Financial Operations

The Financial Close Process a 5-Day Plan for SaaS & Agencies

Master the financial close process with our 5-day plan. This guide helps SaaS and agency founders achieve investor-ready financials, fast. Learn best practices.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readIf your books take most of the month to close, you're not running finance. You're reacting to it. Businesses using manual, spreadsheet-heavy processes average 8.2 days to close, while 58% finish in six days or less, according to InScope's overview of the financial close process. That gap matters because every extra day delays decisions on pricing, hiring, cash use, and profitability.

For a SaaS company or agency, the problem isn't just slow accounting. It's stale management data. When revenue is partially recognized, payroll isn't accrued, and payment processor activity is still unreconciled, your P&L tells a distorted story. You end up managing off bank balance and instinct instead of verified numbers.

A disciplined financial close process fixes that. What's more, a 5-day close is realistic for growth-stage businesses if you stop treating month-end like a one-time event and start running continuous accounting throughout the month.

Table of Contents

- Why Your Month-End Scramble Is Costing You Growth

- Unpacking the Financial Close Process

- The Three Stages Pre-Close Close and Post-Close

- Your 5-Day Month-End Close Roadmap

- KPIs and Best Practices for an Elite Close

- Common Bottlenecks and How to Fix Them

- Achieve Audit and Investor Readiness

Why Your Month-End Scramble Is Costing You Growth

A slow close creates a management blind spot. If your team is still cleaning up last month in the second week of this month, you are pricing, hiring, and spending with stale numbers.

That hurts growth faster than founders expect. You miss margin problems until they are expensive. You mistake timing noise for real cash performance. You walk into board or investor meetings with numbers that still need caveats.

Here is the practical consequence:

- Pricing decisions stall: You cannot see gross margin by client, project, or product line soon enough to fix weak work.

- Cash flow gets misread: A strong bank balance can mask deferred revenue, unpaid bills, missing accruals, or payroll liabilities.

- Forecasts lose value: If the books are not closed early in the month, every forecast starts from outdated assumptions.

- Leadership time gets wasted: Your operators spend days chasing receipts, approvals, and spreadsheet versions instead of improving delivery and sales.

Practical rule: If you are using last month's numbers to run this month's business after the first week, finance is late.

For SaaS and service businesses, the cost is even higher. These models depend on timing accuracy. Revenue recognition, deferred revenue, accrued expenses, contractor costs, and utilization all move profit more than founders think. If those entries are handled in a rush, your P&L stops being a decision tool and turns into a rough draft.

The fix is not a longer month-end checklist. The fix is a 5-day close built on continuous accounting. Post recurring entries during the month. Reconcile high-risk accounts before month-end. Standardize approvals. Keep the general ledger structure and purpose clean enough that your team can review exceptions instead of rebuilding the books from scratch.

I push automation early because repetitive finance work should never consume senior attention. If you're evaluating where automation pays off first, this CFO's guide to automation ROI is a useful framework for prioritizing high-friction workflows like AP, approvals, and recurring transaction handling.

Running the business from your bank balance is a founder mistake. Cash shows liquidity. It does not show whether revenue was earned in the right period, whether delivery was profitable, or whether liabilities are understated. A disciplined close gives you that answer fast, which is what protects cash flow and makes the business credible to lenders, buyers, and investors.

Unpacking the Financial Close Process

The financial close process is the system that turns messy transaction activity into numbers you can rely on. It is not bookkeeping cleanup. It is the operating rhythm that validates your performance.

According to NetSuite's overview of the close process, the modern financial close is a structured process of recording, reconciling, and finalizing all financial activity for a period. It evolved from a basic bookkeeping wrap-up into a formal cadence that supports compliance, audits, and decision-making in more complex businesses.

For a founder, the simplest way to think about it is this: your accounting system is the ship's log, and the close is when your team verifies that every entry matches reality before anyone uses it to steer.

What the close is supposed to accomplish

A good financial close process does three jobs at once:

| Objective | What it means in plain English | Why you should care |

|---|---|---|

| Accuracy | Revenue, expenses, assets, and liabilities are recorded in the right period | You stop making margin and cash decisions off bad data |

| Timeliness | The numbers are ready while they still matter | Leadership can act on current conditions, not old ones |

| Compliance | Documentation and reconciliations support the final statements | Investors, lenders, and auditors see a controlled business |

Most growth-stage companies break here because the business outgrows ad hoc accounting before leadership admits it. SaaS adds deferred revenue, renewals, usage billing, and commission timing. Agencies and professional services firms add project-based revenue, work in progress, retainers, contractor accruals, and client reimbursement issues. Those aren't edge cases. They're normal operating complexity.

