Financial Operations

Reconciliation Services: Fix Slow Month-End Closes

Learn how reconciliation services streamline month-end closes. A CEO's guide to KPIs, outsourcing, & vetting financial providers for 2026 success.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readIt's the 15th. Your bookkeeper says the numbers are “almost done.” Your controller is still chasing Stripe payouts, payroll entries, and a bank feed that duplicated transactions. You're in a leadership meeting making decisions on hiring, pricing, and runway with financials you don't trust.

That's not a reporting problem. It's a reconciliation problem.

For growing SaaS firms, agencies, and service businesses, bad reconciliation creates a chain reaction. Revenue gets misstated. Cash looks better or worse than it is. Expenses sit in suspense accounts. Deferred revenue schedules drift away from billing reality. Then everyone acts surprised when the month-end close drags, margins look strange, and investors start asking sharper questions.

The market for “reconciliation services” doesn't help. Search results often point to nonprofit social-service organizations instead of practical finance support, which leaves founders with a naming problem before they even get to the operational one, as shown by this example of non-financial Reconciliation Services content. If you came here looking for accounting help, you're in the right place.

Table of Contents

- Your Month-End Close Is Broken Here Is Why It Matters

- What Are Financial Reconciliation Services Really

- The Three KPIs That Measure Reconciliation ROI

- In-House vs Outsourced A Decision Framework

- Your Checklist for Vetting Reconciliation Providers

- Pricing Expectations and Real-World Outcomes

- How to Achieve a Five-Day Close

Your Month-End Close Is Broken Here Is Why It Matters

A founder I talk to every month lives the same version of this story. Sales says revenue is strong. Operations says margins are tight. The bank balance looks healthy enough. But nobody can answer a basic question with confidence: what happened last month?

When your close is slow, you don't just lose time. You lose the ability to act. You delay hiring decisions. You keep underperforming clients too long. You overspend because cash feels available before liabilities are fully posted. Then you discover corrections after the fact, when fixing them is more painful and more expensive.

The real bottleneck is reconciliation

Most leadership teams blame “accounting lag.” That diagnosis is too vague. The issue is usually that your records across QuickBooks, Xero, Stripe, Shopify, Gusto, credit cards, and bank accounts don't agree. If those systems don't match, your P&L is a draft, not a management tool.

Historically, businesses were expected to reconcile monthly, while larger or higher-volume organizations may need weekly or daily reconciliation according to guidance on reconciliation frequency. That matters because your business now moves faster than the old monthly rhythm. Subscription billing, auto-renewals, card failures, refunds, contractor payouts, and software spend don't wait for your accounting team to catch up.

Practical rule: If you're making operating decisions before reconciliation is complete, you're managing on assumptions.

A better close starts with a tighter workflow. If you need a useful companion read on process design, this guide to month-end close best practices is worth reviewing alongside your reconciliation cleanup.

Delayed financials create avoidable leaks

Founders usually notice the close problem in one of three ways:

- Cash confusion: You have money in the bank, but you can't explain upcoming obligations cleanly.

- Margin distortion: Revenue is posted, but fees, refunds, and payroll timing haven't been fully matched.

- Decision drag: You wait too long to see trends, then react too late.

This issue shows up outside tech too. Organizations trying to improve church financial stewardship face the same core discipline: the close only works when underlying accounts are reconciled, reviewed, and tied to real activity.

Reconciliation services fix that foundation. They turn messy transaction flow into reliable financial reporting. That's why they matter.

