Financial Operations

Accounting in Startups: The Founder's Financial Playbook

Master accounting in startups with this guide. Learn to manage cash flow, build KPI dashboards, and prepare for audits—know exactly when to outsource.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readThe most popular advice in accounting in startups is also the most expensive: “Keep it simple until you’re bigger.”

That sounds lean. It isn’t. It’s how founders build a company on numbers they can’t trust, then discover the problem during a fundraise, a tax issue, or a cash crunch they should’ve seen coming.

If you’re running a business between $500K and $20M in revenue, accounting is no longer basic bookkeeping. It’s operating infrastructure. It tells you whether you’re profitable by customer, whether your pricing works, whether your burn is controlled, and whether an investor will trust your story.

The High Cost of Ignoring Your Startup's Finances

Founders love to compare finance work to admin. That’s a mistake. Messy books are a business risk, not a back-office inconvenience.

Kruze Consulting describes accounting debt as a parallel to technical debt, where ignoring financial infrastructure creates massive, expensive fixes later. The same source notes that an SSRN paper found improper revenue recognition under ASC 606 affects 70% of early-stage SaaS companies, often forcing restated financials during fundraising (Kruze on startup accounting debt and ASC 606 issues).

That’s the cost of DIY accounting. You think you’re saving cash. What you’re doing is delaying cleanup until the worst possible moment.

What accounting debt looks like in practice

It usually starts small:

- Founder-run bookkeeping: You code transactions at night, after sales calls and hiring interviews.

- Cash basis habits: You record what hit the bank, not what happened economically.

- No close process: Each month becomes a loose pile of reconciliations, receipts, and guesses.

- Generic accounts: Revenue, software, payroll, marketing. That’s not reporting. That’s storage.

Then the business grows. Revenue gets more complex. Payroll expands. Contracts include annual prepayments. Investor questions get sharper. Your books stop answering them.

Practical rule: If you can’t explain last month’s profit, cash movement, and biggest balance sheet changes in plain English, you don’t have a finance function. You have a ledger.

Cash flow is where founders usually pay the price first. Research highlighted by OpStart says cash flow problems are a major reason why nearly half of startups fail within the first five years. That’s why clean accounting matters long before an audit or a board meeting.

For startup owners and CEOs, this isn’t just a finance lesson. It’s a leadership one. You can’t delegate accountability for numbers you never built properly.

