Financial Operations

Intercompany Elimination: A Founder's Guide for 2026

Master intercompany elimination for accurate financials. Our guide covers journal entries, reconciliation, and pitfalls for SaaS & agency founders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readMost founders assume intercompany elimination is a cleanup step for larger companies. It isn't. The bigger surprise is where significant damage emerges. It's often not the obvious receivable and payable mismatch. It's the CTA elimination mismatch, where FX retranslation exposes balances that never matched in the first place. RSM expert Peggy Evleth calls large Cumulative Translation Adjustment eliminations a “canary in the coal mine” for flawed intercompany balances, a warning many teams miss until close is already off track (Peggy Evleth discussion on CTA mismatch).

If you run a parent entity plus one or more subsidiaries, your consolidated numbers aren't reliable unless you eliminate internal activity correctly. That matters whether you're raising capital, reviewing segment profitability, or just trying to trust your monthly P&L.

Table of Contents

- Why Your Consolidated Financials Are Wrong Without Elimination

- The Four Essential Intercompany Elimination Entries

- Your Month-End Workflow for Flawless Eliminations

- Red Flags That Will Wreck Your Intercompany Eliminations

- Automating Eliminations in Your Accounting Software

- Take Control of Your Consolidated Financials

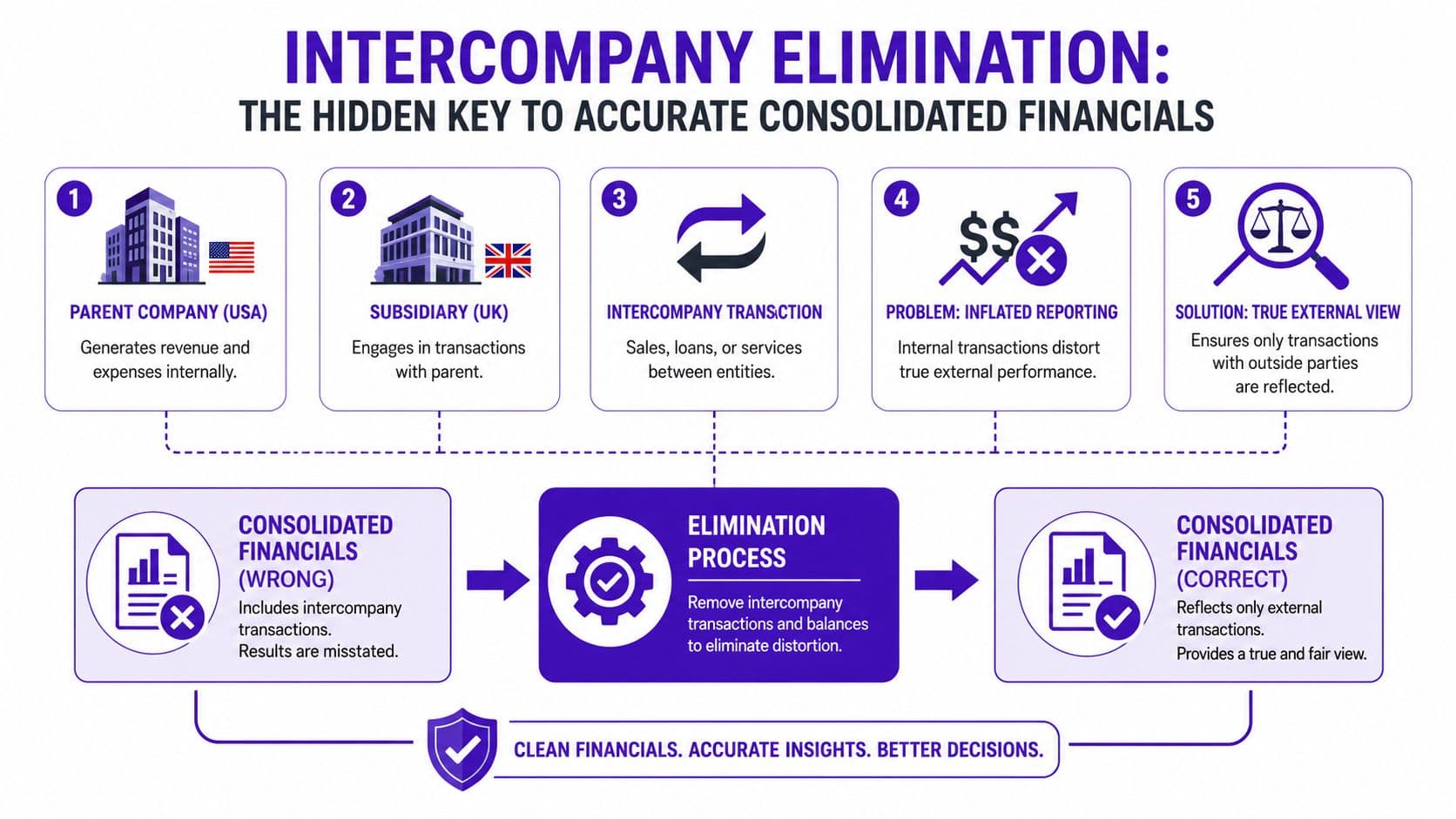

Why Your Consolidated Financials Are Wrong Without Elimination

Consolidated financials without intercompany elimination are misstated. The overstatement is not theoretical. It can change reported revenue, margin, working capital, and entity-level performance enough to mislead management, lenders, and auditors.

At group level, your companies are one economic unit. A charge from the US parent to the UK subsidiary may be valid on each entity's local books, but it is not third-party revenue for the group. Leave it in consolidation and you create fake activity.

What gets distorted

Use a simple example. Parent bills Subsidiary $100 for shared services. If that entry stays in the consolidated results, group revenue is overstated by $100 and group expense includes internal activity that says nothing about customer demand or operating efficiency.

That is the basic error. The harder problem is what sits underneath it.

In multi-currency groups, the intercompany receivable and payable often do not match after FX retranslation, even when the underlying transaction was posted correctly in both entities. One side is remeasured in USD, the other in GBP or EUR, and part of the movement lands in cumulative translation adjustment, or CTA, at consolidation. If you only compare due-to and due-from balances and force them to zero, you can leave a CTA elimination mismatch behind. I see this often in fast-growing groups with a US parent and foreign subsidiaries. The teams think intercompany is reconciled because the invoice matches, but consolidated equity and FX movement still look wrong.

