Financial Operations

How to Audit Financial Records: An Audit-Ready Playbook

Learn how to audit financial records with our step-by-step playbook for SaaS and service firms. Master ASC 606, internal controls, and pass your next audit.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readIf you're running a SaaS company or service firm in the $500K to $20M revenue range, your first audit usually doesn't fail because someone stole money. It fails because revenue was mapped incorrectly, deferred revenue was handled loosely, and the close process never produced clean support in the first place. One widely cited benchmark says 68% of audit adjustments in tech companies stem from improper deferred revenue or subscription period mapping under ASC 606, and pre-audit cleanup often uncovers $47K+ in errors per client (NetSuite overview).

That's why learning how to audit financial records isn't an academic exercise. It's a founder-level operating discipline. If you're preparing for fundraising, debt, a sale process, or your first external audit, your books need to do more than tie out at a high level. They need to hold up under testing.

A solid audit process starts long before fieldwork. It starts with your monthly close, your contract-to-revenue workflow, and the controls around QuickBooks, Stripe, Shopify, Gusto, or NetSuite. If those systems don't agree, the audit becomes expensive, slow, and distracting.

Table of Contents

- Why Your First Audit Is a Test of Your Business Not Just Your Books

- Your 90-Day Pre-Audit Preparation Timeline and Checklist

- Build an Audit-Proof Month-End Close Process

- Master ASC 606 Revenue Recognition for SaaS and Services

- Implement and Document Key Internal Controls

- Find and Fix These Common Errors Before Your Auditor Does

Why Your First Audit Is a Test of Your Business Not Just Your Books

An audit is a business test because it measures whether your finance function can produce evidence, not just whether your P&L looks plausible. Lenders, investors, buyers, and boards don't care that your team “basically knows” how revenue was booked. They care that the accounting is consistent, supportable, and repeatable.

A financial audit gives stakeholders “reasonable assurance,” which means a high, but not absolute, level of confidence that your records are free from material misstatement and prepared under standards such as GAAP or IFRS. Auditors evaluate the balance sheet, income statement, and statement of cash flows as part of that process (financial audit overview).

What your auditor is really evaluating

Auditors aren't just looking for missing receipts. They're asking three harder questions:

- Are your numbers complete

- Are your numbers accurate

- Can your team prove both quickly

That's why the standard audit flow matters. In practice, auditors plan the engagement, test controls and balances, and then issue a report. During planning, they assess business risk and decide where misstatements are most likely. During testing, they reconcile accounts, trace entries, and compare accounting records to outside evidence such as bank statements and customer confirmations. Then they report the result.

Practical rule: If your accounting requires a long verbal explanation, you're not audit-ready.

For founder-led companies, the biggest trap is treating the audit like a one-time project. It isn't. It's the year-end score of how you ran finance all year.

Why this matters before fundraising or a sale

A clean audit does more than satisfy compliance. It validates management's representations, strengthens investor confidence, and gives you a reliable basis for decisions on hiring, pricing, and cash use. If your books don't hold up, every due diligence request gets slower and more expensive.

If you want a plain-English comparison of internal versus external audit roles before you start, Bookkeeping and Accounting of Florida audit advice gives a useful framing for founders who are sorting out who should test what.

Your 90-Day Pre-Audit Preparation Timeline and Checklist

Most painful audits start the same way. The auditor sends the initial request list, your controller starts digging through email threads, contracts are stored in three places, payroll support is incomplete, and no one can explain which Stripe export matches the general ledger.

You fix that with a 90-day countdown, not a week of panic.

What an audit-ready data room looks like

Your goal is simple. Build one secure folder structure where every major balance can be tied to support without extra interpretation. For most companies, that means separate folders for bank activity, revenue, expenses, payroll, taxes, equity, debt, and corporate records.

A good data room has these characteristics:

- One source per item: Bank statements come from the bank, not screenshots from Slack.

- Consistent naming: Use month and account in the file name.

- Clear ownership: One person owns each request.

- Version control: Final files only. No “final_v2_revised_reallyfinal.”

If you work with a nonprofit arm, a fiscal sponsor, or restricted-fund reporting, this guide to preparing for fiscal sponsor audits is a good reference for how disciplined documentation reduces review friction.

For a founder-friendly companion checklist, keep this audit preparation checklist open while you build your folder structure.

