Financial Operations

Master Basic Formulas of Accounting

Master the basic formulas of accounting. Essential for SaaS & agency founders to impress investors, drive valuation, and prevent cash flow crises.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readMost advice about the basic formulas of accounting is too simple to help you run a real company. It gives you textbook equations, then leaves out the part that matters: how those formulas affect cash, valuation, and investor trust.

That gap is not small. A 2025 SaaS Capital survey cited by QuickBooks says 78% of SaaS founders report confusion on revenue recognition formulas, especially for recurring revenue models under ASC 606, and that is why clean-looking dashboards often collapse under diligence (QuickBooks on essential small business accounting formulas). If you run a SaaS company, agency, or professional services firm between $500K and $20M in revenue, you do not need more accounting trivia. You need formulas that tell you when cash is tightening, when margins are lying, and when your numbers are not investor-ready.

Founders often treat accounting formulas as something for the bookkeeper, tax preparer, or controller. That is a mistake. These formulas are your operating language. They tell you whether your growth is financed by real economics or by timing errors, deferred revenue confusion, and underpriced delivery.

The practical standard is simple. If a formula changes a hiring plan, pricing decision, fundraising story, or cash forecast, you need to know it cold. If it does not, it is secondary.

A strong finance stack starts with a short list:

- Accounting equation for financial integrity

- Margin formulas for profitability

- Break-even formula for operating viability

- Liquidity and solvency ratios for survival

- Efficiency formulas for capital discipline

If you are still managing these only in a spreadsheet you review once a month, fix that. Start with a live 13-week cash flow forecast and connect every core formula back to a business decision.

Stop Flying Blind on Your Financials

The biggest misconception in growth-stage finance is that accounting formulas are backward-looking. They are not. Used correctly, they are early warning systems.

If your books say one thing and your bank account says another, the formulas are not the problem. Your application of them is. That usually shows up first in recurring revenue businesses where collections, deferred revenue, and recognized revenue do not move in lockstep.

Why founders get this wrong

Most founders learned some version of basic bookkeeping. Revenue up. Expenses down. Profit good. That logic breaks fast in SaaS and service firms.

You can collect cash today and still not have earned the revenue. You can show a decent gross margin and still have a weak business because delivery labor, software sprawl, and bloated overhead are sitting in the wrong places. You can even raise capital while hiding weak financials from yourself.

Your accountant records history. You use formulas to make decisions.

That distinction matters. A founder who cannot interpret the balance between assets, liabilities, margins, and short-term obligations is managing by instinct. Instinct is useful in product and sales. It is dangerous in finance.

The formulas that matter

Not every formula deserves equal attention. For companies in the $500K to $20M range, I care most about whether your numbers answer five questions:

| Question | Formula category | Why it matters |

|---|---|---|

| Are the books structurally correct? | Accounting equation | Prevents false confidence |

| Are we making money on delivery? | Gross and net margin | Exposes pricing and cost issues |

| How much business do we need to stop bleeding cash? | Break-even point | Sets the operating floor |

| Can we survive short-term pressure? | Liquidity ratios | Flags cash risk early |

| Are we using capital efficiently? | ROI, CAC, conversion metrics | Shapes valuation story |

A lot of content on the basic formulas of accounting stops at definitions. That is not enough for a venture-backed SaaS company or an agency with uneven project margins. You need formulas connected to software, revenue recognition, and reporting discipline.

