Financial Operations

Multi-Entity Accounting: Scale Your Business in 2026

Outgrowing QuickBooks? Master multi-entity accounting for consolidation, tooling, and workflows to scale your SaaS or agency in 2026.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readYou've added a second entity, maybe a foreign subsidiary, maybe a separate LLC for a new line of business, maybe a holdco-opco structure your lawyer insisted on. Your revenue is up, but your visibility is worse. Stripe shows one story, Gusto shows another, and your “consolidated” reporting lives in a spreadsheet that breaks every month.

That's the point where finance stops being bookkeeping and starts being infrastructure.

If your close drags on, if intercompany balances sit unresolved, and if you can't answer a basic question like “which entity has the cash,” your numbers aren't decision-grade. They're delay-grade. That's dangerous when you're hiring, fundraising, entering a new market, or trying to protect margin in a tighter environment.

A lot of founders treat this like a later-stage problem. It isn't. Once you operate across entities, you need a system designed for group reporting, not a patched-together extension of a single-company setup. If you're still using workflows better suited to a single-entry accounting system, you're already behind.

Table of Contents

- Your Spreadsheets Are Lying to You

- The Tipping Point for Multi-Entity Accounting

- Architecting Your Financial Foundation

- Mastering the Multi-Entity Month-End Close

- Choosing Your Multi-Entity Accounting Software

- Your Action Plan Migration and Outsourcing

- From Financial Chaos to Strategic Clarity

Your Spreadsheets Are Lying to You

The classic failure pattern looks like this. Your US entity closes first. Your UK subsidiary closes later. Someone exports trial balances, someone else maps accounts, then finance tries to net intercompany balances in Excel while operations asks for a clean P&L by brand, region, or product line.

You get reports. You just don't get trust.

That's the core issue with multi-entity accounting. The problem isn't that your team lacks effort. The problem is that spreadsheets don't enforce structure. They don't stop one entity from using a different account name for the same expense. They don't force due-to and due-from accounts to match. They don't tell you whether the group looks profitable because one entity billed another.

Your close process tells you whether finance is operating as a control system or a cleanup crew.

This hits SaaS, agencies, and services firms especially hard because your stack is fragmented by default. Stripe captures cash. Gusto handles payroll. Your CRM drives billing assumptions. Your accounting file lags behind all of it. Once you add more than one entity, every integration gap turns into a consolidation problem.

The result is predictable. Leadership starts making decisions from partial data. Hiring plans get approved without knowing which entity can fund them. Tax and compliance risk grows. Board materials turn into a reconciliation exercise instead of a strategic review.

The Tipping Point for Multi-Entity Accounting

At first, founders tolerate the mess because the business still feels manageable. Then one extra entity becomes three, intercompany activity becomes normal, and month-end turns into a scramble. That's when “good enough” stops being good enough.

The red flags founders ignore too long

You need a real multi-entity accounting setup if any of these are true:

- You launched another legal entity. That includes a foreign subsidiary, a new LLC for a product line, or a separate entity for payroll, IP, or real estate.

- Your month-end close drags. According to NetSuite's overview of multi-entity accounting, manual consolidation can take weeks because teams have to collect spreadsheets, adjust intercompany activity, convert currencies, and prepare consolidated reports. NetSuite also says modern systems can cut that workflow from weeks to minutes.

- You can't view performance by entity cleanly. If your agency has one entity servicing US clients and another handling contractors abroad, a blended P&L hides operational truth.

- Your tax, audit, or diligence burden is rising. Once outside parties ask how balances roll up across entities, spreadsheet-based answers stop holding up.

- Your team keeps finding mismatches after the close. That means your process is reactive, not controlled.

If that sounds familiar, you've probably also outgrown a basic finance setup. That's usually the same moment companies realize they've outgrown their bookkeeper and need a different finance structure.

Why this breaks investor trust fast

Investors and lenders don't care that your controller spent all weekend tying out intercompany balances. They care whether the reporting is timely, consistent, and defensible.

