Financial Operations

The Founder's Audit Preparation Checklist: 8 Action Steps

Get your business audit-ready with our 2026 audit preparation checklist. Follow these 8 steps for SaaS, agency, and e-commerce companies for a successful audit.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··25 min readYour first audit doesn't have to be a nightmare. Audit readiness now follows a staged timeline in more demanding environments, with one PCAOB-focused readiness guide outlining an initial preparation phase of 6 to 12 months, an IPO preparation phase of 6 to 12 months, and a final transaction phase of 6 months for documentation and audited statements (Grassi Advisors on PCAOB audit readiness). That should change how you think about an audit preparation checklist. This is not a year-end cleanup project. It's an operating discipline.

For founders running SaaS companies, agencies, and service firms, the financial audit is usually tied to something bigger. A fundraise. A lender review. A strategic partnership. A diligence process. If your books are slow, undocumented, or dependent on one person's memory, the audit exposes it fast.

A real audit preparation checklist also isn't just a pile of files. The core evidence set is recurring and predictable: financial statements, general ledgers, bank statements, invoices, receipts, and tax returns. Stronger checklists also include internal controls, timelines, ownership, org charts, bylaws, board minutes, payroll tax forms, lease agreements, and proof of transaction flow through the business because missing support, not the audit itself, is often what derails the process (HubiFi guide to financial audit checklists). If you're also navigating broader governance demands, this sits alongside mastering Australian compliance.

You don't need generic advice. You need the founder's version of the list. Prioritized. Operational. Tied to speed, cost, and risk. Start here.

Table of Contents

- 1. Organize and Reconcile All Bank and Credit Card Accounts

- 2. Complete Revenue Recognition and ASC 606 Compliance Review

- 3. Prepare and Verify Fixed Assets Schedule with Depreciation

- 4. Document and Test All Journal Entries Especially Manual and Consolidating Entries

- 5. Reconcile All Balance Sheet Accounts Especially Payroll Liabilities and Accruals

