions used for specific engagements

- Media and pass-through spend: Only if you need separate visibility and proper classification

Where agencies usually get this wrong

Most agencies bury direct labor inside payroll overhead. That's a mistake. If the team delivers client work, part of that payroll belongs in cost of goods sold for margin analysis.

Your chart of accounts should answer management questions before you ever export a report.

A clean setup in QuickBooks or Xero should let you see:

- revenue by type,

- direct delivery costs by type,

- overhead separately,

- gross margin before overhead,

- operating margin after overhead.

If your current file can't do that, rebuild it. Don't patch around a broken structure.

For a deeper breakdown of account design choices, this article on what a chart of accounts is is a solid companion.

Mastering Agency Revenue Recognition and Billing

Most agencies don't have a billing problem. They have a timing problem.

You collect cash upfront, start work later, change scope midstream, and blend recurring access with discrete deliverables in the same contract. If you recognize that revenue loosely, your P&L becomes fiction. You'll think you had a strong month when you pulled cash forward from future work.

The three revenue streams need different treatment

Agencies usually work across retainers, fixed-fee projects, and variable fees. Those streams should not hit the books the same way.

- Retainers: If a client pays for ongoing monthly access or stand-ready service, recognize revenue as that service period passes.

- Fixed-fee projects: Recognize revenue based on work performed, not just when the invoice is paid.

- Performance-based fees: Record revenue when the underlying trigger is earned and supportable under the contract.

This matters a lot for hybrid agreements. According to Sage's discussion of accounting for marketing agencies, for agencies with $1M-$5M revenue, untracked change orders and performance obligations under ASC 606 create deferred revenue mismatches, with an estimated 40% of agencies understating liabilities by 15-25% in pre-audit financials. The same source notes that failing to segment stand-ready retainer obligations from discrete project deliverables is a common cause of audit failure.

Worked example for deferred revenue

Here's the clean way to handle an upfront payment.

Assume a client pays $15,000 at the start of a three-month project.

If the work is delivered evenly over the three months, your accounting should look like this:

| Month | Cash received | Revenue recognized | Deferred revenue remaining |

|---|---|---|---|

| Month 1 | $15,000 | $5,000 | $10,000 |

| Month 2 | $0 | $5,000 | $5,000 |

| Month 3 | $0 | $5,000 | $0 |

Cash arrived in Month 1. Revenue did not.

If you book the full $15,000 as revenue immediately, Month 1 looks stronger than it is, and Months 2 and 3 look weaker than they are. That distorts pricing analysis, hiring decisions, and owner expectations.

Rule of thumb: Cash timing affects liquidity. Revenue timing affects truth.

Why billing workflows fail in practice

Most agencies know the concept. They fail in execution because contracts and accounting aren't connected.

Common failure points include:

- Change orders not documented: Extra work gets performed but never formally priced, billed, or reflected in revenue schedules.

- Hybrid contracts not split: A monthly retainer and a defined project sit on one invoice, so nobody separates the obligations.

- Deferred revenue not reviewed monthly: Liability balances drift because no one ties invoices to delivery periods.

- Books run on cash logic: The agency records what cleared the bank instead of what was earned.

If you need a practical reference for ASC 606 workflows in service businesses, this guide to 606 revenue recognition is worth reading.