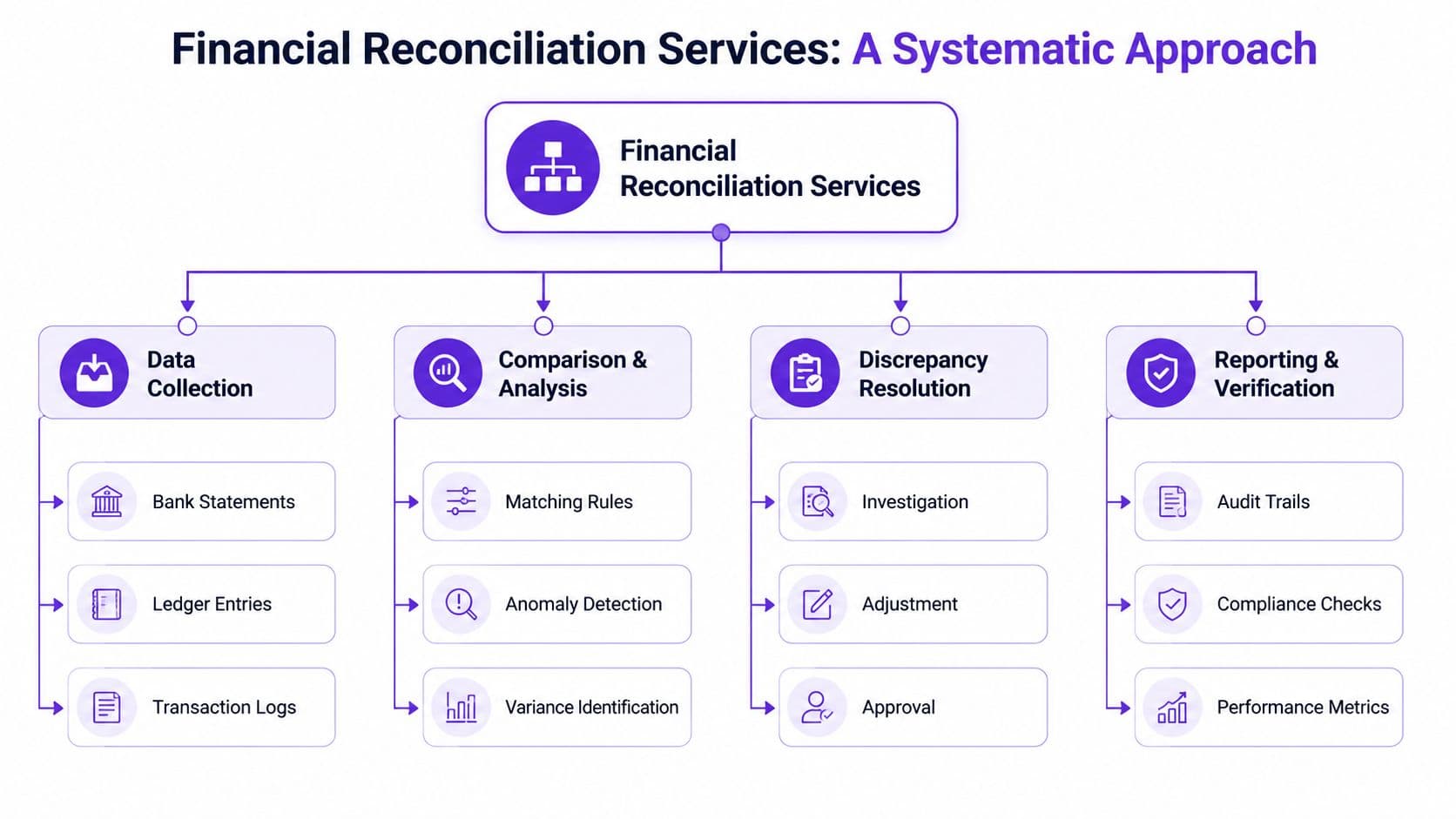

What Are Financial Reconciliation Services Really

Financial reconciliation services are the operating discipline that makes your books line up with reality. At the simplest level, they compare what your accounting system says happened against what banks, payment processors, payroll systems, and other source records say happened.

Think of it as balancing a personal checkbook, except your company has multiple bank accounts, recurring subscriptions, processor fees, accruals, payroll journals, and revenue schedules. The principle is the same. The complexity isn't.

What you are actually reconciling

For most businesses in the $500K to $20M range, reconciliation services usually cover these core areas:

| Area | What gets matched | Why it matters |

|---|---|---|

| Bank accounts | General ledger cash entries to bank statements | Confirms cash is real and complete |

| Credit cards | Card statements to expense postings and receipts | Catches missing expenses, duplicates, and miscoding |

| Payment processors | Stripe, Shopify, Square, or similar activity to recorded sales, fees, refunds, and payouts | Prevents overstated revenue and unexplained cash gaps |

| Payroll | Payroll reports to wage, tax, and benefit entries | Avoids payroll liability mistakes |

| Revenue | Contracts, invoices, billing systems, and revenue schedules to the ledger | Keeps earned revenue separate from billed revenue |

If you want a tactical walkthrough of the most basic piece, review this guide on how to reconcile bank accounts. Founders often underestimate how many downstream reporting errors start with that one account failing to tie out.