- 6. Prepare Debt and Equity Schedule with Covenant Compliance Documentation

- 7. Compile Supporting Documentation for Complex or Non-Routine Transactions

- 8. Schedule Internal Control Assessment and Documentation Review

- 8-Point Audit Prep Checklist Comparison

- Turn Your Audit from a Liability into an Asset

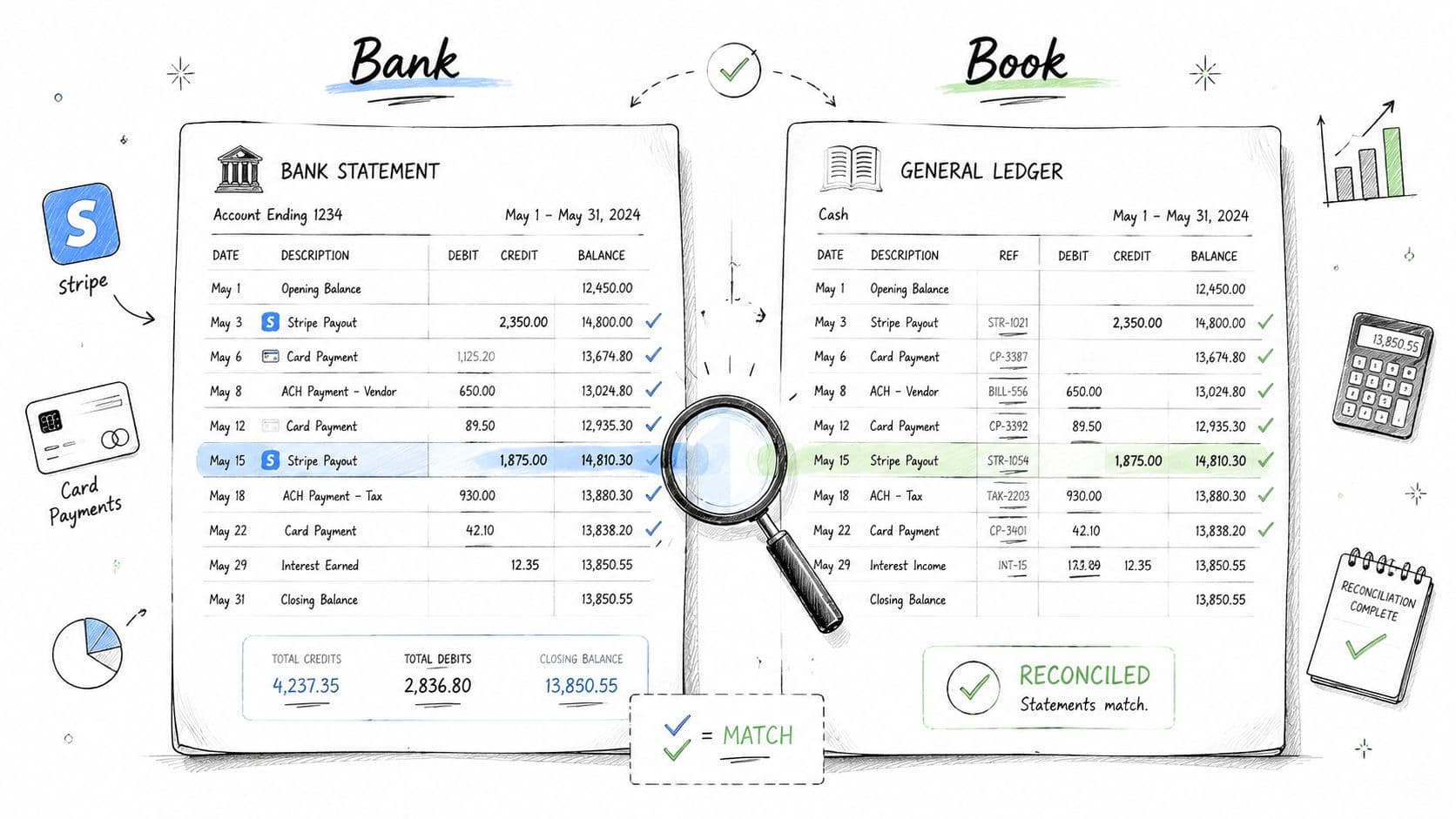

1. Organize and Reconcile All Bank and Credit Card Accounts

If cash doesn't tie out, nothing else matters. Auditors start with cash because it's the fastest way to see whether your books are grounded in reality or stitched together from partial reports, delayed postings, and founder memory.

A SaaS company collecting through Stripe, billing annual contracts upfront, and pushing summaries into QuickBooks can look clean on the P&L while cash postings drift for months. An agency can have the same issue across operating accounts, credit cards, and client-holding accounts. A DTC brand can see it through Shopify payouts, refunds, reserves, chargebacks, and timing differences.

Why cash reconciliation gets expensive fast

When bank accounts aren't reconciled monthly, your team spends audit week rebuilding history instead of answering questions. That's expensive in two ways. You pay your auditor to wait, and you pull your controller, founder, or ops lead into cleanup work that should've been finished during the close.

Practical rule: Reconcile every bank account, credit card, Stripe account, PayPal account, and merchant reserve account through the audit period before fieldwork starts.

Use the native reconciliation workflows in QuickBooks, Xero, or NetSuite. Pull bank statements, merchant processor statements, and clearing account detail by month. Then document every outstanding item with date, explanation, and expected resolution.

What clean support looks like

For this part of your audit preparation checklist, clean means more than “the ending balance matches.” It means an auditor can start with the statement, trace the activity into the general ledger, and understand any difference without a meeting.

- Separate each source of cash: Don't lump Stripe, Square, PayPal, and operating cash into one reconciliation logic. Each has its own fees, timing, and reserve behavior.

- Review aged reconciling items: Anything sitting unresolved across month-end close cycles deserves explanation and owner follow-up.

- Keep support with the rec: Store the statement, reconciliation report, and notes in one folder by month.

- Train one repeatable process: Your team should use the same close checklist every month, not invent a new one in audit season.

If you need a tighter operating process, use a step-by-step bank account reconciliation workflow. For statement cleanup, teams also use tools covered in this bank statement PDF to Excel converter guide.

A practical scenario: if Stripe deposits net of fees and refunds, your ledger should still show gross sales, fees, refunds, and net cash movement separately. If you only book deposits, your revenue, fees, and liabilities are probably wrong.

2. Complete Revenue Recognition and ASC 606 Compliance Review

Revenue is where growth companies get punished for shortcuts. If you sell subscriptions, implementation work, prepaid retainers, usage-based plans, milestone billing, or mixed service bundles, you need a documented revenue position before the auditor asks for it.

Founders often assume the billing system defines revenue. It doesn't. Billing creates invoices and cash collection. Revenue follows performance obligations, contract terms, and timing. That gap is exactly where ASC 606 problems show up.

Revenue is where founders get surprised

A SaaS business with annual contracts billed upfront doesn't earn all of that revenue on invoice date. A professional services firm with milestone invoices doesn't automatically recognize revenue because a payment arrived. An agency with retainer plus project overages has to separate what is recurring from what is delivered over time or at a point in time.