Why ad hoc finance stops working

Once you're beyond founder-led bookkeeping, you need a real ledger discipline. If you need a refresher on how that foundation works, this explanation of what a general ledger is is worth reviewing.

A close process with no documented ownership is just a recurring fire drill.

The close also tends to follow a standardized sequence with roughly ten core activities, including recording key transactions, reconciling accounts, reviewing fixed assets and inventory where relevant, preparing statements, and locking the books for the next period, as outlined in the earlier NetSuite reference. The point isn't the exact count. The point is that mature finance teams don't wing this.

They use checklists, approvals, reconciliations, and cutoff rules because growth punishes improvisation.

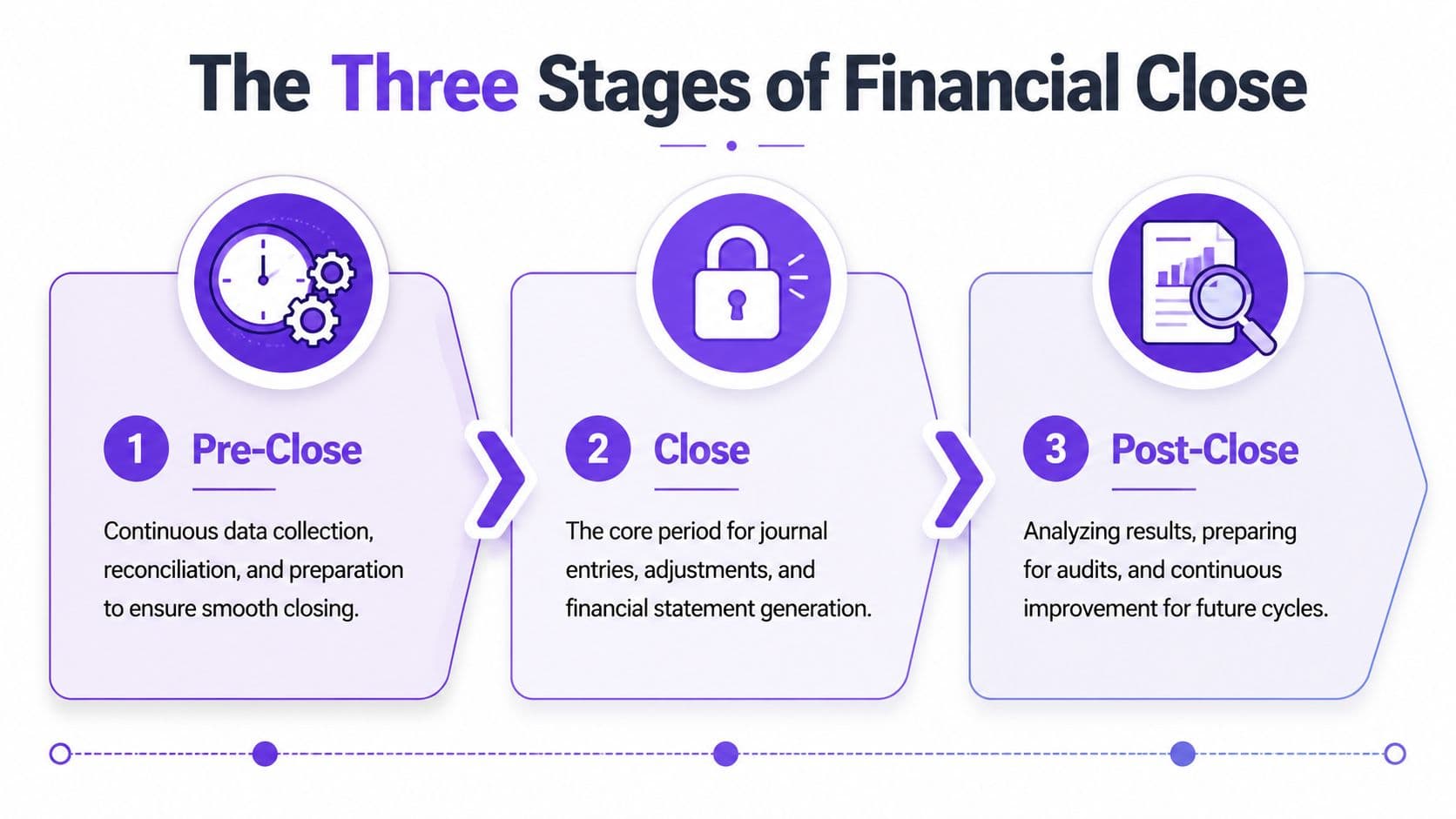

The Three Stages Pre-Close Close and Post-Close

The cleanest close process has three parts. Most founder-led businesses only focus on the middle one. That's why month-end feels chaotic.

