Financial Operations

Double Entry Bookkeeping in Accounting: A Founder's Guide

Master double entry bookkeeping in accounting. A guide for founders on debits, credits, ASC 606, and building investor-ready financials with 99% accuracy.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readYour bookkeeping problem usually shows up in an investor meeting, not in your accounting software.

You get asked a simple question. Why did cash drop if revenue was up? Or why does MRR in your dashboard not match the P&L? You start explaining Stripe timing, prepaid contracts, payroll hitting early, and a spreadsheet your bookkeeper updates “outside the system.” That answer doesn’t build confidence. It tells investors, lenders, and your own leadership team that your financials aren’t dependable.

That’s what sloppy bookkeeping does. It doesn’t just create messy records. It blocks hiring decisions, distorts cash planning, and turns basic reporting into a debate.

The fix is double entry bookkeeping in accounting. Not because it’s academic. Because it’s the operating system behind financials you can trust.

Why Your Financials Are Unreliable and How to Fix Them

You’re probably not short on data. You’re short on financial integrity.

Most founders I talk to have numbers everywhere. Stripe shows one thing. QuickBooks shows another. A spreadsheet tracks deferred revenue. Someone on the team manually adjusts payroll allocations. Then month-end turns into a scavenger hunt. You don’t have one source of truth. You have competing versions of reality.

That’s why basic questions become hard:

- Cash flow: Why did cash tighten even though sales looked strong?

- Revenue: Did you earn that annual contract yet, or just collect the cash?

- Liabilities: Are client deposits sitting correctly on the balance sheet, or buried in revenue?

- Readiness: Could you hand your books to an investor or auditor today without explaining exceptions?

Your current process is holding back the business

If your books depend on memory, off-ledger spreadsheets, or uncategorized bank feeds, you’re not running finance. You’re patching leaks.

Founders often underestimate how much this spills into operations. When revenue is overstated, you hire too early. When liabilities are hidden, cash forecasts lie. When reconciliations lag, fraud and simple mistakes stay buried. If you’re also preparing for procurement reviews or vendor oversight, understanding controls like SOC 1 reports helps you see why reliable transaction handling matters beyond your own books.

Practical rule: If you need a verbal explanation for why the numbers “mostly make sense,” the system is broken.

The old system that still runs modern finance

Double-entry isn’t new. That’s exactly why it matters. Its origins trace back to medieval Italy, with fully developed systems evident by 1340 in Genoa, and Luca Pacioli first codified it in 1494, helping turn merchant recordkeeping into the foundation of modern accounting, as explained by Corporate Finance Institute’s history of double-entry.

That history matters for one reason. This method survived because it works at scale.

Italian merchants used it to manage expanding trade networks. The Medici Bank used it to handle complex transactions across Europe. You need it for the same core reason. Growth creates complexity, and complexity punishes weak bookkeeping.

If you run a SaaS company, agency, or services firm, this isn’t back-office cleanup. It’s how you separate cash from revenue, deposits from earned income, and assumptions from facts.

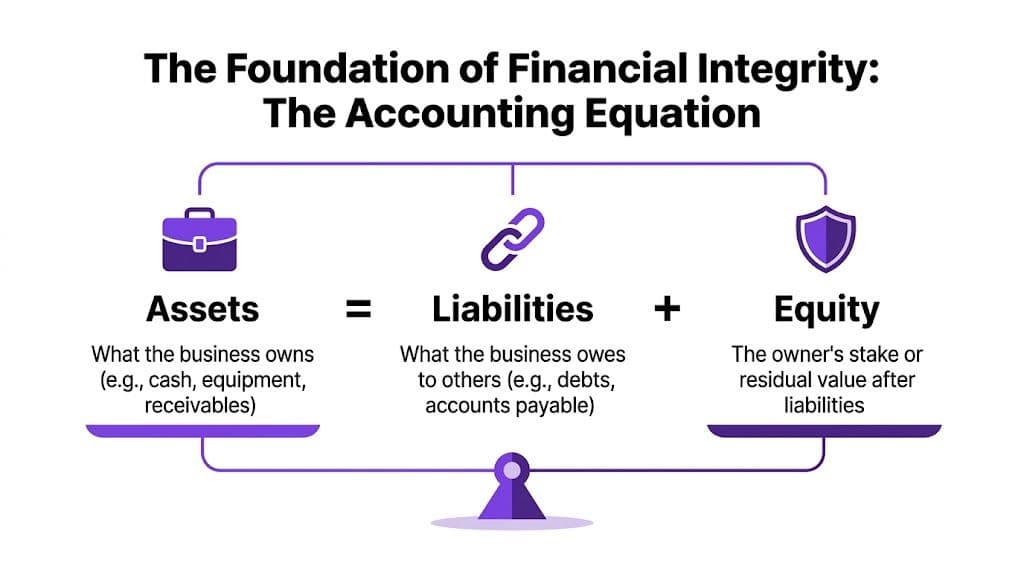

Understanding the Accounting Equation and Financial Integrity

The accounting equation is simple:

Assets = Liabilities + Equity

That’s the backbone of double entry bookkeeping in accounting. If your books don’t preserve that balance with every transaction, your reports are unreliable by definition.