Why this becomes painful as you grow

Manual reconciliation doesn't break all at once. It breaks gradually, then suddenly. One extra bank account becomes three. One Stripe account becomes multiple entities, products, or geographies. Revenue rules get more nuanced. Refunds, credits, and failed payments pile up.

That's why scale changes the conversation. A typical 1,000-person company spends about 100,000 person-hours per year on account reconciliation, and automated reconciliation systems can cut close times by up to 70% according to Resolve's reconciliation operations benchmark. You don't need to be a 1,000-person company to learn the lesson. Reconciliation becomes a cost center long before it becomes a board-level topic.

Good reconciliation services don't just “match transactions.” They create a repeatable control system for cash, revenue, expenses, and reporting integrity.

There's also a technical side that matters more than most finance leaders realize. In data workflows, reconciliation can involve matching records even when labels are inconsistent or ambiguous. The W3C Reconciliation Service API specification describes reconciliation as a protocol that helps consumers match their data to provider entities, including ranked candidate matches when exact string matches fail. That's not accounting guidance, but it captures something useful. Modern reconciliation is an entity-resolution problem as much as a bookkeeping one.

If your systems don't agree, your financials won't either. Reconciliation services exist to force agreement, document exceptions, and close the books faster.

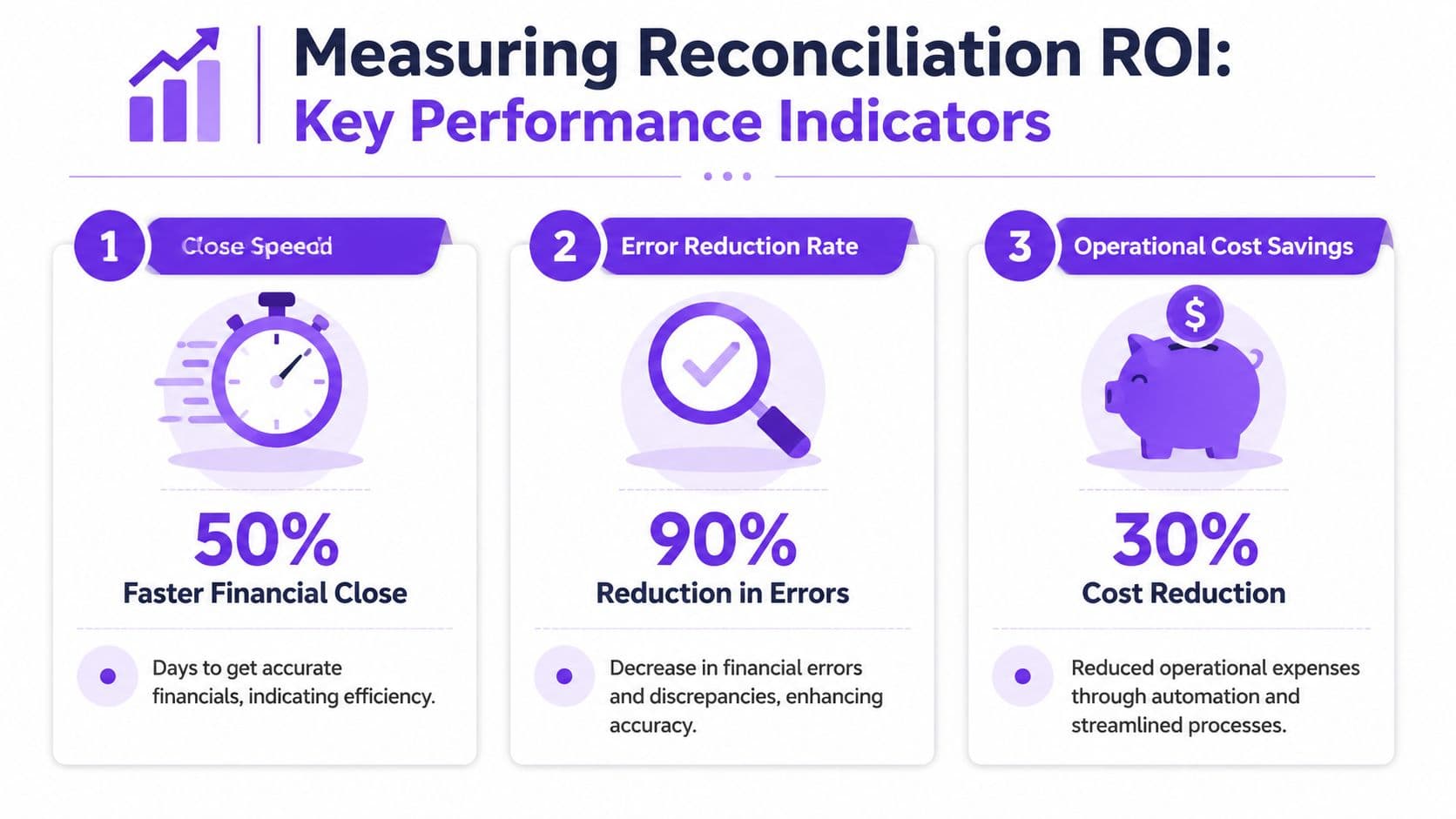

The Three KPIs That Measure Reconciliation ROI

Most finance teams track tasks. Founders should track outcomes. If you're paying for reconciliation services, judge them on three things: how fast you close, how clean the data is, and how much financial leakage gets found.

KPI one close speed

This is the headline metric. How many business days pass before you have accurate financials you can use?

Here's a simple worked example. Say your team currently closes in 15 days and wants to get to 5 days. That improvement gives you 10 additional decision-making days each month.

Over a year, that's:

- 10 days regained per month

- 12 months per year

- 10 × 12 = 120 days regained annually

That doesn't mean you “create” 120 new calendar days. It means leadership gets 120 more days per year with usable, current financial information instead of stale numbers. If you run weekly leadership meetings, that difference changes the quality of every pricing, hiring, spend, and cash decision you make.

If you're building executive reporting around the close, this piece on financial dashboards and CEO metrics is the right next step. A dashboard is only useful if reconciled data feeds it.

KPI two accuracy and exception volume

