Financial Operations

Tax Form 1120: A Founder's Guide to C Corp Taxes

Master IRS Tax Form 1120 with our guide for C Corp founders. Learn to file, handle schedules, avoid penalties, and manage SaaS-specific issues like ASC 606.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readAbout 1.4 million small businesses have to file Form 1120 each year, according to the US Chamber of Commerce summary cited by OnPay. That number reframes the issue. Tax form 1120 isn't some niche filing that only large public companies worry about. It's the annual tax return for a huge share of the C Corps operating in the U.S.

If you run a SaaS company, agency, or professional services firm, your 1120 matters far beyond tax compliance. It becomes part of the paper trail that investors, lenders, and diligence teams use to judge whether your finance function is disciplined or fragile. A messy return usually points to messy books. Clean returns usually come from clean closes, clear reconciliations, and leadership that understands where the numbers come from.

Why Form 1120 Is More Than Just a Tax Form

Form 1120 is the federal income tax return for a domestic C Corporation. You file it to report income, deductions, gains, losses, credits, and your company's tax liability. It applies even when the business is operating at a loss, which is why many early and growth-stage venture-backed companies still have to treat this filing seriously.

Founders underestimate what the return signals

A lot of founders treat tax form 1120 as something to hand off in March and ignore. That approach breaks down when your company is raising capital, taking on debt, or preparing for a quality-of-earnings review.

Your 1120 ties together several things outsiders care about:

-

Revenue quality

If your tax return doesn't reconcile cleanly to your books, investors start asking whether your MRR, ARR, deferred revenue, and margin reporting are reliable. -

Control environment

A clean filing suggests your accounting team closes the books consistently, tracks adjustments, and understands the difference between book and tax treatment. -

Cash planning

Extensions give you more time to file, not more time to pay. If you miss that distinction, you create avoidable penalties and cash stress.

Practical rule: Treat your corporate return like a diligence document. If an investor asked for it tomorrow, it should support your story, not contradict it.

The deadline is simple. The consequences are not.

For calendar-year corporations, Form 1120 is due April 15, and Form 7004 gives you a six-month automatic extension to October 15. But the payment is still due by the original deadline, as noted in this Form 1120 overview.

That distinction matters for growth companies because tax returns often get delayed for understandable reasons. Revenue recognition needs review. State apportionment needs cleanup. Payroll classifications need confirmation. None of that changes the payment deadline.

Here's the founder-level takeaway:

| What founders often assume | What actually matters |

|---|---|

| “We're not profitable, so tax form 1120 isn't urgent.” | C Corps generally still have a filing obligation, even with losses. |

| “An extension solves the deadline problem.” | It solves the filing deadline, not the payment deadline. |

| “This is a CPA task, not an operating issue.” | The return reflects your accounting quality, controls, and readiness for diligence. |

When your books are investor-ready, tax form 1120 becomes easier. When your books are late, inconsistent, or built on spreadsheet patches, the tax return exposes it.