Operator's view: the longer the close, the less useful the numbers become for running the business.

The hidden cost isn't just delay. It's management behavior. When leadership doesn't trust the consolidated numbers, they start building side spreadsheets, using bank balances as proxies for performance, and asking departments for “one-off” reports. That creates more inconsistency, not less.

Common misconceptions make this worse:

| Misconception | Reality |

|---|---|

| “We only have two entities, so Excel is fine.” | Two entities are enough to create intercompany, FX, and consolidation issues. |

| “We'll fix this when we're bigger.” | The mess compounds as transactions and stakeholders increase. |

| “Our external CPA can handle it at year-end.” | Year-end cleanup doesn't give you monthly decision-grade reporting. |

If you're crossing borders, taking investor money, or splitting operations across entities, don't wait for audit season to discover your finance stack can't support your structure.

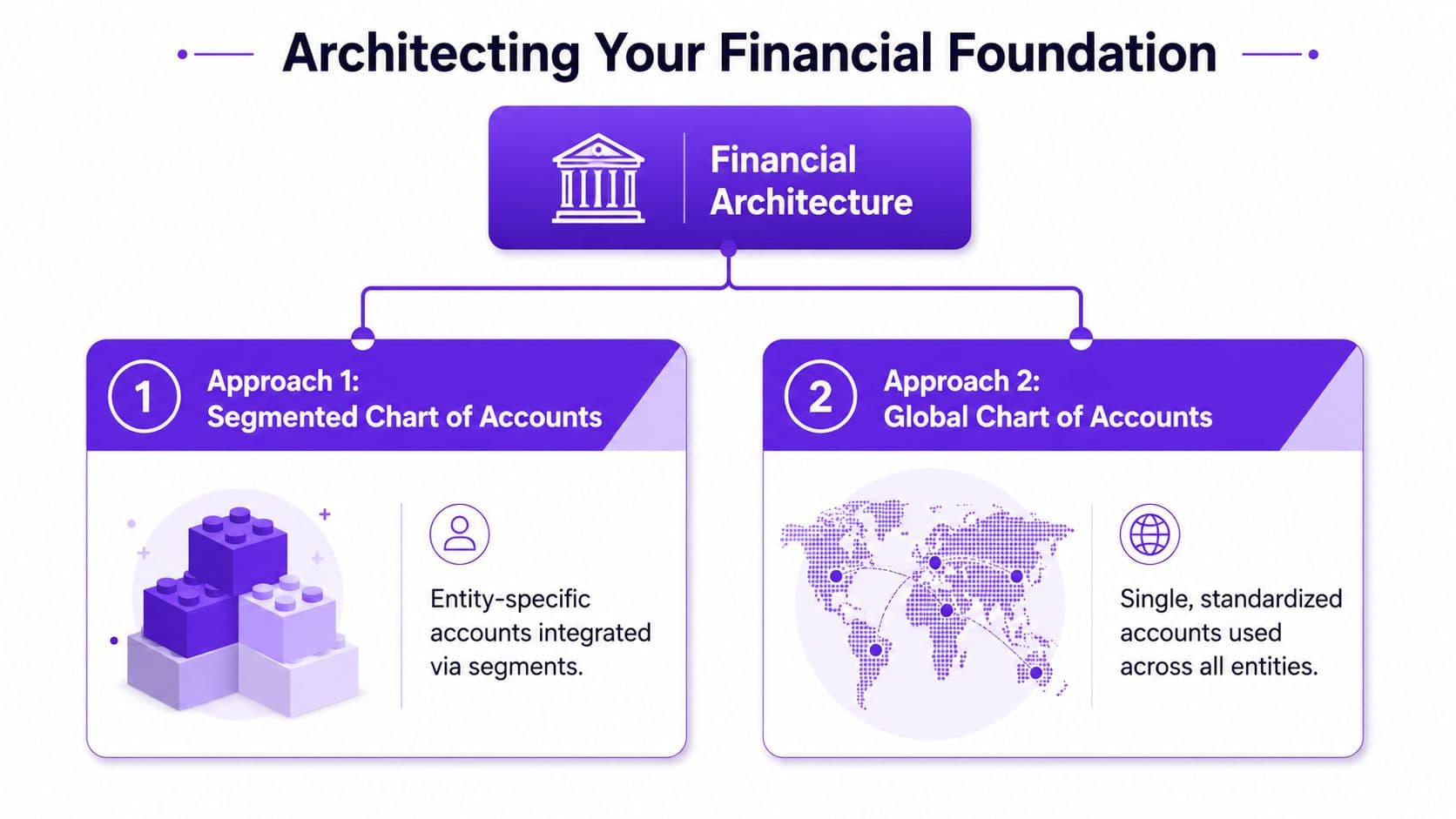

Architecting Your Financial Foundation

Most implementation failures start before software is selected. The company never defines the financial architecture. Then the system gets blamed for bad reporting that was really caused by bad design.

A critical issue is comparability. As explained in Wiss's CFO guide to multi-entity accounting software, the core challenge is ensuring comparability across entities. Purpose-built systems matter because they enforce standardized policies and a consistent chart of accounts. Without that, reconciliation gets heavier and the parent can't reliably eliminate internal transactions to show only third-party activity.

Choose your chart of accounts model

You have two workable models.

Global chart of accounts. Every entity uses the same core account structure. This is usually the right answer for SaaS, agencies, and services firms with similar operating models across entities.