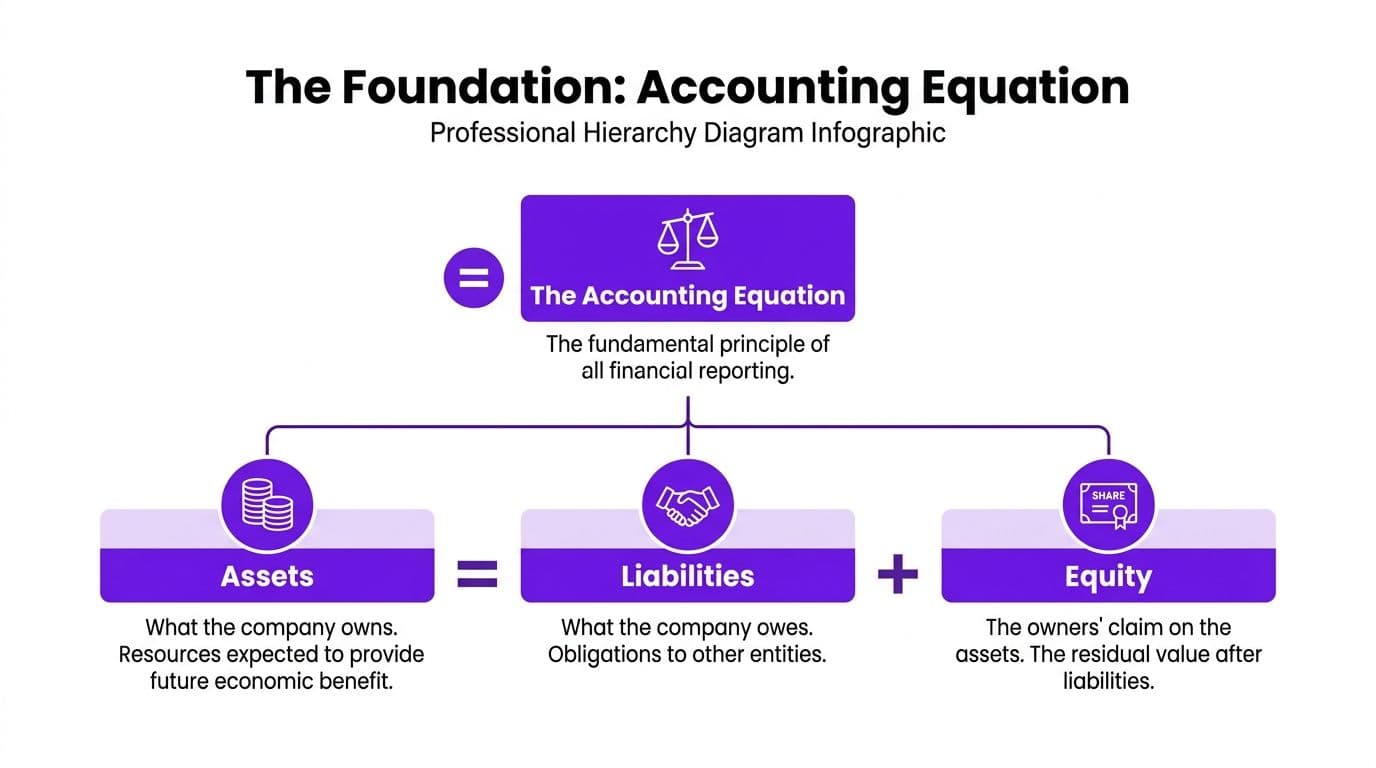

The Unbreakable Law The Accounting Equation

If your balance sheet does not balance, your board deck is built on fiction. The accounting equation, Assets = Liabilities + Equity, is the rule that keeps financial statements usable for operators, lenders, and investors.

This is not textbook trivia. It is the integrity check behind every number in QuickBooks, Xero, and NetSuite. If the equation holds, the books can be traced. If it does not, revenue recognition, liabilities, or equity are wrong, and your decisions will be wrong too.

The logic comes from double-entry accounting formalized by Luca Pacioli in 1494. Every transaction hits at least two accounts, and the books stay in balance when those entries are recorded correctly (history of accounting overview and Pacioli’s double-entry system).

What belongs in each bucket

Assets are the resources you control. Cash, accounts receivable, prepaid software, capitalized equipment, and in some cases implementation costs belong here.

Liabilities are what you owe. Accounts payable, accrued payroll, credit lines, sales tax payable, and for SaaS firms, deferred revenue often matter most.

Equity is the residual value left after liabilities are deducted from assets. For founder-led companies, this includes retained earnings, owner contributions, and any investor capital that has not been consumed by losses.

The formula looks simple because it is simple. The operating consequences are not.

A founder usually gets in trouble in two places. First, cash gets mistaken for revenue. Second, expenses or obligations sit in the wrong period. That is how a company reports strength it has not earned.