That matters because founders usually review the consolidated P&L first. If those numbers include internal sales, mismatched FX effects, or both, reported profitability stops being a reliable management tool. A clean consolidated profit and loss statement should show what the group earned from external customers, not what one legal entity charged another.

Why founders should care

This affects real decisions every month:

- Pricing: Internal markups can make one subsidiary look unprofitable when the group is fine.

- Hiring: Inflated gross margin can lead you to add headcount before the business supports it.

- Cash planning: Unreconciled intercompany balances can hide settlement problems between entities.

- Investor and lender reporting: Diligence teams test whether consolidated numbers exclude intra-group activity and whether FX treatment is consistent.

- Audit readiness: Weak elimination support is a common sign that the close process is not controlled.

I have seen a group report stronger margins for two quarters because internal technology recharges were left in revenue. The board thought the business model was improving. It was not. The improvement disappeared once the elimination entries were posted correctly.

A Critical Point on Ownership

Partial ownership does not change the elimination requirement. If the parent owns 80% of a subsidiary, intercompany revenue between those entities is still eliminated in full in consolidation. Non-controlling interest affects how equity and net income are allocated after consolidation. It does not convert an internal sale into external revenue.

That distinction is where many teams go wrong. They learn the basic receivable and payable match, but miss the higher-risk areas: unrealized profit in inventory, intercompany loans with interest, and CTA mismatches caused by FX retranslation. Those are the issues that turn a routine close into an audit finding.

The Four Essential Intercompany Elimination Entries

Most service businesses and SaaS groups don't deal with exotic elimination scenarios every month. They deal with a handful of recurring patterns. Get these four right and your close gets far more predictable.

The standard operating method starts with dedicated intercompany account codes such as IC-SALE or IC-LOAN, then matching and reconciling balances before posting elimination entries in the consolidation layer (Intuit Enterprise on intercompany identification and matching).

Intercompany revenue and expense

This is the most common entry. A parent company charges a subsidiary a management fee, shared payroll cost, or software allocation.

