Financial Operations

Bookkeeping for Construction Companies: A Founder's Guide

Master bookkeeping for construction companies. This guide covers job costing, progress billing, WIP reports, and software to protect your cash flow and margins.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readGeneric bookkeeping can make a construction company look healthy while the cash account is telling a very different story. That disconnect is expensive. It leads to thin bids that looked profitable on paper, missed billing opportunities, and jobs that consume working capital faster than the office realizes.

That's why bookkeeping for construction companies is a separate discipline, not a minor variation on standard bookkeeping. Construction accounting has long been structured around the job, not just the company, with separate tracking for accounts payable, accounts receivable, and job costs, plus staged billing, retainage, and contract-based revenue recognition under ASC 606's five-step model of identifying the contract, identifying performance obligations, determining transaction price, allocating that price, and recognizing revenue as obligations are satisfied, as noted in Deltek's construction bookkeeping guide.

If you run a contractor business, your books need to answer three questions every month. Which jobs are making money. Which jobs are consuming cash. Which numbers can support a bank, surety, or investor conversation without a scramble.

Build Your Foundation with Job Costing and a Specialized Chart of Accounts

A standard chart of accounts answers whether the company made money. Construction needs a tighter answer. Did this specific job make money, and why?

That's the line many growing contractors miss. They keep a broad expense structure, code labor to payroll expense, put materials in supplies, and book subcontractors under a generic outside services line. The P&L may still tie out. But it won't tell you which estimate was wrong, which foreman is overrunning labor, or which project manager is letting change-order work hit the job before paperwork catches up.

Why a generic chart of accounts fails

Construction bookkeeping works when every transaction lands in two places at once. It belongs to an account category, and it belongs to a job with a cost code or phase.

Industry guidance is clear on the operating model. A strong workflow starts with project-level job costing, then breaks the job into phases, task lists, and three buckets: labor, materials, and overhead. It also recommends separate journals or tracking streams for accounts payable, accounts receivable, and job costs, because profitability gets distorted fast when labor hours, subcontractor bills, or material purchases sit in broad overhead accounts, as explained in Hubstaff's construction bookkeeping overview.

Practical rule: If your bookkeeper can't tell you gross margin by job without exporting data into a spreadsheet and fixing categories by hand, your chart of accounts is already failing you.

A better setup starts with a lean general ledger and pushes the detail into job costing. Your chart of accounts should still separate direct costs from overhead, but your operational reporting should answer job-level questions through cost codes, classes, projects, or a dedicated job-cost module.

For a plain-English walkthrough of how account structures work, this chart of accounts guide is useful background before you rebuild yours.

What to track at the job level

At minimum, each active project should capture:

- Direct labor: Wages tied to field work, plus payroll taxes, workers' compensation, and overtime.

- Materials: Direct materials such as concrete or steel, plus indirect items tied to job execution like delivery, fasteners, and expected waste.

- Subcontractors: Separate from internal labor so you can see scope buyout performance.

- Equipment and rentals: Especially when a project is equipment-heavy.

- Job-specific indirects: Permits, dumpsters, temp utilities, small tools, and mobilization.

- Company overhead: Rent, office salaries, utilities, travel, professional fees, and marketing. These should not get mixed into direct job costs just to make one job look better.

Standard vs construction chart of accounts

| Account Type | Standard COGS | Construction Job Costs (Direct Costs) |

|---|---|---|

| Labor | Payroll expense | Field labor by job and phase, with taxes, workers' comp, and overtime included |

| Materials | Supplies or materials expense | Materials by job and phase, including delivery and waste |

| Subcontractors | Outside services | Subcontractor costs by vendor, job, and scope |

| Equipment | Equipment expense | Job equipment usage, rentals, repairs tied to project execution |

| Indirect job costs | Often buried in overhead | Permits, site supervision, temp facilities, disposal, inspections |

| Overhead | General admin expense | Kept separate from direct job costs so bid margins stay honest |

What works and what doesn't

What works is a system where the estimator, project manager, payroll process, AP workflow, and bookkeeping all use the same cost structure. That gives you clean history for future bids.