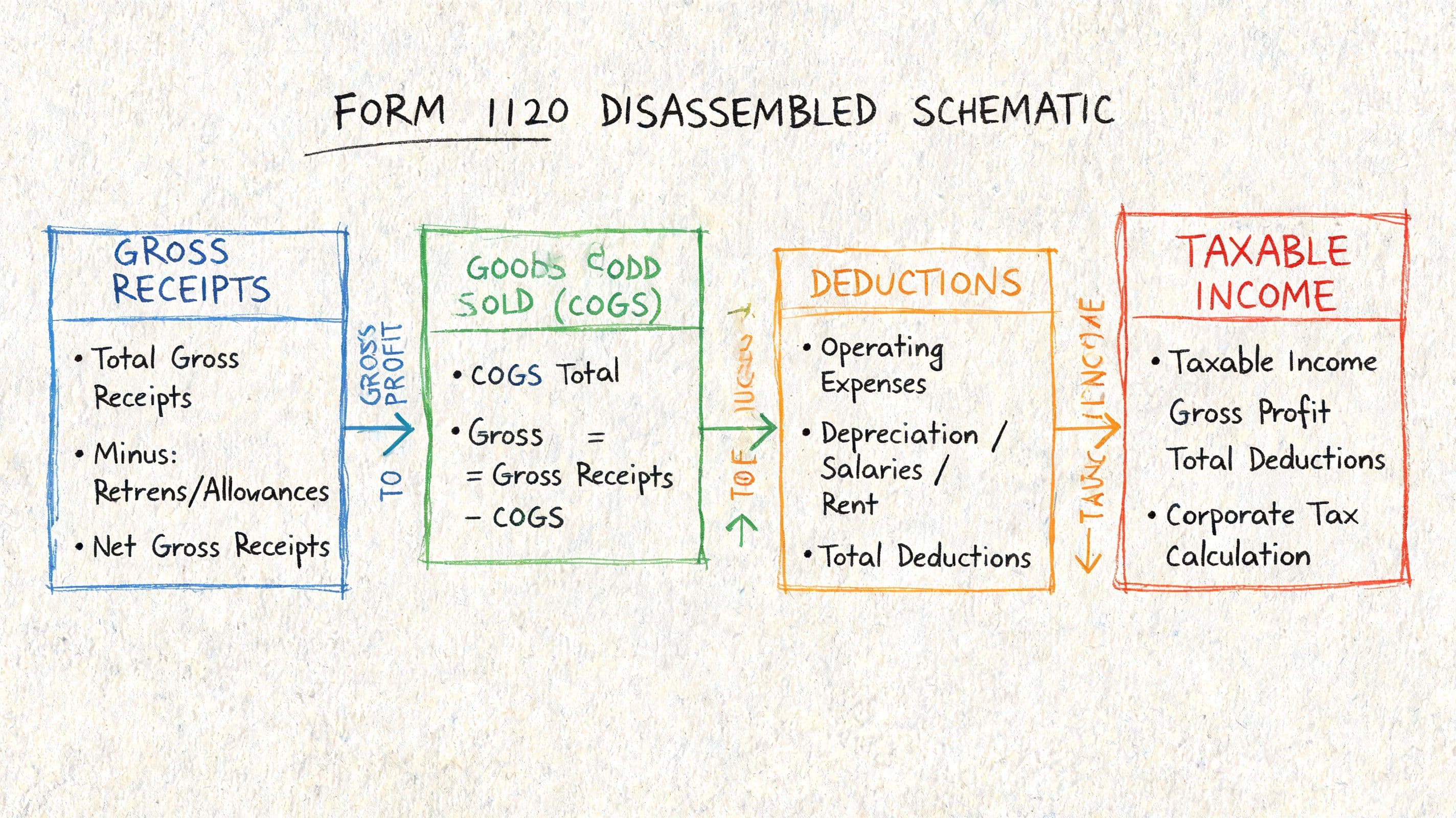

The Anatomy of Your Corporate Tax Return

The basic mechanics of tax form 1120 are straightforward. You start with income, subtract allowable deductions, compute taxable income, and apply the federal corporate tax rate. Since the Tax Cuts and Jobs Act changed the federal corporate rate to a flat 21%, that rate now sits at the center of the return, as explained in this overview of Form 1120 mechanics.

The core math on page 1

At a high level, the form follows this flow:

- Report gross receipts

- Subtract returns, allowances, and COGS if applicable

- Add other income items

- Subtract deductions

- Arrive at taxable income

- Apply the 21% federal corporate rate

For many agencies and professional services firms, the biggest drivers are revenue, payroll, rent, software, contractors, and other operating expenses. For SaaS businesses, you also need to think carefully about how book revenue differs from tax revenue.

A worked example with real numbers

Assume your agency reports:

- Gross receipts: $2,000,000

- Salaries: $1,200,000

- Rent: $150,000

- Marketing: $50,000

To keep the example focused, assume there are no other income items, no COGS, and no additional deductions or credits.

Your taxable income calculation would look like this:

| Item | Amount |

|---|---|

| Gross receipts | $2,000,000 |

| Less salaries | ($1,200,000) |

| Less rent | ($150,000) |

| Less marketing | ($50,000) |

| Taxable income | $600,000 |

Federal income tax at 21%:

- $600,000 × 21% = $126,000

That is the mechanical point many founders miss. Every operating decision that changes deductible expense changes taxable income. If your books are wrong, your tax forecast is wrong. If your tax forecast is wrong, your cash plan is wrong.