Assume Parent bills Subsidiary $10,000 for management support.

On the separate books:

- Parent records $10,000 revenue

- Subsidiary records $10,000 expense

On consolidation, both sides must disappear.

Sample Intercompany Revenue Elimination

| Account | Debit | Credit |

|---|---|---|

| Intercompany Revenue | $10,000 | |

| Intercompany Expense | $10,000 |

This entry removes internal activity from the consolidated P&L.

A common mistake is eliminating only one side because one entity posted it in a different account. That's why standardized account mapping matters more than many realize.

Intercompany loans and interest

Founders often fund a new entity through a related-party loan. On standalone books, that's fine. On consolidated books, the group can't owe money to itself.

Assume Parent lends Subsidiary $50,000. At month-end:

- Parent shows Intercompany Note Receivable $50,000

- Subsidiary shows Intercompany Note Payable $50,000

The balance sheet elimination is:

| Account | Debit | Credit |

|---|---|---|

| Intercompany Note Payable | $50,000 | |

| Intercompany Note Receivable | $50,000 |

If Parent also records $2,000 of interest income and Subsidiary records $2,000 of interest expense, eliminate that from the P&L too:

| Account | Debit | Credit |

|---|---|---|

| Interest Income Intercompany | $2,000 | |

| Interest Expense Intercompany | $2,000 |

Unrealized profit in intercompany work

Service companies miss this when one entity performs work for another that hasn't been recognized externally in substance.

Assume Entity A performs internal implementation work for Entity B and invoices $12,000. Entity A's internal cost was $9,000, so $3,000 of profit sits inside the group. If the related value hasn't been realized with an outside customer at consolidation, that internal profit shouldn't remain.

First eliminate the full internal billing:

| Account | Debit | Credit |

|---|---|---|

| Intercompany Service Revenue | $12,000 | |

| Intercompany Service Expense | $12,000 |

Then remove the unrealized internal profit component:

| Account | Debit | Credit |

|---|---|---|

| Profit Adjustment or Retained Earnings Related Elimination | $3,000 | |

| Work in Process, Deferred Cost, or Related Asset | $3,000 |

The exact accounts depend on where the internal value sits. The key point is operational. If profit exists only because one entity billed another inside the group, that profit isn't consolidated profit yet.

Teams get this wrong when they treat every internal invoice as harmless. It isn't harmless once it affects margin reporting.

Intercompany dividends

A dividend paid by one group entity to another is not group income. It's an internal equity movement.

Assume Subsidiary declares and pays Parent a $8,000 dividend.

On separate books:

- Parent records dividend income $8,000

- Subsidiary reduces equity or records dividend declared $8,000

On consolidation, eliminate the internal income effect:

| Account | Debit | Credit |

|---|---|---|

| Dividend Income | $8,000 | |

| Dividends Declared or Equity Distribution | $8,000 |

The practical takeaway

If your finance team can't answer these three questions quickly, intercompany elimination isn't controlled:

- Which accounts are designated as intercompany accounts

- Which entity is the counterparty for each balance

- Which entries post only in consolidation instead of local books

That discipline matters more than fancy templates.

Your Month-End Workflow for Flawless Eliminations

Strong intercompany elimination isn't built on heroic month-end catch-up. It runs on a routine your team follows every month.

Without elimination, internal transactions overstate the group's financial position by the full amount of those internal movements. Automation helps by matching transactions, flagging breaks, and generating recurring elimination entries faster than manual spreadsheets can (Nominal on why automation speeds intercompany eliminations).

Pre-close checks

Before the month ends, lock down structure.

- Use dedicated intercompany accounts: Don't bury related-party activity inside generic revenue, expense, receivable, or payable accounts.

- Standardize the chart of accounts: Parent and subsidiaries need aligned account logic or eliminations turn into mapping guesswork.

- Assign entity counterparties: Every intercompany entry should identify who the other side is.

- Set a monthly cutoff policy: Both entities need the same close calendar.

If your current process is still spreadsheet-heavy, these controls pair well with broader month-end close best practices, especially for multi-entity teams trying to shorten review cycles.

Reconciliation routine

At this juncture, the close either stays clean or goes sideways.