Imagine a scale. One side shows what the business owns. The other shows who has a claim on those resources, either outsiders through liabilities or owners through equity. Every transaction adds weight, removes weight, or shifts weight. The scale still has to balance.

Every transaction changes at least two accounts

Founders often get tripped up at this point. They think accounting is about categorizing transactions after the fact. It isn’t. It’s about recording the full economic effect of a transaction when it happens.

A payment from a customer doesn’t just mean “money came in.” It also means you either earned revenue or took on a liability to deliver something later. A software subscription expense doesn’t just reduce cash. It also creates an expense entry that affects profit.

According to Salesforce’s explanation of double-entry accounting, every transaction affects at least two accounts with equal and opposite entries, preserving the accounting equation. That self-balancing mechanism acts as an internal control, reducing error rates by up to 99% compared to single-entry methods and supporting the current visibility needed for a 5-day month-end close.

Why this matters to a founder

If you only look at bank balances, you’ll confuse movement with performance.

You need financial statements that tell you:

- What you own now through assets like cash and receivables

- What you still owe through liabilities like deferred revenue or payables

- What’s left for the owners through equity after all obligations

That’s the difference between bookkeeping and management reporting. A proper ledger lets you trust the P&L, balance sheet, and cash flow statement together, not as separate documents that may or may not agree.

For a more detailed breakdown of how the formula flows through your financial statements, this guide on the basic formulas of accounting is a useful reference.

If your balance sheet is treated like an afterthought, your P&L is probably lying to you too.

A quick worked example

Say your SaaS company invoices a client $10,000 for monthly recurring revenue.

Under double-entry:

- Debit Accounts Receivable $10,000

- Credit Revenue $10,000

Later, when the customer pays:

- Debit Cash $10,000

- Credit Accounts Receivable $10,000

That sequence matters. It separates earning revenue from collecting cash. If you collapse those into one mental bucket, you lose visibility into collections, revenue timing, and working capital.