Your 90-day checklist

| Timeline | Document Category | Specific Items to Collect |

|---|---|---|

| T-90 | Cash and banking | All bank statements for the full year, credit card statements, loan statements, merchant processor statements |

| T-90 | Revenue | Signed customer contracts, order forms, billing schedules, invoices, customer payment history, deferred revenue schedules |

| T-90 | Accounting records | General ledger, trial balance, chart of accounts, monthly financial statements, sub-ledgers |

| T-90 | Payroll and people | Payroll reports, contractor payments, bonus documentation, benefit invoices, payroll tax filings |

| T-60 | Balance sheet support | AR aging, AP aging, prepaid schedules, fixed asset rollforward, debt amortization schedules |

| T-60 | Tax and legal | Sales tax filings, income tax returns, state registrations, board consents, cap table, stock issuances |

| T-60 | Systems and controls | User access lists for QuickBooks, Stripe, Shopify, Gusto, approval workflows, change logs where available |

| T-30 | Audit support pack | Reconciliations, tie-out schedules, revenue memos, unusual transaction support, prior issue log and fixes |

The timeline matters because some documents take time to produce cleanly. Contracts need review. Deferred revenue schedules need recalculation. Payroll support often needs reconciliation back to the general ledger.

During substantive testing, auditors often select samples and test them against underlying records, including compliance with standards such as ASC 606 for revenue recognition. They also reconcile ledgers and trace entries through the accounting system (financial audit process reference). If your support is scattered, every sample becomes a delay.

The fastest way to slow an audit is to make the auditor ask twice for the same support.