Match intercompany balances early, not after the consolidated financials are drafted. The workflow described by Intuit includes identifying transactions with unique account codes, reconciling balances across entities, and logging disputes so a designated finance lead settles them quickly. In practice, that means you should review:

- Receivables versus payables

- Loan balances and accrued interest

- Management fees and shared cost allocations

- Intercompany billings tied to projects or inventory-like balances

- Foreign currency balances before and after translation

A simple operating rule helps. If one side posts an intercompany entry, the other side should be visible and reconcilable the same close cycle.

Operational test: If your team is still discovering old intercompany mismatches during final review, your process starts too late.

Posting and review

Elimination entries belong in the consolidation layer, not in the underlying legal entity books. That distinction matters because each legal entity still needs correct standalone records for tax, statutory, and management purposes.

After posting eliminations, review the consolidated statements with targeted questions:

| Review area | What you're checking |

|---|---|

| Revenue | No internal sales or fees remain |

| Expenses | Shared charges don't survive as group expense if they only moved inside the group |

| Balance sheet | Intercompany receivables, payables, and loans net to zero |

| Equity | Internal dividends and stock-related balances are removed |

| FX impact | Translation effects don't hide unresolved intercompany mismatches |

Documentation matters too. Archive the reconciliation support, elimination journal logic, and reviewer signoff each month. That's what keeps a clean process from falling apart when auditors, lenders, or new finance hires start asking questions.

Red Flags That Will Wreck Your Intercompany Eliminations

Bad eliminations do more than create messy workpapers. They distort segment profitability, hide broken processes, and can turn a clean audit into a long argument about balances your team should have resolved before close.

The CTA mismatch black hole

This is the red flag that catches growing multi-entity groups off guard.

A parent and subsidiary can match perfectly in local currency and still fail at consolidation because FX retranslation changes the reported balance on one side. I see this most often when teams assume intercompany elimination is just receivables versus payables. It is not. The harder problem is proving the balance still clears after translation and that any CTA movement is real, not a plug covering bad intercompany accounting.

As Peggy Evleth notes earlier in the article, unusually large CTA elimination entries are often a warning sign, not harmless noise.

Symptom: the receivable and payable agree in local books, but the consolidation produces an unexplained CTA difference or a recurring FX plug.

Root cause:

- One entity booked the transaction in a different period

- The entities used different exchange rates or remeasurement logic

- Partial settlements and old balances were never cleared cleanly

- Rounding and manual top-side entries built up over several closes

Immediate fix:

- Reconcile by entity pair, currency, and transaction date

- Tie the opening balance, current activity, settlements, and ending balance

- Confirm both entities are using the same FX policy for the same transaction type

- Break out true translation movement from posting errors before you book the elimination

If you skip that work, the consolidated statements may still tie mathematically. They will not be reliable.

Unreconciled balances that keep rolling forward

A difference that survives month after month is not temporary. It is an unresolved accounting issue.

The usual pattern is familiar. One team carries a balance as "timing." Another team assumes the other side will clear it next month. Six months later, the group has a reconciliation file full of stale items and no clear owner.

Symptom: your close package includes old intercompany differences that reappear every month.

Root cause: missing counterparty coding, inconsistent entity names, cut-off errors, unsupported manual journals, or no deadline for resolution.

Immediate fix:

- Set a monthly aging review for all intercompany balances

- Require every intercompany entry to include the legal entity counterparty

- Assign one person to investigate and resolve breaks

- Put old items on an escalation list with a due date, not a parking lot tab

This is also a control problem. Strong review workflows and clear segregation of duties reduce the chance that unsupported entries get posted and then carried forward.

Internal profit that inflates project margin

Service groups miss this one because there is no physical inventory to remind them profit may still be unrealized.

If Entity A bills Entity B for internal project work at a markup, that markup can sit inside deferred costs, work in process, capitalized implementation spend, or project-based assets. At the entity level, the margin looks real. At the group level, it is not earned until the customer pays for it externally.

Symptom: a business unit looks highly profitable on internal work while the consolidated margin does not make economic sense.

Root cause: intercompany service billings include markup, and nobody reviews whether that markup remains embedded in an asset or deferred balance at month-end.

