Financial Operations

What Is Accrual Accounting: The Founder's Guide to Real Profitability

Learn what is accrual accounting and how it reveals your true financial picture while guiding smarter decisions.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readThat record-breaking sales month might be misleading you. It’s a classic trap: you see a huge cash deposit from an annual contract and assume you're crushing it, but your bank balance is telling a dangerously distorted story. Without a clear picture of your real profitability, you're flying blind—over-hiring in good cash months and cutting costs when you don't need to. This is the core problem with cash-basis accounting.

So, what is accrual accounting? It’s a non-negotiable accounting method for any scaling business that forces you to match reality. You record revenue only when you earn it and expenses when you incur them, giving you a true picture of your company’s health, regardless of when money moves.

Your Profit and Loss Statement Is Lying to You

As a founder or CEO, you live and die by your numbers. But what if your most trusted report—the profit and loss (P&L) statement—is the source of your worst decisions? For fast-growing SaaS, agency, and professional services firms, this isn't a risk; it's a common reality for anyone still using cash-basis accounting.

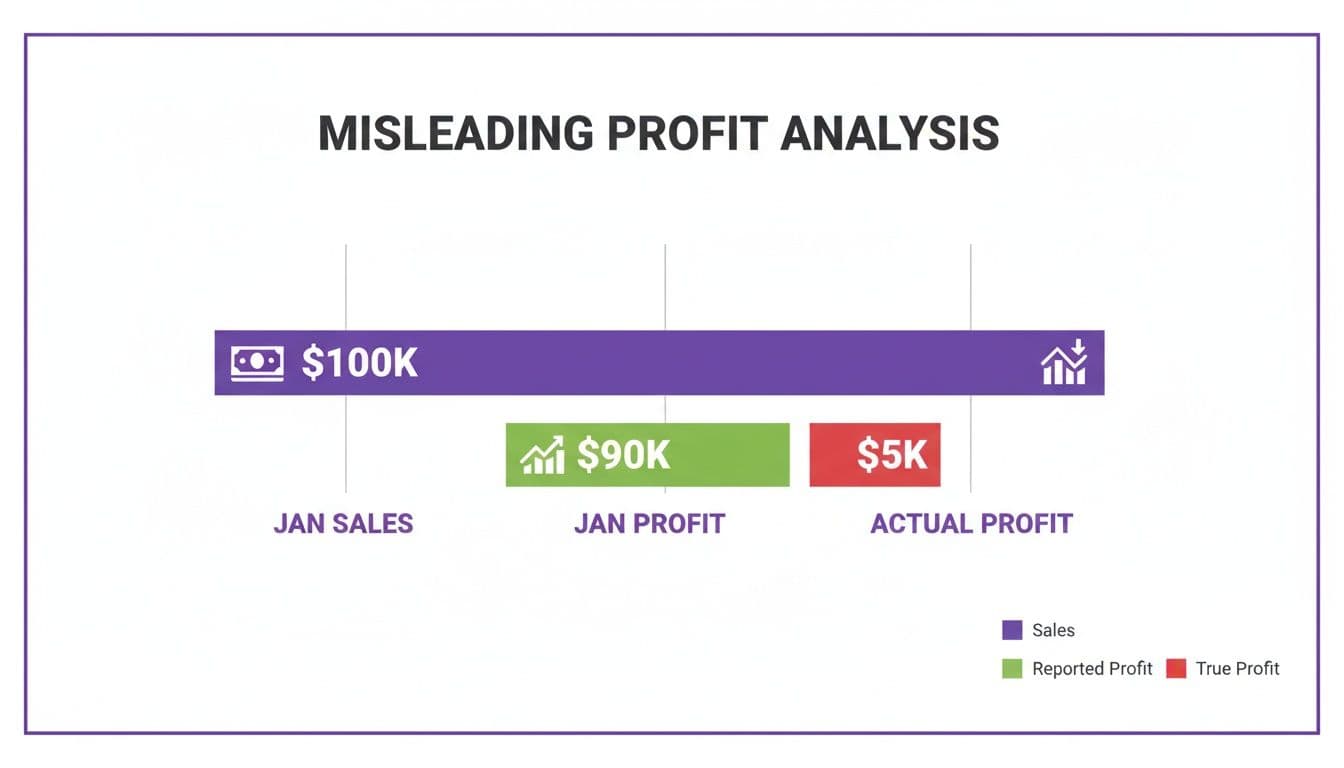

Picture this: You just closed a massive $120,000 annual SaaS contract in January. The full amount lands in your bank account, and your cash-basis P&L shows a spectacular profit spike. Feeling flush, you hire two new developers and greenlight a major marketing campaign.