Entity-specific charts mapped to a master list. Each entity keeps a local chart, but every account maps to a standardized group structure. This works better when local requirements differ, especially across jurisdictions.

Here's the tradeoff:

| Model | Best for | Strength | Risk |

|---|---|---|---|

| Global chart of accounts | Similar entities with centralized finance | Easier consolidation and cleaner management reporting | Can feel rigid for local teams |

| Local charts mapped to a master | Mixed geographies or regulatory complexity | More local flexibility | Mapping discipline becomes critical |

If you're unsure, start simpler. Standardize aggressively unless a real legal or reporting requirement forces variation. If you want a refresher on the mechanics, this overview of what a chart of accounts is and how to structure it is worth reviewing before a migration.

Here's a useful walkthrough on how teams think about financial structure in practice:

Use dimensions before your chart gets bloated

Founders often try to force every reporting need into the chart of accounts. That's a mistake.

Use dimensions or tags for things like department, location, client, product line, or channel. Think of the chart of accounts as the skeleton and dimensions as the metadata. If your SaaS business wants to report revenue by entity, by region, and by product, don't create a jungle of duplicate accounts. Keep the account structure clean and tag the transaction.

Practical rule: if you're creating new accounts just to answer a reporting question, you probably need a dimension instead.

A solid architecture also requires policy decisions, not just technical ones:

- Decide who owns account creation.

- Define intercompany billing rules.

- Standardize expense classifications across entities.

- Lock down mapping changes and review them centrally.

If you skip governance here, you won't have a software problem later. You'll have a credibility problem.