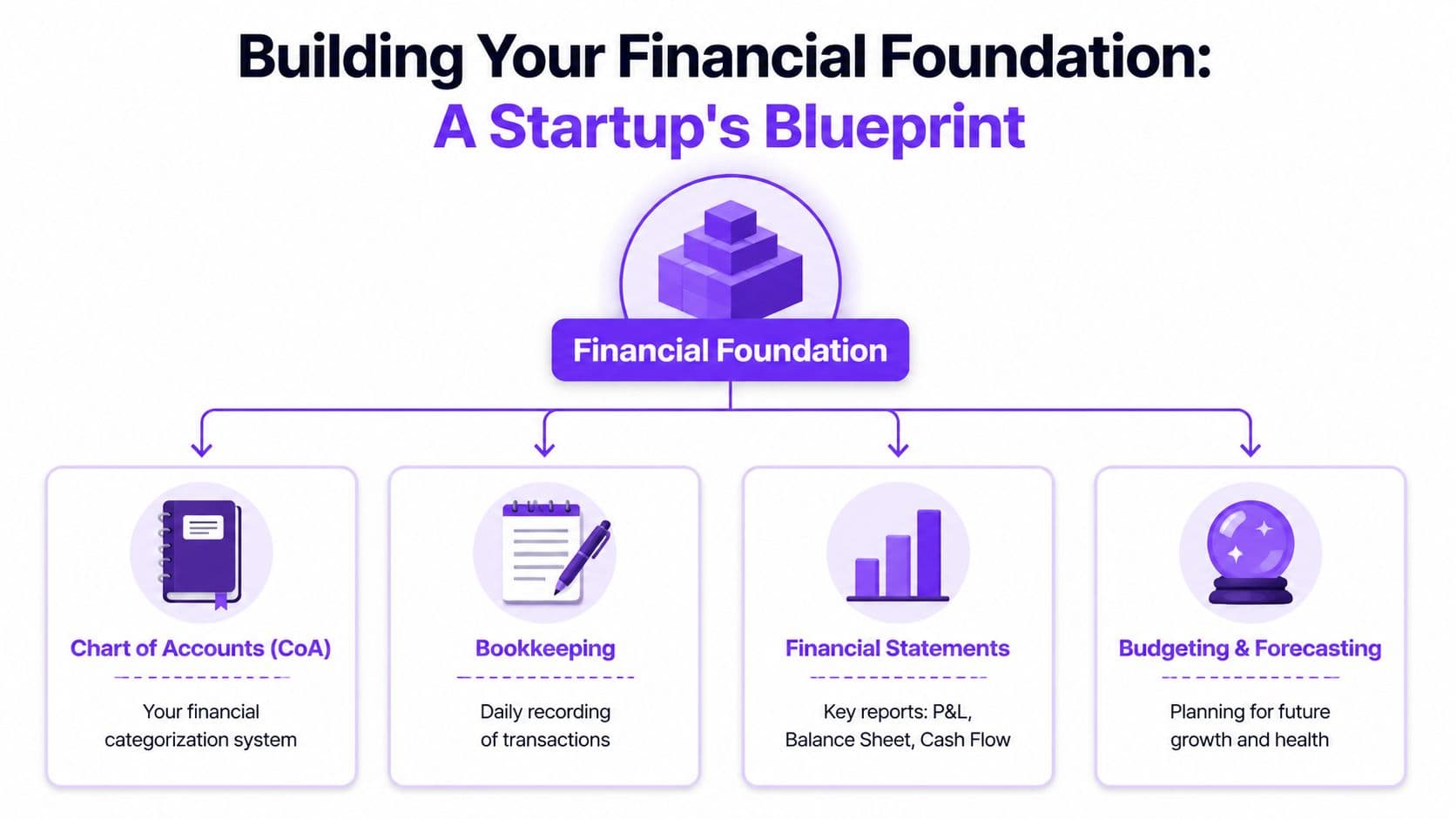

Building Your Financial Foundation from Day One

A real financial foundation has four parts: your chart of accounts, your bookkeeping process, your financial statements, and your budget discipline.

Most founders start with the default chart of accounts in QuickBooks or Xero. That’s fine for a freelancer. It’s weak for a scaling SaaS company, agency, or services firm.

According to Ramp, industry-specific charts matter. E-commerce startups need detailed inventory and fulfillment cost accounts, while SaaS companies need separate subscription revenue categories and cloud infrastructure costs to calculate meaningful KPIs (Ramp on startup accounting structures).

Your chart of accounts should match your business model

A generic chart hides the truth. A customized one exposes it.

For a SaaS company, your chart of accounts should separate items like:

- Subscription revenue types: Monthly plans, annual plans, implementation fees

- Cost to serve: Hosting, third-party software tied to delivery, support tooling

- Sales and marketing: Paid acquisition, commissions, contractors, events

- Product and engineering: Payroll, software, outside development

For an agency or professional services firm, the structure needs a different lens:

- Client revenue streams: Retainers, project fees, pass-through reimbursements

- Labor visibility: Billable payroll, non-billable payroll, contractor delivery costs

- Capacity tracking: Travel, software by team, subcontractors by client function

If your accounts don’t help you answer “Where do we make money?” they’re wrong.

For a practical setup guide, this walkthrough on bookkeeping for startups is useful because it gets into the operational details founders usually skip.

Finance team roles and responsibilities

A founder shouldn’t expect one person to do every finance job well. Recording transactions, building accurate reports, and steering the company are different disciplines.

| Role | Primary Focus | Key Activities | Typical Stage |

|---|---|---|---|

| Bookkeeper | Historical accuracy | Record transactions, reconcile bank and credit cards, maintain ledgers, organize receipts | Earliest stage and ongoing support |

| Controller | Reliable current reporting | Own close process, accruals, revenue recognition, balance sheet integrity, monthly reporting | Once reporting complexity starts hurting decisions |

| CFO | Forward-looking decisions | Forecast cash, plan hiring, support fundraising, guide pricing, model scenarios, communicate with investors | When leadership needs financial strategy, not just accounting |

The minimum foundation you need

You don’t need a bloated finance department. You need discipline.

Start here:

- Separate business accounts immediately. No personal card cleanup. No mixed expenses.

- Build a custom chart of accounts. Keep it simple, but make it useful.

- Close monthly. Every month. Same process. Same deadline.

- Review all three statements. P&L alone is not enough.

- Track actuals against plan. Budgeting isn’t optional once payroll and recurring contracts are involved.