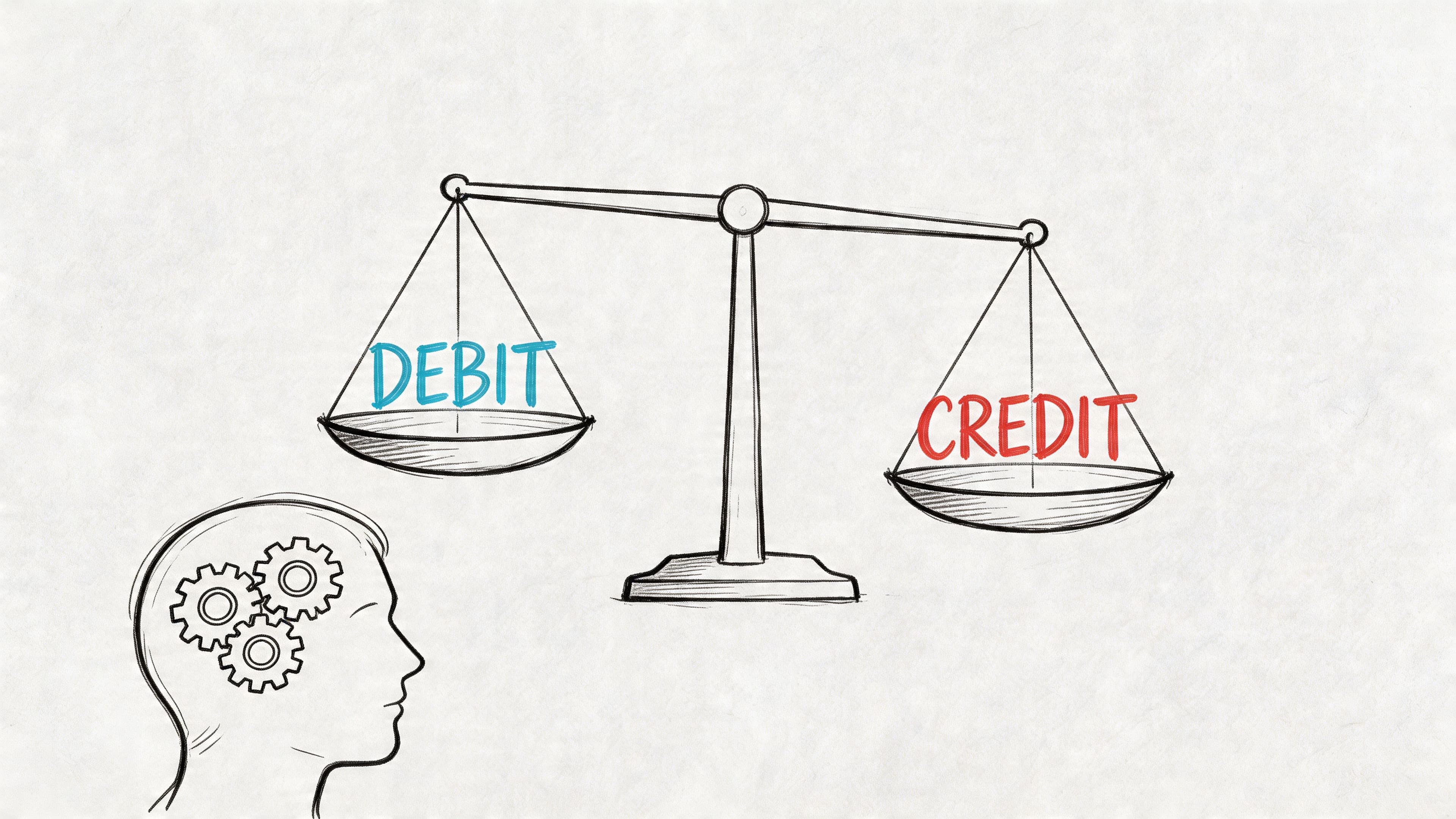

Mastering Debits and Credits Without an Accounting Degree

Most founders hear “debits and credits” and tune out. That’s a mistake. You don’t need an accounting degree to understand them. You need a usable rule.

Here it is. Debit means left side of the ledger. Credit means right side. Those words don’t mean good or bad. They tell you where the entry goes.

The mechanics are straightforward once you stop treating the terms like accounting jargon.

The rule that actually matters

As explained in QuickBooks’ guide to double-entry bookkeeping, one core rule is “debit the receiver, credit the giver.” In practice, debits increase asset and expense accounts, while credits increase liability, revenue, and equity accounts. Total debits must equal total credits, which is why the system catches errors so effectively.

Use this table. Keep it handy.

| Account Type | To Increase Account Balance | To Decrease Account Balance | Normal Balance |

|---|---|---|---|

| Asset | Debit | Credit | Debit |

| Expense | Debit | Credit | Debit |

| Liability | Credit | Debit | Credit |

| Revenue | Credit | Debit | Credit |

| Equity | Credit | Debit | Credit |

A founder-friendly example

Your company buys a laptop for $2,000 cash.

You didn’t just “spend money.” You exchanged one asset for another.

The journal entry is:

- Debit Equipment $2,000

- Credit Cash $2,000

Cash goes down, so Cash gets credited. Equipment goes up, so Equipment gets debited. Total debits equal total credits. The ledger stays balanced.

That’s the whole point. The transaction tells the truth about what happened. You didn’t lose $2,000 into a black hole. You converted cash into equipment the business now owns.

Use T-accounts when the entry feels confusing

A T-account is just a visual. Left side is debit. Right side is credit. It helps when software hides the journal logic.

For the laptop example:

| Equipment | Cash |

|---|---|

| Debit $2,000 | Credit $2,000 |

That visual matters because a lot of bookkeeping errors come from founders or junior staff posting based on bank feed labels instead of account behavior.

If you want to understand where these entries live after posting, review how the general ledger works. That’s where your financial story gets built.

Common misconceptions that waste time

Founders repeat the same mistakes here.

- “A debit means money out.” No. A debit can increase an asset, like receivables or equipment.

- “A credit means money in.” No. A credit can increase revenue, but it can also increase liabilities.

- “The bank feed should decide the category.” No. The bank feed shows movement in cash. Accounting has to capture the business event.

- “If the P&L looks right, the books are right.” No. You can have a reasonable-looking P&L and a broken balance sheet.

Debits and credits aren’t complexity. They’re the minimum structure required to make your financials believable.

Once you understand that, double entry bookkeeping in accounting stops feeling abstract. It becomes a practical way to protect cash flow, reporting accuracy, and decision quality.

Applying Double Entry in SaaS and Service Firms

Generic accounting tutorials use inventory examples because they’re simple. Your business isn’t simple.