A worked example with real numbers

Tipalti provides a straightforward example of the equation in balance: $359,268 in total assets = $107,633 in liabilities + $251,635 in equity (Tipalti on the accounting equation). That is the standard. Your reports should reconcile cleanly, with every movement tied to an entry you can explain.

For a venture-backed SaaS company, deferred revenue is where this usually gets tested.

Transaction 1. You collect an annual contract upfront

A customer pays $12,000 for a 12-month subscription.

On receipt:

- Cash increases by $12,000

- Deferred revenue increases by $12,000

Assets rise. Liabilities rise. The equation stays balanced.

After one month of service:

- Deferred revenue decreases by $1,000

- Revenue, which flows into retained earnings and equity, increases by $1,000

Liabilities fall. Equity rises. The equation stays balanced again.

That entry pattern is what separates investor-ready reporting from founder math. If you book the full $12,000 as revenue on day one, MRR looks inflated, equity looks stronger than it is, and the next reporting period starts with a hole in it. In QuickBooks or Xero, this usually shows up as a manual journal entry problem. In NetSuite, it often shows up in a broken revenue schedule or a lazy implementation of ASC 606 rules.

Service firms run into a related issue with retainers and prepaid project work. Cash arrives early, but the work has not been delivered. Until the service is performed, part of that cash belongs in liabilities, not earned income.

Why this matters in diligence

Investors do not just inspect your P&L. They test whether the balance sheet supports the story. If deferred revenue is understated, accrued expenses are missing, or equity moves without a clear reason, they assume the rest of the reporting may be unreliable too.

That hurts valuation fast. It also slows diligence, triggers cleanup work, and weakens your credibility with lenders and acquirers.

Use a disciplined monthly close to catch this early. Review deferred revenue roll-forwards, accrued liabilities, and retained earnings every month. Then pressure-test the statement structure with a clear balance sheet analysis process. If your team cannot explain why assets, liabilities, and equity changed, do not use those numbers to make hiring, pricing, or fundraising decisions.

A quick visual helps if your team needs the concept laid out clearly.

Measure Your Profitability Correctly

A company can grow fast and still be weak. The first place that weakness shows up is in margin math.

Most founders watch revenue. Experienced operators watch gross profit, net profit, and break-even. Those formulas tell you whether your pricing works, whether delivery is efficient, and how much volume you need before growth becomes useful.

Gross margin first, not net margin

Gross profit formula:

Gross Profit = Revenue - Cost of Goods Sold

Gross margin formula:

Gross Margin = Gross Profit / Revenue

For a SaaS company, COGS usually includes delivery-related costs such as hosting, implementation labor tied directly to serving customers, and third-party usage costs. For an agency, COGS often includes contractor labor, freelancer production, and project-specific tools.

Worked example for a SaaS company

Suppose you recognize $12,000 of monthly revenue.

If direct delivery costs are:

- Hosting and infrastructure: $2,000

- Support tied to fulfillment: $1,000

Then:

- Gross Profit = $12,000 - $3,000 = $9,000

- Gross Margin = $9,000 / $12,000 = 75%

That tells you the service model is leaving room to cover overhead. It does not tell you the company is healthy.

Worked example for an agency

Suppose an agency bills $20,000 for a client project in a month.

If direct project costs are:

- Contractors: $8,000

- Project software allocated to delivery: $1,000

Then:

- Gross Profit = $20,000 - $9,000 = $11,000

- Gross Margin = $11,000 / $20,000 = 55%

That can be a workable delivery model. But if account management, founder overhead, and admin costs are out of control, net margin can still be poor.

Net margin is where discipline shows

Net profit formula:

Net Profit = Revenue - All Expenses

Net margin formula:

Net Margin = Net Profit / Revenue

Using the SaaS example above, if monthly operating expenses outside COGS total $7,000:

- Net Profit = $12,000 - $3,000 - $7,000 = $2,000

- Net Margin = $2,000 / $12,000 = 16.7%

You do not need perfect precision in the first pass. You do need correct classification. If implementation labor is hidden in overhead instead of COGS, your gross margin looks better than reality and your pricing decisions get worse.