Put the accounting policy in writing. Pull a sample of standard contracts, non-standard deals, renewals, credits, free trial conversions, and amended statements of work. Then reconcile your subscription system or CRM billing detail to the general ledger every month. If you need a practical reference on the mechanics, use this ASC 606 revenue recognition overview.

This walkthrough helps teams visualize where revenue treatment breaks:

How to document the judgment

Your audit file should show how you identified performance obligations, determined transaction price, and allocated revenue across the service period. If the deal is standard, the memo can be short. If the deal is unusual, the memo needs enough detail that the auditor doesn't have to reconstruct your logic from contracts and Slack threads.

Revenue treatment should be understandable without the salesperson, founder, or controller in the room.

Keep a deferred revenue rollforward. Keep a schedule that shows what was billed, what remains deferred, and what was recognized in each month. For SaaS and agency businesses, this one schedule often becomes a central audit support file.

A real-world example: if you sell a twelve-month software contract with a setup package and one-off training, document whether setup creates a separate performance obligation or supports the subscription service. The answer changes the timing. If you don't write it down when the contract is signed, you'll argue about it during the audit, when the stakes and pressure are higher.

3. Prepare and Verify Fixed Assets Schedule with Depreciation

Fixed assets rarely break a business. They regularly expose sloppy finance operations. If your schedule is outdated, missing invoices, or inconsistent with your capitalization policy, the auditor learns two things quickly. Your close process is weak, and your policy discipline is weak.

For many founder-led companies, the fixed asset list starts as a tax schedule and never evolves. That's not enough. Your audit file has to support what you bought, when it went into service, how you classified it, how you depreciated or amortized it, and whether it still exists.

The schedule has to prove existence and policy

Build a detailed schedule for laptops, office build-outs, leasehold improvements, capitalized software, furniture, equipment, and any implementation costs you've capitalized. Include cost basis, date placed in service, useful life, depreciation method, accumulated depreciation, and any disposal history.

A software company may capitalize internal development costs or purchased software. An agency may need support for leasehold improvements from an office expansion. A business that shut down a location needs to show what was impaired, disposed of, or still in use.

The strongest operational checklists emphasize a centralized evidence index, standardized naming, direct mapping of each artifact to a control or clause, version control, and audit trails because that cuts search time and makes every balance traceable (AI Gap Analysis on audit readiness checklist structure).

What founders usually miss

The common misses are simple. No invoice attached. No capitalization threshold documented. No proof of disposal. No review of lease agreements. And no consistency across periods.

- Set one capitalization policy: Apply the same threshold and useful-life logic across the year.

- Tie every addition to support: Keep the vendor invoice, approval, and placed-in-service date.

- Review disposals deliberately: If an employee laptop was replaced or an office was closed, remove or impair the asset correctly.

- Check lease-related additions: Build-outs and lease incentives often need separate support.

A clean example: if you spent money on a tenant improvement project, don't book one lump line and move on. Split contractor work, furniture, wiring, and software-related items where needed. That single step saves hours of audit back-and-forth because the auditor won't need to decode one blended amount after the fact.