If you run SaaS, an agency, or a professional services firm, the core issue is timing. Cash arrives before work is delivered. Contracts span months. Billing doesn’t line up neatly with performance. That’s exactly where weak bookkeeping distorts revenue and creates audit problems.

SaaS example with deferred revenue

A customer prepays $24,000 for an annual subscription.

A lot of founders want to book all $24,000 as revenue immediately because the cash hit the account. That’s wrong. You haven’t earned the full amount on day one.

The correct entry when cash is received:

- Debit Cash $24,000

- Credit Deferred Revenue $24,000

Deferred revenue is a liability. You owe the customer service over the contract term.

Then each month, you recognize one month of revenue:

- $24,000 ÷ 12 = $2,000 per month

Monthly entry:

- Debit Deferred Revenue $2,000

- Credit Revenue $2,000

That’s the discipline founders need if they want clean ASC 606 treatment and credible investor reporting.

“Founders often confuse cash in the bank with revenue. We see this constantly. For a SaaS company, that $120K annual contract you just closed is a liability on your books until you earn it. Double-entry forces that discipline, which is what separates fundable companies from lifestyle businesses. It's the language investors speak.”

Sarah Jennings, CPA and Partner at Jumpstart Partners

If you want a deeper walkthrough on the mechanics specific to software companies, this guide on accounting for SaaS is the right place to start.

Agency or services example with an upfront deposit

Now take a services firm with a $50,000 project and a 50% upfront deposit.

The client pays $25,000 before your team delivers the work.

Initial entry:

- Debit Cash $25,000

- Credit Unearned Revenue $25,000

That’s not earned income yet. It’s an obligation.

Assume you complete half the project scope and issue progress billing that reflects earned work. At that point, you recognize the portion delivered by moving the amount out of the liability account and into revenue.

Recognition entry for the delivered amount:

- Debit Unearned Revenue for the earned portion tied to the deposit

- Credit Revenue for the same amount

If the remaining work is invoiced later, you also record the receivable:

- Debit Accounts Receivable

- Credit Revenue

Agencies encounter difficulties. They mix deposits, billings, and earned revenue in one income account. The result is a P&L that looks strong while delivery obligations still sit off the books.

Why investors and auditors care

They care because the books should answer three questions cleanly:

| Question | Wrong Approach | Correct Double-Entry View |

|---|---|---|

| Did cash come in? | Book it all as revenue | Separate cash receipt from revenue recognition |

| Have you earned it? | Assume invoice date equals revenue date | Recognize revenue as service is delivered |

| What do you still owe? | Ignore contract liability | Track deferred or unearned revenue on the balance sheet |

Here’s a useful primer before you watch the walkthrough below.

The business outcome is better decisions

This isn’t technical purity. It changes how you operate.

When SaaS revenue is recognized correctly, your MRR and retained obligations are easier to reconcile. When agency deposits are held as liabilities until earned, you stop overstating margin. When receivables and deferred revenue are posted properly, cash forecasting becomes useful instead of theatrical.

If you’re scaling, that’s the difference between having financial statements and having management tools.

Spotting Costly Errors Before Your Auditor Does

Most accounting failures aren’t dramatic. They’re repetitive. A date gets entered wrong. A deposit gets booked as revenue. A reconciliation gets skipped because “nothing major changed.” Then the errors stack up until an audit, diligence review, or board meeting forces the cleanup.

Red flags you shouldn’t ignore

A useful data point here is that a 2025 SaaS Capital report found 25% of mid-stage SaaS startups face significant delays or failures in financial audits due to improper revenue recognition tied to incorrect double-entry treatment of deferred revenue and contract liabilities, as noted in this summary referencing the double-entry bookkeeping background.

That doesn’t just apply to SaaS. The same failure pattern shows up in agencies and services firms whenever timing and obligations get blurred.

Warning signs and corrective actions

| Red Flag | Likely Cause | What You Need to Do |

|---|---|---|

| Profit looks strong but cash is tight | Revenue recognized too early, receivables aging, or liabilities ignored | Reconcile cash, AR, and deferred revenue together |

| Trial balance won’t clear cleanly | Entries posted one-sided or to wrong accounts | Review source transactions and correct journal entries |

| Monthly numbers change after you’ve “closed” | Close process is informal and adjustments happen ad hoc | Lock a formal close calendar and approval workflow |

| Big deposits hit revenue immediately | Client prepayments or annual contracts booked incorrectly | Move unearned amounts to liability accounts |

| Card and bank balances don’t match the books | Reconciliations skipped or unreconciled items left hanging | Complete reconciliations every month, then investigate exceptions |

| Equipment or implementation costs hit operating expense without review | Misclassification between capex and opex | Review account mappings and reclass where needed |

The pattern behind these mistakes

The symptom usually shows up in the P&L. The cause usually sits on the balance sheet.

