Financial Operations

The Founder's Guide to Quality of Earnings in 2026

Understand your company's true value. This guide to Quality of Earnings reports helps founders navigate fundraising, M&A, and due diligence with confidence.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··13 min readYour P&L might show a healthy seven-figure profit, but buyers and investors see a completely different story. They don’t just glance at your reported numbers; they dig deep into the quality of earnings (QoE) to find out what your business really makes.

If you are a founder, CEO, or finance leader of a $500K-$20M SaaS, agency, or professional services firm, this process is the single most critical hurdle in any high-stakes deal. A Quality of Earnings report is designed to uncover your company's true, sustainable cash flow—the number that actually determines your valuation. Getting this wrong can slash your exit price by millions.

Why Your Profits Aren't What They Seem

A QoE report is a financial stress test for your profitability. It goes far beyond a standard audit, which just confirms your numbers follow accounting rules. The QoE's job is to determine your company’s real-world, repeatable profit.

For you as a leader, this distinction is everything. An investor or buyer uses the QoE to "normalize" your earnings, stripping out all the noise to answer one question: How much cash can this business reliably generate year after year?

The Problem with Your P&L Statement

Your Profit and Loss statement is a good start, but it's often misleading. It is frequently cluttered with items that don’t reflect the core, repeatable health of your business. The QoE process is built to find and adjust for these exact items.

Common adjustments include:

- One-Time Events: Did a huge, non-recurring government grant or a single massive client contract inflate last year's revenue? A QoE removes that outlier to show a more realistic baseline profit.

- Owner-Related Expenses: Those personal vacations, family member salaries, or luxury car leases you run through the business? Buyers won't have those costs, so a QoE "adds them back" to your profit, increasing your adjusted EBITDA.

- Accounting Methods: Many private companies use cash-basis accounting, which paints a distorted picture of profitability. A QoE almost always restates your financials on an accrual basis for a more accurate view of when revenue is actually earned. If you're not clear on the difference, you need to understand what accrual accounting means for your business.

"A QoE analysis investigates the sustainability and accuracy of earnings by adjusting for anomalies, non-recurring items, and inconsistencies. Unlike an audit, a QoE focuses on true operational cash flow—not GAAP compliance."

- Pioneer Capital Advisory

Getting this right is the difference between a smooth, successful exit and a painful, last-minute valuation cut. Understanding your quality of earnings gives you control over your financial narrative long before you ever step into a deal room. It’s not just for M&A—it’s about building a fundamentally stronger, more valuable business.

From Reported Profit to Real-World Value

Abstract formulas are useless in a deal room. Your valuation comes down to a single, defensible number—normalized EBITDA. Let's walk through a concrete example of a quality of earnings calculation for a fictional $5M ARR SaaS company to see how reported profit transforms into the number that actually matters.

Imagine your company’s P&L shows a healthy reported EBITDA of $1,000,000. You feel confident. But a buyer’s QoE analyst sees this as just a starting point. Their job is to apply a series of systematic adjustments to uncover the true, sustainable earnings of the business.

This process is why QoE reports are non-negotiable in M&A. Data from hundreds of transactions shows that QoE adjustments frequently reveal discrepancies averaging 15-25% between reported and sustainable EBITDA. In fact, a recent analysis of over 500 deals found that QoE adjustments reduced the purchase price in 68% of cases, with SaaS firms seeing the highest impact. You can explore the full findings of why QoE adjustments are so impactful on Windes.com.

