Financial Operations

Consolidated Profit and Loss Statement for SaaS Leaders

Consolidated profit and loss statement - Master your consolidated profit and loss statement for SaaS success in 2026. Unlock key financial insights and drive gr

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··23 min readYou close the month. Revenue looks strong in one entity, margins look weak in another, and your board deck tells three different stories depending on which P&L someone opens first.

That’s where founders get into trouble.

If you run a SaaS company, agency, or services firm with more than one legal entity, a consolidated profit and loss statement is not a nicer version of reporting. It’s the only version that shows how the business performed as a group. Without it, intercompany billings can inflate revenue, shared costs can get counted twice, and minority ownership can make your profit look lower than your operating team expects.

Most explanations stop at “combine the statements and eliminate intercompany activity.” That’s not enough for operators. You need to know what gets removed, what stays, why investors care, and where SaaS businesses usually misstate performance.

Introduction to Consolidation Risks

A familiar scenario shows up during fundraising.

You’ve built a parent company and added one or two subsidiaries. One entity owns the product. Another employs the team. A third handles a regional market or an acquired service line. Internally, that structure makes sense. Externally, it creates reporting noise.

Your sales entity charges the operating entity. The parent bills a subsidiary for shared leadership time. One subsidiary recognizes revenue, another carries the support payroll. If you hand investors separate P&Ls, they won’t see one company. They’ll see fragmented economics.

That’s dangerous because investors price clarity. Lenders do too. Auditors absolutely do.

A consolidated profit and loss statement fixes that by treating the group like one business. It strips out transactions that happened inside your own structure and leaves only the financial result from real activity with customers, vendors, and outside stakeholders.

Practical rule: If money moved from one entity you control to another entity you control, that movement should not make the group look bigger or more profitable.

The risk isn’t abstract. The history of consolidation rules comes from exactly this problem. The consolidated P&L became a cornerstone of reporting in the twentieth century, formalized by AICPA’s Accounting Research Bulletin No. 43 in 1953 and reinforced by FASB Statement No. 94 in 1987 to require consolidation for majority-owned subsidiaries, as summarized by Centage’s overview of consolidated P&L statements.

If you’re preparing for diligence, debt, or a board process, fragmented reporting slows everything down. A clean consolidated view gives you one set of margins, one operating story, and one defensible answer when someone asks, “What did the business earn?”

Understanding the Key Concepts

A consolidated profit and loss statement shows the income and expenses of a parent company and its controlled subsidiaries as one set of results.

That definition sounds simple. The confusion starts when founders try to decide what belongs in that single view, what must come back out, and why a group can be profitable at the operating level while the parent’s share of profit is smaller than expected.

At a practical level, consolidation answers one question: what did the business group earn from the outside world?

What gets combined

You combine the parent and every entity it controls. Revenue comes in. Expenses come in. Gains and losses come in. Then you remove activity that happened only inside the group.

That last step is where hidden errors creep in.

In SaaS, one entity may sell the customer contract, another may deliver onboarding, and a third may invoice for shared engineering or support. If you add each entity’s P&L together, internal charges can inflate revenue, overstate costs, or both. A bundle sold to one customer can appear to create revenue twice if the internal recharges are left in the group numbers.

Clean consolidation starts with clean books. A consistent general ledger structure across entities makes it much easier to identify internal billings, shared cost allocations, and duplicate revenue lines before they distort the final statement.

Why founders get confused

The hard part is not the math. It is separating ownership, control, and economics.

A legal entity can have its own bank account, contracts, and local P&L. Investors still want a group view if the parent controls that entity. They are evaluating one economic engine, not a folder full of entity reports.

That usually means four things happen at once:

- Revenue and expenses from controlled subsidiaries are included in the group results.

- Intercompany sales, management fees, and cost recharges are eliminated.

- The consolidated total reflects the full performance of controlled entities, not just the parent’s ownership percentage.

- Profit may then be split between the parent and other owners if a subsidiary has minority investors.

The third and fourth points often get mixed up. Founders hear “we own 80%” and assume only 80% of the subsidiary’s revenue and expenses belong in consolidation. That is not how control-based consolidation works. If you control the subsidiary, you include 100% of its operating results, then show how much of the bottom line belongs to other owners.

Where non-controlling interest fits

Non-controlling interest, or NCI, is the share of a controlled subsidiary’s profit that belongs to someone other than the parent.