Founders spend too much time looking at revenue and margin, and not enough time inspecting receivables, payables, deferred revenue, accrued expenses, and unreconciled cash. That’s where double-entry errors become visible.

Your auditor doesn’t create the problem. Your auditor finds the problem you let survive.

If you’re preparing for diligence or a formal review, use a structured checklist for auditors to see whether your support, reconciliations, and revenue treatment would hold up.

Automating Accuracy with the Right Tech Stack and Workflow

You shouldn’t be hand-posting routine journal entries in a spreadsheet. Your accounting system should do the heavy lifting.

QuickBooks, Xero, and NetSuite already run on a double-entry framework. Stripe, Gusto, Ramp, Shopify, and Square can feed transaction data into that system. Used properly, the stack saves time and improves consistency. Used badly, it just automates bad assumptions faster.

Automation helps, but it doesn’t think for you

Recent AI tools for NetSuite and Xero have been shown to reduce manual entry errors by 78% in agency settings, and when paired with Stripe integrations they can cut the month-end close from 15 days to 5, according to Salesforce’s reporting on accounting automation.

That’s meaningful. But software won’t fix broken logic.

If Stripe pushes a customer prepayment into revenue instead of deferred revenue, the sync is fast and wrong. If payroll maps to the wrong departments, the report is polished and wrong. If someone auto-approves uncategorized expenses, your close is efficient and wrong.

Build a workflow, not just a stack

The right setup has three layers:

- Source systems like Stripe, Gusto, Ramp, and your bank feeds.

- Accounting platform like QuickBooks, Xero, or NetSuite where entries post into the ledger.

- Close workflow where a finance lead reviews reconciliations, revenue schedules, accruals, and exceptions.

A strong process usually includes:

- Bank and card reconciliations: Match statements to the books every month

- Revenue review: Check deferred revenue, contract liabilities, and earned revenue postings

- AR and AP aging: Verify what customers owe you and what you owe vendors

- Adjustment entries: Post accruals, prepaid allocations, and corrections before locking the period

- Management review: Compare current month output against expectations and prior trends

If you’re evaluating reporting tools on top of your accounting platform, this overview of how AI query tools can improve financial accuracy is worth reading because it gets into how teams interrogate data quality instead of just generating dashboards.

One practical recommendation

Stop treating month-end close as an accounting ritual. It’s an operating cadence.

You need a documented workflow, assigned owners, and a review step that catches classification errors before reports go out. For companies that don’t want to build that internally, firms such as financial reporting automation providers can manage the reconciliation and reporting layer on top of the core systems.

From Financial Chaos to Investor-Ready Clarity

Weak books don’t stay a bookkeeping problem. They become a valuation problem, a cash problem, and a credibility problem.

If your team can’t explain deferred revenue cleanly, investors will question the revenue number. If your balance sheet is full of stale receivables and unreconciled liabilities, lenders will question cash controls. If audit support requires forensic cleanup, leadership loses time that should go into growth.

What investor-ready actually looks like

Investor-ready financials aren’t fancy. They’re reliable.

They show earned revenue, not just collected cash. They tie the P&L to the balance sheet. They support board reporting without side spreadsheets. They hold up when someone asks for detail behind contract liabilities, accruals, or reconciliations.

That’s why diligence checklists matter. If you want to see what serious buyers and investors examine, review this VC's tactical finance due diligence checklist. It’s a useful reminder that no one funds “close enough” books.

The clear recommendation

If your business is between $500K and $20M in revenue, stop tolerating accounting that depends on heroic cleanup.

You don’t need to become an accountant. You do need:

- A double-entry system that reflects the actual economics of the business

- Accurate treatment of deferred revenue, receivables, payables, and accruals

- A disciplined month-end close

- Reports you can hand to investors without an apology

That standard is a fundamental requirement if you’re raising capital, preparing for audit, or trying to run the business with any confidence.

Clean books don’t just help you report the past. They let you make the next decision with conviction.

If your current setup still depends on spreadsheets outside the ledger, unclear mappings, or delayed reconciliations, fix it now. The longer you wait, the more expensive the cleanup gets.

If you need help building a real accounting backbone, talk to Jumpstart Partners. Their team provides outsourced controller and bookkeeping support for SaaS, agencies, and service firms, including reconciliations, revenue recognition workflows, and investor-ready reporting so you can stop guessing and start trusting your numbers.