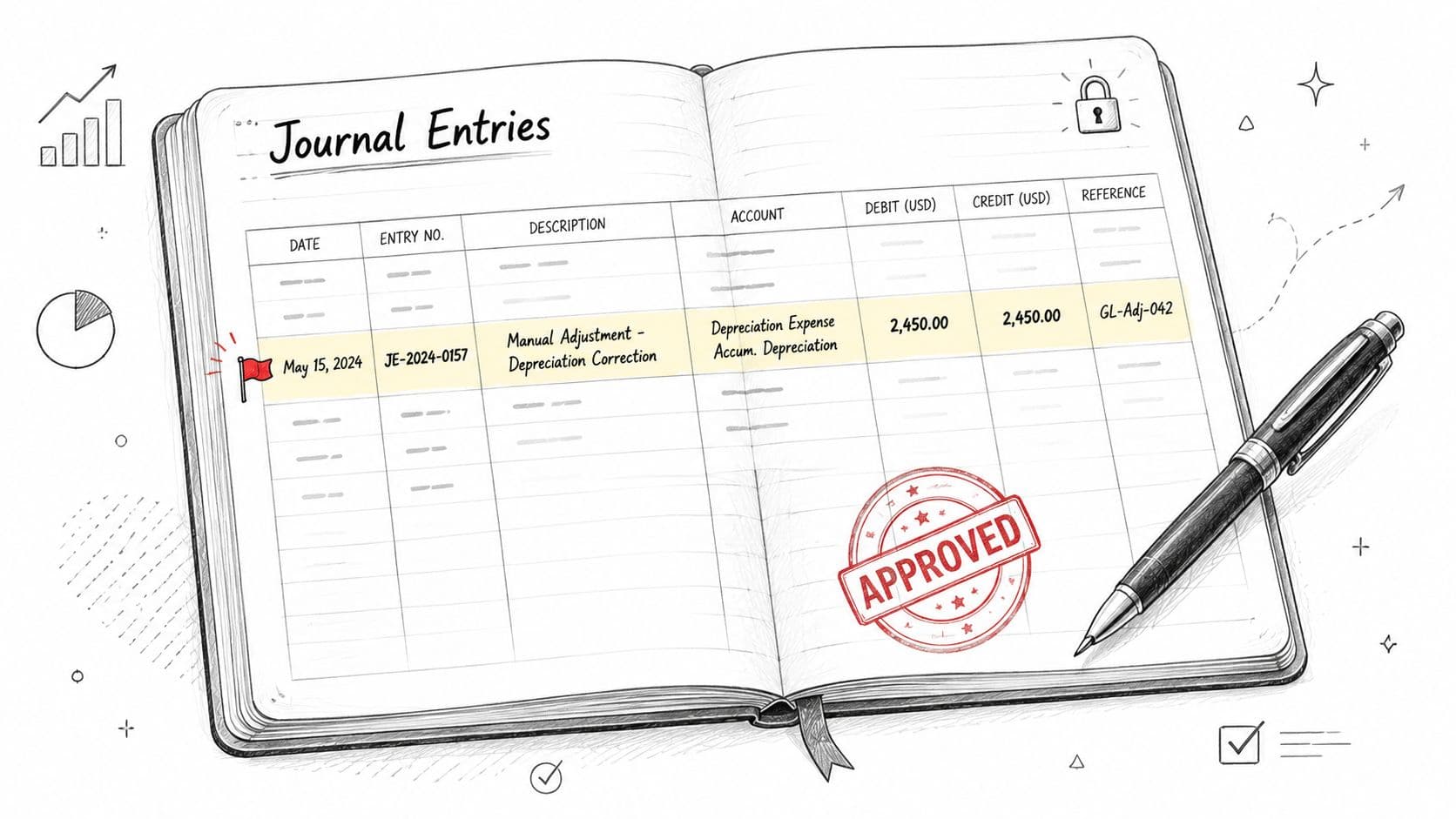

4. Document and Test All Journal Entries Especially Manual and Consolidating Entries

Manual journal entries are where auditors look for overrides, rushed fixes, and unsupported accounting. That doesn't mean manual entries are bad. It means undocumented manual entries are expensive.

If your close depends on spreadsheet uploads, top-side entries, revenue true-ups, accrual releases, and late founder adjustments, every one of those needs a support trail. The risk increases again if you run multiple entities and post consolidating entries at month-end or year-end.

Manual entries attract scrutiny

Your journal entry population should be complete and easy to filter. Separate automated system entries from manual entries. Tag consolidating entries. Flag revenue, payroll, accrual, and equity entries because those usually deserve more scrutiny.

Use a standard template for every manual entry. Include the date, amount, accounts, business purpose, preparer, approver, supporting file link, and whether the entry reversed automatically. If the entry was based on a calculation, archive the calculation with the source data.

If a journal entry needs a meeting to explain it, the documentation is weak.

For teams cleaning this up, understanding the structure of the general ledger and journal flow helps standardize support and reviewer expectations.

Build a journal entry log auditors can follow

A SaaS company may post a deferred revenue adjustment after reconciling billing exports. An agency may post unbilled revenue accruals based on work delivered before invoice. A parent company may eliminate intercompany balances and revenue during consolidation. None of that is unusual. What matters is whether the entry ties to source support and approved logic.

Use one centralized log by month. Make sure the memo field in the accounting system says something useful. “To adjust balance” is useless. “To record deferred revenue release for annual contract recognized ratably” is useful.

This part of your audit preparation checklist pays off operationally too. The same documentation that satisfies the auditor also makes your month-end review faster, reduces controller dependency, and lowers the odds that the same correction gets posted twice in different periods.