What doesn't work is trying to “clean it up later.” Later usually means after billing has gone out, payroll has been processed, and the job has drifted far enough off estimate that the only remaining option is explaining the miss.

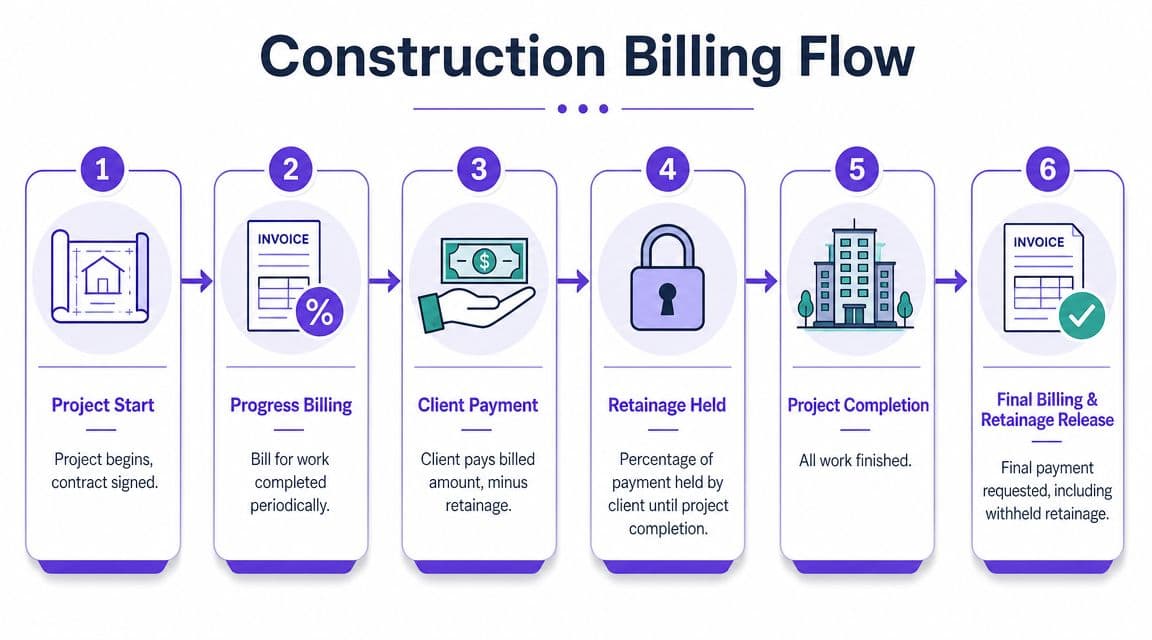

Manage Cash Flow with Progress Billing and Retainage

Construction firms don't fail because revenue is absent. They fail because cash arrives later than costs leave. Progress billing and retainage sit at the center of that problem.

If you bill like a normal service business, you'll finance the job for your client. Large and mid-sized projects need a billing discipline built around the contract. That usually means a Schedule of Values, periodic Applications for Payment, approved change orders, and a separate retainage receivable balance that never gets mistaken for spendable cash.

The billing math has to be visible

Construction accounting guidance distinguishes among cash basis, accrual, percentage of completion, and completed contract methods. It also emphasizes that retainage is commonly 5% to 10% of contract value and should be recorded in a retainage receivable account rather than as immediate cash, with continuous reconciliation of project cost accumulation, billing, and retainage for accurate cash forecasting, as described in Premier's guide to construction accounting methods.

Here's a simple worked example using the billing structure many contractors deal with.

Contract value: $500,000

Retainage: 10%

Current completion: 25%

Step through the math:

- Earned revenue to date = $500,000 × 25% = $125,000

- Retainage withheld = $125,000 × 10% = $12,500

- Current billable amount before prior billings adjustment = $125,000

- Cash expected from this billing = $125,000 - $12,500 = $112,500

Your books should show two realities at once:

- You've earned $125,000 based on progress.