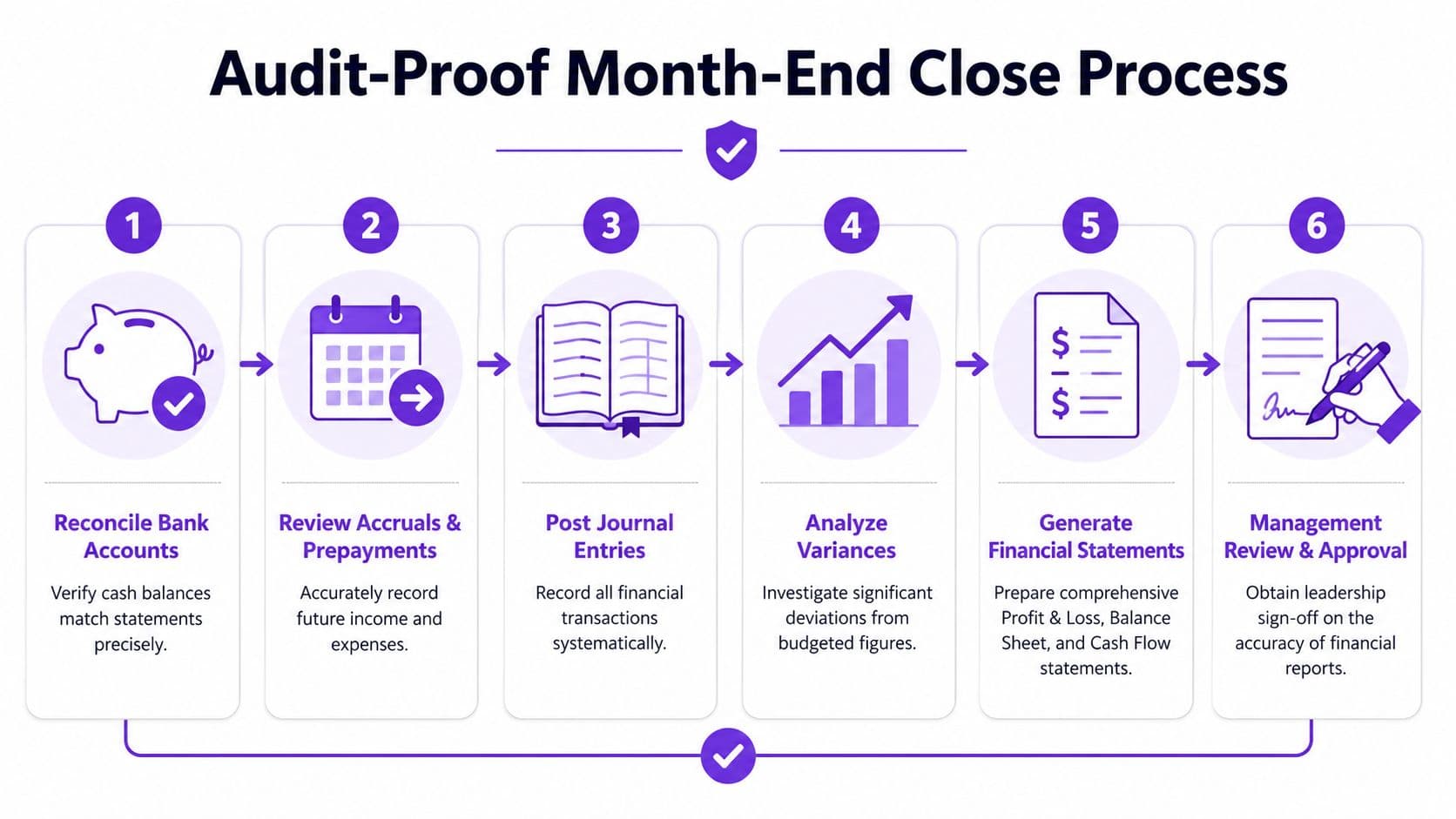

Build an Audit-Proof Month-End Close Process

Your audit result is the output of your monthly close. If the close is sloppy for eleven months, a clean December binder won't save you.

According to OpenView's 2024 SaaS Benchmarks, high-performing SaaS firms complete the month-end close within 5 days, and your audit plan should include a monthly reconciliation checklist so journal entries hit the general ledger on time (Maxio summary of the benchmark).

What good looks like in a 5-day close

A fast close doesn't mean cutting corners. It means you've standardized the work, assigned owners, and stopped waiting until year-end to clean up recurring issues.

Here's the benchmark-driven standard I recommend for SaaS, agencies, and services firms:

| Close Day | Primary Focus | What must be completed |

|---|---|---|

| Day 1 | Revenue and billing | Sync invoices, cash receipts, processor activity, deferred revenue changes |

| Day 2 | Expenses and accruals | Code transactions, accrue missing vendor costs, review prepaid activity |

| Day 3 | Cash reconciliations | Reconcile bank accounts, credit cards, Stripe or Shopify clearing balances |

| Day 4 | Balance sheet review | Reconcile AR, AP, payroll liabilities, loans, deferred revenue, fixed assets |

| Day 5 | Final review | Variance analysis, management review, financial package issuance |

The teams that struggle usually skip Day 4 discipline. They post revenue and expenses but leave balance sheet accounts half-reconciled. That creates audit pain because auditors test the balance sheet heavily.

For a deeper operating model, this guide on month-end close best practices is worth using as your internal checklist.

The close process that actually works

The close has to be repeatable. That means no heroic spreadsheet rebuilds and no month-end logic that lives in one person's head.

Use this sequence:

- Reconcile processor balances first: If you use Stripe, Square, or Shopify, tie payout activity to gross sales, fees, refunds, and timing differences.

- Post accruals with support: Every accrual needs a source. Vendor invoice, contract, payroll report, or a documented estimate.

- Review unusual variances: If gross margin, payroll, software expense, or deferred revenue moved unexpectedly, explain it before you close.

- Lock the period: Don't let the team back-post without approval after statements go out.

Auditors performing fieldwork typically test internal controls, verify segregation of duties, review access controls, and vouch transactions to source documents such as invoices and bank statements (audit process phases). A disciplined close gives them a clean trail.

This walkthrough helps visualize the rhythm of a tighter close:

Master ASC 606 Revenue Recognition for SaaS and Services

Revenue recognition drives a large share of first-year audit adjustments for SaaS and service businesses. In companies between $500K and $20M, I usually see the same pattern: billing is organized, cash collection is fine, but the revenue schedule does not match the contract.

For audited financials, cash timing is not the answer. Contract terms are. If you sell subscriptions, implementation, onboarding, managed services, support retainers, or bundled packages, ASC 606 needs to be applied at the contract level and then tied back to the general ledger.

The mistake that creates audit trouble

Founders often book from the invoice and only revisit revenue at year-end. That works until the auditor asks for three things on the same sample: the signed agreement, the billing record, and the revenue entry. If those three do not agree, the auditor expands testing.

For SaaS and service businesses, your revenue file needs one clear chain from contract to journal entry:

- Signed contract terms and amendments

- Billing schedule and invoice dates

- Service start date or subscription term

- Identified performance obligations

- Revenue recognition schedule

- Deferred revenue rollforward

That support needs to hold up for renewals, upgrades, discounts, early terminations, and credits. Those are the high-risk areas generic audit guides skip, and they are exactly where smaller SaaS companies get hit with adjustments.