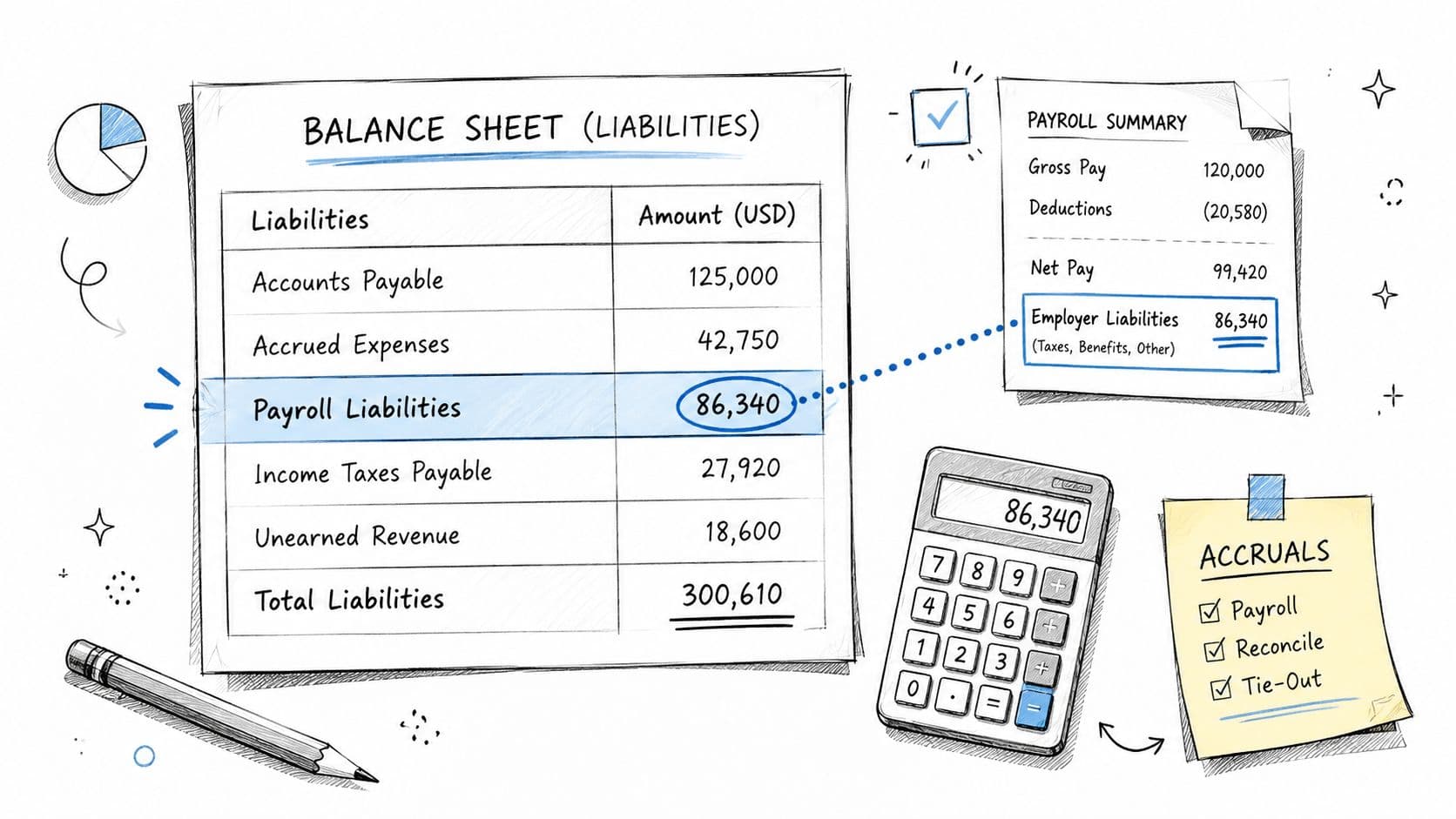

5. Reconcile All Balance Sheet Accounts Especially Payroll Liabilities and Accruals

Most founder-led teams watch the P&L and ignore the balance sheet until something breaks. That's backward. A clean balance sheet is the strongest evidence that your close is real.

Accounts receivable, prepaid expenses, accrued payroll, accrued expenses, deferred revenue, sales tax payable, inventory, intercompany balances, and customer deposits should all reconcile to something outside the general ledger. If a balance has no supporting schedule, treat it as suspect.

This is where the close either works or fails

Payroll liabilities are a common failure point. Your books may show one amount while Gusto, Rippling, ADP, or another provider shows something else because payroll timing, benefit deductions, tax remittances, and off-cycle runs weren't mapped properly. The same pattern appears in accrued expenses when teams leave old estimates sitting in the books long after invoices arrive.

Use monthly reconciliation templates by account. Tie payroll liabilities to payroll reports. Tie accrued expenses to invoices, contracts, or management-approved estimates. Tie deferred revenue to your billing or subscription system. Tie AR to aging reports and reserve logic.

Red flags to fix before fieldwork

At this point, I tell founders to stop accepting vague answers from the finance function.