For a deeper breakdown, this guide on how to calculate gross margin is worth using with your finance lead.

'Unit economics are the truth serum for SaaS businesses. You can have beautiful growth charts and impressive MRR, but if your margins are wrong, you're just scaling a cash-burning machine,' states Jason Lemkin, Founder of SaaStr.

Break-even is your operating floor

The break-even point formula is:

Fixed Costs / (Sales Price per Unit - Variable Cost per Unit)

Navitance gives a useful SaaS example. With $50K per month in fixed costs, $1,200 ARPU, and $400 in variable cost per customer, the break-even point is 62.5 customers (Navitance bookkeeping formulas and break-even point).

The math:

- Contribution per customer = $1,200 - $400 = $800

- Break-even customers = $50,000 / $800 = 62.5

Navitance also notes that falling short of this level can lead to a 25% monthly cash bleed in that example. That is why founders need break-even math on a live dashboard, not buried in an annual budget.

Use benchmarks carefully

The brief asked for benchmark data from OpenView and HubSpot, but no verified benchmark figures were provided. So the right move is qualitative guidance, not invented targets.

| Metric | SaaS Target (Source: OpenView) | Agency Target (Source: HubSpot) | |---|---| | Gross margin | Track for consistency and pricing discipline | Track by service line and delivery model | | Net margin | Watch operating efficiency as revenue scales | Watch utilization, scope control, and overhead | | Break-even | Monitor against recurring revenue base | Monitor against active retainer and project mix |

If your gross margin looks strong but cash still tightens, check three things immediately:

- Revenue recognition timing

- COGS classification

- Fixed cost creep

Those three errors account for a large share of bad operating decisions in growth-stage firms.

Formulas for Financial Survival and Solvency

Profitability matters. Survival matters more.

I have seen founders celebrate booked revenue while ignoring short-term obligations that are already choking the business. Liquidity and solvency formulas stop that nonsense. They tell you whether you can pay bills on time and whether your capital structure is getting fragile.

Current ratio and quick ratio

The current ratio is:

Current Assets / Current Liabilities

It measures your ability to cover short-term obligations with short-term assets.

The quick ratio is stricter:

Cash + Accounts Receivable + Short-Term Investments / Current Liabilities

For SaaS and service firms, the quick ratio is often more useful because these businesses usually do not rely on inventory the way product-heavy businesses do.

Worked example

Assume your balance sheet shows:

- Cash: $90,000

- Accounts receivable: $60,000

- Prepaids: $10,000

- Current liabilities: $100,000

Current assets = $90,000 + $60,000 + $10,000 = $160,000

So:

- Current Ratio = $160,000 / $100,000 = 1.6

- Quick Ratio = ($90,000 + $60,000) / $100,000 = 1.5

That is a cleaner short-term position than many founder-led firms have. The lesson is not the exact number. The lesson is whether your obligations can be covered without relying on accounting optimism.

Debt-to-equity tells investors how exposed you are

The formula is:

Total Liabilities / Total Equity

If liabilities are rising faster than equity, your flexibility is shrinking. That affects hiring, fundraising flexibility, and lender confidence.

Here, expense classification matters. If you are still unclear on what should be treated as capital spending versus operating cost, this guide to CapEx and OpEx is useful background because bad classification muddies both profitability and solvency analysis.

Liquidity buys time. Solvency buys options.

Why these formulas rest on bookkeeping discipline

The reason these ratios work at all is that double-entry accounting forces structural consistency. Debits and credits must match. That system, formalized by Pacioli in 1494, is still the backbone of financial analysis because it lets you test solvency from a balanced set of records, not from founder intuition.

Here is the practical implication:

- If payables are stale, your liquidity ratios are wrong.

- If deferred revenue is missing, your liabilities are understated.

- If equity rolls forward without support, your solvency story is weak.

Warning signs you should not ignore

| Red flag | What it usually means |

|---|---|

| Current ratio keeps falling | Expenses are outrunning collections |

| Quick ratio is weak despite reported profit | You have earnings without cash discipline |

| Debt-to-equity rises after “good” months | Growth is being financed by obligations, not retained value |

Your operating cash flow view should sit beside these ratios, not separate from them. If you do not already track that relationship, fix it with a tighter operating cash flow process.

