Financial Operations

The Single Entry Accounting System Your Business Outgrew

Is your single entry accounting system exposing your business to risk? Learn the warning signs, compliance costs, and how to migrate to double-entry.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readIf you're still running your company on a single entry accounting system, you're not saving money. You're delaying a cleanup that gets more painful once you hit growth, fundraising, audit prep, or even basic management reporting.

The strongest wake-up call is this: a 2024 survey by Bench.co found 62% of sub-$5M SaaS startups still on single-entry, and those companies faced 25% higher error rates in fundraising P&Ls. During migration work, outsourced finance teams like Jumpstart Partners have found an average of $47K in errors per client according to Aurora Training Advantage's summary of that data. If you're in the $500K to $20M range, this isn't a bookkeeping preference anymore. It's an operating risk.

Founders often think single entry is "good enough" because cash is moving, bills are getting paid, and the bank account hasn't gone negative. That's a low bar. A scaling SaaS firm, agency, or services business needs clean accruals, a reliable balance sheet, and reporting you can defend under pressure.

Your Business Is Not a Checkbook So Stop Managing It Like One

A single entry accounting system records each transaction only once. Think of a check register or a simple cash book with a date, description, amount in or out, and running balance. It tells you where cash went. It does not tell you the full financial reality of your business.

Single-entry bookkeeping was the foundational method used for centuries before Luca Pacioli's guide to double-entry bookkeeping was published in 1494, and the shift away from it accelerated as trade grew and business complexity increased, eventually making it obsolete for professional financial management, as described in this history of accounting overview from Staxbill.

What single entry actually looks like

Here's a stripped-down example.

Assume your business starts the week with $20,000 in the bank.

| Date | Description | Money In | Money Out | Running Balance |

|---|---|---|---|---|

| Apr 1 | Opening balance | $20,000 | ||

| Apr 2 | Client payment received | $8,000 | $28,000 | |

| Apr 3 | Software subscriptions | $1,200 | $26,800 | |

| Apr 4 | Contractor payment | $4,000 | $22,800 | |

| Apr 5 | Loan proceeds deposited | $30,000 | $52,800 |

At first glance, this looks fine. You can see cash moved up and down. But the record creates a serious problem on Apr 5. The $30,000 loan deposit increases cash, but in single entry it often sits beside customer receipts as just another inflow. That means your books can blur borrowed money with earned revenue unless someone manually rebuilds the story later.

The worked calculation founders rely on, and why it breaks

Single-entry users often estimate profit by comparing owner capital over time.

A basic formula used in this system is:

Profit or loss = Closing Capital - Opening Capital + Drawings - Capital Introduced

Here's a simple worked example using real numbers:

- Opening capital: $50,000

- Closing capital: $68,000

- Owner drawings: $6,000

- New capital introduced: $4,000

Calculation:

$68,000 - $50,000 + $6,000 - $4,000 = $20,000 profit

That may be usable for a very small cash-only operation. It is not enough for a business with deferred revenue, unpaid invoices, prepaid expenses, loans, payroll liabilities, card settlements, or project profitability questions.

Practical rule: If you need to explain why profit and cash don't match, you've already outgrown single entry.

Why simplicity becomes a liability

Single entry feels clean because it's short. That's also why it fails you. It doesn't naturally show:

- What customers owe you

- What you owe vendors

- Whether cash came from sales, debt, or owner contributions

- Whether you've earned revenue or just collected cash

- What your company owns and owes overall

If you're a founder, you need more than a bank balance. You need a financial system that answers questions quickly and correctly. Single entry doesn't do that. It forces you or your team to reconstruct reality by hand every month.

That's not finance. That's damage control.

The Hidden Costs and Compliance Risks You Are Ignoring

The biggest problem with a single entry accounting system isn't that it's old. It's that it gives you false confidence.