I care less about abstract “accuracy rate” language and more about unresolved exceptions. You want a shrinking list of items that require manual investigation.

Track questions like these:

- Unmatched cash entries: How many ledger cash transactions don't tie to statement activity?

- Processor gaps: How many payouts, fees, refunds, or chargebacks remain unexplained?

- Recurring reclasses: Which errors repeat every month because the upstream workflow is broken?

When this list is short, your close is under control. When it keeps rolling forward, your team is doing cleanup, not accounting.

For e-commerce businesses especially, reconciled data is what makes downstream analysis worth trusting. If you're thinking beyond bookkeeping into channel performance, SKU margin, and fee visibility, this overview of e-commerce reporting and analytics is a useful operational complement.

KPI three error detection value

This is the most ignored metric. Strong reconciliation doesn't just support reporting. It finds money.

Use a direct calculation. If your team identifies:

- 3 duplicate software charges

- 2 missed customer billings

- 4 misclassified contractor or reimbursement items

- 1 processor mapping error affecting revenue timing

Then add the dollar value of each issue discovered and corrected. That total is your error detection value.

Management lens: If reconciliation only produces “clean books” but never surfaces root-cause issues, the process is too shallow.

You don't need a fancy model here. Keep a running log of discrepancies found, who fixed them, whether cash was affected, and whether the issue was one-time or systemic. Over a few closes, you'll know whether your provider is merely matching transactions or actively protecting margin.

The right KPI set is boring on purpose. Faster close. Fewer unresolved exceptions. More leakage caught early. That's ROI.

In-House vs Outsourced A Decision Framework

It is the third business day of the month. Your head of finance is still chasing Stripe timing differences, a payroll liability does not tie out, and the board packet is waiting on one person who also handles AP. That is not a staffing plan. It is a single point of failure.

The in-house versus outsourced decision is not about preference. It is about whether your reconciliation workload matches the team, controls, and review structure you have today. Growing tech and service businesses usually wait too long to answer that forthrightly. They keep reconciliation in-house because the work feels close to the business. Then volume rises, systems multiply, and close quality slips before anyone admits the model broke.

Cadence is usually the turning point. Once bank activity, processor volume, payroll changes, and deferred revenue activity need attention during the month instead of after it, the role stops being a side duty. It becomes an operating function with defined ownership, review, and escalation.