Clean bookkeeping tells you what happened. Controller-level accounting tells you whether the numbers mean anything.

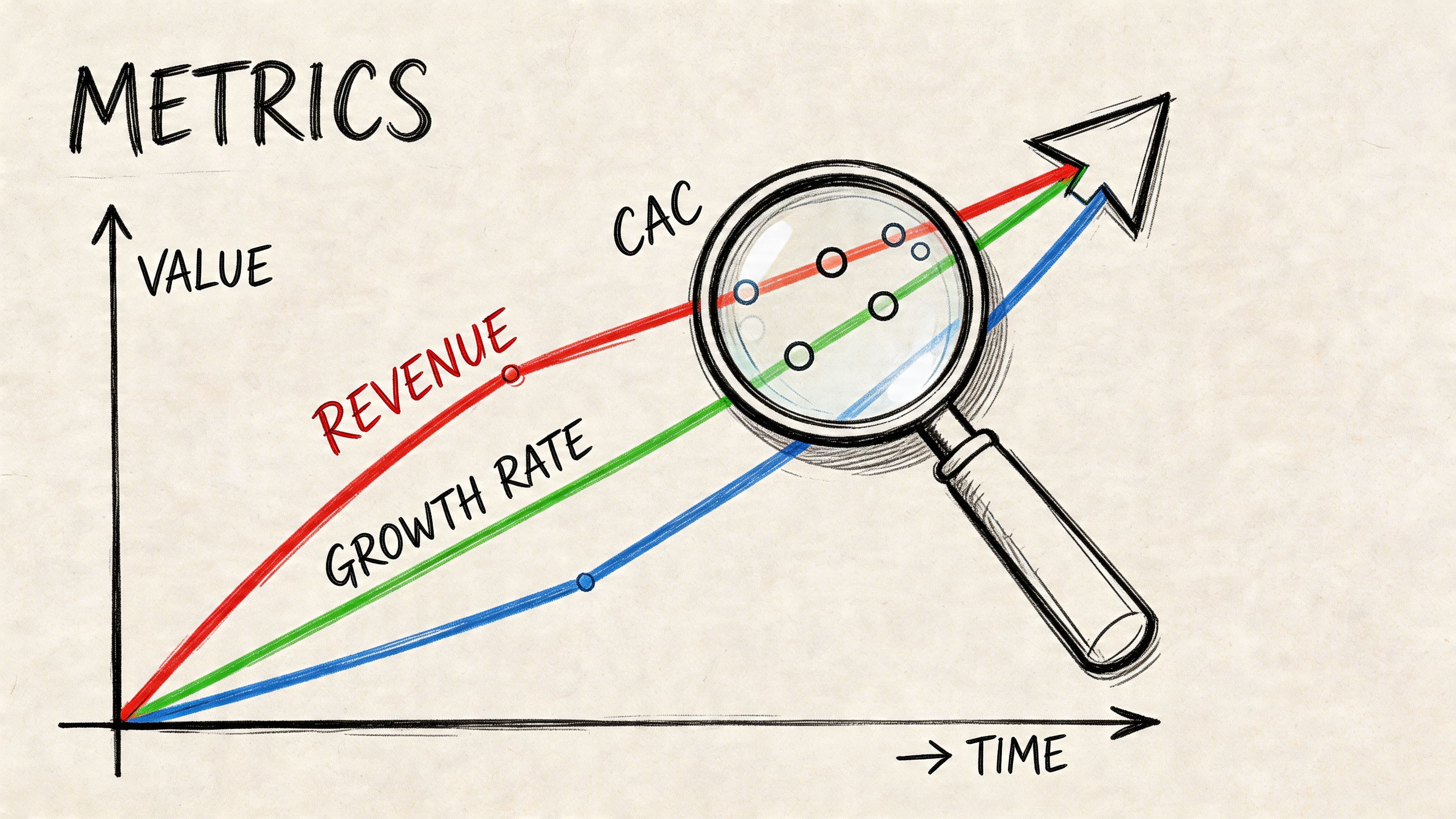

The Startup Metrics That Actually Matter

Most startup dashboards are cluttered with vanity metrics. Pageviews, signups, impressions, followers. Investors don’t fund noise. They fund businesses with credible economics.

For venture-backed startups, OpStart notes that investors scrutinize burn rate, financial statements, and other indicators of financial health. It also notes that gross margins typically vary by industry, with SaaS often at 80% to 90% and retail at 20% to 30% (OpStart on accounting for tech startups).