A tax forecast built on stale financial statements is worse than no forecast at all. It gives you false confidence.

What works and what doesn't

What works:

- Monthly close discipline so the year-end tax provision isn't assembled from twelve different versions of reality

- Clear account mapping between your general ledger and return categories

- Reviewed financial statements before the return gets drafted, using a process like this guide to prepare financial statements

What doesn't work:

- Booking major year-end adjustments after the return draft is already in progress

- Mixing shareholder, founder, and business expenses in one operating account

- Treating tax prep as the first time anyone reviews the books in detail

The return itself isn't complicated in theory. The hard part is feeding it numbers you can defend.

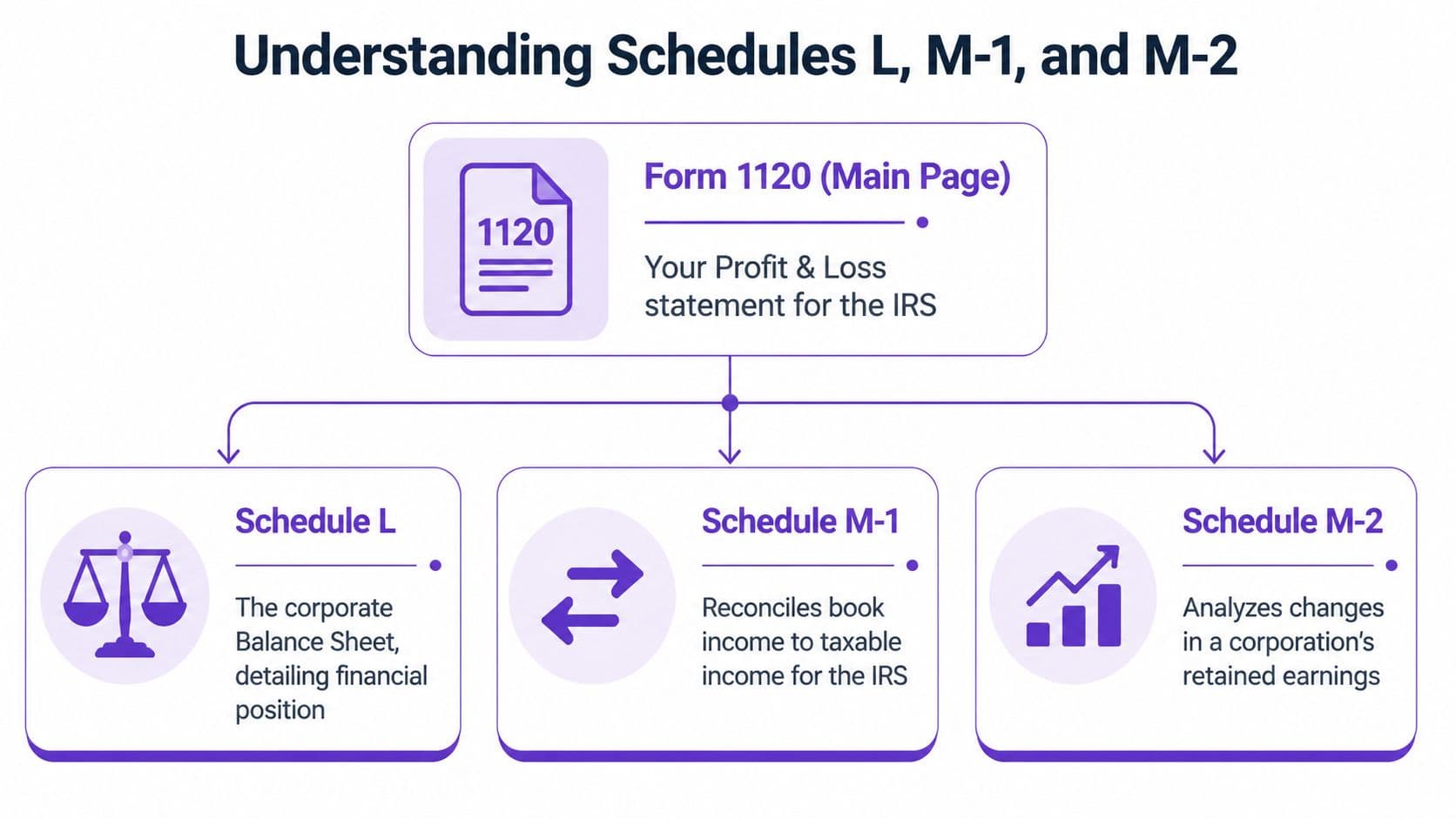

Understanding Schedules L M-1 and M-2

Most founders look at page 1 of Form 1120 and assume that's the whole story. It isn't. For a growth company, Schedule L, Schedule M-1, and Schedule M-2 are where financial discipline becomes visible.

Schedule L shows whether your balance sheet is believable

Schedule L serves as your balance sheet per books. It reports assets, liabilities, and equity at the beginning and end of the year. For SaaS companies, deferred revenue and other balance sheet positions stop being abstract accounting concepts and become tax return line items here.

If your balance sheet in the return doesn't tie to your books, the problem usually isn't tax. The problem is your accounting process. That's one reason finance teams regularly use the balance sheet to assess business financial health before the return ever gets prepared.

A founder should care about Schedule L because it answers practical questions:

- Did cash reconcile?

- Are receivables collectible and correctly stated?

- Is deferred revenue carried properly?

- Does equity reflect what occurred during the year?