- You should only expect $112,500 in current payment.

- The remaining $12,500 belongs in retainage receivable, not in cash and not hidden inside standard trade receivables.

That gap matters. Payroll, subs, and suppliers don't wait for retainage release.

How to keep billing from breaking cash flow

A reliable operating routine looks like this:

- Build a Schedule of Values early: Break contract value into logical billing lines that match the field reality.

- Tie billing to actual progress: Don't let billing percentages drift away from superintendent or PM input.

- Track retainage separately: Keep it visible by customer and by job.

- Log change orders immediately: Approved, pending, and disputed change orders need distinct statuses.

- Reconcile weekly on active jobs: Month-end is too late if your pay apps are already out the door.

For teams tightening their process, these account payable automation insights are helpful because the billing side only works when vendor approvals, invoice capture, and payment timing are controlled on the disbursement side too.

A stronger billing cadence also improves forecasting. If you need a practical framework for that, this guide on improving cash flow is a good companion to your monthly project reviews.

A short visual explanation can help align field and finance teams on the same workflow:

Retainage isn't missing money. It's earned money with a delayed collection date. Book it that way, forecast it that way, and manage the job as if that cash is unavailable until release.

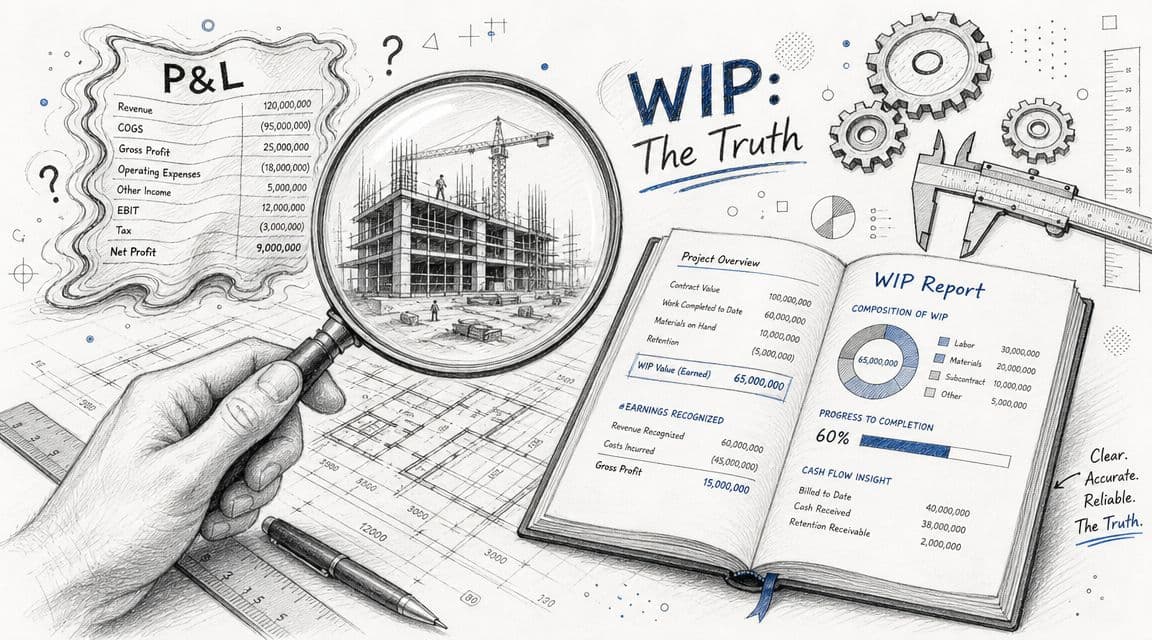

Unlock True Profitability with WIP Reporting

Your income statement can flatter a job that is already going sideways. A work-in-progress report removes that illusion by forcing job costs, estimated costs to complete, earned revenue, and billings onto the same page.

This is the report owners avoid when they already suspect a problem. That's exactly when they need it most.