Pre-close prevents surprises

Pre-close is the work you do before the period ends so month-end doesn't become an excavation project.

For SaaS and service businesses, that usually includes:

- Daily or weekly cash review: Match bank activity, card activity, and payment processor deposits.

- Invoice hygiene: Confirm customer invoices and vendor bills are entered promptly.

- Recurring entries prep: Queue standard items like payroll accruals, software subscriptions, and amortization.

- Revenue support review: Make sure contracts, scopes, and delivery status are accessible before close starts.

- Open item cleanup: Chase missing receipts, reimbursement support, and uncategorized transactions before cutoff.

Lean teams win by distributing work across the month instead of piling it into three painful days.

The close is where you lock accuracy

The actual close is the period when you stop transaction drift, reconcile balances, and finalize the books. The order matters.

According to OneStream's guidance on close sequencing, operational subledgers such as AR, AP, and payroll must be closed first because downstream consolidation quality depends on upstream ledger completeness. If those ledgers are still changing, the general ledger becomes a moving target and errors multiply.

That means you do not start with the P&L review. You start with source systems.

A simple sequence looks like this:

-

Close subledgers first

AR, AP, payroll, and any operational systems feeding the books must stop changing for the period. -

Reconcile cash and clearing accounts

Bank accounts, credit cards, Stripe or other processor clearing accounts, and payroll clearing need to tie out. -

Post adjusting entries

Accruals, prepaid amortization, deferred revenue movement, and corrections happen here. -

Review balance sheet support

Every material balance should tie to a report, schedule, or external statement. -

Generate draft financials

Then leadership reviews the income statement, balance sheet, and cash flow statement.

If cash reconciliation is still moving, your P&L review is premature. If AR is incomplete, revenue analysis is unreliable. If payroll hasn't posted, margins are fake.

For teams that still struggle with cash tie-outs, a stronger bank reconciliation process usually removes more close friction than any fancy dashboard.

Post-close turns numbers into decisions

Post-close is where finance becomes useful to leadership instead of merely compliant.

Use the final numbers to answer business questions such as:

- Which customers, service lines, or channels produced margin?

- Where did collections lag?

- Which expenses spiked and need action this month?

- What changed in working capital?

The close is not finished when the entries are posted. It's finished when leadership can use the numbers confidently.

Post-close should also include documentation cleanup, lessons learned, and updates to the close checklist so the next cycle gets easier instead of repeating the same failures.

Your 5-Day Month-End Close Roadmap

A 5-day close isn't aggressive. It's disciplined. The key is to stop cramming routine accounting into the first week of the next month.

Sample 5-day month-end close workflow

| Day | Focus Area | Key Tasks |

|---|---|---|

| Day 1 | Subledgers and cash | Lock AR, AP, payroll, and billing activity for the period. Reconcile bank accounts, credit cards, and payment processor clearing accounts. Confirm invoice and bill cutoff. |

| Day 2 | Balance sheet reconciliations | Reconcile key balance sheet accounts including receivables, payables, deferred revenue, prepaid expenses, accrued liabilities, and payroll-related balances. |

| Day 3 | Accruals and adjustments | Post recurring and non-recurring accruals. Review revenue recognition for in-progress work or subscription schedules. Record prepaid amortization and corrections. |

| Day 4 | Financial statement review | Generate draft P&L, balance sheet, and cash flow. Review gross margin, operating expenses, unusual variances, and entity-level consistency. |

| Day 5 | Finalization and reporting | Approve the package, lock the books, distribute management reporting, and note issues that need process fixes before next month. |

This workflow assumes you've already done continuous accounting during the month. If Day 1 begins with “find missing invoices” or “figure out Stripe,” you're already behind.

Worked example for accrued revenue

Here's a simple real-world example for a service business.

You signed a $30,000 project that runs across two months. By month-end, the work is 50% complete. You haven't billed the final amount yet, but under accrual accounting, you need the financials to reflect the work already performed.