This matters a lot in PE-backed rollups. A platform company may own a controlling stake in several add-ons while leaving equity with local operators or rollover investors. The consolidated P&L still includes the full operating result of those entities. Then part of net income is allocated away from the parent.

Here is the clean way to read it:

- The business group earned the full subsidiary profit.

- The parent does not own all of that profit.

- The amount attributable to minority holders is shown separately.

A simple example helps. If a parent controls a subsidiary but owns only 80%, the consolidated P&L includes 100% of that subsidiary’s post-acquisition revenue and expense. After net income is calculated, 20% of that subsidiary’s profit is allocated to non-controlling interest, and 80% remains attributable to the parent.

That presentation can surprise a board member who sees strong operating performance but a lower "net income attributable to parent" line. The business did better. The parent just shares part of the earnings.

Why SaaS leaders need precision here

For software companies, consolidation is tightly linked to revenue recognition and package design.

A common trap looks like this: Subsidiary A signs the annual SaaS contract. Subsidiary B provides implementation. Subsidiary C supplies managed support. If A records the full customer invoice as revenue and B or C also book intercompany charges as revenue, the group can look larger than it really is unless those internal amounts are eliminated properly.

The same issue appears in bundled offers. A founder may believe the bundle economics are strong because each entity reports margin on its piece of the work. The consolidated P&L may show something very different after internal revenue is stripped out and shared delivery costs are lined up against the actual external contract value.

So the key concepts are straightforward, but the judgment behind them is not. Consolidation means combining controlled entities, removing internal activity, and showing clearly which profit belongs to the parent versus other owners. That is the foundation for every journal entry, elimination, and investor question that follows.

When You Need a Consolidated Report

Some leaders treat consolidation like a year-end exercise. That’s too late.

You need a consolidated report when external readers expect a group view, and when internal decisions depend on one version of truth.

The compliance trigger

If you control subsidiaries, consolidation moves from optional to expected under mainstream reporting frameworks. Public company rules have required consolidated reporting under SEC Regulation S-X since 1938, and IFRS 10 uses a control-based approach to determine when consolidation applies, based on the verified data summarized earlier.

For founders, the practical takeaway is straightforward. Once your structure includes parent and controlled subsidiaries, separate entity P&Ls are no longer enough for serious reporting.

The diligence trigger

Fundraising, acquisitions, and lender review all expose weak reporting fast.

A buyer or investor doesn’t want to reconstruct your business from separate files. They want a group-level statement that answers basic questions cleanly:

| Decision context | What they want to see | Why separate P&Ls fail |

|---|---|---|

| Fundraising | Group revenue and profit | Internal billings distort scale |

| Acquisition review | Combined operating performance | Shared costs sit in the wrong entity |

| Debt review | One view of recurring earnings | Legal entities hide cash generation |

| Board reporting | Comparable monthly trends | Different entity cutoffs confuse trends |

The management trigger

Even if no investor is asking yet, you still need consolidation when entity boundaries are starting to distort operating decisions.

That usually shows up in a few ways:

- Shared services blur margins because payroll sits in one company and customer revenue sits in another.

- Intercompany charges create fake growth when one entity bills another for support or implementation.

- Leaders debate the numbers instead of debating the business.

A founder should never have to ask, “Which P&L should I trust?” If that question exists, the reporting stack is already behind the business.

A simple decision test

Use this test at month-end.

- Do you control more than one entity? If yes, start from a consolidation mindset.

- Do entities sell, bill, lend, or transfer costs to each other? If yes, separate statements will mislead.

- Will an investor, lender, auditor, or buyer review your numbers? If yes, prepare the consolidated profit and loss statement before they ask.

If your legal structure has outgrown your reporting structure, consolidation becomes an operating necessity, not an accounting preference.