But that celebration is dangerously premature. You didn't earn $120,000 in January. You have an obligation to deliver your service for the next 12 months to earn that money. By recognizing it all at once, you’ve created a fiction—a dangerously inflated view of your real profitability that leads to poor capital allocation.

The Hidden Dangers of Cash-Basis Reporting

Relying on cash-in-the-door financials almost always leads to bad strategic calls. You over-hire after a big cash injection, only to face a payroll crunch three months later. Or you slash vital costs during a tight cash month, even when your underlying growth is perfectly healthy.

This warped view creates serious operational risks:

- Misguided Hiring: You expand your team based on a one-time cash spike, then struggle to make payroll when that cash has to stretch over the next year.

- Flawed Unit Economics: You cannot accurately calculate true customer profitability, like Customer Acquisition Cost (CAC) or Lifetime Value (LTV), if your revenue and expenses aren't properly matched to the same time period.

- Investor Red Flags: Showing up to a pitch with cash-basis financials tells savvy investors you don't have a real handle on your business performance. It's an immediate credibility killer.

For a deeper look at how to manage this correctly, explore our guide on profit and loss management for more actionable insights. The foundation for accurate reporting starts with understanding profit and loss statements through the lens of accrual principles.

Accrual Versus Cash Accounting: A Practical Comparison

Let’s set the theory aside and look at a real-world comparison. The difference between accrual and cash accounting isn't an academic exercise—it completely changes how you see your company's performance and make critical business decisions.

It all comes down to timing.

Cash accounting is simple: you record revenue when money hits your bank account and expenses when money leaves. Accrual accounting is more sophisticated, painting a truer picture of your business's health. You record revenue when you earn it and expenses when you incur them, regardless of when cash actually changes hands.

Cash vs. Accrual Accounting For a $120,000 Annual Contract

Imagine your SaaS company signs a $120,000 annual contract, and the client pays the full amount upfront in January. Here's how each method reflects this on your monthly profit and loss statement.

| Month | Cash Basis Revenue | Accrual Basis Revenue | Business Implication |

|---|---|---|---|

| January | $120,000 | $10,000 | Cash basis shows a massive, misleading profit spike. Accrual basis reflects one month of earned revenue. |

| February | $0 | $10,000 | Cash basis shows zero revenue, creating a false "down month." Accrual shows stable, predictable performance. |

| March | $0 | $10,000 | The pattern continues, with accrual providing a consistent view of your actual earnings. |

| ...through December | $0 | $10,000 | By year-end, both methods have recorded the same total revenue, but only accrual provided an accurate monthly picture. |

This table makes the distinction crystal clear. With cash accounting, your P&L looks like a roller-coaster that doesn’t reflect your operational reality. With accrual accounting, you get a stable, realistic view of your profitability month after month.

This is exactly why looking at a single month's sales on a cash basis can be so dangerously misleading.

While the January sales number looks incredible, the real profit after accounting for the full year of service costs tells a completely different story. This is precisely why investors, auditors, and GAAP (Generally Accepted Accounting Principles) all insist on accrual financials. It’s about accuracy and predictability, not just tracking bank deposits.

The engine driving accrual accounting is the matching principle.

The matching principle insists that you recognize revenue as you earn it and match it with the expenses incurred in that same period to generate that revenue. This provides the only true measure of profitability.

For you as a founder or executive, this means you can finally trust your financial reports to make strategic decisions. Understanding this is also a core part of effective financial modeling. For a closer look at how this impacts your financial planning, check out our cash flow forecasting guide for more detailed strategies.

How Accrual Accounting Works in the Real World

Theory is one thing, but seeing accrual accounting in action makes the concept click. Let's walk through two common scenarios you face in a SaaS or services business to see how these principles play out on your actual financial statements.

These examples demystify how core concepts like deferred revenue and prepaid expenses translate into the numbers you show investors and use to make decisions.

This process gives you a true measure of your company's performance and obligations each month, not just a snapshot of your bank balance. Understanding the timing of revenue and expenses is key, and concepts like deferred revenue income examples are central to getting it right.