A worked example for ConnectSphere Inc.

Use one clean example and force your business through it.

Assume ConnectSphere Inc. is a SaaS company with:

- 200 customers on a $100 monthly subscription

- $20,000 in monthly subscription revenue

- $6,000 monthly hosting and support cost

- $12,000 monthly sales and marketing spend

- 12 new customers acquired in the month

- $35,000 total monthly cash spent

- $20,000 monthly cash collected from customers

Now calculate the metrics that matter.

MRR

Monthly Recurring Revenue = Paying customers × average monthly subscription price

200 × $100 = $20,000 MRR

This is your recurring revenue baseline. It’s not bookings. It’s not pipeline. It’s the subscription revenue you can reasonably expect monthly, before churn and expansion move it.

CAC

Customer Acquisition Cost = Sales and marketing spend ÷ new customers acquired

$12,000 ÷ 12 = $1,000 CAC

If that number rises while sales quality falls, you have a go-to-market problem, not a reporting problem.

Gross margin dollars and margin percent

Gross profit = Revenue - direct cost to deliver

$20,000 - $6,000 = $14,000 gross profit

Gross margin = Gross profit ÷ revenue

$14,000 ÷ $20,000 = 70% gross margin

That’s below the SaaS range OpStart says is common. If ConnectSphere really is a software business, management should inspect hosting efficiency, support load, and pricing discipline.

Burn rate is the metric founders avoid

OpStart breaks burn into gross burn and net burn. You should, too.

- Gross burn = total monthly cash spent

- Net burn = monthly cash spent - monthly revenue or cash inflow

Using the example:

- Gross burn = $35,000

- Net burn = $35,000 - $20,000 = $15,000

That tells a very different story than “we’re growing fast.” If you have weak margin and rising CAC, burn becomes the summary of every operational mistake.

Investors don’t just ask how fast you’re growing. They ask what it costs you to grow that way.

If you want a cleaner leadership view, a good starting point is a practical guide to financial dashboards with CEO KPIs.

What non-SaaS founders should track instead

Not every founder needs MRR. Agencies and professional services firms should care more about operational efficiency and cash conversion.

Watch these instead:

- Utilization: Are delivery staff spending time on client work or overhead?

- Gross margin by service line: Which offers create profit, and which ones just create busyness?

- Accounts receivable aging: If clients pay late, growth can still crush cash.

- Revenue concentration: One oversized client can distort the whole business.

For subscription companies, retention belongs on the dashboard, too. This primer on gross vs net retention metrics is useful if your team keeps mixing up customer stickiness with expansion revenue.

Here’s a simple leadership test. If your dashboard doesn’t help you decide hiring, pricing, and runway, it’s decoration.

Surviving ASC 606 Revenue Recognition in SaaS

ASC 606 confuses founders because they think payment equals revenue. It doesn’t.

For SaaS and subscription businesses, OpStart notes that ASC 606 requires tracking deferred revenue from upfront payments, and that this is a core part of accrual accounting because investors want a picture of financial health that isn’t distorted by cash timing (ASC 606 revenue recognition for startup founders).

The rule in plain English

You recognize revenue when you deliver the service, not when the cash arrives.

If a customer prepays for a year, you haven’t earned all of that revenue on day one. You owe service over time. Until you deliver it, part of that cash sits on your balance sheet as deferred revenue, which is a liability.

That liability matters because it changes how your business looks.

A simple SaaS example

A customer pays $12,000 in January for an annual subscription.

Under bad founder logic, you book $12,000 of January revenue.

Under ASC 606, you book:

- January cash received: $12,000

- January revenue recognized: $1,000

- Deferred revenue remaining after January: $11,000

Then you recognize $1,000 per month over the next 12 months as you deliver the subscription.

Here’s the difference:

| Method | January revenue | February revenue | Balance sheet impact |

|---|---|---|---|

| Cash basis thinking | $12,000 | $0 | No deferred revenue tracked |

| Accrual under ASC 606 | $1,000 | $1,000 | Deferred revenue recorded and reduced over time |

That’s why cash basis books mislead founders. January looks fantastic. The rest of the year looks soft. Neither view reflects reality.

Why investors care

Investors don’t want a bank statement dressed up as performance.

They want to know whether revenue is earned consistently, whether margins are real, and whether growth holds up after accounting cleanup. If your finance team has to restate revenue during diligence, trust drops immediately.