Schedule M-1 explains why book income and tax income differ

This is the schedule many smart operators ignore until it causes trouble.

Your books are prepared under your accounting framework and internal policies. Your tax return follows tax law. Those two numbers often differ. Schedule M-1 is the bridge between them.

For SaaS and agency businesses, common causes of book-to-tax differences include:

- Deferred revenue timing

- Meals, penalties, and other partially or non-deductible items

- Depreciation and amortization differences

- Compensation timing or accrual differences

If your M-1 feels improvised, your close process probably is too.

When the M-1 is clean, a reviewer can understand the differences quickly. When it's sloppy, every downstream conversation gets harder.

Schedule M-2 tracks retained earnings movement

Schedule M-2 shows how retained earnings changed over the year. It captures the effect of book income, distributions, and other equity movements. That matters because retained earnings should move in a way that matches the rest of your financial reporting.

If retained earnings on the tax return doesn't make sense, people start checking everything else.

A strong review process should compare the tax schedules back to your books before filing. This is the same discipline used to analyze a balance sheet properly, not just to finish the tax package.

Here's the shortest way to think about the three schedules:

| Schedule | What it tells the IRS | What it tells an investor or lender |

|---|---|---|

| Schedule L | Your year-end financial position | Whether your balance sheet is coherent |

| Schedule M-1 | Why book and tax income differ | Whether your finance team understands its own numbers |

| Schedule M-2 | How retained earnings changed | Whether equity movements are tracked cleanly |

A clean set of schedules doesn't guarantee a great business. But it does show that your finance function is controlled, consistent, and credible.