Example 1: SaaS Revenue Recognition (Deferred Revenue)

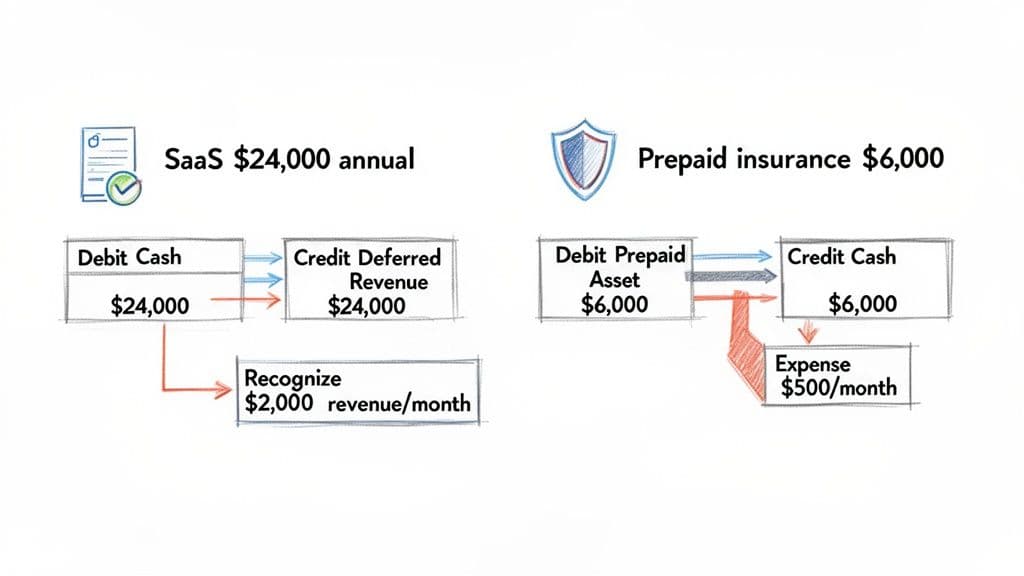

Your SaaS company signs a new customer to a $24,000 annual contract on January 1st. They pay the full amount upfront.

On a cash basis, your January books would show a massive—and misleading—$24,000 revenue spike. Accrual accounting fixes this.

-

Record the Cash and Liability: When the $24,000 cash hits your bank, you don't record it as revenue. Instead, you create a liability on your balance sheet called deferred revenue. This represents the money you’ve collected but haven’t yet earned.

- Initial Entry (January 1):

- Debit (increase) Cash: $24,000

- Credit (increase) Deferred Revenue: $24,000

- Initial Entry (January 1):

-

Recognize Earned Revenue Monthly: At the end of each month, you make an adjusting entry to recognize the portion of revenue you’ve actually earned by delivering one month of service ($24,000 / 12 months = $2,000/month).

- Monthly Adjusting Entry (End of Jan, Feb, Mar, etc.):

- Debit (decrease) Deferred Revenue: $2,000

- Credit (increase) Earned Revenue: $2,000

- Monthly Adjusting Entry (End of Jan, Feb, Mar, etc.):

You repeat this exact entry every month for the entire year. Your Profit and Loss statement now shows a stable, predictable $2,000 in monthly recurring revenue from this customer, painting an accurate picture of your business's health. For a deeper dive, check out our guide on what is deferred revenue.

Example 2: Prepaid Expense Amortization

Now let's flip to the expense side. Your professional services firm prepays its annual liability insurance for $6,000 on January 1st.

Expensing the full $6,000 in January would artificially crush your profitability for the month. Instead, you record it as a prepaid expense, which is an asset on your balance sheet. This asset represents the value of the insurance coverage you'll benefit from all year long.

-

Record the Asset:

- Initial Entry (January 1):

- Debit (increase) Prepaid Insurance: $6,000

- Credit (decrease) Cash: $6,000

- Initial Entry (January 1):

-

Expense the Asset Over Time: As each month passes, you "use up" one month's worth of that coverage. You record this by moving a portion of the asset over to an expense on your P&L ($6,000 / 12 months = $500/month).

- Monthly Adjusting Entry (End of Jan, Feb, Mar, etc.):

- Debit (increase) Insurance Expense: $500

- Credit (decrease) Prepaid Insurance: $500

- Monthly Adjusting Entry (End of Jan, Feb, Mar, etc.):

This matching of expenses to the period they benefit is the soul of accrual accounting. It's a global standard for a reason. A 2024 World Bank report notes that while only 30% of governments globally have fully adopted accrual principles, adoption in high-income nations is at 55%, signaling its importance in major markets. You can read the full research about public sector accounting standards.

Why Accrual Accounting Is Non-Negotiable for Scaling

If you have any real intention of scaling your business, switching to accrual accounting isn't an "option"—it’s a foundational requirement. Trying to steer a growing company with cash-basis books is like navigating a ship with a broken compass. You feel motion, but you have no real idea where you're headed.

This is about building a company that can attract capital, make intelligent decisions, and sustain its growth. Investors and lenders simply will not take you seriously without GAAP-compliant, accrual-basis financials. They need to see a true picture of your company's health, not just the temporary highs and lows of your bank account.