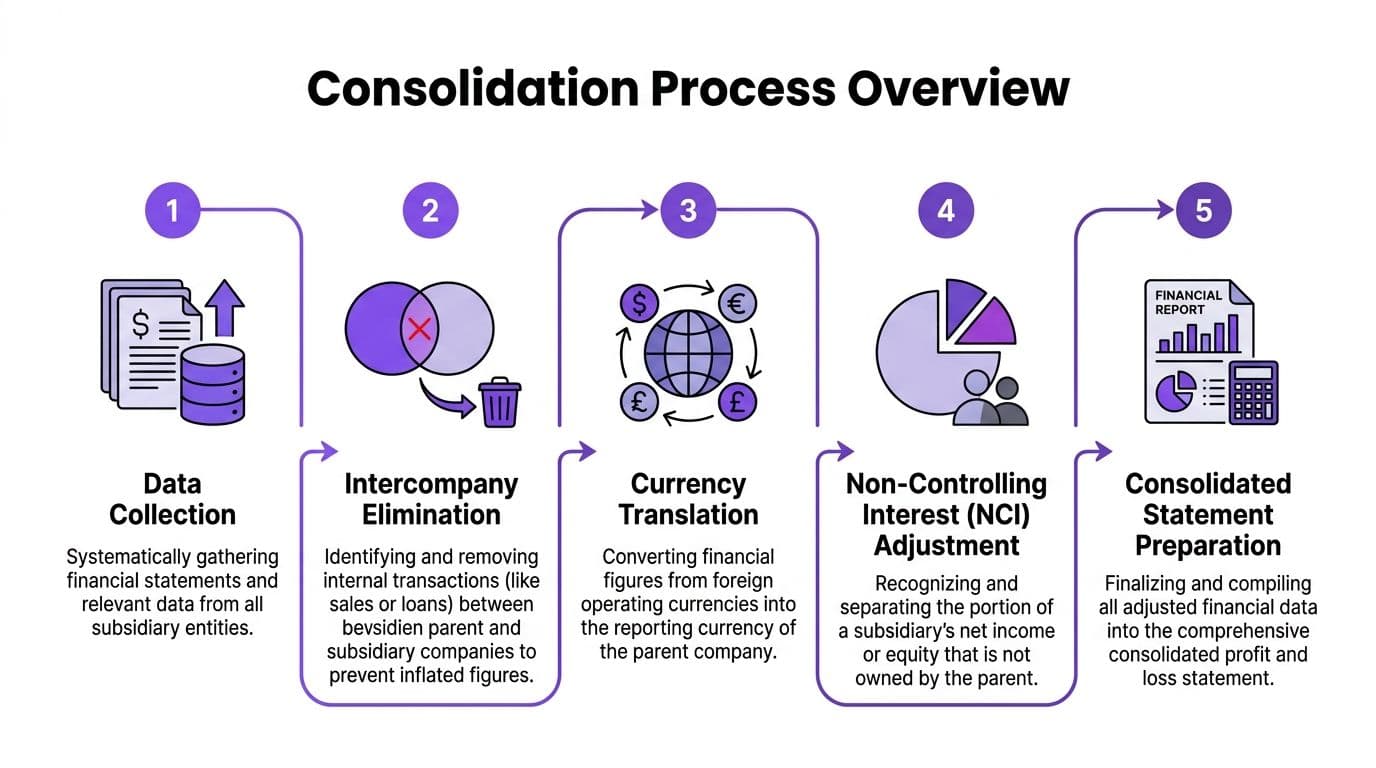

Consolidation Process Overview

A strong consolidated profit and loss statement comes from a repeatable workflow, not from copying and pasting trial balances into a spreadsheet.

Use this five-stage process.

Stage 1 data collection

Start with clean entity-level financials.

You need each entity’s trial balance, revenue recognition detail, intercompany accounts, and a consistent close date. If one subsidiary closes on a different basis or uses different account mapping, the combined report will be unreliable before you even begin.

For growing finance teams, automation begins to pay off. A systemized workflow for financial reporting automation reduces manual mapping errors and keeps entity reporting aligned.

A useful checklist for the collection stage:

- Use one chart logic: Different account names can still work, but the mapping to the group P&L has to be consistent.

- Lock the period: Don’t consolidate one entity on a draft close and another on a final close.

- Flag intercompany accounts early: Don’t wait until the end to figure out what was internal.

Stage 2 intercompany elimination

This is an often underestimated step.

Under IFRS 10 and IAS 27, intercompany sales, services, inventory transfers, dividends, and asset sales are fully eliminated so the report shows only external activity. A verified example from Sage’s explanation of consolidated financial statements shows the mechanics clearly: if the parent sells $500K of inventory to a subsidiary at a 20% markup, creating $100K of unrealized profit, the consolidated statements eliminate the $500K intercompany sale, reduce COGS by $400K, and defer the $100K profit until the inventory is sold to outside customers.

That example matters even if you don’t sell inventory. SaaS groups run into the same issue with internal implementation fees, support recharges, and shared service billings.

A plain-English example

Assume your parent company bills a subsidiary for internal engineering support.

- Parent records revenue.

- Subsidiary records expense.

- Group-wide, nothing was sold to a customer.

So in the consolidated profit and loss statement, both sides come out. If you leave them in, your group looks larger than it is.