You can have money in the bank and still be underpricing projects, missing liabilities, overstating revenue, and walking into tax or diligence issues blind. That's what makes single entry dangerous for SaaS companies, agencies, and professional services firms. The errors don't announce themselves.

Your books don't self-check

In single entry, there is no built-in balancing mechanism. One transaction goes in one place, and nothing forces the rest of the record to agree with it.

According to Remote Books Online's explanation of single-entry system features, single-entry increases error risk by 20-30% in manual setups. The same source notes that 40% of single-entry books required adjustments during IRS reviews versus 15% for double-entry, and that unrecorded receivables can inflate apparent liquidity by 15-25% on average.

That last point matters more than most founders realize.

Say you think you have $100,000 available to operate because the bank looks healthy. If your receivables aren't being tracked properly and your cash view is overstated by 15% to 25%, your apparent liquidity can be off by $15,000 to $25,000. You hire too early, spend too aggressively, or assume you can cover taxes and debt service without pressure. Then reality shows up.

A healthy bank balance doesn't prove your numbers are healthy. It only proves cash hit the account.

SaaS and services firms get hit first

Single entry is especially bad for businesses that earn revenue over time.

If you're a SaaS company billing annual contracts upfront, cash collection and revenue recognition are not the same thing. If you're an agency invoicing retainers, paying contractors before client collections, or carrying work in process, cash movement tells only part of the story. If you're a consulting firm with prepaid software, payroll accruals, and reimbursable expenses, the gap gets wider.

Here are the practical failures I see most often:

-

Deferred revenue gets ignored

You collect cash today and treat it like earned revenue, even though the service will be delivered over future periods. -

Accounts receivable disappears from view

A founder sees less urgency on collections because unpaid invoices never show up cleanly in the reporting set. -

Loans get treated like income

Debt proceeds hit the bank and make the month look stronger than it is. -

Vendor obligations stay off the page

Your cash book doesn't tell you what bills are already incurred but unpaid. -

Tax positions get messy fast

Sales tax, use tax, payroll liabilities, and income tax support all depend on complete records.

For founders selling across states or through multiple channels, tax complexity gets worse quickly. If you're dealing with nexus, online sales, and varying filing requirements, this guide to internet sales tax compliance is worth reading because tax mistakes compound when the underlying books are incomplete.

Fundraising pressure exposes weak books immediately

Investors and lenders don't want a story about your cash book. They want financial statements they can trust.

If your reporting depends on someone manually translating a single-entry ledger into accrual-based numbers each month, you're creating avoidable risk in every board deck and diligence request. That's also why stronger financial controls for growing businesses matter. Controls aren't bureaucracy. They're how you stop one bad spreadsheet assumption from contaminating everything downstream.

Use this quick diagnostic:

| Question | If the answer is no, you have a problem |

|---|---|

| Can you produce a current balance sheet? | You don't fully know what the business owns and owes |

| Can you separate cash receipts from earned revenue? | Your P&L is likely misleading |

| Can you track unpaid invoices and unpaid bills? | Your forecast isn't reliable |

| Can you support tax filings and diligence requests quickly? | You are one deadline away from a scramble |

Single entry is fine for a hobby business. It is not fine for a company that wants clean KPIs, credible reporting, and controlled growth.