If your model combines software with payroll administration, outsourced operations, or other service layers, guidance like these revenue considerations for PEO helps frame where bundled arrangements get harder to account for.

What ASC 606 looks like in a real SaaS contract

Use a straightforward example:

- Annual software subscription: $24,000

- One-time implementation fee: $2,500

- Total contract value: $26,500

Assume the contract has two performance obligations:

- Software access delivered over 12 months

- Implementation completed during setup

If standalone selling prices match the contract pricing, the allocation is simple:

- Subscription revenue: $24,000

- Implementation revenue: $2,500

Recognition follows delivery.

Recognition schedule

| Item | Amount | Recognition pattern |

|---|---|---|

| Annual subscription | $24,000 | $2,000 per month over 12 months |

| Implementation fee | $2,500 | Recognized when setup is completed |

| Total contract | $26,500 | Based on each obligation's completion pattern |

Journal logic in plain English

If the customer pays the full $26,500 upfront on day one, do not book $26,500 to revenue.

On cash receipt:

- Debit Cash $26,500

- Credit Deferred Revenue $26,500

When implementation is complete:

- Debit Deferred Revenue $2,500

- Credit Revenue $2,500

At each month-end for the subscription:

- Debit Deferred Revenue $2,000

- Credit Subscription Revenue $2,000

After month one, recognized revenue is $4,500. Deferred revenue is $22,000.

Auditors want to see this math tied to source documents, not rebuilt in a spreadsheet the night before fieldwork.

Where SaaS and service companies usually get ASC 606 wrong

The problem is rarely the basic annual subscription. The problem is everything attached to it.

Common trouble spots include:

- Discounted bundles: A contract includes software, onboarding, and support, but all revenue is recognized ratably because no one allocated the discount across obligations.

- Upgrades mid-term: The customer adds seats or a premium module in month five, but billing is updated without revising the revenue schedule.

- Auto-renewals with price changes: The invoice is correct, but the revenue schedule still uses the prior contract value.

- Implementation that is not distinct: Teams recognize setup fees immediately even when the work does not transfer a separate benefit to the customer.

- Managed services mixed with SaaS: A monthly fee covers both access to the platform and recurring service work, but the company treats the entire amount as subscription revenue.

Those errors create two expensive outcomes. Revenue is misstated, and deferred revenue no longer ties to underlying contracts. Once that happens, the audit team tests more samples and asks for manual reconciliations.

A practical fix is to maintain a contract matrix that lists each customer agreement, the promised goods or services, the recognition pattern, and the related deferred revenue balance. For a more detailed operating framework, use this guide to 606 revenue recognition for SaaS and service businesses.

What good audit support looks like

A clean revenue file should let an auditor pick one contract and trace it in minutes.

That means:

- The signed agreement matches the customer, term, and pricing in your billing system

- The billing system matches the amounts posted to accounts receivable or cash

- The revenue schedule matches the contract obligations and timing

- The deferred revenue rollforward agrees to the balance sheet

- Any manual journal entry has written support and reviewer sign-off

If any one of those links breaks, revenue becomes a high-risk audit area. For SaaS and service firms, that risk grows fast when month-end close is sloppy or contract changes sit outside accounting until quarter-end.

Implement and Document Key Internal Controls

Even if your numbers are right, weak controls make auditors do more work. When they can't rely on your process, they increase testing. That drives delays, more questions, and more fees.

To support SOX-style financial accuracy, companies need to document and test controls, including logs of changes to billing, CRM, and accounting software, and they need to verify that deferred revenue reconciles to underlying data (SOX-focused audit guidance).

Controls auditors expect to see

You don't need enterprise bureaucracy. You need a small set of controls that operate effectively.

| Control Area | What good looks like | Why it matters |

|---|---|---|

| Cash disbursements | One person enters bills, another approves payment | Reduces unauthorized or duplicate payments |

| User access | Regular review of QuickBooks, Stripe, Shopify, Gusto users | Prevents former staff or excess admins from changing data |

| Revenue changes | Billing plan and contract changes logged and approved | Stops silent edits that break revenue schedules |

| Journal entries | Non-routine entries reviewed before posting | Catches manual misstatements |

| Reconciliations | Monthly sign-off on all key balance sheet accounts | Creates audit evidence and accountability |

The control founders resist most is segregation of duties. They'll say the team is too small. Sometimes that's true operationally, but then you need a compensating review. If one person can create a vendor, enter a bill, and release payment, someone senior needs to review the full disbursement report.