Key takeaway: Internal revenue is not growth. It’s internal movement.

Here’s a simple elimination view:

| Item | Parent books | Subsidiary books | Consolidated result |

|---|---|---|---|

| Intercompany service revenue | Recognized | Eliminated | |

| Intercompany service expense | Recognized | Eliminated | |

| External customer revenue | Recognized | Recognized | Kept |

| External vendor expense | Recognized | Recognized | Kept |

Stage 3 currency translation

If one subsidiary operates in a different currency, you have to translate its results into the reporting currency of the parent.

The concept is easy. The execution is where teams slip. If one entity translates revenue one way and another translates expenses another way, the group P&L stops being comparable.

For founders, the practical discipline is to document one translation policy and apply it consistently each close. The exact rates and translation entries depend on your reporting framework and entity facts, but the operating principle is stable: one group report needs one reporting currency.

A short video explanation can help if you’re training a controller or new finance lead on the broader mechanics of consolidation:

Stage 4 non-controlling interest adjustment

If you own less than all of a subsidiary, the group still includes the full operating result of that subsidiary after acquisition, assuming control exists. Then you allocate part of that profit away from the parent.

The process has two parts:

- Include the subsidiary’s full post-acquisition revenue and expenses.

- Allocate the non-parent share of profit to NCI.

Investor communication often breaks down at this point. The business can improve operationally while “net income attributable to parent” moves less than expected because some of the earnings belong to minority holders.

Stage 5 consolidated statement preparation

After collection, eliminations, translation, and NCI allocation, you produce the final P&L.

That final statement should answer three things quickly:

- What did the group earn from external customers?

- What did it cost the group to deliver that work?

- How much profit belongs to the parent after minority allocations?

A workable month-end process usually looks like this:

| Stage | Main output | What to review |

|---|---|---|

| Data collection | Aligned trial balances | Missing mappings and late closes |

| Intercompany elimination | Removal entries | Internal revenue, expense, balances |

| Currency translation | Common reporting currency | Policy consistency |

| NCI adjustment | Parent vs minority profit split | Ownership and post-acquisition timing |

| Final prep | Consolidated P&L | Margin logic and board-readiness |

Done well, the process gives you one report you can operate from. Done poorly, it gives you a polished statement built on duplicated revenue and incomplete eliminations.

Sample Statements and Journal Entries

A founder sees consolidated revenue jump after an acquisition and assumes the group is selling more. Then diligence starts, internal bundle charges get stripped out, and the story changes fast.

Examples help prevent that mistake.

A consolidated profit and loss statement is only as reliable as the entries behind it, especially in SaaS groups that split delivery across entities and PE-backed rollups with minority owners. So let’s use a compact example that shows three pressure points many guides gloss over: full inclusion of a subsidiary’s operating results, removal of intercompany activity, and the profit split between the parent and non-controlling interest.

Example setup

Assume Parent owns 80% of Sub. Parent controls Sub, so Sub’s post-acquisition revenue and expenses appear in the consolidated P&L in full.

Sub generates:

- $2M of revenue

- $1.2M of expenses

- $800K of profit

The group includes all $2M of revenue and all $1.2M of expenses. After that, 20% of Sub’s profit, or $160K, is allocated to non-controlling interest. The remaining $640K is profit attributable to the parent.

If you want a quick refresher on how the income statement, balance sheet, and cash flow statement fit together before building the group view, this guide on how to prepare financial statements is a useful starting point.

What the consolidated P&L is actually saying

A good way to read this is to separate operating performance from ownership economics.

The business activity of Sub produced $800K of profit for the group before attribution. Ownership determines how much of that profit belongs to the parent versus outside holders.

| Line item | Amount |

|---|---|

| Subsidiary revenue included in consolidation | $2M |

| Subsidiary expenses included in consolidation | $1.2M |

| Subsidiary profit included before NCI allocation | $800K |

| NCI allocation at 20% | $160K |

| Profit attributable to parent from subsidiary | $640K |

That distinction trips people up in board meetings. The group earned $800K through Sub. Parent shareholders have a claim on $640K of it.

Journal entry logic

These entries usually sit in the consolidation worksheet, not in the legal entity books. That matters because you are adjusting the group view, not rewriting what Parent or Sub recorded on their own ledgers.

Entry 1. Include the subsidiary’s post-acquisition result

You pull in Sub’s revenue and expense lines line by line. You do not book one summary profit number.