Why the WIP report matters more than the P&L

Construction bookkeeping has to treat retainage, change orders, and WIP as one revenue-recognition and cash-flow problem. Better WIP controls improve cash visibility and reduce disputes because they show when revenue is earned versus when cash arrives, as explained in Brecken Business Solutions' discussion of construction bookkeeping differences.

A plain P&L by itself doesn't capture that timing well enough. A WIP schedule does. It shows:

| WIP element | What it tells you | Why it matters |

|---|---|---|

| Contract value | Original contract plus approved change orders | Sets the revenue ceiling for the job |

| Costs to date | What you've actually spent | Shows current execution reality |

| Estimated cost to complete | What remains | Reveals margin compression early |

| Percentage complete | Cost-to-cost progress measure | Supports revenue recognition |

| Revenue earned to date | What should be recognized | Anchors the job to economics, not billing speed |

| Billings to date | What you've invoiced | Exposes over- and under-billings |

If you need a refresher on how gross profit is calculated before layering in WIP analysis, this explanation of the gross profit formula for businesses is a useful baseline.

A simple WIP example

Assume a job has these numbers:

- Contract value: $500,000

- Estimated total cost at start: $400,000

- Costs incurred to date: $220,000

- Revised estimated total cost: $460,000

- Billings to date: $300,000

Now calculate the current position:

- Percent complete = $220,000 ÷ $460,000 = 47.8%

- Revenue earned to date = $500,000 × 47.8% = $239,000

- Overbilling = $300,000 billed - $239,000 earned = $61,000

On the surface, billing looks strong. Cash may even look decent for the month. But the WIP report shows something more important. The estimated total cost has moved from $400,000 to $460,000, which means the expected gross profit on the job has dropped from $100,000 to $40,000.

That is the kind of bad news a normal monthly P&L can hide.

What to watch every month

Owner's test: Ask your team which three jobs changed expected margin this month, and why. If the answer starts with “we haven't updated the WIP yet,” you're operating blind.

A useful WIP review process includes:

- Under-billings: These sit as an asset, but they often mean you've performed work you haven't converted into invoices.

- Over-billings: These sit as a liability. They can support short-term cash, but they are not profit.

- Margin fade: If estimated profit keeps shrinking as the job progresses, estimating or execution has a problem.

- Pending change orders: These should be visible so PMs don't treat unapproved revenue as settled fact.

For service firms that want a simpler analogy, this work-in-progress accounting guide explains the same core idea in another project-based environment. The mechanics differ, but the discipline is similar. You need to see unfinished work accurately.

Handle Payroll Subcontractors and Compliance

Labor is where construction bookkeeping stops being clerical and becomes operational. If labor isn't coded correctly, job costing fails. If subcontractor records are incomplete, compliance risk rises fast.

Burdened labor is the real labor cost

Industry guidance for construction job costing treats labor as more than wage rates. It includes taxes, workers' compensation, and overtime inside the labor bucket used for job costing, not as an afterthought in overhead. That distinction matters because bids based on base wages alone are usually too optimistic.

A simple example makes the point.

If an employee earns $30,000 in wages on a specific job during a reporting period, and the related payroll taxes, workers' compensation, and overtime tied to that same labor total $6,000, your direct labor cost for job-costing purposes is $36,000, not $30,000.

That difference changes estimated margin. It also changes what you should charge on future work.

Subcontractor controls that are not optional

Before a subcontractor starts work, your file should include:

- Signed agreement: Scope, billing terms, indemnification language, and change-order procedure.

- W-9 on file: Needed for vendor setup and year-end reporting.

- Certificate of Insurance: Current and matched to contract requirements.

- Licensing check: Especially when the trade or jurisdiction requires it.

- Compliance documentation for public work: If certified payroll applies, get the process set before labor hits the site. Teams dealing with public contracts can use this practical overview to get certified payroll help from Helpside.