The calculation is straightforward:

- Total project value = $30,000

- Percentage complete at month-end = 50%

- Revenue to recognize this month = $15,000

Journal entry at month-end:

| Account | Debit | Credit |

|---|---|---|

| Accrued revenue | 15,000 | |

| Service revenue | 15,000 |

Why this matters:

- If you skip the entry, this month's revenue is understated.

- If you book the full amount too early, this month's revenue is overstated.

- If you wait until invoicing, your P&L follows billing timing instead of delivery reality.

For SaaS, the same logic applies differently. If an annual contract is billed upfront, cash may arrive now, but revenue is recognized over the service period. For agencies and professional services firms, the issue is often the opposite: work gets delivered before billing catches up.

What founders should personally review on Day 4

You don't need to inspect every journal entry. You do need to review the parts that affect decisions.

Focus on:

- Revenue quality: Does recognized revenue match delivered work or subscription service periods?

- Gross margin: Did contractor costs, payroll allocation, or software COGS land correctly?

- Cash conversion signals: Did AR increase faster than revenue? Did AP or accrued expenses spike?

- Outliers: Large new expenses, negative margins by client, or unusual balance sheet movements need explanation.

If you need a stronger baseline process, use a formal month-end close checklist template and assign owners to every line item. Ownership is what turns a checklist into a management system.

A 5-day close works best when responsibility is explicit:

- Controller or finance lead: Owns the calendar, reviews reconciliations, and signs off on the package.

- Bookkeeper or staff accountant: Handles daily cash, AP, AR, and standard reconciliations.

- Founder or department lead: Confirms operational facts finance cannot guess, like project completion status or contract changes.

Without that operating discipline, the close always drifts back into a monthly scramble.

KPIs and Best Practices for an Elite Close

A close that drags past the first week of the month is a management failure, not a finance inconvenience. If you do not have current numbers, you cannot make current decisions on hiring, pricing, cash preservation, or sales efficiency.

Key Performance Indicators for the Close

Track four metrics. Ignore vanity measures.

| KPI | What good looks like | What a bad result means |

|---|---|---|

| Days to close | Final financials are ready in 5 business days or less for a SaaS or services business | Leaders are making decisions with stale numbers |

| Post-close adjusting entries | Few corrections after the books are issued | Revenue, expenses, or accruals were missed before review |

| Accounts reconciled before final review | Cash, AR, AP, payroll, debt, and deferred revenue are tied out before the package is released | The team is still investigating basic balances too late in the process |

| Variance resolution speed | Large swings are explained quickly with clear owner comments | Finance is producing statements, not decision support |

A 5-day close is the benchmark that matters here because this guide is built for SaaS and service businesses that need speed without losing accuracy. If you are closing in 8 to 10 business days, the problem is rarely effort. It is process design.

Operator's view: Fast and wrong is useless. Accurate and late is expensive.

The best finance teams also track these KPIs by entity, business unit, or workflow. If deferred revenue is always the last schedule finished, that is your bottleneck. If agencies keep posting cost reclasses after the close, your project accounting process is weak upstream.

Tie these close metrics to your reporting package so leadership sees whether finance is improving the operating system, not just publishing statements. This guide to financial dashboards and CEO KPIs shows how to connect close quality with the metrics founders review every month.

Best practices that separate elite teams from tired teams

Elite close performance comes from continuous accounting. That means the work is spread through the month so month-end becomes a review cycle, not a cleanup project.

For SaaS companies, that starts with revenue and cash systems talking to each other. Stripe, your billing platform, the general ledger, and the bank feed should reconcile throughout the month. Deferred revenue should not be rebuilt in a spreadsheet on Day 3.

For agencies and professional services firms, the same rule applies to project data. Time tracking, contractor costs, and percent-complete inputs need weekly review. If delivery leaders wait until month-end to explain what was completed, finance is guessing at margin.

Use these practices:

- Reconcile high-risk accounts during the month. Cash, payment processors, AR, AP, payroll liabilities, debt, and deferred revenue should not wait for month-end.

- Automate recurring entries. Standard accruals, prepaid amortization, payroll allocations, and software subscriptions should post from rules, not memory.

- Set hard cutoff rules. Late invoices, contract changes, and expense submissions need a policy with deadlines and owners.

- Require variance commentary. Material changes in revenue, gross margin, operating expenses, and working capital need explanation before the package is issued.

- Store support in real time. Approvals, invoices, contracts, and reconciliations belong in the close folder when the transaction happens, not after the audit request arrives.