That works like combining two department P&Ls into one company report. You want the full operating shape of the business to show up, not a single net line that hides where revenue came from or where costs sit.

Entry 2. Allocate non-controlling interest

Using the same facts:

- Subsidiary profit: $800K

- NCI ownership: 20%

- NCI share: $160K

A worksheet-style allocation can look like this:

| Consolidation adjustment | Debit | Credit |

|---|---|---|

| Net income attributable to NCI | $160K | |

| Non-controlling interest allocation | $160K |

System labels vary. The point does not. $160K of Sub’s profit belongs to minority holders, so it is presented separately from profit attributable to the parent.

For PE-backed groups, reporting often gets messy in these circumstances. Teams may fully consolidate the add-on acquisition, then underexplain why the bottom line available to the sponsor is lower than the operating result suggests.

Worked elimination example

Now add an intercompany transaction. This principle also applies to SaaS bundles, which can distort growth if finance treats internal cross-charges like customer revenue.

Assume Parent sold inventory to Sub for $500K at a 20% markup, so Parent recorded $100K of profit. Sub still holds the inventory at period end, which means the group has not sold it to an outside customer yet.

From the group’s perspective, that profit is still sitting on the shelf.

The consolidation entries remove the internal sale and defer the unrealized gain:

| Elimination effect | Amount |

|---|---|

| Reduce intercompany revenue | $500K |

| Reduce COGS by parent’s cost | $400K |

| Defer unrealized profit | $100K |

A simple worksheet entry looks like this:

| Consolidation adjustment | Debit | Credit |

|---|---|---|

| Intercompany revenue | $500K | |

| Cost of goods sold | $400K | |

| Inventory or unrealized profit reserve | $100K |

The logic is the same in a SaaS setting, even if the labels change. If one entity invoices another for onboarding, implementation, support, or bundled services, that internal charge cannot stay in consolidated revenue unless an outside customer bought it from the group. Otherwise, top line looks stronger than the business really is.

Why founders should care

These are not bookkeeping cosmetics.

Miss the NCI allocation and you overstate what belongs to parent shareholders. Miss the intercompany elimination and you inflate revenue or margin. Miss both, and your first investor readout may look healthy while your diligence version tells a weaker story.

That gap is avoidable.

Quick review questions before sign-off

Use these questions before you approve the consolidated P&L:

- Which subsidiaries were fully consolidated this period?

- Are the revenues shown here all external, or do any bundle-related intercompany charges remain?

- Was any unrealized profit deferred because the group had not completed a sale to an outside customer?

- How much profit was allocated to non-controlling interest, and what ownership percentages support that split?

- Can the team show the worksheet entries behind each material elimination?

If your finance lead can answer those questions cleanly, the statement is much closer to investor-ready.

Common Mistakes SaaS and PE Backed Firms Make

The biggest consolidation mistakes are rarely technical. They’re operational. Teams know the rule but skip the discipline.

Missing intercompany revenue hidden in SaaS bundles

SaaS groups often split the customer journey across entities. One company contracts with the customer. Another handles onboarding. A third provides support or managed services.

If those internal charges remain in the consolidated P&L, your top line gets inflated. The problem gets worse when bundle pricing makes it hard to see whether a charge was external or internal.

A practical screening tool during diligence is a broader technical due diligence checklist. It helps leadership teams surface structural issues that accounting review alone may miss, especially when revenue delivery spans multiple teams and systems.

Treating ASC 606 as an entity-level issue only

Revenue recognition has to hold together across the group, not just inside each legal entity.

If one entity defers implementation revenue and another recognizes a related internal recharge immediately, the consolidated P&L becomes inconsistent. This is one reason finance leaders need a solid grip on ASC 606 revenue recognition before they trust consolidated SaaS metrics.

Underexplaining minority interest to investors

This one creates unnecessary skepticism.

Verified research highlights a major blind spot: consolidated P&L statements often fail to explain NCI allocation clearly, and a 20% minority stake directly reduces parent-reported profit, which can mask operational improvements if founders don’t explain it well, as discussed in this analysis of non-controlling interest disclosure gaps.

If your operating profit improved but part of a subsidiary is minority-owned, your parent-attributable profit won’t move one-for-one. Investors need that bridge explained in plain English.

“The group earned the profit. Part of it belongs to minority holders.” That sentence prevents a lot of confusion.

Letting manual spreadsheets own the process

Spreadsheets are fine for analysis. They are weak control systems for recurring consolidation.