That problem gets worse in businesses with:

- Annual contracts

- Multi-year agreements

- Setup fees

- Bundled implementation and subscription services

- Discounts tied to term commitments

Each one creates timing questions. If you answer those questions with spreadsheet patches and memory, your reporting is fragile.

Founder test: If a customer prepays today and cancels halfway through the term, can your books show what was earned, what remains deferred, and what liability still exists? If not, your revenue process isn’t built.

What to do this month

You don’t need to become an accountant. You do need a repeatable workflow.

Use this checklist:

- List every contract type. Monthly, annual, setup, bundled, usage-based.

- Define when service is delivered. That drives recognition.

- Track deferred revenue on the balance sheet.

- Move to accrual reporting before your next serious fundraise.

- Review contracts with someone who understands startup revenue recognition.

Founders resist this because cash basis feels easier. It is easier. It’s also less truthful.

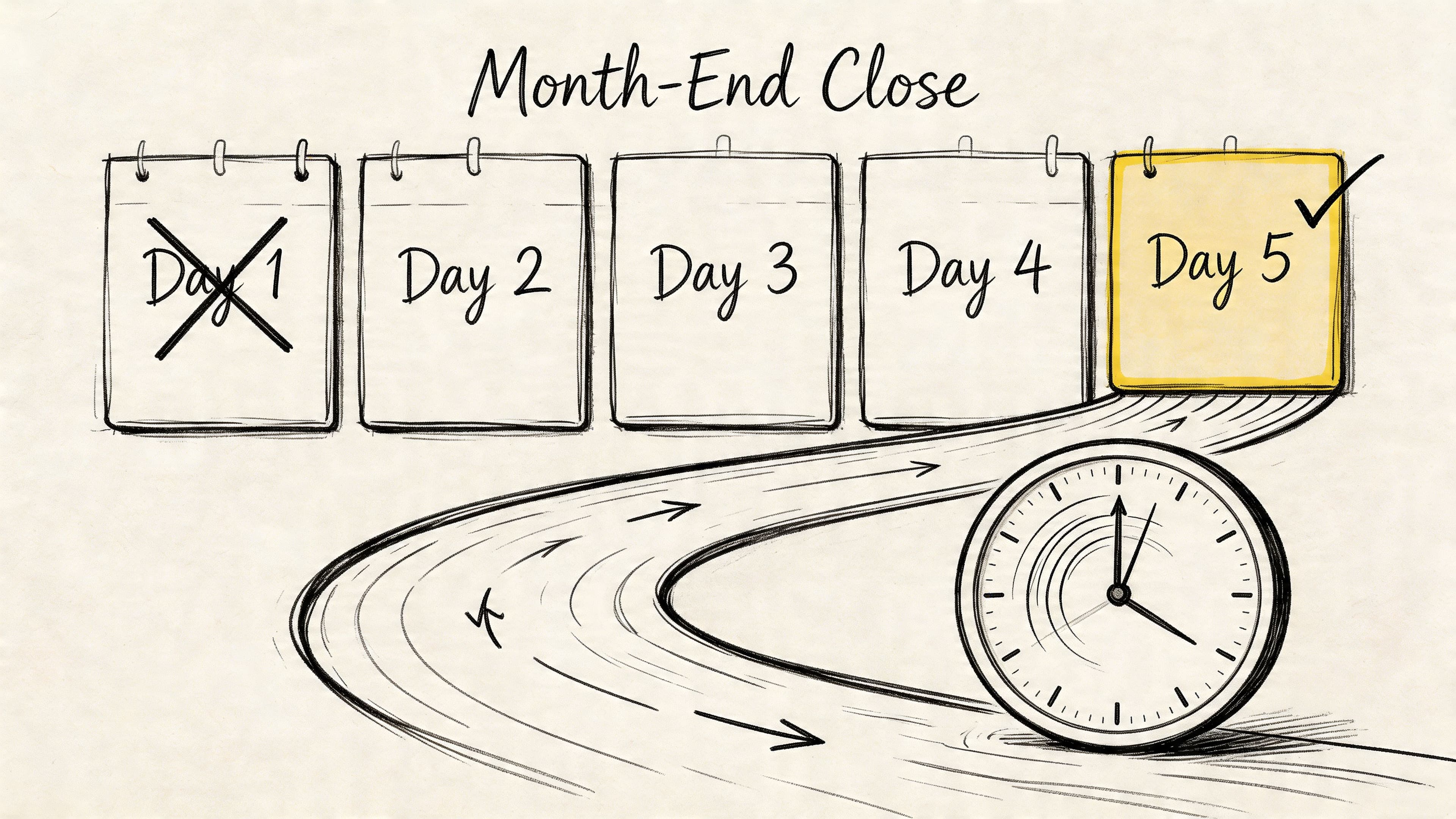

Your Guide to a Painless 5-Day Month-End Close

A slow close is a leadership problem disguised as an accounting problem.