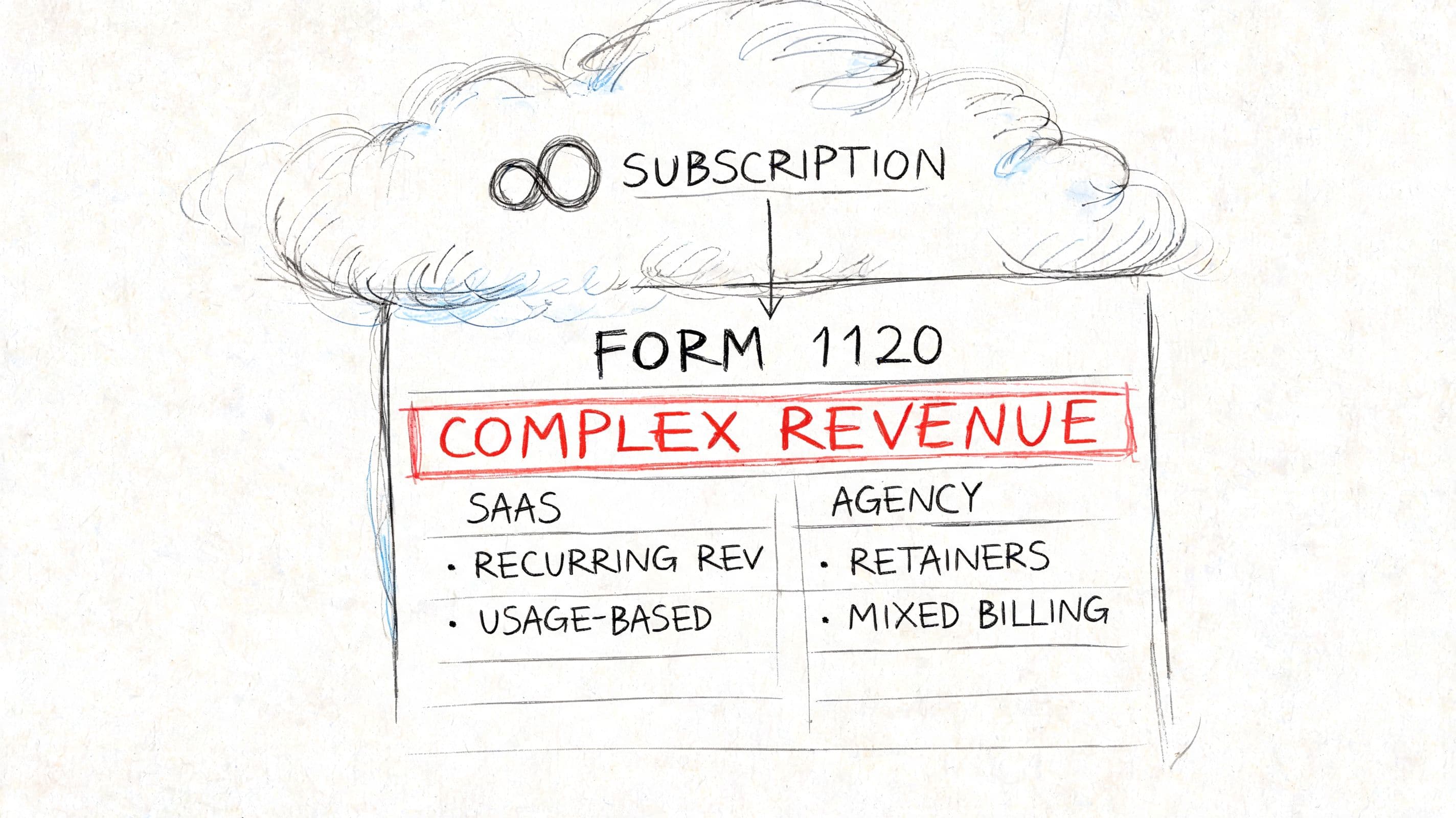

Form 1120 for SaaS and Agency Leaders

Generic guidance on tax form 1120 breaks down fast for SaaS companies and complex service firms. The issue isn't that the form is different. The issue is that your revenue model, contract structure, and accounting treatment create risks that basic small-business tax content never addresses.

According to Kruze Consulting's discussion of Form 1120 for startups, most public resources don't address how SaaS companies should report deferred revenue or handle ASC 606 complexities, and approximately 40% of SaaS companies filing Form 1120 have material misstatements in revenue reporting that require restatement when seeking institutional funding. That's not a tax nuisance. That's a financing problem.

“Founders think of Form 1120 as a compliance task, but investors see it as an x-ray of your financial discipline,” says a Principal at Jumpstart Partners. “For a SaaS company, a sloppy M-1 reconciliation tied to messy ASC 606 rev rec is a major red flag that kills deals. Clean, audit-ready tax filings are table stakes in a competitive funding environment.”

SaaS companies trip on deferred revenue

Under ASC 606, book revenue may not equal billed cash. If you invoice annual contracts upfront, your books may carry a deferred revenue liability for the portion not yet recognized. That creates immediate tax-return implications.