Formula drift, version confusion, and undocumented elimination entries create exactly the kind of issues that show up late in diligence. If your team relies on one heroic finance manager to remember every elimination each month, you don’t have a process. You have a vulnerability.

Ignoring review controls

A consolidation file without review evidence is a trust problem.

Use a simple close discipline:

- Match internal balances: Parent receivable must match subsidiary payable.

- Approve elimination entries: Someone other than the preparer should review them.

- Document ownership changes: New investors, option structures, or acquisition terms can change NCI treatment.

- Tie the narrative to the math: Board materials should explain why consolidated profit differs from entity-level profit.

- Keep support in one place: Diligence gets slower when backup lives in inboxes and side files.

Red flags

| Warning sign | What it usually means |

|---|---|

| Revenue rises sharply after adding entities | Intercompany activity may be sitting in top line |

| Entity margins look strong but group margins don’t | Shared costs may be misallocated or duplicated |

| Parent profit looks weaker than operators expect | NCI may be reducing attributable income |

| Month-end close depends on one spreadsheet owner | Control risk is high |

| Investors ask for reconciliations repeatedly | The group story isn’t clear enough |

Investor Ready Checklist and Tool Comparisons

An investor-ready consolidated profit and loss statement is accurate, explainable, and reproducible.

Use this checklist before any board meeting, financing process, or diligence request.

Five-point checklist

-

Validate entity data Confirm every entity has closed the same period and mapped accounts to the same group structure.

-

Review elimination entries Trace internal sales, service fees, loans, and dividends. Make sure internal activity does not survive in consolidated revenue or expense.

-

Confirm currency treatment Apply one translation policy across entities that report in different currencies.

-

Disclose NCI clearly Show the bridge from consolidated net income to net income attributable to parent whenever minority ownership exists.

-

Test revenue recognition across the group Make sure your ASC 606 logic works at the consolidated level, not just inside one entity.

For teams preparing a broader diligence package, this financial due diligence checklist is a practical companion.

Comparison of Consolidation Tools

You asked for tools, not abstractions. Here’s the operating view.

| Tool | Key Features | Cost | Best For |

|---|---|---|---|

| NetSuite | Multi-entity structure, native consolidation workflows, stronger control environment | Cost varies by configuration and license | Businesses with several entities and growing complexity |

| Sage Intacct | Solid multi-entity reporting, good finance controls, strong for structured closes | Cost varies by modules and implementation | Firms that want accounting depth without a full ERP footprint |

| Xero with apps | Simpler base ledger, can work with add-ons for multi-entity reporting | Cost varies by subscription and app stack | Smaller groups with lighter complexity |

| Manual Excel | Flexible and familiar, but control-heavy and person-dependent | Low software cost, high process risk | Temporary use only when structure is still simple |

How to choose

Choose based on failure risk, not software preference.

- If you have frequent intercompany activity, prioritize systems that support elimination workflows.

- If ownership is changing, choose tools that make NCI support easy to document.

- If your team is small, reduce manual dependencies before fundraising starts.

- If your board wants faster closes, favor systems that standardize mappings and review steps.

The right tool won’t fix bad accounting. It will make good accounting repeatable.

Conclusion and Next Steps

A consolidated profit and loss statement gives you the one number set that matters when your business spans multiple entities.

It removes internal noise. It shows group-level profitability. It explains why revenue, gross profit, and net income look different once your legal structure gets more complex. For SaaS leaders and PE-backed operators, that clarity affects fundraising, lender conversations, board trust, and close speed.

The biggest hidden issues are usually not in the headline totals. They sit in intercompany charges, deferred internal profit, and non-controlling interest allocations that no one explains clearly. Those are the spots investors notice first because they change the story behind the numbers.

If you’re tightening your finance stack, pair consolidation work with stronger operating planning. A resource like strategic financial planning can help leadership teams connect reporting discipline with growth decisions, especially when multiple entities are involved.

Your next move should be concrete:

- Review your entity structure against your current reporting pack.

- Identify every recurring intercompany transaction.

- Build a monthly elimination review.

- Add an explicit NCI explanation to investor and board materials.

- Move away from spreadsheet-only consolidation if the business has outgrown it.

A founder should be able to answer, with confidence, what the group earned, what it cost to earn it, and how much of that profit belongs to the parent. If your current reporting can’t do that, it’s time to fix the process.

If you want help building a cleaner consolidated close, Jumpstart Partners works with SaaS, agencies, and multi-entity businesses to produce investor-ready financials, strengthen month-end controls, and turn fragmented books into a reporting package your board can trust.