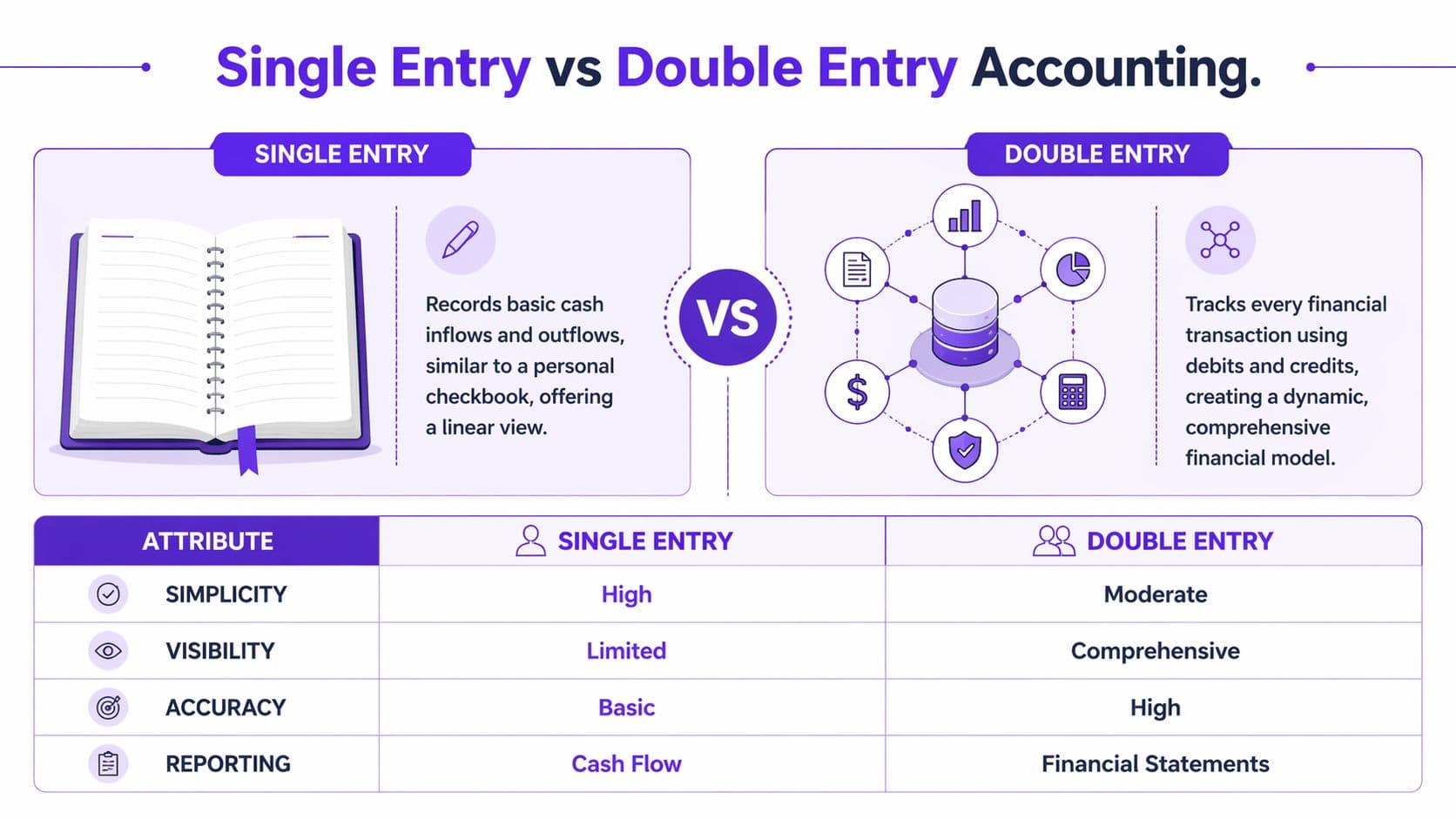

Single Entry vs Double Entry A Practical Comparison

The difference between single entry and double entry isn't academic. One records activity. The other models the business.

Double-entry bookkeeping became the standard because every transaction affects two sides of the books, and those entries have to stay in balance. Luca Pacioli provided a detailed description of the standardized system in 1494, and with support from Leonardo da Vinci, his work remained widely taught and in print for almost 400 years, helping cement double-entry as the dominant method for serious commerce, as explained by Babington's history of accounting.