See Your Business Through an Investor’s Eyes

Imagine walking into a due diligence meeting and sliding cash-basis financials across the table. You've just raised your first, and biggest, red flag.

“When a scaling SaaS company presents cash-basis financials during due diligence, it's an immediate red flag. It tells me they don't have a true handle on their unit economics or recurring revenue model. We can't invest without clear, accrual-based visibility into their performance.” – Jane Doe, Partner at ScaleUp Ventures

Investors need to see predictable revenue streams and a clear path to profitability. Cash accounting completely hides this reality. Without understanding what is accrual accounting, you cannot calculate your most critical growth metrics with any accuracy.

According to OpenView’s 2024 SaaS Benchmarks, top-quartile companies are intensely focused on metrics that are only possible to track with accrual accounting. These essential SaaS and service metrics are impossible to track correctly on a cash basis:

- Monthly Recurring Revenue (MRR): An annual payment looks like a massive one-time revenue spike, not a recurring stream.

- Annual Recurring Revenue (ARR): The lifeblood of any subscription business, which requires monthly recognition to be meaningful.

- Customer Lifetime Value (LTV): This requires matching revenue over a customer’s lifetime against the cost to acquire them.

- Churn Rate: You can't track churn accurately if you don't know when revenue was supposed to be recognized each month.

The Foundation for Compliance and Strategy

Beyond metrics, growing businesses must comply with ASC 606, the official revenue recognition standard. This standard is fundamentally built on accrual principles, forcing you to recognize revenue as you deliver on your promises to the customer. If you ever plan to undergo an audit, non-compliance isn't an option.

Ultimately, accrual reporting is what empowers you to see the real profitability of your services, products, and customer segments. This clarity fuels smarter strategic decisions that drive real growth—a process that can be radically improved with the right systems in place. You can learn more about how to streamline your reporting with financial reporting automation.

Warning Signs: Red Flags in Your Accrual Migration

Making the switch from cash to accrual accounting is a huge step toward financial maturity. But the transition is filled with landmines. A messy migration can corrupt your historical data and make your financial reports useless for months, defeating the entire purpose of the switch.

Here are the most common red flags to watch for.

Red Flag #1: Mishandling Deferred Revenue and Prepaid Expenses

The most frequent errors pop up when companies fail to apply accrual principles correctly. These mistakes directly warp your profitability.

-

Improperly Booking Deferred Revenue: You land a $60,000 annual contract and get the cash upfront. It’s incredibly tempting to book that entire amount as revenue right away. The correct move is to record it as a liability (deferred revenue) on your Balance Sheet and then recognize just $5,000 in revenue each month. If you don't, you'll drastically overstate your near-term profit, which might trick you into over-investing in hiring or marketing based on phantom income.

-

Violating the Matching Principle: A classic mistake is expensing the entire $12,000 cost of an annual software subscription in the month you pay for it. The matching principle demands that you amortize this cost at $1,000 per month over the year, matching the expense to the period you receive the benefit. Failing to do so creates a volatile and completely inaccurate P&L.

Red Flag #2: A Messy or Undefined Cut-Over Process

One of the most damaging mistakes is simply executing a poor transition process. This happens when there isn't a firm cut-over date or a clear plan for converting existing cash-basis data into the accrual world.

The result? A corrupted financial history where old cash-based numbers get jumbled up with new accrual-based entries. This makes any kind of year-over-year or even quarter-over-quarter analysis totally impossible. Your financial reports become unreliable.

“A messy cut-over process is one of the biggest risks. Without a clean, well-documented transition, you lose the ability to compare historical and current performance, effectively blinding you to your own growth trends.” — John Carter, Fractional CFO

Failing to get this right doesn't just frustrate your finance team; it puts the business at risk. If you present corrupted financials during a funding round or an audit, you will immediately lose all credibility. The transition has to be handled with precision, which is why a structured approach is essential and why a clean month-end close best practices is critical.