Formulas That Signal Growth and Efficiency

Once the company is stable, investors stop asking only whether the business survives. They ask whether you use capital well.

That is where growth and efficiency formulas matter. These are not vanity metrics when they are tied back to clean accounting. They show whether spend turns into durable results and whether your operations convert effort into cash.

ROI starts with a clean denominator

The basic formula is:

ROI = Net Gain / Investment Cost

Simple formula. Easy to abuse.

If you spend on a sales initiative, a hiring push, or a systems rollout, ROI only means something if the costs are captured correctly and the resulting gain is measured consistently. That is why standardized accounting still matters. The accounting profession’s formal recognition, starting with chartered accountants in 1854 and later CPAs in the US, established the discipline that modern investors still rely on when they evaluate efficiency metrics (Maryville University on the history of accounting and the profession).

CAC payback and recurring revenue discipline

For SaaS businesses, one of the most useful operating formulas is:

CAC = Total Sales and Marketing Spend / New ARR

The exact target benchmark requested in the brief was not supported by verified data, so I will keep this practical. Use CAC formulas to answer one question: how long does it take for gross profit from a customer to recover acquisition cost?

If your team cannot explain CAC using recognized revenue logic instead of loose pipeline assumptions, your board deck is not ready.

A clean way to pressure-test efficiency:

- Pull sales and marketing spend from the P&L

- Tie new ARR to actual closed business

- Compare acquisition spend to the gross profit generated by those customers over time

Cash conversion cycle matters beyond ecommerce

The traditional cash conversion cycle formula is often discussed in inventory-heavy businesses, but service and SaaS firms still need the underlying discipline. The question is the same: how long does cash stay tied up before it returns?

For agencies and services firms, focus on:

- Billing lag

- Collections lag

- Contractor and payroll timing

For SaaS, focus on:

- Collections timing

- Deferred revenue treatment

- Sales commission timing

- Vendor payment discipline

If receivables grow while recognized revenue looks strong, your growth engine is not as efficient as it appears.

Asset efficiency still deserves attention

Asset-heavy businesses watch this constantly, but growth-stage service firms should not ignore it. A business that uses its asset base efficiently usually closes faster, forecasts better, and makes cleaner capital allocation decisions.

A useful next step is to review your asset turnover ratio alongside revenue quality. That combination often reveals whether the business is becoming more efficient or just more complex.

Investors fund efficient growth more readily than messy growth.

What finance leaders should ask every month

Use these prompts in your monthly review:

- Did recent spend produce measurable economic value, or just activity?

- Are acquisition costs tied to recognized customer value, not pipeline optimism?

- Is cash arriving in step with reported growth, or lagging behind it?

The basic formulas of accounting become strategic once you ask those questions consistently.

Common Accounting Errors That Destroy Investor Confidence

Most investor skepticism starts before the meeting. It starts when your numbers do not reconcile cleanly.

Founders assume investors care only about top-line growth and margin trajectory. Astute buyers care about discipline. If the formulas are wrong, the story is wrong.

Red flags investors notice fast

Annual contracts recognized upfront This is one of the fastest ways to signal weak finance controls in SaaS. Cash collected upfront is not the same as revenue earned. If you book it all immediately, your revenue, profit, and equity all look stronger than they are.

Bookings confused with revenue A signed contract matters. It is not the same thing as recognized revenue. If your reporting slides between those terms, nobody trusts the rest of the package.

COGS buried in operating expenses This is common in agencies and hybrid service businesses. Delivery labor gets mixed into overhead. Gross margin then looks inflated, pricing seems healthier than reality, and your service line economics become unusable.

Payment processor balances not reconciled If Stripe, Shopify, or another processor does not tie to the ledger, cash reporting gets messy fast. Fees, reserves, refunds, and timing differences distort both income and balance sheet reporting.

Why these mistakes hit valuation

A serious investor does not need every number to be perfect. They do need to see a company that understands its own economics.