Same transactions, two very different systems

Here is what typical transactions look like in both systems.

| Transaction | Single-Entry Record (Cash Book) | Double-Entry Record (Debits & Credits) |

|---|---|---|

| Customer pays $12,000 invoice | Cash in $12,000 | Debit Cash $12,000; Credit Accounts Receivable $12,000 |

| You pay vendor $3,500 | Cash out $3,500 | Debit Accounts Payable or Expense $3,500; Credit Cash $3,500 |

| Bank deposits $40,000 loan | Cash in $40,000 | Debit Cash $40,000; Credit Loan Payable $40,000 |

| Buy software annual plan for $2,400 | Cash out $2,400 | Debit Prepaid Expense or Software Expense $2,400; Credit Cash $2,400 |

| Owner puts in $15,000 | Cash in $15,000 | Debit Cash $15,000; Credit Owner Equity $15,000 |

That table is the whole argument.

In single entry, three completely different inflows can look similar:

- customer revenue

- debt proceeds

- owner contribution

In double entry, each one lands in a different account and changes the financial picture correctly.

What founders actually get from double entry

You don't switch to double entry because accountants like complexity. You switch because you need outputs that are useful.

With double entry, you can produce:

- An income statement that separates revenue from expenses

- A balance sheet that shows assets, liabilities, and equity

- A statement of cash flows that explains how cash moved

With single entry, you're usually trying to reverse-engineer those answers from cash activity and memory.

Operator's view: If your reporting depends on remembering what a transaction "really was," your accounting system isn't doing its job.

A practical reporting difference

Take this short sequence:

- You invoice a client for $18,000

- The client pays $10,000 now

- You incur $7,000 in payroll and contractor costs this month

- You collect the remaining $8,000 next month

In a single-entry setup, this month can look weaker or stronger depending on timing because the books follow cash. In double entry, the revenue and receivable are recorded when earned, the costs hit the correct period, and the later payment clears the receivable instead of distorting next month's performance.

That distinction matters if you're trying to understand gross margin, client profitability, or runway.

If your team needs a clearer primer on how debits and credits work in practice, this guide to bookkeeping journal entries is a useful companion. For a deeper explanation of the operating advantage, this overview of double-entry bookkeeping in accounting connects the mechanics to real business reporting.

A blunt comparison

| Capability | Single Entry | Double Entry |

|---|---|---|

| Easy to start | Yes | Moderate setup required |

| Tracks cash movement | Yes | Yes |

| Tracks receivables and payables clearly | No | Yes |

| Separates debt, revenue, and equity | Weakly | Yes |

| Produces balance sheet | No | Yes |

| Supports reliable audits and diligence | Weakly | Yes |

| Gives you management-grade reporting | No | Yes |

Single entry records events. Double entry explains the business.

Warning Signs Your Business Has Outgrown Single Entry

Single entry usually fails before founders call it a failure. It shows up as confusion, delays, and constant manual fixes. You feel it when cash looks wrong, reporting takes too long, and basic questions require a spreadsheet hunt.

At that point, the issue is no longer bookkeeping preference. It's operating risk.

Red flags founders recognize immediately

If any of these are happening, your business has already outgrown a cashbook-style system.

-

You can't close the month fast enough to use the numbers

If reports arrive after you've approved hiring, marketing spend, or vendor payments, the books are lagging the business. -

You describe revenue based on cash received

Deposits, prepayments, milestone billing, and collections are not the same thing as earned revenue. If your team mixes those up, your margin reporting is unreliable. -

Your cash forecast keeps surprising you

Payroll, debt service, sales tax, annual software renewals, and unpaid bills do not disappear because they were not recorded properly. -

You get asked for a balance sheet and scramble

Lenders, investors, buyers, and serious operators expect one. If you cannot explain assets, liabilities, and equity cleanly, you are running with limited visibility. -

Your tax preparer has to reconstruct the year

Cleanup work means your records are incomplete, misclassified, or both. That costs money and increases the chance of filing errors. -

Fundraising or board reporting depends on spreadsheet adjustments outside the books

Once your source records need manual patches every month, your controls are weak and your numbers are harder to defend.