A practical comparison

| Decision factor | In-house | Outsourced |

|---|---|---|

| Team structure | Often one person handles preparation, posting, and review | Separate responsibility for prep, review, and exception handling |

| Coverage | PTO, turnover, and hiring delays slow the close | Team coverage reduces single-person dependency |

| Process quality | Varies with internal experience and discipline | Usually built around documented workflows and recurring checklists |

| Scalability | Capacity expands only after you hire and train | Service can expand faster as transaction volume grows |

| Founder attention | Leaders spend time chasing missing items and clarifying numbers | Leaders spend time reviewing outcomes and approving decisions |

Use a simple rule. Keep reconciliation in-house if you have a controller-level owner, documented account checklists, a real review layer, and transaction complexity that your team can clear without heroics. Outsource if one person is carrying the process, close timing depends on overtime, or your books rely on manual tie-outs across multiple systems.

The break point often shows up first in commerce and subscription workflows. If your team has to pull Amazon settlements, processor exports, billing reports, and bank activity into spreadsheets just to understand cash, the process is already too manual. Teams that sync Amazon data with Google Sheets can speed up analysis, but integration alone does not fix reconciliation. Someone still needs to own mapping, exception review, and close accountability.

If you are weighing the broader operating model, this guide to finance and accounts outsourcing is useful for evaluating what belongs inside your team and what should sit with an external finance partner.

Control quality matters more than location. The U.S. Treasury describes reconciliation as a control process used to compare balances and transaction activity across systems against authoritative records in its overview of agency reconciliations. That principle applies directly to your business. Reconciliation is how you prove completeness and accuracy. It is not clerical cleanup.

A short explainer can help frame the tradeoffs before you decide:

Red flags your current process is failing

You do not need a consultant to spot this. Check for these signs:

- Reports change after close: Revenue, cash, or expense numbers move after management has already reviewed them.

- One person controls too much: The same employee imports data, books entries, reconciles accounts, and signs off on the result.

- Cash from processors never clears cleanly: Stripe, Shopify, or other payout activity needs a custom explanation every month.

- Balance sheet accounts drift: Bank accounts get reconciled, but clearing accounts, payroll liabilities, credit cards, and deferred revenue sit unresolved.

- Questions pile up in Slack or email: The team cannot tell whether a discrepancy is timing, mapping, or a real error.

- Month-end depends on memory: Steps live in someone's head instead of a documented checklist with deadlines and reviewers.

If your close depends on one employee remembering what to check, you do not have a process. You have risk.

My recommendation is straightforward. Build in-house only if you are willing to fund the right level of finance leadership, documentation, and review discipline. Otherwise, outsource reconciliation before weak controls turn into misstated reporting, missed billing, or cash surprises. The cheapest option is rarely the one with the lowest cost.