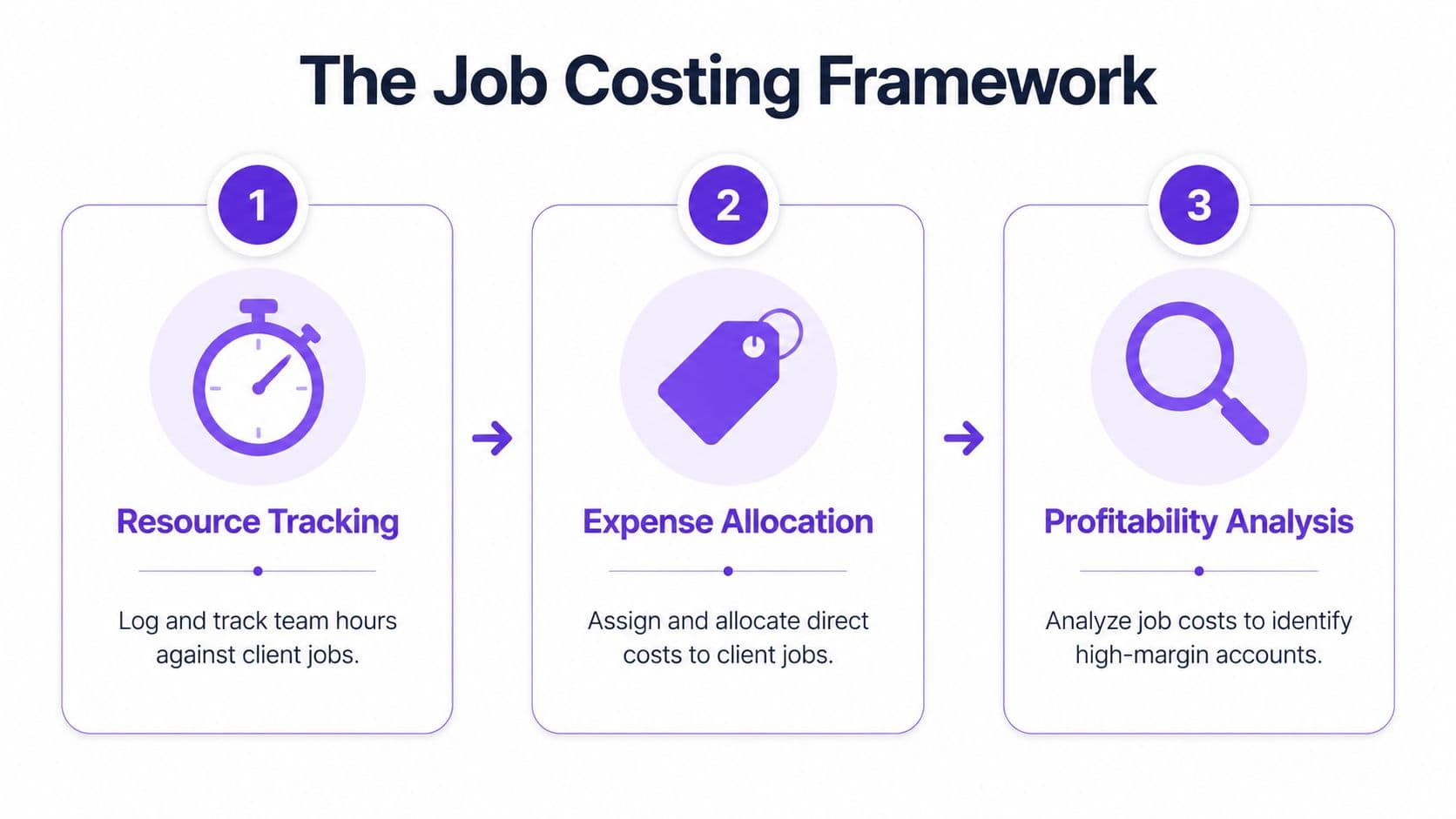

The Job Costing Framework for True Profitability

Agencies do not lose profit in the P&L summary. They lose it inside client work that looked busy, got delivered, and never got priced, tracked, or staffed correctly.

Job costing exposes the leak. It shows which accounts produce healthy gross profit, which ones are subsidized by your team, and which hybrid deals were sold in a way that guarantees margin erosion.

The framework

Start with three controls.

-

Track labor where the work happened

Every strategist, media buyer, designer, and account manager should log time to a client and a project code every day. Weekly reconstruction produces fiction. If your SEO team spends 18 hours on Client C and logs it to a generic delivery bucket, you cannot measure margin by account. -

Assign every direct cost to the same job

Subcontractors, ad spend management labor, client-specific software, list purchases, production costs, and pass-through expenses belong in the client record. If those costs sit in overhead, weak accounts look profitable. -

Review gross profit by client, service line, and project type

A blended agency margin hides bad pricing. You need to know whether retainers, one-off projects, paid media management, web builds, and content production each make money after labor and direct costs.

The formula is simple:

Gross profit = Revenue recognized for the job - direct labor - direct project costs

The hard part is getting the inputs right.

A worked example for a hybrid agency contract

Take a common hybrid deal:

- Monthly retainer for strategy and reporting: $8,000

- Landing page project sold alongside the retainer: $12,000

- Total contract value across the first month of work: $20,000

Now look at what happened in Month 1:

| Hybrid client, Month 1 | Amount |

|---|---|

| Revenue recognized, retainer portion | $8,000 |

| Revenue recognized, project portion | $6,000 |

| Total revenue recognized | $14,000 |

| Direct labor, strategy team | $3,200 |

| Direct labor, design and dev team | $5,100 |

| Freelance copywriter | $1,200 |

| Client-specific software and tools | $500 |

| Gross profit | $4,000 |

| Gross margin | 28.6% |

That margin is a problem.

The agency likely sold the landing page project too cheaply, staffed it with expensive senior labor, or let scope drift beyond the original estimate. If the owner only sees the client paying $20,000 and assumes the account is strong, the team keeps repeating an unprofitable delivery model.

Now compare that to what many agencies book by mistake. They record the full $20,000 as current-month revenue, miss the copywriter invoice until next month, and keep part of delivery payroll in overhead. The internal report then shows a healthy client margin that does not exist.

That is how bad pricing survives for six months.

Where job costing usually fails

The failure is rarely the formula. The failure is the operating discipline behind it.

Watch for these issues:

- Delivery payroll sits in overhead. Gross margin looks inflated because the people doing the work are missing from cost of sales.

- Time is logged late or not at all. Client effort disappears, especially account management and revision rounds.

- Freelancer bills hit after month-end. One month looks strong, the next looks weak, and neither is useful.

- Project codes are inconsistent. The same client work ends up split across multiple names or generic expense buckets.

- Hybrid contracts are tracked as one blob. Retainer work and project work have different economics, but the books combine them.