- Old reconciling items: If no one can explain why a balance has sat unchanged across multiple closes, clear it or support it.

- Round-number accruals: Repeating the same estimate without refresh is a warning sign.

- Payroll mismatches: If payroll reports and GL balances don't tie, resolve the mapping before the audit.

- Intercompany balances that don't match: One entity's receivable should equal the other entity's payable.

A practical agency example: if your project system shows unbilled work delivered before month-end, reconcile that support to unbilled revenue or WIP. Don't wait for the auditor to ask why gross margin shifts after invoicing.

6. Prepare Debt and Equity Schedule with Covenant Compliance Documentation

Loan defaults and cap table mistakes rarely start as big problems. They start as missing approvals, stale covenant calculations, and terms no one translated into the accounting.

This section matters because debt and equity errors are expensive. A missed covenant can trigger default language, waiver fees, and extra legal work. A sloppy cap table can slow a financing, create disputes over ownership, and force auditors to spend hours tracing documents you should have organized before fieldwork.

If you have venture debt, a line of credit, SAFEs, preferred stock, options, warrants, founder notes, or related-party loans, build one master schedule and keep it current every month. For founders, that is the standard. Annual cleanup costs more and creates avoidable risk.

Build one schedule that ties legal terms to accounting

Your debt schedule should show lender, original amount, current balance, interest rate, payment terms, maturity, collateral, covenant definitions, reporting deadlines, and amendment history. Your equity schedule should show every issuance, exercise, repurchase, conversion, cancellation, and board approval, with dates that tie back to the general ledger and legal records.

Keep the support in one indexed folder. Include signed loan agreements, amendments, board consents, subscription documents, SAFE agreements, option grant approvals, and cap table reports. If approval authority is unclear or too concentrated, clean that up now with stronger segregation of duties in finance processes. Auditors will ask who approved what, and lenders care too.

If your cap table still lives in a spreadsheet passed around by email, fix that before the audit. This capitalization table software overview is a useful starting point.

Calculate covenant compliance monthly, not at quarter-end panic speed

Founders often wait until the lender reporting package is due to test covenants. That is a mistake. You want covenant compliance calculated as part of the monthly close, with evidence of management review.

For a SaaS company, that can mean proving recurring revenue, cash balance, or EBITDA metrics using numbers that already reflect ASC 606. For an agency, it may mean adjusting for owner compensation, earnout terms, or debt service coverage definitions that do not match GAAP presentation. For e-commerce businesses, inventory financing, seasonal working capital swings, and related-party support can change covenant headroom fast.

A covenant worksheet should include the exact formula from the agreement, the source data, the calculation, and sign-off. If you needed a waiver or amendment, file that correspondence with the schedule. Do not leave it in someone's inbox.

What auditors will expect to see

Auditors test more than ending balances. They test whether the legal terms support classification, valuation, presentation, and disclosure.

That means your file should answer practical questions quickly:

- What debt instruments were outstanding during the year, and what changed

- Which instruments are current versus long-term, and why

- Whether any covenant breach occurred, even briefly

- How SAFEs, convertible notes, warrants, or preferred returns were evaluated under the applicable accounting guidance

- Whether stock option grants tie to board approval dates, valuation support, and expense recognition

- Whether founder or related-party loans have documented terms, stated interest, and a clear repayment history

One clean file lowers audit hours. It also speeds diligence when you raise money. Investors and lenders lose confidence fast when finance, legal, and the cap table tell different stories.

If you have unusual rights such as liquidation preferences, redemption clauses, conversion triggers, or side letters, write a short memo in plain English that explains the economics and the accounting conclusion. That memo saves time, reduces back-and-forth, and prevents inconsistent answers from the CEO, controller, and outside counsel.

7. Compile Supporting Documentation for Complex or Non-Routine Transactions

Most audits don't get delayed by rent, payroll, or standard customer invoices. They get delayed by one-off transactions no one documented properly.

That could be a contract modification with a major customer. A financing round. A founder loan conversion. A related-party transaction. A lease modification. A business acquisition. A large legal settlement. A software impairment. The accounting may be correct, but if the support is fragmented, the auditor will keep pulling the thread.

One unusual transaction can stall the audit

Every non-routine transaction should have a dedicated folder and a short summary sheet. Include what happened, when it happened, who approved it, why it happened, how it was accounted for, and where the support sits.

A SaaS company that changed the commercial terms on a major enterprise contract should preserve the original contract, amendment, billing impact, and revenue memo. A digital agency that sold equipment or exited an office lease should keep the disposal support, approval trail, and accounting entry analysis together. A company that issued equity as part of compensation should tie the arrangement to legal documentation and approval.