Red flags you should act on immediately

| Warning sign | What it usually means |

|---|---|

| Field hours posted late | Labor is being estimated instead of measured |

| Subs billing without approved change documentation | Margin erosion is coming |

| COIs expired mid-job | You've accepted uninsured risk |

| One vendor paid as both employee and subcontractor | Classification and tax issues are likely |

| Payroll booked to overhead first, jobs later | Job margins are already distorted |

Don't let AP “figure out the coding later.” In construction, late coding is how accurate labor cost turns into fiction.

The practical trade-off is simple. Tighter compliance takes more setup work before the job starts. But weak setup produces surprise cost, payment disputes, and audit trouble after the work is already in place.

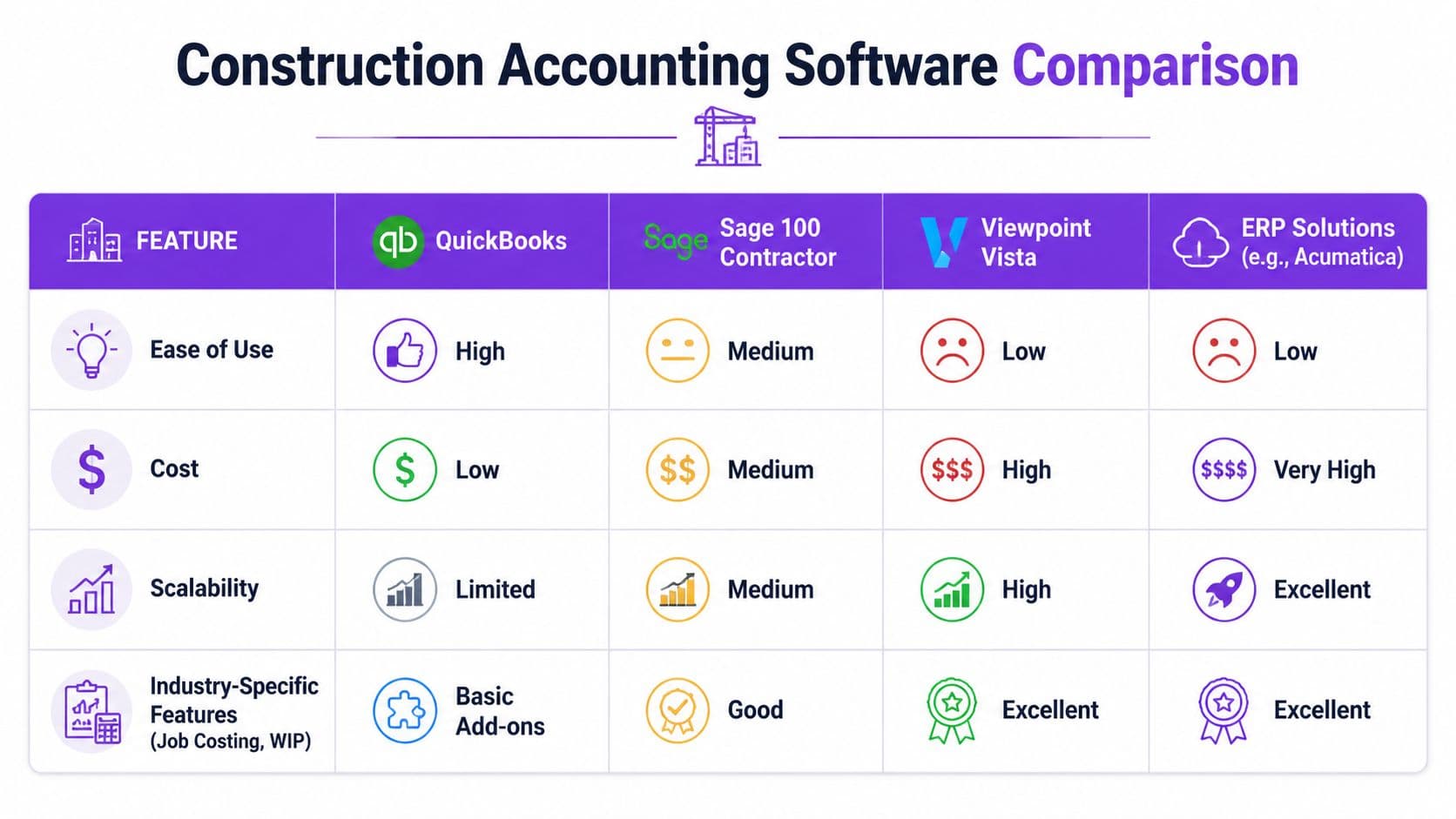

Choose the Right Software and Key Financial Reports

Software doesn't solve weak processes, but bad software absolutely makes them worse. Construction companies need systems that can handle project tracking, billing complexity, cost coding, and reporting without forcing the finance team to maintain a shadow spreadsheet universe.

Many owners start with standard QuickBooks because it's familiar. That can work for a small contractor with simple jobs. It breaks down once you need dependable WIP reporting, tighter approval routing, or multi-entity and multi-jurisdiction control.

What software should do for you

Recent practice is shifting away from bookkeeping as simple categorization and toward automation that prevents duplicate payments, speeds approvals, and keeps daily project costs current. For companies operating across multiple projects or jurisdictions, that shift is increasingly tied to tax tracking and 1099 reporting, as noted in J.M. Co.’s construction bookkeeping article.

That means your stack should support:

- Job and phase tracking

- Progress billing and retainage handling

- Approval workflows for AP

- Payroll integration

- Document attachment at the transaction level

- Reporting by job, PM, and division

- Tax and contractor reporting support

A practical comparison

| Platform | Best fit | Strengths | Limits |