What these signs usually mean

These problems are not random. They usually point to the same underlying issue. Your business has started carrying obligations and timing differences that single entry does not track well.

| Warning sign | What it usually means |

|---|---|

| Loan proceeds are mixed in with operating inflows | Revenue or cash from operations is overstated |

| Client prepayments hit income immediately | Deferred revenue is missing |

| Unpaid invoices live in a spreadsheet outside the books | A/R is disconnected from reporting |

| Bills are recorded only when paid | Expenses land in the wrong month |

| Founders keep asking what a payment was for | Chart of accounts and coding discipline are too weak for scale |

A $700K services firm with monthly retainers can hit this wall. So can a $12M ecommerce brand with inventory, debt, and sales tax exposure. Revenue size matters less than operational complexity.

Common founder objections, and why they fail

Founders usually defend single entry for three reasons.

"It's simpler."

It is simpler to type in. It is harder to run a company from. Every shortcut in the ledger becomes extra cleanup, explanation, and correction later.

"We're still too small for this."

Small businesses still sign contracts, collect deposits, owe vendors, borrow money, and pay people. If your company does those things, you need books that reflect them correctly.

"We'll fix it later."

Later is more expensive. Historical cleanup gets slower, opening balances get harder to rebuild, and old reporting decisions become harder to trust.

If your team needs outside help just to explain month-end results, stop patching the process. Replace the system before the next growth phase exposes the gaps.

Many founders who hit these warning signs have also outgrown basic transaction processing support. If your reporting process already feels strained, read these signs you've outgrown your bookkeeper and what to do next.

Your Step-by-Step Migration to Double Entry Accounting

A clean migration doesn't start in software. It starts with a cut-off decision and disciplined cleanup.

If you try to flip from single entry to double entry without a plan, you create duplicate activity, wrong opening balances, and bad management reports. The right move is controlled conversion.

Step 1 Pick a hard cut-off date

Use the end of a month. Don't migrate in the middle of a reporting period unless you enjoy confusion.

The cut-off date gives your team a line in the sand:

- everything before that date gets cleaned and summarized

- everything after that date gets entered into the new ledger structure

- reconciliations tie the two together

For most businesses, month-end or quarter-end is the cleanest transition point.

Step 2 Clean your historical records before migration

Don't dump bad data into a better system. Fix the obvious issues first.

Review your cash records and supporting documents for:

- Unclear deposits such as owner contributions, loan proceeds, customer payments, and refunds

- Duplicate or missing payments

- Outstanding customer invoices that were tracked outside the books

- Unpaid vendor bills

- Recurring subscriptions, payroll items, and debt obligations

This is also where you rebuild opening balances for assets and liabilities. If your team needs context on how those balances roll into a formal ledger, this explainer on what a general ledger is helps clarify the structure you're moving into.

Step 3 Build a chart of accounts that fits your business

Don't use a generic template and call it done. A SaaS company, an agency, and a consulting firm need different reporting logic.

Your chart of accounts should separate things that matter operationally, such as:

| Business type | Accounts that usually deserve special attention |

|---|---|

| SaaS | Deferred revenue, subscription revenue, payment processing fees, customer refunds |

| Agency | Client reimbursables, contractor costs, pass-through media spend, retainers |

| Professional services | Work in process, labor costs, reimbursable expenses, unbilled receivables |

A good chart of accounts makes reporting easier later. A sloppy one guarantees rework.

Step 4 Set opening balances correctly

This is the part founders often underestimate.

You need opening balances for:

- cash

- accounts receivable

- accounts payable

- loans and credit cards

- prepaid expenses

- fixed assets, if applicable

- owner equity or retained earnings

Here's a simple worked example.

Assume your migration date is May 1 and you verify these balances:

- Cash: $85,000

- Accounts receivable: $22,000

- Prepaid software: $3,600

- Accounts payable: $14,000

- Bank loan: $50,000

Your opening equity is the balancing figure.