- Change requests are delivered without a budget update. Labor rises, revenue does not.

One rule matters here: if labor is not assigned to the job, the client P&L is wrong.

What to do with the result

Use job costing to make decisions quickly.

If a client sits below your target gross margin for two consecutive months, do one of four things:

- raise the fee

- reduce labor hours

- cut scope

- change the staffing mix

Do not keep a low-margin account because top-line revenue looks good. Revenue that consumes your best people and produces weak gross profit blocks growth.

This is also why agencies need project-level accounting, not just monthly bookkeeping. If you want the mechanics, this guide on project accounting agencies use to track profitability walks through the reporting structure in more detail.

Some of the setup principles are similar in other job-costed businesses. This article on mastering QuickBooks for contractors is useful because the same discipline applies. Clean project codes, timely cost capture, and job-level reporting produce better decisions.

If you need a finance partner to build these workflows inside your existing systems, Jumpstart Partners provides agency-focused controller and bookkeeping support, including project accounting setup and reporting.

The Agency KPI Dashboard You Must Be Tracking

Once your accounting foundation is clean, your dashboard should tell you what's happening before the month gets away from you.

Most agency dashboards are too shallow. They show revenue, maybe cash, and maybe net income. That's reporting for spectators. Operators need leading and diagnostic metrics.

The core metrics

According to Wow Remote Teams' benchmarks for marketing agency accounting, healthy marketing agencies should target gross profit margins of 50-70%, operating margins of 15-25%, and net profit margins of 10-20%. The same source says the average agency utilization rate hovers around 73%, and notes that a strong gross margin paired with a weak net margin indicates that overhead costs are too high.

Use those benchmarks to evaluate this dashboard:

| Metric | Target Range | What It Measures |

|---|---|---|

| Gross profit margin | 50-70% | Delivery efficiency after direct costs |

| Operating margin | 15-25% | Profit after overhead allocation |

| Net profit margin | 10-20% | Bottom-line performance after all expenses including owner compensation |

| Utilization rate | Around 73% | How much of your team's available time is spent on billable work |

| Realization rate | Track internally | How much billable work actually gets invoiced |

| Days sales outstanding | Track internally | How quickly clients pay |

| Cash forecast accuracy | Track internally | How reliable your short-term planning is |

| Customer acquisition cost | Track internally | What it costs to win a new client |

Worked CAC example

Customer Acquisition Cost is straightforward:

CAC = Total sales and marketing expense ÷ New clients acquired

Use the example provided in NetSuite's agency accounting guidance:

If you spend €30,000 on sales and marketing and acquire 12 new clients, your CAC is €2,500 per client.

Calculation:

€30,000 ÷ 12 = €2,500

That number matters because it tells you whether your growth engine is efficient. If CAC rises while gross margin weakens, you have pressure on both ends of the model. You're paying more to bring in clients and earning less from serving them.

What founders misread on KPI dashboards

The most common mistake is celebrating revenue growth while ignoring conversion quality and delivery economics.

Revenue growth with weak utilization and soft margins usually means your process is broken, not that your agency is scaling well.

Use the dashboard to answer practical management questions:

- Should you hire: Only if utilization is consistently tight and client margins justify added capacity.

- Should you raise prices: Yes, if realization is weak because scope and billing are out of sync.

- Should you cut overhead: Yes, if gross margin is healthy but operating margin lags.

- Should you invest more in sales: Only after CAC and client economics are visible together.

If your current reporting doesn't connect these metrics in one place, build a better operating view. This article on financial dashboards CEOs use to track key metrics and KPIs is a practical starting point.

Your Path to Financial Clarity

You don't need another finance theory deck. You need a tighter month-end process.

When accounting for marketing agencies is done well, the close tells you three things fast: what you earned, what it cost to deliver, and which clients are dragging down the business. If your team can't produce that view consistently, your process is still broken.

A month-end close checklist for agencies

Run this every month:

- Reconcile cash and receivables: Confirm invoices, collections, and open balances are accurate.

- Review deferred revenue: Match upfront billings to service periods and project completion status.

- Allocate all direct costs: Push labor, freelancers, software, and pass-through costs to the right client or project.

- Audit time entries against billing: Find missing billable hours, scope drift, and coding errors.

- Check client-level P&Ls: Flag low-margin accounts before they keep compounding.

- Review margin by service line: Know whether retainers, project work, or performance engagements carry the best economics.

- Compare actuals to plan: Look for expense overruns, weak realization, and overhead creep.

- Update your cash forecast: Uneven collections and project timing require active cash management.

What this looks like in practice

A disciplined close turns your books into a management tool. You stop debating whether the business feels profitable and start seeing exactly where margin is being created or lost.

If you've outgrown DIY bookkeeping and need structure around close management, reporting, and control, outsourced finance support usually makes sense. This overview of outsourced controller services explains what that layer should own.

If you want accounting for marketing agencies built around client profitability, clean revenue recognition, and a close process your leadership team can trust, talk to Jumpstart Partners. They work with growing businesses that need controller-level discipline, reliable monthly reporting, and better visibility into the numbers that drive decisions.