|---|---|---|---|

| QuickBooks | Smaller contractors with lighter complexity | Familiar interface, broad accountant support, low barrier to entry | Limited native construction depth, reporting often needs workarounds |

| Sage 100 Contractor | Growing firms that need stronger job cost structure | Built for contractors, solid operational accounting | More setup discipline required |

| Viewpoint Vista | Larger firms with complex reporting needs | Deep construction functionality, strong project accounting | Heavier implementation and training burden |

| ERP tools such as Acumatica or NetSuite | Multi-entity or highly scaled firms | Broad control across finance and operations | Higher cost, longer implementation, more internal ownership needed |

The choice depends less on brand name than on operational maturity. If your field team won't code time consistently, a larger system won't save you. If your controller is exporting data into spreadsheets every month to produce lender-ready reports, you've likely outgrown the current setup.

For a broader framework on evaluating systems as complexity grows, this guide on choosing accounting software for a growing business is a practical reference.

The three reports you must review monthly

Don't judge software by dashboard aesthetics. Judge it by whether you can review these three reports without manual repair work:

-

WIP schedule

Look for margin fade, stale estimates, and unexplained under-billings. -

P&L by job

Check whether direct costs are landing in the right jobs and whether closed jobs still show activity. -

Job cost detail

Review exceptions. Large miscoded invoices, labor posted to the wrong phase, and subcontractor costs without supporting commitments stand out here.

One option in this broader category is Jumpstart Partners, which provides outsourced controller and bookkeeping support across platforms such as QuickBooks, Xero, and NetSuite for growing businesses that need structured reporting and close support. For construction firms, the relevant question isn't whether a provider can “do bookkeeping.” It's whether they can produce job-cost, WIP, and cash-flow reporting that management can trust.