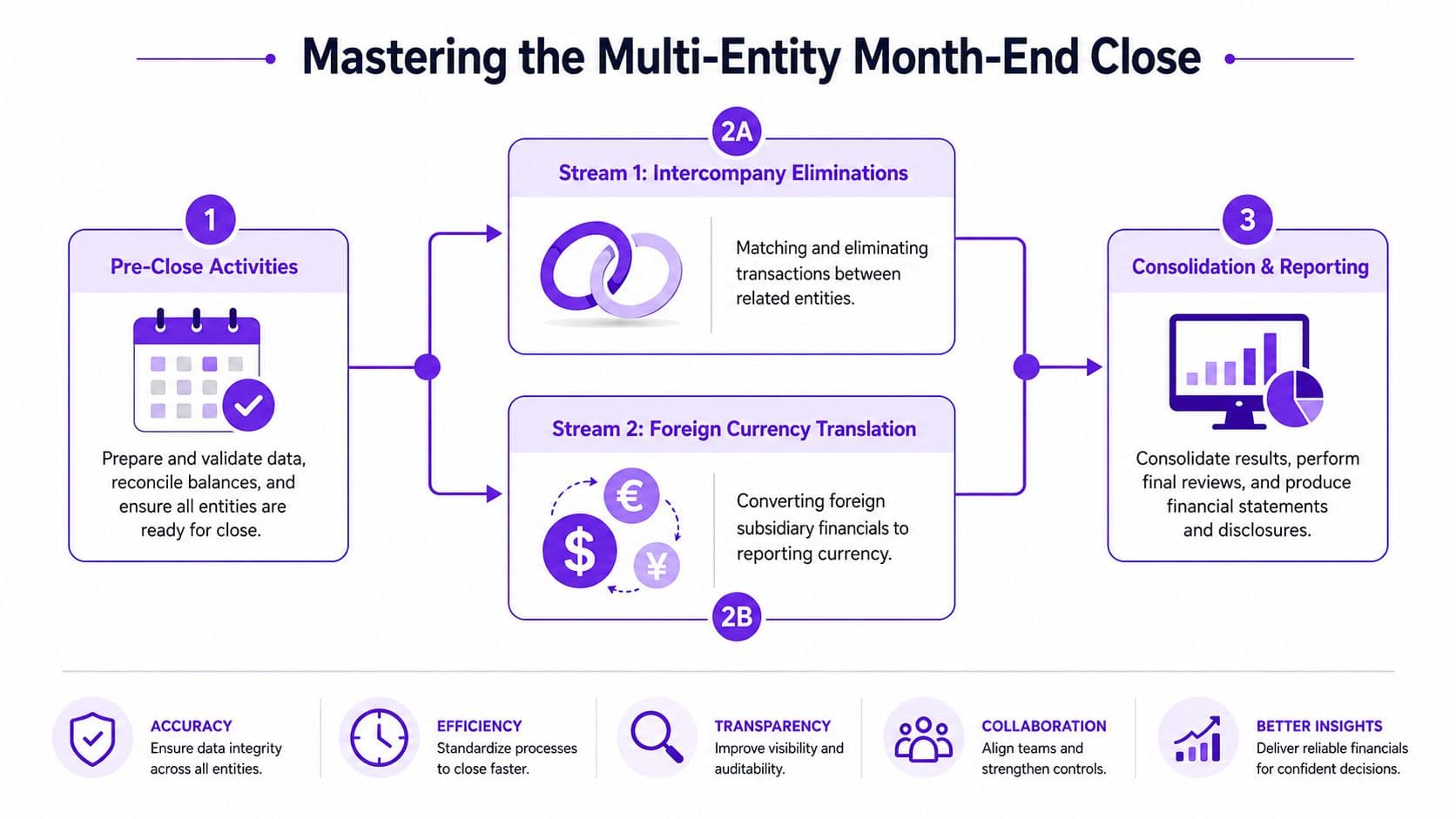

Mastering the Multi-Entity Month-End Close

Month-end is where weak architecture gets exposed. If your entities each maintain their own books, the parent still needs a consolidation layer that removes internal activity, handles currency translation where relevant, and produces a clean group view.

A strong close process doesn't just move faster. Insightsoftware's guidance on multi-entity reporting notes that the operational gain from automation is a faster close because manual invoice processing, reconciliations, and consolidation steps are reduced. It also highlights the importance of centralized transaction processing and real-time dashboards for businesses with frequent intercompany activity.

If your current checklist is still a loose collection of exports and manual tie-outs, tighten it up with a more disciplined month-end close process.

A worked intercompany example

Here's a basic example that every founder should understand.

Entity A provides services to Entity B for $10,000.