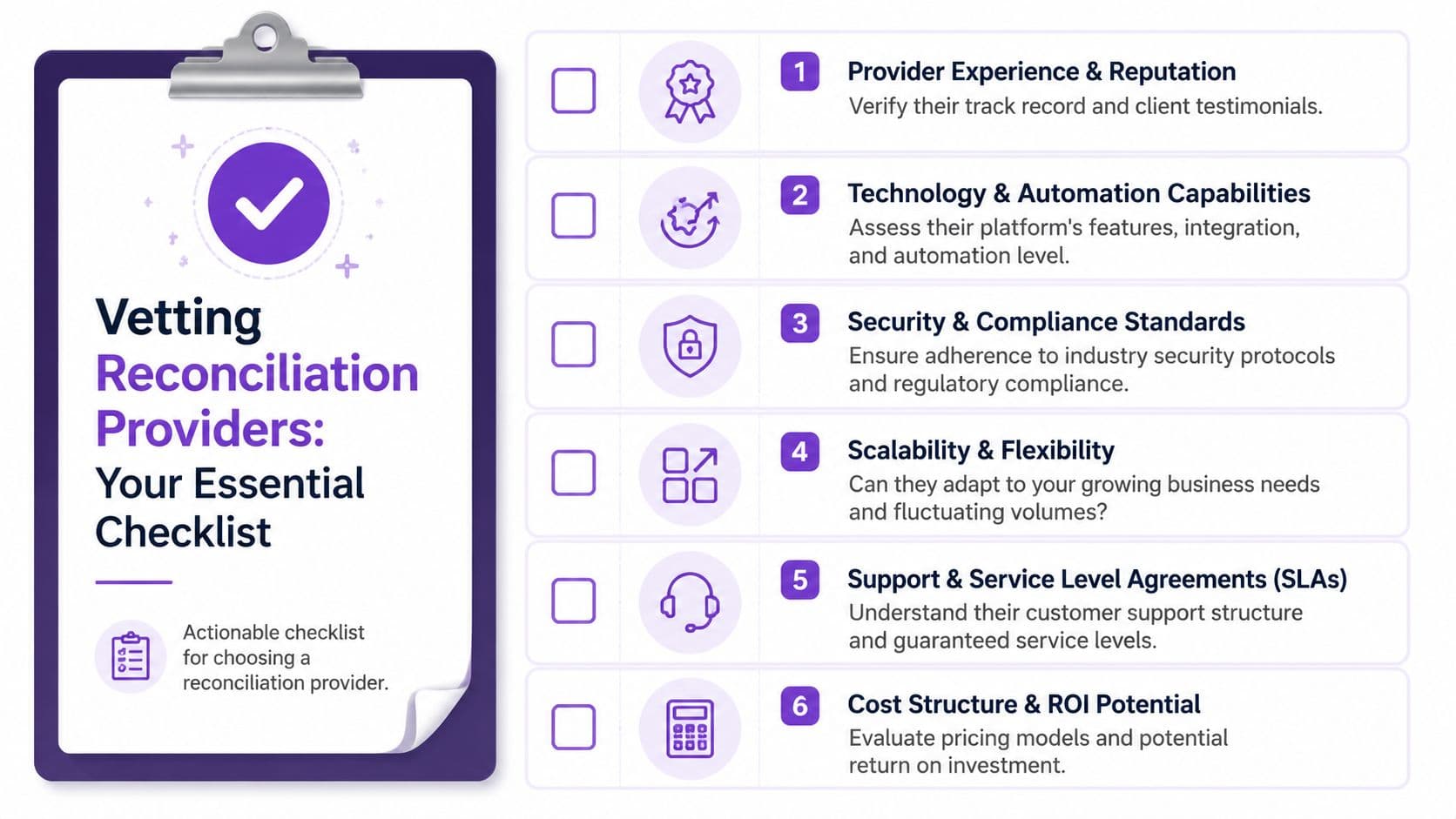

Your Checklist for Vetting Reconciliation Providers

It is the third business day of the month. Your team is asking whether cash is right, a processor balance still does not tie out, and nobody can tell you if the problem is timing, mapping, or a real error. That is the moment you find out whether you hired a reconciliation provider or just outsourced data entry.

Start with one question: how do you keep bad numbers from reaching management reporting? Price matters, but control matters first. If a provider cannot explain how errors are prevented, reviewed, and fixed, keep looking.

Core requirements

Use this checklist to separate firms that close books cleanly from firms that just clear tasks.

- Security controls: You are handing over access to bank feeds, payroll, payment processors, and the general ledger. Require role-based access, approval rules, documented data handling, and a clear process for removing access when staff changes.

- System competence: Your provider should know the systems that create your accounting reality. QuickBooks, Xero, NetSuite, Stripe, Shopify, Square, Gusto, Bill, Ramp, and payroll platforms all create different failure points.

- Close cadence: “Monthly support” is too vague. Get a written schedule for daily, weekly, and month-end reconciliations based on your transaction volume and cash risk.

- Exception resolution: Ask how breaks are logged, aged, assigned, approved, and closed. Old reconciling items are not harmless. They hide billing errors, duplicated expenses, stale liabilities, and missing cash.

- Close ownership: Require a committed close timeline, defined deliverables, and a named owner for unresolved items. If nobody owns the carryforward list, it becomes permanent.

- Review discipline: Preparation and review must sit with different people. You are buying independent review, not one person checking their own work.

Test them with a messy real-world example. If your operations team still exports files by hand or tries to sync Amazon data with Google Sheets to patch reporting gaps, ask the provider to walk you through import validation, field mapping, duplicate detection, and version control. A strong firm answers in steps. A weak one talks in generalities.