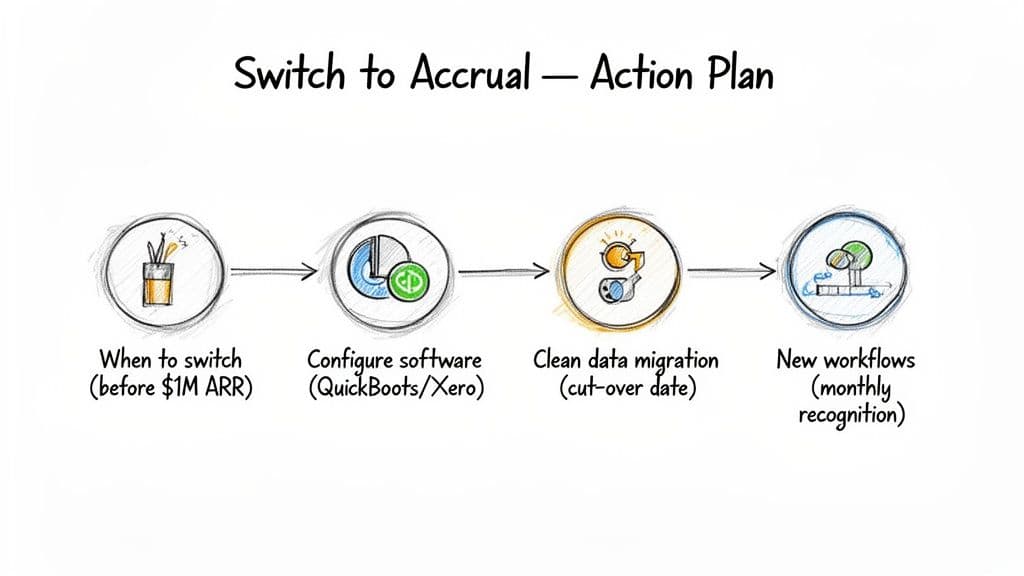

Your 4-Step Action Plan to Implement Accrual Accounting

Ready for financials that give you true clarity? Switching to accrual accounting is a strategic upgrade for your company's future. It delivers the investor-ready reports and sharp operational insights needed to scale, and making the move doesn't have to be a painful overhaul if you follow a clear roadmap.

This plan breaks the entire process down into four manageable steps.

A Four-Step Implementation Roadmap

Executing a smooth migration comes down to precision and planning. Here are the essential steps to get it right.

| Step | Action | Why It's Critical |

|---|---|---|

| 1. Pinpoint the Right Time | Switch before you hit $1M in ARR or start a serious fundraising round. | Proactively migrating prevents a rushed, chaotic transition forced by investors or auditors. It gives you control over the process. |

| 2. Configure Your Software | Set up your chart of accounts in QuickBooks Online or Xero to include Deferred Revenue, Prepaid Expenses, and Accrued Expenses. | The software is built for accrual, but it's not plug-and-play. Correct configuration is the technical foundation for accurate reporting. |

| 3. Execute a Clean Data Migration | Pick a firm cut-over date (e.g., the first day of a new quarter). All transactions after this date will be recorded using accrual principles. | This simple rule preserves your historical data integrity and prevents a messy overlap that corrupts your financial trend analysis. |

| 4. Build New Workflows | Create documented processes for your team to track contracts, recognize revenue monthly, and amortize prepaid expenses systematically. | Accrual accounting is an ongoing process, not a one-time setup. Disciplined workflows ensure your data remains accurate and reliable. |

"Implementing accrual accounting is more than a bookkeeping change; it's a fundamental upgrade to your company's operational infrastructure. It unlocks the ability to see your business with the clarity that investors demand and that sustainable growth requires." — Emily Hayes, CPA & Financial Strategist

Following this structured plan is your next step to achieving financial clarity and making your business truly investor-ready.

Common Objections and Misconceptions

As a founder, you're rightfully protective of your time and resources. Migrating to accrual accounting can feel like a complex, "nice-to-have" project. Let's address the common objections we hear.

"We're too small for this—it seems overly complicated."

This is a common misconception. If you sell annual contracts or have multi-month service agreements, you're already facing the exact problems accrual accounting solves. The complexity of accrual accounting is far less than the complexity of making bad business decisions based on flawed cash-basis data. The "right" time to switch is always earlier than you think—ideally before you hit $1M in ARR.

"Cash is king. I just need to know what's in the bank."

Knowing your cash position is critical, but it's only half the story. A healthy bank balance today can mask an unprofitable business model that will collapse in six months. Accrual accounting doesn't replace cash flow management; it complements it. You need both: an accrual P&L to understand your true profitability and a Statement of Cash Flows to manage liquidity.

"Can't I just do this myself in QuickBooks?"

While platforms like QuickBooks Online support accrual accounting, the migration process itself is fraught with risk. A single error in setting up deferred revenue schedules or amortizing expenses can corrupt your data for months. Getting it right requires expertise in GAAP, particularly ASC 606 revenue recognition standards. This is not a "figure it out as you go" task.

Ready to get investor-ready financials and a true picture of your profitability? Don't let flawed data dictate your strategy. Schedule a consultation with Jumpstart Partners today and let our expert team migrate you to accrual accounting in weeks, not months.