On Entity A's books

- Debit Due from Entity B: $10,000

- Credit Intercompany Revenue: $10,000

On Entity B's books

- Debit Intercompany Expense: $10,000

- Credit Due to Entity A: $10,000

At the entity level, those entries are fine. One entity earned revenue. The other incurred expense. But at the group level, nothing happened with an outside customer. The consolidated financials must remove the internal activity.

Consolidation elimination entry

- Debit Intercompany Revenue: $10,000

- Credit Intercompany Expense: $10,000

- Debit Due to Entity A: $10,000

- Credit Due from Entity B: $10,000

After elimination, group revenue and group expense both drop by $10,000, and the intercompany receivable and payable disappear from the consolidated balance sheet.

That's the logic. If you don't do this consistently, your group P&L is inflated and your balance sheet is cluttered with balances that don't belong in external reporting.

Why cash visibility matters more than consolidation optics

This is a common oversight. Consolidation is not the same as liquidity control.

One entity can look healthy in the consolidated reporting while another is short on cash and struggling to cover payroll or vendors. That's especially common when the operating entity incurs costs and a holding or parent entity collects cash, or when one subsidiary funds another through recurring settlements that nobody tracks tightly.

Use a separate view for intercompany cash management:

| Question | What you need to see |

|---|---|

| Which entity holds the cash? | Entity-level bank balances |

| Which entity is funding operations? | Due-to and due-from aging |

| Are transfers operational or long-term? | Clear treatment of loans vs settlements |

| Is the group masking local stress? | Entity-level cash runway, not just consolidated profit |

A profitable consolidated P&L can hide a cash problem inside the entity that actually runs the business.

For SaaS companies, this often shows up when Stripe deposits land in one entity while engineering payroll sits in another. For agencies, client receipts may pile up in a parent while local teams bear delivery costs elsewhere. If you don't actively manage intercompany settlements, you'll confuse accounting performance with usable cash.

Choosing Your Multi-Entity Accounting Software

Software choice matters, but not in the way founders usually think. The decision isn't “which platform has the longest feature list.” The decision is “which platform fits our entity structure, reporting needs, and control requirements without creating operational drag.”

What to compare before you buy

Start with these criteria:

- Native multi-entity support. Does the system consolidate inside the platform, or are you bolting on another tool?

- Intercompany handling. Can it track due-to and due-from balances cleanly?

- Multi-currency support. If you operate internationally, this isn't optional.

- Revenue recognition workflow. SaaS teams dealing with deferred revenue and ASC 606 complexity need more than a basic GL.

- Integrations. Stripe, Gusto, Shopify, and CRM billing tools all affect finance reality.

- Auditability. Rule changes need approvals, logs, and review discipline.

That last point matters more now. As discussed in Nominal's perspective on multi-entity accounting and automation, the emerging risk with AI isn't speed. It's control quality. The best systems preserve strong human review for intercompany, FX, and compliance judgments.

Don't buy the most automated system. Buy the system your team can govern.

If your legal structure is also getting more complex, finance and contracting start to overlap. Teams dealing with approvals across related entities often benefit from cleaner workflows for streamlining multi-party contract signing, especially when vendor obligations and entity ownership need to stay aligned with the accounting setup.

Software comparison table

| Feature | QuickBooks Online Advanced | Xero + Add-ons | NetSuite |

|---|---|---|---|

| Core fit | Smaller groups that want familiarity | Lean teams comfortable with app stacks | Businesses needing native multi-entity ERP depth |

| Multi-entity setup | Limited compared with native ERP workflows | Usually depends on third-party consolidation tools | Native multi-entity capability |

| Intercompany accounting | Manageable at lower complexity, but process-heavy | Depends heavily on add-on design | Stronger fit for structured intercompany workflows |

| Multi-currency | Available, but operational depth varies | Available, often with app dependencies | Better suited for broader global structures |

| ASC 606 readiness | Often needs workarounds or supplemental tools | Often needs specialized apps | Better fit when revenue recognition complexity rises |

| Stripe and Gusto ecosystem | Strong SMB familiarity | Strong SMB familiarity | Usually requires more implementation planning |

| Total cost of ownership | Lower upfront, but manual overhead can grow | Moderate, with app sprawl risk | Higher investment, stronger long-term architecture |

| Best for | Simpler groups with disciplined processes | Teams comfortable stitching tools together | Companies that have clearly crossed the complexity threshold |

Common objections deserve direct answers.