If it takes you weeks to close the books, your decisions are always late. Hiring, pricing, spend control, collections, and forecast updates all get pushed onto stale numbers.

What a disciplined close looks like

A good close is boring. That’s the goal.

The team knows what gets done, in what order, by whom, and what support is needed to finish. No hunting for receipts on day four. No surprise bank adjustments on day seven. No last-minute revenue debates.

A useful reference for building that discipline is this guide to month-end close best practices.

Sample 5-Day Month-End Close Checklist

| Day | Task |

|---|---|

| Day 1 | Lock prior-month transactions, import bank feeds, collect missing documents, review payroll postings |

| Day 2 | Reconcile bank accounts and credit cards, review uncategorized transactions, post routine journal entries |

| Day 3 | Record accruals and prepaids, review accounts payable and accounts receivable, confirm revenue schedules |

| Day 4 | Finalize balance sheet reconciliations, prepare P&L, balance sheet, and cash flow statement, investigate variances |

| Day 5 | Management review, approve final adjustments, distribute monthly reporting package, update forecast assumptions |

Red flags that your close is broken

If any of these sound familiar, your process isn’t under control:

- You close whenever you get around to it. A close without deadlines turns into forensic accounting.

- Prior months keep changing. Frequent restatements mean your controls are weak.

- No one owns reconciliations. That guarantees balance sheet errors.

- You can’t explain variances quickly. If revenue or payroll moved, management should know why.

- Operational systems don’t tie to accounting. Stripe, payroll, and expenses shouldn’t live in separate truths.

This matters even more for e-commerce and marketplace businesses. If you sell through Amazon, finance teams often need to reconcile payout timing, fees, and reserve activity. This breakdown of Settlement Finance Transactions is a useful reference because those feeds regularly confuse otherwise solid close processes.

A fast close doesn’t mean rushing. It means the cleanup happened throughout the month instead of after it.

The habits that make five days realistic

You won’t get there with heroics. You get there with routine.

- Daily transaction discipline: Code and review transactions during the month, not at the end.

- Weekly cash review: Keep bank balances, outgoing payments, and collections current.

- Contract tracking: Revenue issues should never first appear during close.

- Balance sheet ownership: Every account needs an owner and support file.

- Management review cadence: Leadership should review the package on the same day every month.

Most founders think the P&L is the close. It isn’t. The close is a system that makes the P&L trustworthy.