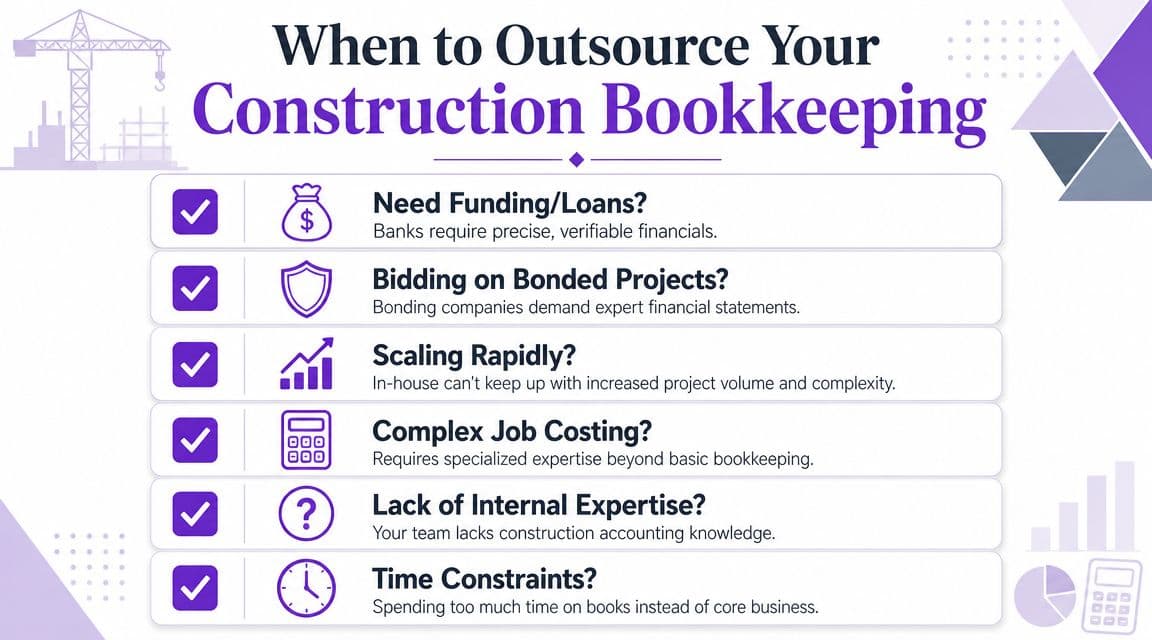

Know When to Outsource Your Construction Bookkeeping

There's a point where owner-led bookkeeping becomes a growth constraint. It usually shows up before the owner admits it. Bids feel less certain. Cash swings become harder to explain. The bank asks for cleaner statements. The surety asks for schedules your team has never produced consistently.

That's when specialized support stops being a convenience and becomes operating infrastructure.

The clearest trigger points

You should seriously consider outsourced construction bookkeeping or controller support if any of these are true:

- You need lender or surety-ready reporting: Basic monthly bookkeeping isn't enough.

- You're managing several active jobs at once: Volume creates coding drift and billing delays.

- Your CEO or owner still estimates job profitability from instinct: The reporting layer isn't doing its job.

- Change orders, retainage, and WIP don't reconcile cleanly: Financial statements are losing credibility.

- Month-end close turns into forensic work: That usually means the daily workflow is weak.

According to the Construction Financial Management Association, construction companies with dedicated financial management, whether in-house or outsourced, report 25% higher net profit margins on average than those relying on generic bookkeeping practices, primarily due to improved bidding accuracy and project cost controls.

Specialized financial management pays for itself when it changes how you bid, bill, and correct job issues before they reach the income statement.

What outsourcing should actually deliver

A solid outsourced partner should give you more than reconciled books. It should provide:

- Job-cost discipline: Transactions coded correctly the first time

- Billing support: Progress billing, retainage tracking, and change-order visibility

- Monthly WIP reporting: With management review, not just report generation

- Cash forecasting: Built around collections timing and project commitments

- External readiness: Financials that hold up in bank, investor, and surety conversations

If you're comparing providers, this roundup of outsourced accounting services is a useful place to start.

The main objection I hear is cost. The better question is cost compared to what. Compared to a bad bid. Compared to a delayed draw. Compared to discovering three months late that a job you thought was profitable was consuming cash and margin the entire time.

If your construction company has outgrown generic bookkeeping and you need clearer job-cost reporting, WIP visibility, and stronger cash forecasting, Jumpstart Partners can help you build the financial structure behind better bids and fewer surprises. A good next step is a review of your chart of accounts, billing workflow, and monthly reports to see where job profitability is getting obscured.