“We're too small for a real system.” Size is less important than structure. A messy two-entity business can need better controls before a larger single-entity business does.

“We'll stay on QuickBooks no matter what.” That's fine if complexity remains low and someone owns the process tightly. It's not fine if your workaround stack becomes your operating model.

“AI will automate most of this soon.” Not the judgment layer. Eliminations, FX rules, ownership mappings, and exception review still need accountable humans.

Your Action Plan Migration and Outsourcing

Most migrations fail because the company starts with software and skips process discipline. You need readiness before cutover.

If your broader systems are changing too, borrow a page from engineering leadership. The logic behind defensible modernization decisions for technical leaders applies here too. Don't migrate because the old setup feels annoying. Migrate because the target state is clearer, more controllable, and easier to support.

Migration readiness checklist

Use this before you commit to a platform or timeline.

- Clean historical data first. Close open reconciliations, resolve suspense balances, and identify stale intercompany accounts.

- Standardize the chart structure. Finalize your global chart or mapping logic before import.

- Document entity relationships. Ownership, reporting currency, tax IDs, and bank accounts should live in one controlled source.

- Define intercompany rules. Spell out which entity bills, which entity pays, and how settlements happen.

- Map your integrations. Stripe, Gusto, Shopify, payroll, expense tools, and billing systems all need an owner and a data flow.

- Choose a cutover date. Don't drift into transition mode. Pick a hard date and build backward from it.

- Assign decision rights. One person approves mappings. One person approves new accounts. One person owns consolidation review.

A migration succeeds when you remove ambiguity before the first import.

Outsourcing decision framework

A lot of growing companies shouldn't build this in-house immediately. They need the process sooner than they can hire, train, and manage for it.

Use this framework:

| Question | Build internally if | Outsource if |

|---|---|---|

| Team capacity | You already have strong controller-level ownership | Your team is stretched or junior |

| Entity complexity | Low and stable | Increasing across entities or jurisdictions |

| Systems expertise | You have implementation and reporting experience in-house | You need specialized migration support |

| Reporting demands | Internal management only | Investors, lenders, or diligence require cleaner outputs |

| Close discipline | Existing team closes accurately and consistently | Close quality depends on heroics |

If you're evaluating outside support, compare firms on operating model, review depth, and system fluency. Ask who handles intercompany reconciliations, who signs off on mappings, and how exception handling works. If you need a baseline on what outsourced support can look like, review this guide to finance and accounts outsourcing.

The right answer isn't ideological. It's practical. If outsourcing gets you control faster, do that first. You can always build later once the architecture and process are stable.

From Financial Chaos to Strategic Clarity

Multi-entity accounting isn't a back-office upgrade. It's a management upgrade.

When you replace fragmented entity files and spreadsheet consolidations with a controlled structure, your reporting stops being late, fragile, and arguable. You see which entity is performing, which entity is consuming cash, and where intercompany activity is distorting the picture. That gives you better capital allocation, cleaner board reporting, and fewer surprises during audit, diligence, or expansion.

If you're running multiple entities on a single-entity mindset, fix it now. Don't wait for an investor question, a tax issue, or a payroll squeeze in the wrong subsidiary to force the decision.

The companies that scale cleanly treat finance architecture as infrastructure. They standardize the chart. They govern intercompany rules. They choose software that fits the structure. Then they build a close process that produces numbers leadership can use.

If you want help designing or upgrading your multi-entity accounting setup, Jumpstart Partners works with growing SaaS, agency, and services businesses that need cleaner closes, investor-ready reporting, and a finance function built to scale.