For tax form 1120, the practical pressure points are usually:

- Schedule L classification of deferred revenue and related liabilities

- Schedule M-1 adjustments where book revenue recognition differs from tax treatment

- Contract changes such as renewals, implementation obligations, discounts, or credits that complicate the timing

This is why a SaaS-specific accounting process matters. If your revenue schedules live in Stripe exports, CRM notes, and spreadsheet overrides, your tax return becomes a reconstruction exercise. A stronger approach starts with a system that handles accounting for SaaS correctly throughout the year.

Agencies have a different problem

Agencies and professional services firms usually don't struggle with deferred subscription revenue in the same way. Their risk is often misclassifying labor, project costs, owner compensation, and reimbursements.

That creates distortions in:

- Gross margin reporting

- Officer compensation disclosure

- Taxable income calculation

- State filing positions when teams work across multiple jurisdictions

A clean close for an agency should answer basic questions quickly. Which labor belongs in delivery? Which spend is overhead? Which costs are reimbursable? If you can't answer those before tax prep starts, your return is already on unstable ground.

R&D credits and capitalization need planning

For software companies, R&D tax treatment often creates confusion because leaders hear “credit” and assume every engineering dollar lowers taxes immediately. That isn't how disciplined tax planning works.

The return can involve both:

- R&D credits, which are claimed through the appropriate attachment process

- Capitalization or amortization issues for development-related costs depending on the applicable tax rules and fact pattern

The operational lesson is simple. Don't ask your tax preparer to reverse-engineer product development activity from payroll detail after year-end. Build a chart of accounts and project coding structure that isolates technical labor and related costs during the year.

Here's a practical diagnostic table:

| Issue | What weak teams do | What strong teams do |

|---|---|---|

| Deferred revenue | Rebuild support at year-end | Maintain contract-level schedules monthly |

| ASC 606 adjustments | Book manual entries without documentation | Document policy and retain support for each adjustment |

| R&D activity | Lump engineering into one expense bucket | Track by function and project from the start |

| Agency labor mapping | Mix delivery and admin payroll | Separate direct labor, management, and overhead clearly |

A short walkthrough helps many founders see the issue more clearly:

The hard truth is that a generic tax preparer can file an 1120 for a SaaS company and still leave serious diligence risk behind. Filing isn't the same as filing cleanly.

C Corp vs S Corp The Critical Choice

A lot of founders hear the same advice once revenue grows: “Why not switch to an S Corp and avoid double taxation?” That question is worth taking seriously. It's also where many businesses make the wrong decision by focusing only on tax mechanics and ignoring capital structure.

For high-growth businesses planning to raise outside capital, issue equity broadly, or keep structural flexibility, the entity choice is strategic.

Entity Type Comparison C Corp vs. S Corp vs. Partnership

| Feature | C Corporation (Form 1120) | S Corporation (Form 1120-S) | Partnership (Form 1065) |

|---|---|---|---|

| Federal tax structure | Entity-level corporate tax return | Pass-through return | Pass-through return |

| Core filing form | Form 1120 | Form 1120-S | Form 1065 |

| Investor fit | Usually aligns better with venture-style fundraising | Often more restrictive for institutional investment structures | Often less practical for venture-backed operating companies |

| Ownership flexibility | Generally broader corporate structuring flexibility | More restrictive shareholder rules | Flexible economically, but more complex for many operating companies |

| Treatment of earnings | Corporate earnings taxed at entity level, distributions can create a second tax layer | Income generally flows through to owners | Income generally flows through to partners |

| Operational complexity for founders | Familiar for venture-backed companies | Can simplify some tax outcomes, but adds eligibility constraints | Often requires more owner-level coordination |

The real trade-off

If your goal is maximizing near-term tax efficiency for a closely held business with stable ownership, an S Corp can be attractive. If your goal is institutional fundraising and clean equity administration, the C Corp structure usually holds up better.

That's why the “avoid double taxation” argument is often too narrow. It ignores:

- equity incentives for employees

- preferred stock structures

- outside investor expectations

- future conversion friction

- board and legal simplicity

The best entity choice isn't the one with the lowest abstract tax burden. It's the one that fits how you plan to finance and operate the business.