Immediate fix:

- Tag intercompany project charges with separate account codes

- Identify assets and deferred balances that include internal markup

- Eliminate the internal profit until the group realizes it through an external transaction

This issue matters because it changes management decisions. Founders start backing the wrong business line when internal margin is left in the numbers.

Inconsistent accounting policies across entities

Clean trial balances do not guarantee a clean consolidation.

A parent can book a management fee to one account, the subsidiary can record the offset in a different section of the P&L, and both teams can insist their books are correct. They may be right at the entity level and still create a bad elimination result at the group level. Upflow highlights inconsistent policies, fragmented systems, and weak governance as common intercompany accounting failure points (Upflow on common pitfalls and leading practices in intercompany accounting).

Symptom: balances exist on both sides, but the elimination entry requires too much manual reclassing to make the statements present correctly.

Root cause: different charts of accounts, inconsistent markup policies, uneven close calendars, and entity-specific workarounds that never got standardized.

Immediate fix:

- Standardize the chart of accounts where possible

- Write one intercompany accounting policy and use it across entities

- Align cut-off rules, pricing logic, and account mapping

- Review exceptions monthly instead of fixing presentation at year-end

The practical test is simple. If your team needs a custom explanation every month for why an intercompany balance did not eliminate cleanly, the process is broken.