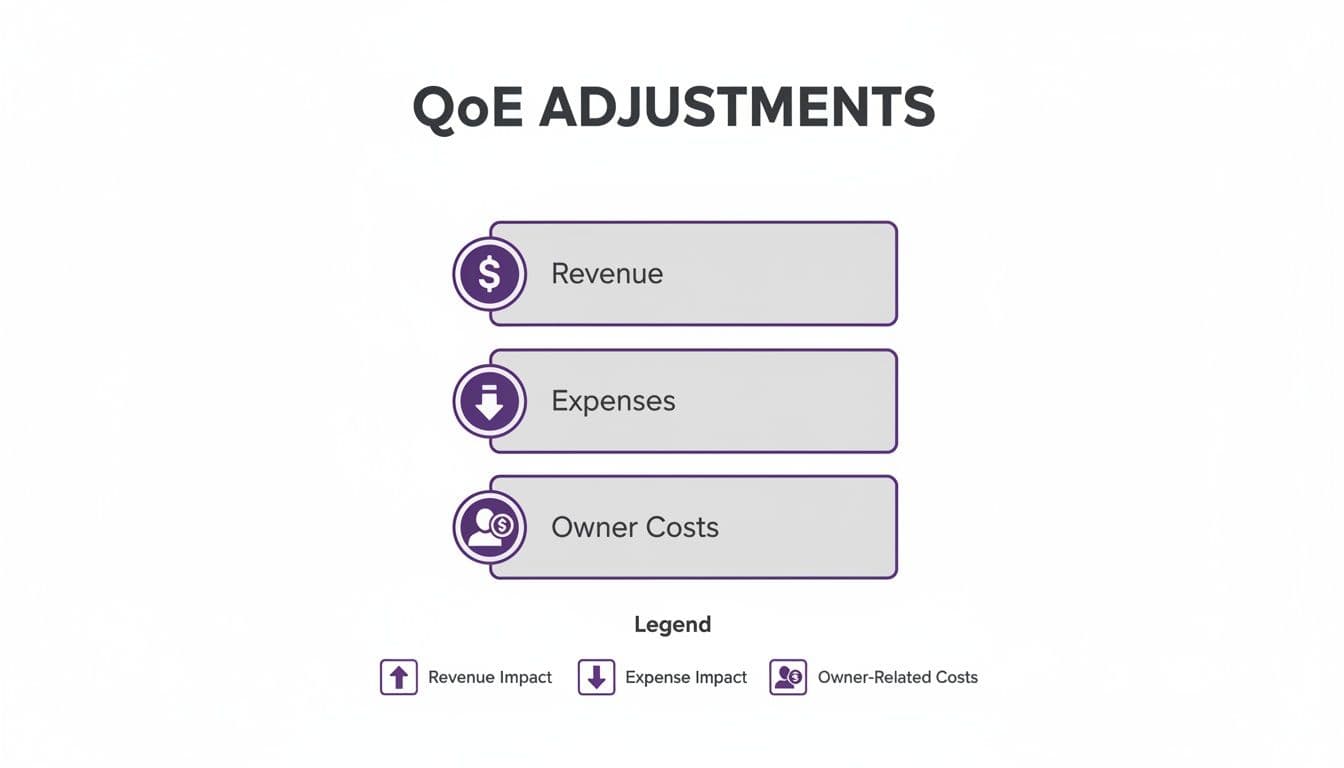

Building the Bridge to Normalized EBITDA

Here’s how an analyst would deconstruct that $1M reported figure. They'll scrutinize every revenue and expense line, sorting them into categories that represent the core, ongoing business—not one-time events or owner-specific costs.

The infographic below shows the three main buckets of adjustments that get made during a QoE review.

These adjustments aren't just about finding mistakes; they're about recasting your financials to predict future performance. Let's apply this thinking to our SaaS company's numbers.

A Step-by-Step QoE Calculation

Here is a breakdown of how a QoE analyst would transform your initial $1,000,000 EBITDA.

1. Adjusting for Non-Recurring Revenue Last year, you completed a large, one-time implementation project for a client outside your core SaaS offering, generating $200,000 in revenue. While great for cash flow, a buyer cannot count on this revenue repeating.

- Adjustment: Subtract $200,000 from EBITDA.

2. Adding Back Non-Recurring Expenses Your company went through a legal dispute that was settled and paid for last year. The total legal fees amounted to $150,000. Since this is a one-off event and not part of normal operations, it gets added back.

- Adjustment: Add back $150,000 to EBITDA.

3. Normalizing Owner-Related Expenses You expensed $100,000 in personal travel and entertainment through the company. A new corporate owner won't have these costs, so they aren't part of the business's core earnings. This is a classic "add-back" that increases your normalized profit.

- Adjustment: Add back $100,000 to EBITDA.

4. Correcting for Revenue Recognition (ASC 606) Here’s a big one for SaaS. Your team incorrectly recognized $120,000 from a new annual contract in a single month instead of spreading it out over 12 months ($10,000/month). The QoE analyst will correct this, moving $110,000 of that revenue out of the current period.

- Adjustment: Subtract $110,000 from EBITDA.

Let’s put it all together in a "bridge" table that clearly shows the path from reported to normalized EBITDA.

| Description | Amount | Running Total |

|---|---|---|

| Reported EBITDA | $1,000,000 | |

| 1. Non-Recurring Revenue Adj. | - $200,000 | $800,000 |

| 2. Non-Recurring Expense Add-Back | + $150,000 | $950,000 |

| 3. Owner Expense Add-Back | + $100,000 | $1,050,000 |

| 4. ASC 606 Revenue Recognition | - $110,000 | $940,000 |

| Normalized EBITDA | $940,000 |

After this process, your seemingly strong $1M in profit is now a more realistic normalized EBITDA of $940,000. While lower, this number is defensible, credible, and gives a buyer confidence in what they are acquiring.