Common misconceptions founders carry

-

“We can always switch later without friction.”

Structural changes ripple into legal documents, tax filings, ownership records, and investor conversations. -

“S Corp is automatically better if we aren't profitable yet.”

The right answer depends on ownership plans, future financing, and how losses interact with your broader tax situation. -

“Form 1120 means we chose wrong.”

Not if your company is built for scale, outside capital, and a conventional venture-backed path.

For the audience that usually reads this kind of guide, the C Corp often remains the practical answer because financing strategy outruns pure tax optimization. The mistake isn't being a C Corp. The mistake is being a C Corp with weak books and an unmanaged tax process.

Deadlines and Red Flags Common Filing Errors

The fastest way to turn tax form 1120 into an expensive problem is to treat it as an annual paperwork event instead of a year-round finance process.

According to IRS Form 1120 information, 22% of the 2.1 million Form 1120 filers incurred a total of $4.7 billion in penalties. The same source notes that underpayment of estimated taxes is a major cause, with penalties applying if less than 90% of the prior year's tax or 100% of the current year's liability is prepaid quarterly.

The filing calendar founders need to respect

For a calendar-year corporation:

| Requirement | Timing |

|---|---|

| Form 1120 due date | April 15 |

| Extension via Form 7004 | Six months |

| Extended filing deadline | October 15 |

| Tax payment deadline | Original due date, not the extension date |

The operational mistake is obvious. Teams file the extension and relax. Then they discover the payment was still due in April.

Red flags that trigger pain

The biggest filing problems usually start in the books, not in the tax software.

-

Estimated taxes ignored

If you don't monitor profit and tax liability during the year, quarterly payments get missed and penalties start accumulating. -

Book-to-tax reconciliation is weak

When the M-1 is assembled from memory, reviewers can't trace the logic. That slows the filing and raises questions. -

Officer compensation is poorly classified

Founders often run compensation through multiple channels. Payroll, reimbursements, distributions, and personal spending need clear boundaries. -

Personal expenses flow through the business

This is still one of the fastest ways to create adjustment risk and undermine credibility.

Reviewers don't get nervous because one number is large. They get nervous when no one can explain how the number was produced.

A practical pre-filing checklist

Before your return is drafted, confirm these items:

- The general ledger is closed and major reconciliations are complete.

- Revenue support is documented, especially for subscriptions, annual prepaids, and implementation work.

- Payroll and officer compensation reports tie out to the books.

- Balance sheet accounts have support, including loans, accrued expenses, and deferred revenue.

- Estimated payments are summarized so the preparer isn't guessing what has already been remitted.

The businesses that file cleanly don't rely on heroics in March. They build the tax file during the year.

How to Get Your Form 1120 Right Without the Headache

Tax form 1120 gets easier when it becomes the output of a controlled finance system rather than a stand-alone tax project.

That means your process should do a few things consistently:

- close the books on time

- reconcile the balance sheet every month

- maintain revenue support

- separate tax-sensitive accounts clearly

- preserve documentation before your preparer asks for it

What a better workflow looks like

For most growth-stage SaaS and services businesses, the cleanest setup is a coordinated workflow between bookkeeping, controller review, and tax prep. The controller function matters because someone needs to own the bridge between the general ledger and the return.

A few tools can help on the document side. For example, if you need to extract and review data from prior returns, notices, and supporting PDFs, an AI finance tax document analyzer can speed up initial review. It won't replace judgment, but it can reduce time spent hunting through files.

Where founders usually go wrong

The two bad options are common:

- DIY until the filing gets too complex

- hire a generalist who can file the form but doesn't understand your revenue model

A stronger option is specialized controller support that keeps the books tax-ready all year. If you want to understand what that operating model looks like, this overview of outsourced controller services is a useful starting point.

The right goal isn't just filing on time. It's producing a return that ties to your books, supports diligence, and doesn't create avoidable tax leakage or credibility problems.

If your company needs tax form 1120 handled with the same discipline investors expect from your financials, talk to Jumpstart Partners. Their team supports SaaS, agency, and services businesses with investor-ready books, controller oversight, and a cleaner path from month-end close to tax filing.