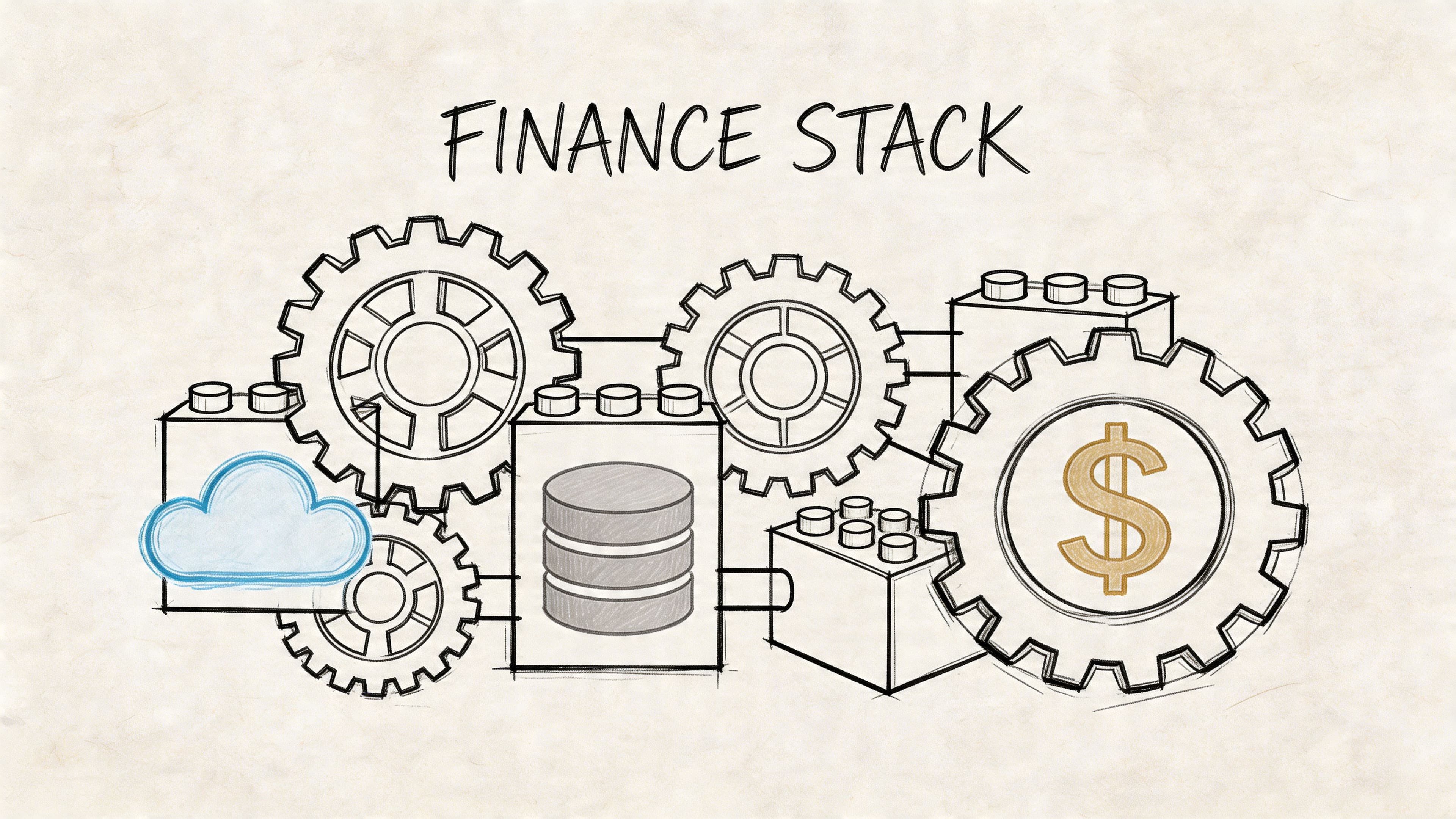

Building an Investor-Ready Finance and Tech Stack

Founders love to blame bad reporting on software. That is usually wrong. Early-stage finance problems come from accounting debt: disconnected systems, weak mapping, and no clear owner for the monthly output. The longer you wait to fix that, the more expensive cleanup gets during diligence, a board meeting, or a fundraise.

Grand View Research projects the U.S. accounting services market for startups to reach $39.09 billion by 2033, and reports that the bookkeeping segment accounted for 38.3% of market revenue in 2025, reflecting demand for cost-efficient expertise and cloud-based delivery models (Grand View Research on startup accounting services growth).

Build the stack around reporting, not apps

An investor-ready stack gives you clean monthly reporting without spreadsheet triage. For many startups between $500K and $20M in revenue, that means a simple architecture with tight rules around how data enters the ledger.

- General ledger: QuickBooks Online or Xero

- Billing and collections: Stripe or another billing platform tied to your contract terms

- Payroll: Gusto or a similar payroll system

- Expense management: Ramp or another spend platform with clear coding controls

- Reporting layer: A board package, KPI dashboard, or controller-built reporting file

- Document system: Signed contracts, cap table records, debt agreements, and close support stored in one place

The stack changes by business model. A SaaS company needs billing and deferred revenue support. An agency needs project, payroll, and margin visibility by client or service line. E-commerce and marketplace companies need payout, fees, reserves, and returns tied back to cash and revenue. If your tools do not reflect how the business makes money, your reporting will stay weak no matter how many subscriptions you buy.

What investor-ready means

“Investor-ready” is not a design choice. It is a standard.

You should be able to produce a clean package, fast:

- Profit and loss statement

- Balance sheet

- Cash flow statement

- Revenue support tied to contracts or orders

- Bank and credit card reconciliations

- Deferred revenue schedule, if applicable

- Cap table and equity support

- Monthly management reporting with variance explanations

Every report should tie out to the ledger and underlying support. If your team needs post-close journal entries, side spreadsheets no one trusts, or founder memory to explain the numbers, you are not investor-ready.

Upgrade points for the finance stack

Do not upgrade because a tool feels more professional. Upgrade when the cost of staying put is higher than the cost of better systems and oversight.