Questions to ask before you sign

Use blunt questions. You are hiring this firm to reduce financial leakages and shorten the close, not to sound polished in a sales call.

| Question | Strong answer sounds like | Weak answer sounds like |

|---|---|---|

| How do you handle unreconciled items? | A documented workflow with aging, escalation, and root-cause correction | “We review them at month-end” |

| Which systems do you reconcile most often? | Specific platforms, transaction patterns, and examples of common breaks | Generic accounting terminology |

| Who reviews the work before close is issued? | Named reviewer, signoff steps, and evidence retained in workpapers | “Our team reviews everything” |

| What happens if an error is found after close? | A defined correction process, ownership, and communication standard | “It depends on the issue” |

| How do you scale as our volume grows? | A staffing plan, revised cadence, and tooling changes tied to volume | “We should be able to handle it” |

Advisor view: If you do not test a provider's controls before signing, you are paying to move the same risk outside your company.

One option in this market is Jumpstart Partners, which offers outsourced controller and bookkeeping support for growing businesses and includes reconciliation within that workflow. The relevant question is not the brand. It is whether the provider can prove process depth, review discipline, system integration, and accountability when something breaks.

Choose the firm that can give you a faster close and fewer surprises on the balance sheet. Everything else is sales polish.

Pricing Expectations and Real-World Outcomes

Pricing for reconciliation services varies based on transaction volume, entity count, system complexity, revenue recognition needs, and how broken the books are when the provider starts. Expect pricing models to fall into three buckets: fixed monthly support, tiered service plans, or project-based cleanup plus ongoing monthly work.

The wrong way to buy is to compare providers as if they're all doing the same job. They aren't. Some are handling bank recs only. Others are tying out cash, cards, payroll, processor activity, accruals, deferred revenue, and close reporting together. Those are very different scopes.

What you are paying for

You're paying for four outcomes:

- Consistency: Reconciliations happen on schedule, not when someone finds time.

- Investigation: Exceptions get resolved instead of rolling forward forever.

- Documentation: Review support, audit trail, and workpapers exist when needed.

- Decision-grade reporting: The close produces numbers leadership can use.

A cheaper provider that only checks the box on bank recs often becomes expensive later when revenue, liabilities, or processor balances are wrong.

What good outcomes actually look like

For a SaaS company, the visible change is usually this: billing data, collections, deferred revenue, and recognized revenue stop fighting each other. Finance can explain what was billed, what was collected, and what was earned without relying on spreadsheet patches.

For an agency, the payoff is cleaner client profitability. You stop guessing whether a “profitable” client covers all associated labor, software, contractor spend, and pass-through costs. Reconciled expense and revenue mapping makes account-level reporting credible.

For an e-commerce brand, the shift is operational clarity. Processor fees, refunds, reserves, inventory-related adjustments, and payout timing stop muddying the picture. You can finally evaluate product and channel performance without wondering whether the underlying transaction flow is distorted.

That's the outcome to look for. Not prettier books. Better decisions backed by numbers that tie out.

How to Achieve a Five-Day Close

A five-day close doesn't come from pushing your team harder. It comes from removing ambiguity from the workflow.

Start with a blunt self-audit. List every balance sheet account, every payment source, every payroll feed, and every revenue-related system that touches your books. Then mark which ones are reconciled on a defined cadence, who reviews them, and where exceptions live. Most companies find the same problem fast. The close is bottlenecked by a handful of accounts nobody owns.

Next, calculate the operational drag. If your close takes 15 business days and your target is 5, you already know you're giving away 10 decision days every month. Put that gap in front of your leadership team and tie it to delayed pricing decisions, late expense corrections, and weak cash visibility.

Then fix the process in this order:

- Standardize inputs: Reduce manual exports, duplicate entry, and inconsistent mappings.

- Assign ownership and review: Every account needs a preparer, reviewer, due date, and escalation path.

- Shorten the cadence: High-volume accounts need more frequent attention, not more month-end panic.

If you want a detailed framework for the full reporting cycle, review this guide to the financial close process. Reconciliation is the engine inside it.

You don't need more accounting activity. You need tighter financial controls and a close process that produces reliable numbers while they still matter.

If your close is slow, your reconciliations are late, or your numbers keep changing after month-end, talk to Jumpstart Partners. A good strategy call should leave you with a clear view of where your reconciliation workflow is breaking, which accounts need tighter cadence, and what it would take to get to faster, more accurate financial reporting.