Use a transaction memo not a loose email trail

Founders often assume “we have the emails” is enough. It isn't. Your accounting team needs a defensible memo that summarizes the transaction and points to the evidence.

- State the business purpose clearly: Why did management approve the transaction?

- Capture the accounting judgment: What treatment was used, and why?

- Preserve approval evidence: Board consent, executive approval, or signed agreement should be easy to locate.

- Archive calculations: If the entry involved an estimate or allocation, keep the working papers.

One of the biggest gains here is speed. When a non-routine transaction is documented contemporaneously, the audit request becomes retrieval. When it isn't, the audit request becomes a forensic exercise across email, legal files, and memory.

8. Schedule Internal Control Assessment and Documentation Review

Weak internal controls raise audit fees, slow fundraising, and create expensive clean-up work after year-end. Founders who treat controls like paperwork usually pay for it twice. First in longer audit fieldwork, then in credibility loss when investors or lenders spot preventable process gaps.

This part of the audit preparation checklist should focus on how money moves, who can approve it, who can change records, and what evidence exists after the fact. Auditors are not just checking whether the numbers tie out. They are testing whether your process can produce reliable numbers again next month without founder intervention.

For SaaS, agency, and e-commerce companies, the highest-value controls usually sit around revenue, cash, disbursements, and system access. A SaaS business needs clear approval and review over contract changes, pricing exceptions, credits, and revenue schedules under ASC 606. An agency needs documented review of project accruals, pass-through costs, and client billing adjustments. An e-commerce company needs tight controls over refunds, processor reconciliations, inventory adjustments, and user access across storefront, ERP, and payment tools.

Document the control, the owner, and the evidence

Write down who performs each control, how often it happens, what they review, and what proof remains. If there is no evidence, auditors often treat the control as if it never happened.

Cover the controls that move audit timing and risk:

- Cash controls: Bank reconciliations, wire approvals, new vendor setup, and changes to payment instructions

- Close controls: Journal entry review, month-end checklists, account reconciliation sign-off, and consolidation review

- Revenue controls: Contract approval, billing change review, credit memo approval, and deferred revenue rollforward review

- Access controls: Who can add vendors, post entries, issue refunds, change customer terms, or edit revenue data

- Payroll and spend controls: New hire approval, payroll change review, expense reimbursement approval, and bonus authorization

Small teams rarely have perfect segregation of duties. Document the compensating review instead. If one person prepares and posts an entry, another person should review the output and sign off. If the founder approves wires, someone else should build the payment batch and maintain the vendor file. If your team needs a practical primer, start with this guide to segregation of duties in finance operations.

Test the controls before auditors do

A documented control that fails in practice still creates delays. Pull samples yourself. Check whether approvals were retained, whether reviews happened on time, and whether system access matches current job responsibilities.

This step pays off fast. Catching one broken approval flow in July is cheap. Discovering during fieldwork that six months of billing overrides lacked review can trigger expanded testing, more audit requests, and rework across finance, sales ops, and engineering.

Treat audit findings like operating issues

Post-audit remediation belongs here because weak controls do not stay contained inside the audit. They spill into forecasting, board reporting, collections, and fundraising diligence.

Assign each control gap to an owner. Set a deadline. Define the evidence required to prove the fix is working. Then retest it. A closed finding without proof is still a live risk.

Good control documentation cuts audit friction. Good control execution cuts business risk. You need both.

8-Point Audit Prep Checklist Comparison

| Task | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes ⭐ | Ideal Use Cases 📊 | Key Advantages & Tips 💡 |

|---|---|---|---|---|---|

| Organize and Reconcile All Bank and Credit Card Accounts | High, detailed, frequent tie‑outs and processor matching | Moderate→High, reconciliation tools, bank/processor access, staff time | ⭐⭐⭐⭐, clean cash balances; fewer audit adjustments | E‑commerce, SaaS, agencies with multiple payment processors | Automate feeds; reconcile monthly; document reconciling items |

| Complete Revenue Recognition and ASC 606 Compliance Review | Very High, contract‑by‑contract technical analysis | High, ASC 606 expertise, contract review, subscription systems | ⭐⭐⭐⭐⭐, GAAP compliance; reduced revenue risk in audit | SaaS, subscription, usage‑based or multi‑period contracts | Implement ASC 606 workflows; maintain revenue policy and contract memos |