Invoice capture is one of the easiest places to reduce manual work. Better OCR and structured extraction tools are reshaping AP workflows, and the future of invoice data extraction points in one direction. Fewer hand-keyed bills, fewer coding errors, and faster closes.

Founders usually ask whether this requires a larger finance team. It does not. It requires cleaner integrations, weekly discipline, and fewer spreadsheet patches. That is the whole point of a 5-day close roadmap. You prevent the end-of-month fire drill by building a system that keeps the books close-ready every week.

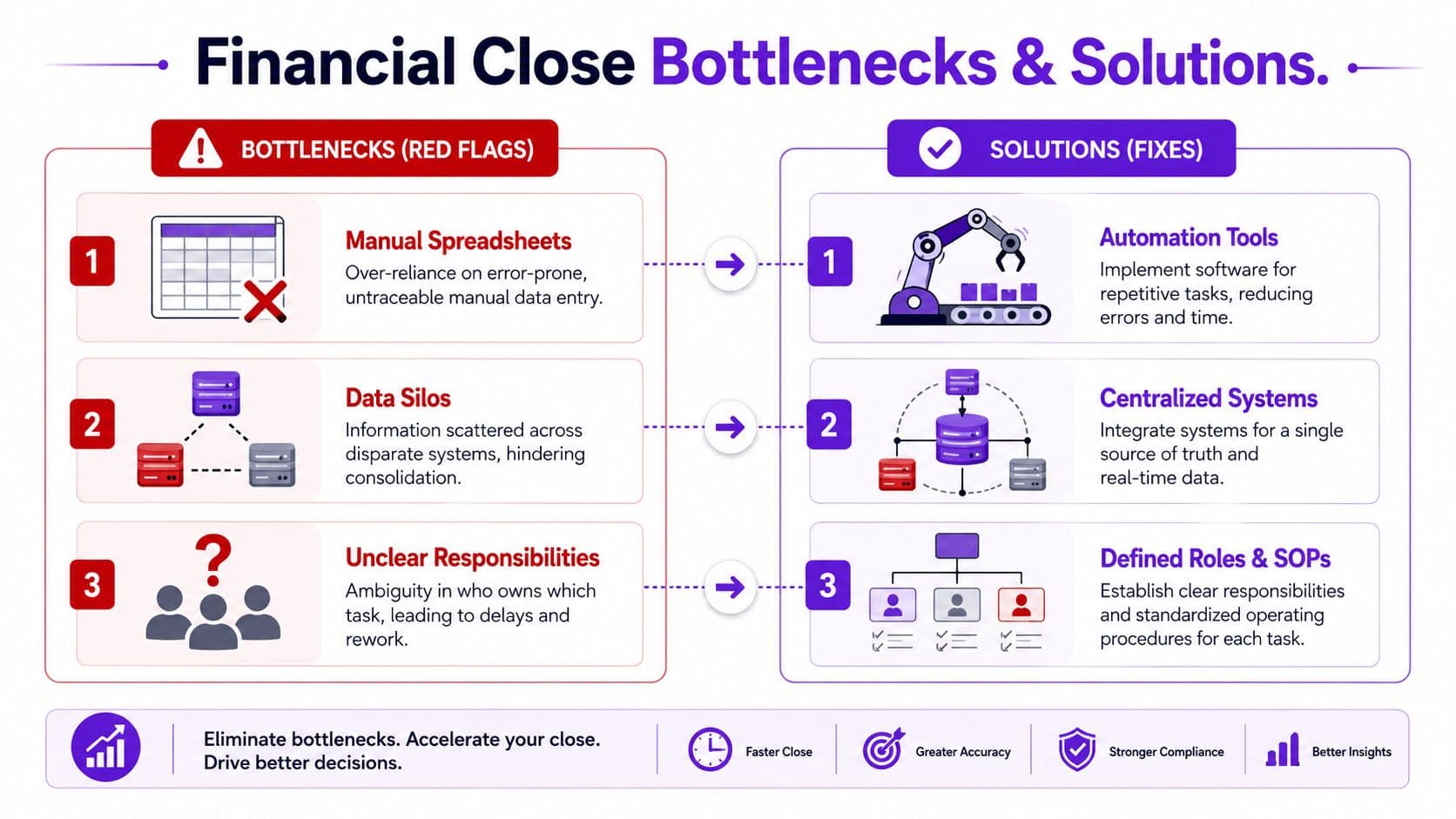

Common Bottlenecks and How to Fix Them

A close breaks for operational reasons long before it breaks for technical accounting reasons. In SaaS and service businesses, the pattern is predictable. Data sits in billing tools, payroll systems, bank feeds, AP software, and project platforms. Then finance tries to assemble the full picture in the last few days of the month. That is how you get delays, rework, and numbers nobody fully trusts.