A $60,000 adjustment might not seem catastrophic, but if a buyer applies a 10x multiple, that’s a $600,000 reduction in your company’s valuation. This is why mastering the details of your earnings quality is not just an accounting exercise—it's a direct driver of your final exit price.

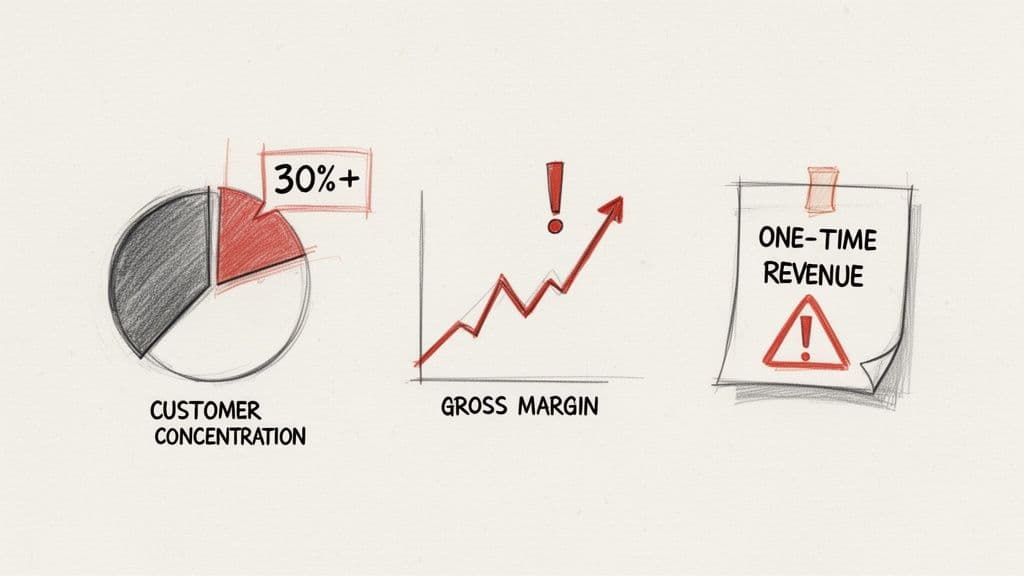

Red Flags That Kill Deals (and How to Fix Them)

A clean Quality of Earnings report accelerates your deal. A messy one stops it cold. During due diligence, QoE analysts are paid to find skeletons in your financial closet—risks a buyer will use to demand a lower price or simply walk away.

Think of this as your early warning system. Understanding these red flags gives you a massive head start. You can spot and fix the issues before they ever land on a buyer’s desk, protecting your valuation and keeping your deal on track. Here are the most dangerous red flags we see kill deals for businesses in your revenue range.

High Customer Concentration

Does one client make up 30% or more of your annual revenue? To a buyer, this is not a strong client relationship; it is an existential threat. If that single client leaves after the acquisition, the company's revenue—and the buyer's entire investment—craters.

- Benchmark: Top-quartile SaaS companies ensure no single customer accounts for more than 10% of ARR.

- Actionable Fix: Launch a targeted sales initiative to land 5-10 new mid-market clients over the next six months to diversify your revenue base. Incentivize your team on net new logo acquisition, not just account expansion.

Inconsistent or Declining Gross Margins

Your gross margin is the purest measure of your core profitability. A declining margin screams that you are losing pricing power, facing rising delivery costs, or wrestling with operational inefficiencies.

- Benchmark: According to OpenView's 2024 SaaS Benchmarks, the median gross margin for companies over $1M ARR is 78%. Best-in-class companies exceed 85%.

- Actionable Fix: Conduct a service-line profitability analysis. Identify which offerings have the lowest margins and re-price, productize, or eliminate them. Renegotiate vendor contracts and explore automation to reduce your cost of goods sold (COGS).

Heavy Reliance on One-Time Revenue

One of the main jobs of a QoE analysis is to strip out temporary, one-time revenue spikes. If a big chunk of your "growth" last year came from a single, non-recurring project, a government grant, or selling an asset, analysts will immediately pull it from their calculations. You see a banner year; the buyer sees a business with weaker core operations.

- Actionable Fix: Re-segment your P&L to clearly distinguish between "Recurring Revenue" and "Non-Recurring/Project Revenue." This shows you understand the difference and allows you to build a defensible narrative around your core, repeatable profit engine.

Aggressive Add-Backs and Contractor Dependency

Trying to add back the salary of your head of marketing is a non-starter. If the role is critical, the new owner must hire someone to fill it, making it a real business cost. This problem is especially common in agencies and services firms that lean heavily on freelancers, which hides the true cost of labor.