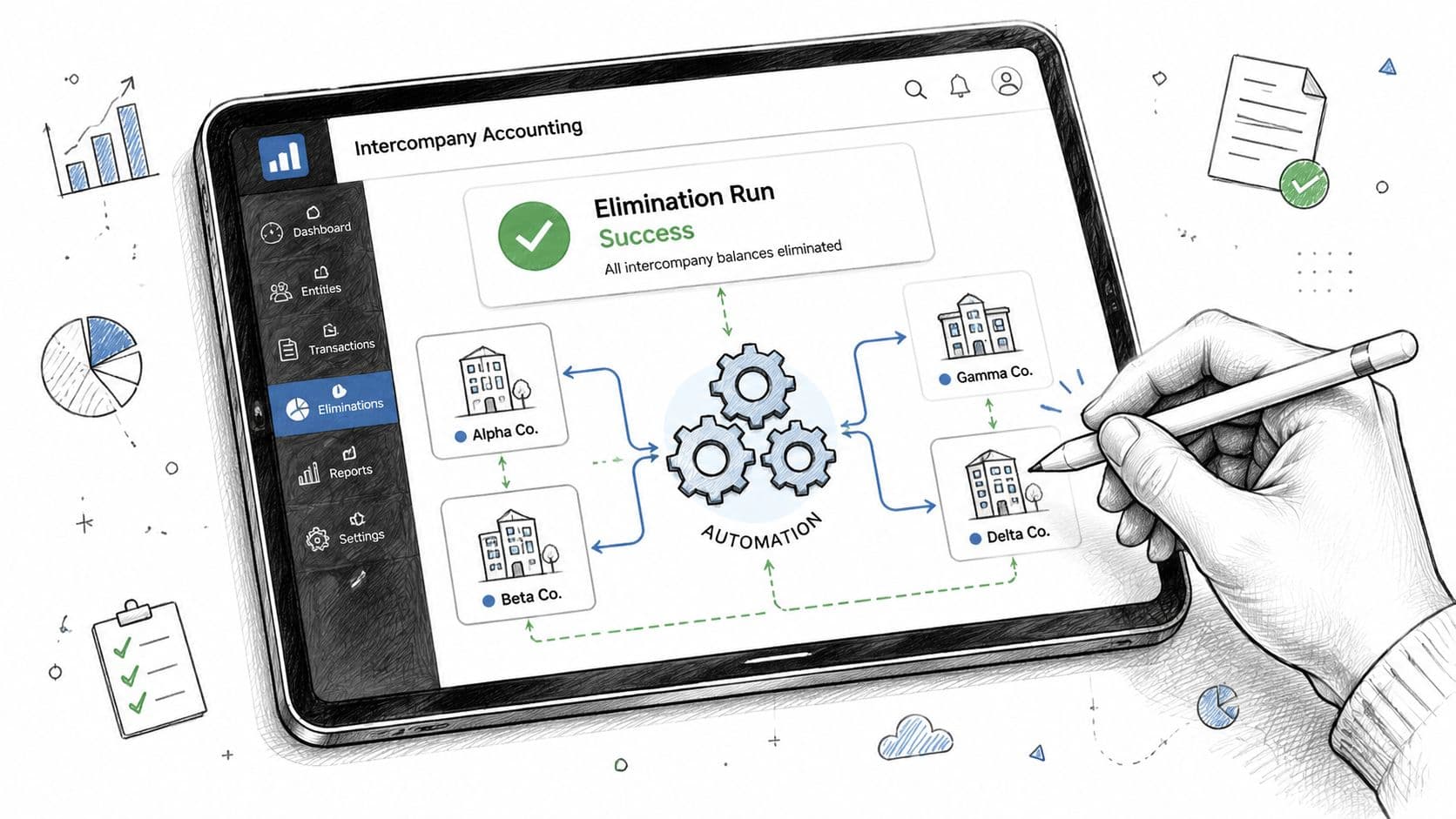

Automating Eliminations in Your Accounting Software

Software doesn't replace accounting judgment. It does remove a lot of avoidable manual friction.

QuickBooks Online and Xero

For many businesses in the $500K to $20M range, QuickBooks Online or Xero is still the operating system of finance. Both can support disciplined intercompany accounting at the entity level, but neither gives you a true native multi-entity consolidation engine.

That means the usual workaround looks like this:

| Platform | What works | Where it breaks |

|---|---|---|

| QuickBooks Online | Separate files per entity, disciplined intercompany accounts, export to consolidation workbook | Manual elimination entries, fragile spreadsheets, review bottlenecks |

| Xero | Similar entity-by-entity control, strong basic bookkeeping workflows | No native consolidated elimination layer, difficult scaling across entities |

| Add-ons like Fathom or Spotlight | Better management reporting and consolidated views | Still depends on clean underlying intercompany setup and manual policy discipline |

For smaller groups, that can be enough if you also invest in financial reporting automation around exports, mappings, and close checklists.

NetSuite OneWorld

NetSuite OneWorld is the more integrated answer once complexity grows. It's built for multi-entity operations, which means intercompany workflows, account mapping, consolidation logic, and approvals can sit inside one system instead of being stitched together across spreadsheets.

That matters when your pain points include inconsistent reporting formats, uneven pricing policies, and month-end bunching. The stronger practice is a centralized ERP with standardized charts of accounts and a continuous close approach, where intercompany work gets handled throughout the month instead of all at once at the end.

Here's a quick product walkthrough to frame what automated intercompany workflows look like in practice.

What automation should actually do

Don't buy software because it says “multi-entity.” Buy it if it does these jobs well:

- Matches counterparties reliably

- Flags breaks before final consolidation

- Supports entity and currency-level review

- Posts elimination entries in a separate consolidation layer

- Leaves a clean audit trail

If your team still has to rebuild intercompany logic manually every month, the software isn't solving the underlying problem.

Take Control of Your Consolidated Financials

Intercompany elimination is one of those finance processes that looks technical but drives basic business clarity. You need it so your revenue isn't inflated by internal activity, your margins reflect real outside performance, and your close doesn't unravel under audit or investor review.

The good news is that the process is manageable when the structure is right. Dedicated intercompany accounts, a repeatable reconciliation routine, proper consolidation-layer entries, and attention to FX-related mismatch risk will get you most of the way there. If you run more than one entity, that discipline is part of operating a serious finance function.

For founders who are already dealing with multiple entities, shared services, cross-border operations, or messy consolidation workbooks, it helps to step back and rebuild the process before the next raise, lender review, or audit. A strong multi-entity accounting setup gives you cleaner reporting and better decisions every month, not just cleaner year-end files.

The objective isn't just compliance. It's confidence. You should be able to look at a consolidated P&L and know it reflects the business you run.

If your team is wrestling with intercompany elimination, messy consolidations, or unreliable month-end reporting, Jumpstart Partners can help you build a cleaner, audit-ready close process. Their outsourced controller team works with growing SaaS, agency, and professional services businesses to tighten multi-entity accounting, improve reporting accuracy, and give founders financials they can trust.