The fix is process design built for a 5-day close. Keep the books close-ready throughout the month, automate what repeats, and force exceptions to the surface early.

Red flags that tell you your close is fragile

These are the failure points I see repeatedly in SaaS companies, agencies, and professional services firms.

-

Manual spreadsheet dependence

If your team exports data from QuickBooks, Xero, NetSuite, Stripe, Gusto, and project tools into multiple spreadsheets just to explain one month, the close is fragile. Version control fails, formulas drift, and reviewer time gets wasted checking mechanics instead of business performance. -

Revenue recognition handled manually at the end

SaaS companies often calculate deferred revenue movement at month-end instead of capturing contract changes as they happen. Agencies and service firms do the same with percent-complete estimates. The result is late adjustments, missed accruals, and margin reporting that changes after leadership already reviewed it. -

Receipts, bills, and approvals arrive late

Founders, department heads, and project leads often slow the close more than finance does. If invoices are sitting in inboxes or expenses are waiting for approval, AP ages badly and cash forecasts lose accuracy. -

Payment processor and payroll data do not tie cleanly

Stripe, Shopify, Square, PayPal, and Gusto create timing differences, fees, refunds, chargebacks, and clearing activity. A weak ledger setup can leave cash looking correct while revenue, fees, liabilities, or payroll allocations are wrong.

Fixes that work for lean finance teams

You do not solve these issues by pushing the team harder during the last two days of the month. You solve them by removing manual handoffs and assigning owners before month-end starts.

| Bottleneck | Better approach |

|---|---|

| Spreadsheet-based reconciliations | Use system rules, bank feeds, and standardized reconciliation templates so the team reviews exceptions instead of rebuilding the same schedules every month |

| Disconnected systems | Connect billing, payroll, expense, and payment platforms to the accounting system so transactions flow into one controlled record |

| Late approvals and missing support | Set cutoff dates by function and assign named owners for invoices, receipts, contract updates, and project status inputs |

| Manual invoice capture | Use structured extraction and approval workflows to reduce rekeying, coding delays, and missing documentation |

Invoice intake is a common bottleneck because it looks small until it stacks up. AP falls behind, accruals get guessed, and department spend becomes harder to explain. If that is happening in your business, the future of invoice data extraction shows where modern AP workflows are heading and why better capture upstream shortens the close downstream.

A few operating models work well, depending on your complexity.

-

QuickBooks or Xero plus disciplined integrations

This setup works for smaller teams when bank feeds are clean, AP and expense tools sync reliably, and revenue workflows are straightforward. -

NetSuite for multi-entity or more complex revenue operations

This is the better fit when you need stronger approval controls, entity-level reporting, or more nuanced revenue and deferred revenue handling. -

Outsourced controller support when the problem is execution Sometimes the software stack is adequate and the close still drags. That usually means ownership is unclear, review steps are inconsistent, and nobody is running the close like an operating process. Jumpstart Partners is one example of a firm that supports SaaS and agency businesses with outsourced controller and bookkeeping services built around a 5-day close.

If your close depends on one person remembering 20 manual steps, you have a key-person risk, not a finance process.

Document the close the same way you would document a revenue workflow or customer onboarding process. Every recurring task needs an owner, due date, review point, and backup. Every balance sheet account needs support that can stand up to diligence. Use an auditor readiness checklist to pressure-test whether your reconciliations and documentation would hold up under investor or audit scrutiny.

Achieve Audit and Investor Readiness

Investors don't just look at growth. They look at control. A business that can close accurately and quickly signals that leadership understands the numbers and can scale without losing grip.

A disciplined financial close process also makes audits less painful. When reconciliations are current, support is organized, and policies are documented, the audit becomes a review of evidence instead of a scramble to recreate history. If you're preparing for that stage, this auditor readiness checklist is the right place to pressure-test your documentation.

For founders, the takeaway is simple. A fast close is not a vanity metric. It is proof that your company can produce reliable financials, explain performance, and respond to diligence requests without chaos.

That matters when you're raising money, managing cash tightly, or preparing the business for a sale.

If you want a tighter financial close process without building a full internal finance team, Jumpstart Partners can help you implement a practical 5-day close, clean up reconciliations, and produce investor-ready monthly financials for your SaaS company or agency.