Common thresholds:

- DIY plus basic bookkeeping: Early stage, one entity, simple cash activity, low transaction volume

- Add a stronger close process and reporting owner: Recurring revenue, growing payroll, outside capital, or departmental budgeting

- Add an outsourced controller: Deferred revenue, multi-system integrations, board reporting, lender requests, or a close that slips past day 10

- Consider an ERP such as NetSuite: Multiple entities, international operations, consolidations, high transaction counts, or advanced revenue workflows

That middle stage is where startups waste the most money. They are too complex for founder-led finance, but not complex enough for a full in-house team. A good outsourced controller setup closes that gap by connecting systems, enforcing review, and producing reporting the business can use. If you are comparing providers, this guide to outsourced accounting services for growing companies is a useful starting point.

Software does not create financial maturity. Clear ownership, accurate data flows, and disciplined monthly reporting do. The software just makes a good process faster.

When to Stop DIY and Outsource Your Startup Accounting

DIY accounting has a short shelf life.

It works when the company is tiny, transactions are simple, and nobody outside the business relies on the numbers. Once you have recurring revenue, a team, meaningful payroll, outside capital, or lender scrutiny, founder-led accounting becomes an expensive use of executive time.

The decision triggers are operational, not emotional

You should stop doing it yourself when any of the following is true:

- Your monthly close drags on. You’re managing from stale numbers.

- Revenue timing gets complex. Annual contracts, retainers, deferred revenue, and client prepayments need stronger controls.

- You’re preparing for diligence, a loan, or an audit. Sloppy books always surface.

- You can’t answer basic financial questions fast. Margin by service line, cash obligations, and trend explanations should not require a week of cleanup.

- The founder is still the backstop. If every accounting question lands on your plate, the system hasn’t matured.

Choosing your finance solution

| Factor | DIY (Founder) | In-House Hire | Outsourced Firm (e.g., Jumpstart) |

|---|---|---|---|

| Cost structure | Lowest apparent cost, highest hidden executive time cost | Fixed salary and overhead | Recurring service fee tied to scope |

| Setup speed | Immediate, but inconsistent | Slower hiring and onboarding | Faster implementation if processes already exist |

| Skill coverage | Usually limited to basic bookkeeping | Depends on one person’s strengths | Broader coverage across bookkeeping, controller work, and finance support |

| Industry-specific knowledge | Usually weak | Variable | Often stronger if the firm focuses on your model |

| Close process discipline | Inconsistent | Can be strong with the right hire | Usually process-driven by design |

| Fundraising readiness | Weak unless founder has finance depth | Depends on hire quality | Stronger when the firm regularly supports diligence |

| Key risk | Errors, missed accruals, bad use of founder time | Key-person dependency | Requires clear ownership and communication rhythm |

| Best fit | Very early, low-complexity operations | Businesses ready to build internal finance | Companies that need better reporting before building a full team |

Common objections founders use to delay the decision

“I’m not big enough yet.”

If your books affect hiring, pricing, taxes, or fundraising, you’re big enough.

“My CPA handles it.”

Tax preparation is not the same as monthly accounting. Most CPAs are not running your close, managing deferred revenue, or building operational reporting.

“Software can automate most of this.”

Software helps. It doesn’t decide accruals, review contract logic, explain margin shifts, or catch broken workflows.

“I’ll hire a controller later.”

Later usually means during pressure. That’s the worst time to build finance infrastructure.

Operator insight: The right time to upgrade finance is before the pain becomes visible to investors, lenders, or the IRS.

What I recommend for a $500K to $20M business

Keep the roadmap simple.

- Get the books clean. Reconcile everything. Fix categorization. lock down the chart of accounts.

- Move to a real monthly close. The reporting package should arrive on a dependable schedule.

- Adopt accrual accounting where complexity demands it.

- Install dashboards that match your business model. SaaS, agency, and services firms need different views.

- Outsource before you build in-house. It’s usually the fastest way to get controller discipline without making a full-time senior hire.

If you’re evaluating providers, this breakdown of outsourced accounting services helps clarify what to look for and where firms differ.

The founders who wait the longest usually say the same thing after cleanup starts: “I wish we’d done this earlier.”

If your books are late, your revenue reporting is messy, or your team still treats finance like cleanup work, it’s time to fix it. Jumpstart Partners works with growing startups and service businesses that need controller-level reporting, a dependable close process, and investor-ready financials without building a full in-house team first.