A useful implementation guide for this is segregation of duties, especially for lean finance teams using outsourced support.

How to document controls without overbuilding

Documentation should answer four questions:

- Who performs the control

- What they review

- When they perform it

- Where evidence is stored

Examples that work:

- Monthly bank reconciliation signed and dated

- Approval screenshot for a non-routine journal entry

- Quarterly export of system users with management review notes

- Change log for billing settings in Stripe or CRM fields tied to invoicing

Weak controls don't just increase fraud risk. They also make clean numbers harder to prove.

One more point that gets missed in founder-led teams. Auditors care about management's commitment to ethical practices and the control environment before they place reliance on individual controls. If approvals are inconsistent, backdating is tolerated, or system access is shared, the problem isn't just bookkeeping. It's governance.

Find and Fix These Common Errors Before Your Auditor Does

Auditors rarely find new problems. They surface problems your close process has been carrying for months.

For SaaS and service businesses between $500K and $20M, the expensive errors usually sit in three places: ASC 606 revenue recognition, weak reconciliations, and balance sheet accounts nobody has cleared. I see founders focus on EBITDA and cash runway while deferred revenue, accrued expenses, and contract timing drift out of line. Then the audit starts, and a two-week fieldwork plan turns into six weeks of follow-up.

Start with the items that trigger the most audit questions and the most rework.

- Deferred revenue does not tie to signed contracts or billing data: A common example is a $24,000 annual SaaS contract billed upfront, with the full amount recognized in month one instead of $2,000 per month over the service term.

- Subscription changes are booked with shortcut logic: Mid-cycle upgrades, downgrades, credits, free months, and renewals often break the revenue schedule if the team relies on spreadsheets instead of contract-level support.

- Implementation or onboarding fees are recognized too early: If setup work is not a distinct performance obligation, that revenue often needs to be recognized over the contract term, not on the invoice date.

- Unbilled revenue is booked from expectation instead of evidence: “We'll invoice it next month” is not support. Auditors want proof that the work was performed, the amount is measurable, and the customer is obligated to pay.

- Stripe, payment processor, or merchant balances do not reconcile to the general ledger: Fees, reserves, chargebacks, and payout timing differences often sit in clearing accounts for months and distort cash and revenue.

- Capitalized software costs are inconsistent: Teams capitalize internal development hours one quarter, expense them the next, and have no written policy for what qualifies.

- Accrued expenses and prepaid expenses are stale: Service firms often carry old accruals long after the vendor bill is paid, or they expense annual software subscriptions immediately instead of amortizing them.

The pattern matters. One mistake in revenue usually points to a larger process gap. If deferred revenue is wrong, contract review is usually weak, the close checklist is incomplete, or billing system changes are not being reviewed before month-end.

Cash is the fastest place to test whether the books are dependable. If your reconciliations are late, incomplete, or full of old reconciling items, assume other accounts have similar issues. A disciplined bank reconciliation process for audit-ready books gives you an early read on whether the close is based on real support or guesswork.

Errors that cost more than they look

Some issues look small and still create outsized audit pain.

A $15,000 revenue misclassification may not change the business materially on its own. But if it exposes that revenue is being posted from invoices instead of performance obligations, the auditor will expand testing across the full population. That means more samples, more support requests, more partner review time, and more pressure on your team.

I have seen a single unsupported accrual lead auditors to retest the entire liability rollforward. I have also seen one bad contract memo force a full rework of SaaS revenue for the year because nobody documented how implementation, licenses, and support were separated under ASC 606.

Common objections that do not hold up

“We're too small for auditors to care about this.”

Smaller companies often get more scrutiny because the process depends on one or two people, with more manual overrides and less formal review.

“Our books are closed every month, so we should be fine.”

A closed month is not the same as an audit-ready month. I regularly see closed books with unsupported journal entries, uncleared suspense accounts, and revenue schedules that do not match the contract terms.

“We'll fix adjustments during fieldwork.”

You can, but you will pay for it. Audit fees rise, internal time gets pulled into support requests, and lenders or investors start asking why basic accounting issues were found so late.

The practical fix is straightforward. Pull a sample of contracts, trace them to invoices and revenue recognition, reconcile every cash and clearing account, clear old balance sheet items, and force written support for unusual entries before the auditor asks for it.

If your team cannot explain how a number was calculated in two minutes, fix that now.