Calculation:

Assets = $85,000 + $22,000 + $3,600 = $110,600

Liabilities = $14,000 + $50,000 = $64,000

Opening equity = $110,600 - $64,000 = $46,600

That means your opening entry in the new system must balance to $46,600 in equity.

Step 5 Run both systems briefly

Don't shut off the old method on day one. Parallel-run for a short period so you can compare outputs and catch mapping issues.

One practical approach:

- Enter current activity into the new accounting platform.

- Keep the old cash record updated for reference.

- Compare cash, major invoices, bills, and debt balances weekly.

- Reconcile differences immediately.

Migration teams usually catch misclassified deposits, missing liabilities, or customer balances that never made it into the opening entry.

Migration rule: Parallel-run long enough to validate the books, not long enough to create two competing sources of truth.

Step 6 Lock the new process down

Once balances reconcile and the new books are stable, standardize the month-end routine.

That means:

- bank and credit card reconciliations every month

- invoice and bill cut-off procedures

- revenue recognition policy

- documented close checklist

- role ownership across bookkeeping, controller review, and founder approvals

Founders often ask whether they should wait for a "perfect" time to migrate. No. The best time is before the next financing process, tax crunch, or major growth push forces a rushed cleanup.

Building Your Scalable Finance Stack with an Expert Partner

The move away from a single entry accounting system isn't just an accounting upgrade. It's the point where your finance operation stops being reactive.

Once your books run on double entry, you can build a finance stack that gives you usable reporting instead of delayed guesswork. For most growth-stage companies, that means connecting the accounting platform to the systems already driving cash and operations.

What a scalable setup looks like

A solid finance stack usually includes:

- Accounting platform such as QuickBooks, Xero, or NetSuite

- Bank and card feeds for transaction capture and reconciliation

- Billing and payments systems such as Stripe or Shopify

- Payroll tools such as Gusto

- Expense controls and AP workflows for bill approvals and payment timing

- Controller review to catch classification issues and maintain reporting quality

The goal isn't more software. The goal is one reliable reporting layer.

What changes after the migration

When the system is set up properly, you stop asking basic reconstruction questions and start using finance as a management tool.

You can review:

- customer collections against receivables

- liabilities before they turn into surprises

- revenue timing instead of just cash timing

- margins by client, project, or service line

- financing decisions with clearer debt visibility

That last point matters when you're evaluating ways to fund growth. Founders comparing short-term capital options should understand the tradeoffs before booking them, and this guide on comparing MCA to traditional business loans is a useful resource because financing structure affects both cash flow and reporting.

Why expert support matters

Most growing businesses don't need a full in-house finance department immediately. They do need disciplined implementation, controller oversight, and a reporting process that doesn't break under pressure.

That's why outsourced controller support is often the right bridge. It gives you the technical setup, reconciliations, close process, and management reporting without forcing a premature full-time hire. If you're evaluating that model, this overview of outsourced controller services is a practical place to start.

"Founders think they're saving money with DIY single-entry bookkeeping, but they're really just deferring the cost," says [Name], CEO of Jumpstart Partners. "That cost comes due during their first audit or fundraising round, and it's always 10x more expensive to fix it under pressure than to build it right from the start."

That quote is blunt because it's true. Single entry feels cheap only while nobody is testing the numbers. The moment a lender, investor, tax authority, or buyer asks harder questions, the hidden cost shows up as cleanup time, credibility loss, and delayed decisions.

A scalable finance operation doesn't happen by accident. It comes from using the right accounting structure, setting up the right workflows, and having experienced people review the numbers before they hit your desk.

If you're done managing your company like a checkbook and want investor-ready financials, better cash visibility, and a finance function built for growth, talk to Jumpstart Partners. Their team works with SaaS, agencies, and other growing businesses to clean up books, migrate to scalable systems, and build a reporting process you can trust.