| Prepare and Verify Fixed Assets Schedule with Depreciation | Medium, requires historical tracking and lease accounting | Moderate, asset registry, depreciation tool, physical counts | ⭐⭐⭐⭐, accurate PP&E, depreciation and disclosures | Manufacturing, software capitalizing dev costs, agencies with build‑outs | Use asset software; perform annual counts; keep capitalization policy |

| Document and Test All Journal Entries (Especially Manual and Consolidating Entries) | High, exhaustive entry documentation and approvals | Moderate→High, time, approval workflows, centralized register | ⭐⭐⭐⭐, strong control evidence; fewer audit findings | Businesses with many manual adjustments or multi‑entity consolidations | Use templates; two‑approver thresholds; centralize support links |

| Reconcile All Balance Sheet Accounts (Especially Payroll Liabilities and Accruals) | High, many accounts and system tie‑outs required | High, access to payroll, inventory, subscription and GL reports | ⭐⭐⭐⭐, validated balances; reduced audit scope | Companies with payroll liabilities, inventory, unbilled revenue | Create monthly templates; automate payroll imports; document allowances |

| Prepare Debt and Equity Schedule with Covenant Compliance Documentation | Medium‑High, legal review and covenant modeling | Moderate, loan docs, cap table tools, financial modeling | ⭐⭐⭐⭐, proven covenant compliance and transparent cap table | Borrowed firms, VC‑backed, PE‑owned, fundraising candidates | Maintain master schedule; track covenant metrics monthly; summarize terms |

| Compile Supporting Documentation for Complex or Non‑Routine Transactions | Medium‑High, judgment and document aggregation | Moderate, management input, contracts, transaction memos | ⭐⭐⭐⭐, efficient audit testing of significant items | Acquisitions, asset sales, related‑party deals, contract modifications | Prepare transaction summary sheets and accounting memos; centralize docs |

| Schedule Internal Control Assessment and Documentation Review | High, enterprise‑wide mapping and testing of controls | High, cross‑functional time, IT evidence, control testing tools | ⭐⭐⭐⭐⭐, stronger governance; reduced audit testing and risk | Pre‑SOC2, investor/lender readiness, growing operational complexity | Map to COSO/SOC2; document roles/frequency; gather execution evidence |

Turn Your Audit from a Liability into an Asset

A strong audit preparation checklist changes more than audit week. It changes how your company runs. You close faster. You answer diligence questions faster. You defend your numbers with less founder involvement. And when a lender, investor, or buyer asks for support, your team retrieves it instead of rebuilding it.

That's the payoff. Audit readiness reduces friction across the entire finance function. Cash reconciliations become part of the monthly close instead of a year-end emergency. Revenue recognition becomes a documented policy instead of a debate driven by whoever knows the deal best. Balance sheet accounts stop accumulating mystery balances. Debt and equity records stop living in legal inboxes. Complex transactions stop turning into last-minute accounting memos built under pressure.

There's also a management benefit founders often underestimate. Once you impose structure on reconciliations, journal entries, controls, and supporting schedules, you start seeing the business more clearly. You spot stale accruals. You catch broken billing logic. You identify contract terms that create accounting risk. You find approval gaps around spend, access, and cash movement. Those aren't audit problems. Those are operating problems, and the audit just happens to expose them.

If you're preparing for your first audit, don't run this as a side project owned by one overextended bookkeeper or controller. Assign owners by workstream. Set deadlines by month, not by audit request. Build one evidence index. Standardize file naming. Link each major support file to the underlying balance, policy, or control. The businesses that handle audits well don't necessarily have larger teams. They have tighter systems.

There's another shift worth making. Stop thinking of the audit as an annual event. The strongest readiness processes now treat audit support as an ongoing discipline. Monthly reconciliations, indexed support, version control, and documented controls shorten the audit because the evidence already exists in usable form. You're not creating readiness during the audit. You're proving that your finance function was ready before the auditor arrived.

If this feels overwhelming, take that as a useful signal. Your business has likely outgrown DIY finance habits. That's common in the revenue range where companies move from founder-led accounting to investor-grade reporting. The answer isn't to work harder every year-end. The answer is to put a repeatable close and documentation system in place.

Jumpstart Partners is one relevant option for companies that need outsourced controller and bookkeeping support built around audit-ready reporting. Their services are focused on growing businesses, including SaaS, agencies, and other companies that need stronger reconciliations, revenue workflows, and month-end discipline. If your team needs help turning this checklist into a repeatable process, get support before the audit calendar forces the issue.

If you want a finance function that closes cleanly, supports ASC 606, and stays ready for diligence year-round, talk to Jumpstart Partners. They work with growing companies that need outsourced controller support, better reconciliations, and audit-ready financials without building a full in-house team first.