- Misconception: Many founders believe "all contractors are add-backs." This is false. A buyer will reclassify any contractor who functions like a full-time employee as a permanent cost.

- Actionable Fix: Review your top 5 contractors. If they have worked 30+ hours per week for over a year, a buyer will treat them as de facto employees. Decide now whether to convert them to full-time staff to stabilize your cost base or develop a plan to reduce reliance on them. Data from the St. Louis Fed shows how freelance labor volatility impacts earnings quality, and you can read more on how freelance labor volatility impacts earnings quality from the St. Louis Fed.

Messy books are the root cause of these red flags. The best defense is a good offense: getting your financials clean is non-negotiable. You can learn more about our professional QuickBooks cleanup services to get ahead of these issues.

How to Prepare for Your QoE Review

The worst time to think about your Quality of Earnings (QoE) is after you've signed a letter of intent. By then, it’s too late. You are playing defense on the buyer's field, by their rules, and you've already lost control of your company's financial story.

Proactive preparation is about seizing control. Getting QoE-ready lets you find and fix issues on your own terms, long before an investor sees your books. This transforms your company from a risky bet into a premium asset.

Your QoE Readiness Action Plan

Getting your business ready for this level of scrutiny is about building financial discipline into your company's DNA. Here’s a 6-month timeline to get you prepared for any transaction.

| Timeline | Key Actions & Focus | Outcome |

|---|---|---|

| Months 1-2 | Foundation & Cleanup: Close all open accounting periods and reconcile every historical transaction. If you're on cash-basis, begin the switch to accrual accounting. | A clean historical record and a 10-day month-end close. |

| Months 3-4 | Process & Systems: Implement a formal ASC 606 revenue recognition process. Start tracking every potential add-back (e.g., owner expenses, one-time legal fees) in a dedicated schedule with supporting documentation. | A defensible add-back schedule and a close time reduced to 7 days. |

| Months 5-6 | Reporting & Refinement: Build out KPI dashboards (MRR, churn, LTV) reconciled directly to your financial statements. Run a mock internal QoE to pressure-test your numbers and narrative. | A 5-day close and a bulletproof financial story ready for diligence. |

Investors and acquirers perform exhaustive M&A due diligence to uncover hidden issues. Handing them a clean, well-documented financial story puts you in a powerful position from day one.

"A QofE assessment is an in-depth earnings analysis that takes place during the M&A due diligence process. The goal is to clarify where a company’s earnings are coming from, how reliable those earnings have been historically, and whether current performance is likely to continue post-acquisition." – Embarc Advisors

This proactive approach turns the formal QoE from a stressful interrogation into a simple validation of the story you’ve already built. It's the single most powerful way to control your narrative and maximize valuation. If you're ready to get your financials in order, our guide on how to prepare for an audit offers more insights into building financial discipline.

Your Top QoE Questions, Answered

As a founder or CEO, you need straight answers, not financial jargon. Here are direct responses to the most common questions about the QoE process.

What is the difference between a QoE report and an audit?

Think of it this way: an audit looks backward, while a QoE looks forward.

An audit is a history report. Its job is to confirm that your past financial statements are accurate and follow the rules (like GAAP). It’s about compliance. An auditor's opinion tells a buyer your numbers are "correct."

A Quality of Earnings (QoE) report is an investigation. It stress-tests your financials to predict the future. The goal isn’t to check for accounting mistakes but to find a “normalized” EBITDA that a buyer can trust to forecast future cash flow. It answers the real question: how sustainable are these earnings?

Who pays for the QoE report?

Traditionally, the buyer pays for a “buy-side” QoE report as part of their due diligence.

However, smart sellers are flipping the script by commissioning their own “sell-side” QoE before going to market. This puts you in the driver’s seat. You find and fix financial issues on your own time, not under a deal clock. You control the narrative, frame the adjustments, and walk into negotiations from a position of strength with a pre-vetted financial package.

How long does a QoE analysis take?

Plan for 4 to 8 weeks. The single biggest factor that extends this timeline is the state of your books. If your financials are clean, organized, and you have documentation ready for any adjustments, the process is fast. If your records are a mess, the QoE team first has to act as forensic accountants just to clean things up. That’s more time, more questions, and a lot more cost—all of which erode buyer confidence.

Don't wait for due diligence to become a problem. Jumpstart Partners delivers the investor-ready financials and strategic finance leadership you need to control your narrative and maximize your valuation. We help businesses like yours build bulletproof financial operations that stand up to any scrutiny.

Schedule your free consultation today to learn how we can prepare your business for its next chapter.