Here is what bad accounting application communicates:

- Management lacks control over reporting

- Forecasts are based on weak assumptions

- KPIs may be inflated

- The close process is unreliable

That last point matters more than founders think. If your monthly close drags, your formula outputs are stale by the time you review them.

A practical pre-diligence checklist

| Investor concern | Internal test |

|---|---|

| Revenue credibility | Reconcile contracts, billings, and recognized revenue |

| Margin reliability | Reclassify direct costs and recheck gross margin |

| Cash visibility | Tie processor activity to the ledger and bank |

| Balance sheet integrity | Review deferred revenue, receivables, payables, and equity roll-forward |

If you need to “explain away” core metric inconsistencies, the problem is usually the books, not the investor.

A founder does not need to become a CPA. A founder does need to know when the formulas are producing false confidence. That is the difference between a finance function that supports valuation and one that undermines it.

How to Surface These Metrics in Your Accounting Software

The formulas are straightforward. The hard part is surfacing them consistently in the systems you already use.

A lot of teams still calculate core metrics offline, then paste the outputs into board decks. That creates lag, version issues, and arguments about whose spreadsheet is right. Put the formulas as close to the source system as possible.

QuickBooks Online

In QuickBooks Online, start with report structure.

- Profit and Loss customization: Group direct delivery costs cleanly so gross profit is visible without manual rework.

- Class or location tracking: If you run multiple service lines, use classes to separate margin by offering.

- Balance sheet detail: Review deferred revenue, receivables, and payables monthly so your accounting equation remains credible.

If gross margin requires spreadsheet surgery every month, your chart of accounts is the problem.

Xero

Xero works well when you keep the dashboard lean.

Use it to surface:

- Revenue and direct costs

- Receivables aging

- Payables aging

- Bank balances

- Short-term obligations

For service firms, Xero becomes much more useful when invoice timing and collection timing are reviewed together. That is often enough to spot cash pressure before it becomes urgent.

If your organization has fund restrictions or more specialized reporting needs, a review of nonprofit accounting software can help clarify when a standard setup is no longer enough. The lesson applies beyond nonprofits. Software fit matters when reporting complexity grows.

NetSuite

NetSuite is where you should automate more of this logic.

Build saved searches and dashboards for:

- Deferred revenue roll-forward

- Gross margin by product or customer segment

- Current and quick ratio inputs

- Receivables and payables trend lines

NetSuite becomes powerful when you stop using it as a glorified ledger and start using it as an operational finance system.

What to automate first

| Priority | Metric | Why it comes first |

|---|---|---|

| First | Gross margin | Pricing and delivery decisions depend on it |

| Second | Deferred revenue | SaaS reporting breaks without it |

| Third | Current and quick ratio | Cash risk needs a live view |

| Fourth | CAC and efficiency views | Best used once the books are clean |

Do not automate bad accounting. Clean the chart of accounts, fix recognition logic, reconcile processors, then build the dashboard.

From Formulas to Financial Clarity

The basic formulas of accounting are not just academic tools. They are operating controls.

The accounting equation tells you whether the books make structural sense. Margin formulas tell you whether your delivery model works. Break-even tells you how much volume the business needs. Liquidity and solvency ratios tell you whether you have room to maneuver. Efficiency formulas tell investors whether growth is disciplined.

Most finance problems in the $500K to $20M range are not caused by lack of ambition. They are caused by weak translation between accounting outputs and business decisions. Founders see revenue and miss liabilities. They see growth and miss burn. They see profit and miss timing.

That is why strong reporting changes decision quality. Once the formulas are accurate, your dashboard becomes useful. Hiring gets sharper. Pricing gets cleaner. Board conversations improve. Fundraising gets easier because the numbers survive scrutiny.

If your team is still wrestling with deferred revenue, inconsistent margin definitions, or software that does not surface the right metrics, the answer is not more spreadsheet work. The answer is better finance infrastructure and cleaner monthly reporting.

If you want help turning messy books into investor-ready financials, talk to Jumpstart Partners. Their outsourced controller team supports growing SaaS, agency, and service businesses with fast month-end closes, cleaner reporting, and the financial visibility you need to make decisions before cash problems show up.