Financial Operations

A Founder's Guide to the Valuation of Startup Companies

Unlock your startup's true worth. This guide demystifies the valuation of startup companies with actionable methods and benchmarks for SaaS and agency founders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readYour company's valuation isn't just a vanity metric for a press release. It's the foundation of your next fundraise, a critical tool for attracting top talent with equity, and the north star guiding your strategic decisions. Get it wrong, and you face painful dilution, tense investor relationships, and a failed funding round.

This guide skips the abstract theory and dives straight into the actionable methods investors use to put a number on your business. You will get clear, data-backed answers, not vague possibilities.

Why Your Startup Valuation Is Your Most Critical Number

As a founder, CEO, or finance leader, you must be fluent in the language of valuation. It’s a direct reflection of your company's story, metrics, and place in the market. Nailing your valuation isn't about getting the biggest check possible; it's about setting your company up for long-term success, from making competitive equity offers to key hires to successfully navigating future funding rounds.

In a volatile market, the stakes are higher than ever. According to data from Carta, after hitting a fever pitch in Q1 2022 with a median Series A valuation of $60.5 million, early-stage startup valuations plummeted to $38.2 million just a year later in Q1 2023. That’s a staggering 37% drop. This rollercoaster ride proves that investors no longer bet on a good story—they demand rock-solid proof of growth before opening their checkbooks.

Moving From Theory to Action

We wrote this guide to give you the language, benchmarks, and calculations you need to walk into investor meetings with confidence and secure the capital you deserve on favorable terms.

You’ll learn how to:

- Confidently calculate and defend your valuation with real numbers.

- Turn a complex, intimidating process into a strategic advantage.

- Master the key metrics that drive investor decisions.

Ultimately, your goal is to land on a number that's both ambitious and defensible—one grounded in the reality of your business performance. Understanding this process is vital whether you're gearing up for your first major investment or a more advanced round like a guide on what is Series B funding.

The Three Core Valuation Methods Every Founder Must Know

While a hundred different factors can nudge a startup's valuation up or down, nearly every investor conversation comes back to three fundamental methods. As a founder of a business with $500K to $20M in revenue, you absolutely have to know how each one works.

For startups with predictable revenue, one method is king.

Market Approach (SaaS Multiples) for Revenue-Generating Companies

For any SaaS, digital agency, or professional services business with real revenue, the Market Approach is the go-to method. It values your company by comparing it to similar businesses ("comps") that were recently funded or acquired. The most common flavor for SaaS is the ARR Multiple method.

The logic is straightforward. An investor takes your Annual Recurring Revenue (ARR) and multiplies it by a number they've pulled from recent market deals.

"A company being 'hot' with investors at Demo Day is generally a positive signal, but a relatively weak one, especially once you take into account their higher entry valuation... >90% of a company’s success is driven by other factors." — Jared Heyman, Managing Partner at Rebel Fund

This quote gets right to the point. Market hype helps, but investors always fall back on hard metrics to justify a valuation multiple. Your growth rate, gross margin, and net revenue retention (NRR) are what really move that multiple up or down.

A Worked Calculation: Let’s say your SaaS company is doing $3 million in ARR. Looking at the market, you find that similar companies are getting valued at around 8x ARR.

- Valuation = ARR x Multiple

- Valuation = $3,000,000 x 8 = $24,000,000

That $24 million is your starting line for negotiations. Show investors fantastic metrics, and you can argue for a higher number. Weak metrics? They will have all the leverage they need to push for a lower one.

Income Approach (Discounted Cash Flow) for Future Potential

The Income Approach, usually in the form of a Discounted Cash Flow (DCF) analysis, is more common for mature, profitable companies. But don't dismiss it. Smart VCs use a DCF to stress-test your long-term vision and see if your financial model holds water.

A DCF projects your company’s future cash flow for the next 5-10 years and then "discounts" that future money back to what it's worth today. The entire analysis hinges on the assumptions baked into your financial projections. This is where building a credible three-year forecast becomes an essential skill.

Asset-Based Approach for Pre-Revenue Startups

What if you don't have revenue yet? The Market and Income approaches are useless. For pre-revenue or super early-stage companies, investors lean on qualitative frameworks that fall under the Asset-Based Approach.

Methods like the Berkus Method or Scorecard Valuation offer a structured way to put a number on your non-financial assets:

- Strength of the Founding Team: What's their track record? Have they done this before?

- Soundness of the Idea: Is the market huge and growing? Is the problem real?

- Prototype or Technology: How far along is the product? Is there any defensible tech?

- Strategic Relationships: Do you have partnerships that give you an unfair advantage?

This approach is more art than science, but it provides a necessary framework to set a valuation before you have meaningful traction.

A Founder's Comparison of Startup Valuation Methods

So, how do you know which method applies to you? It depends on your stage and business model. Each approach tells a different part of the story, and it's your job to know which story to tell investors.

| Valuation Method | Best For | Key Advantage | Key Disadvantage |

|---|---|---|---|

| Market Approach (Multiples) | SaaS & services with recurring revenue ($500K+ ARR) | Grounded in real-world market data and easy to understand. | Can be misleading if comparable companies are not truly similar. |

| Income Approach (DCF) | Mature, profitable businesses or for stress-testing models. | Focuses on a company's intrinsic ability to generate cash. | Highly sensitive to assumptions about future growth and risk. |

| Asset-Based Approach | Pre-revenue or very early-stage startups. | Provides a structured way to value a company without financial data. | Highly subjective and relies on qualitative judgment. |

Early-stage valuation is a blend. An investor uses the Asset-Based approach for a pre-seed round but will always have an eye on the market multiples you’ll need to hit later. As you grow, the conversation will shift almost entirely to market comps and your core SaaS metrics.

How to Calculate Your SaaS Valuation With a Practical Example

Theory is one thing; running the numbers is where the truth comes out. Let's get practical and walk through exactly how an investor would value a SaaS business like yours. This isn't an academic exercise—it's how you move from knowing concepts to applying them.

Imagine your SaaS company, "DataOrb," just hit a huge milestone: $2 million in Annual Recurring Revenue (ARR). Your metrics are solid:

- ARR Growth Rate: 80% year-over-year

- Gross Margin: 75%

- Net Revenue Retention (NRR): 110%

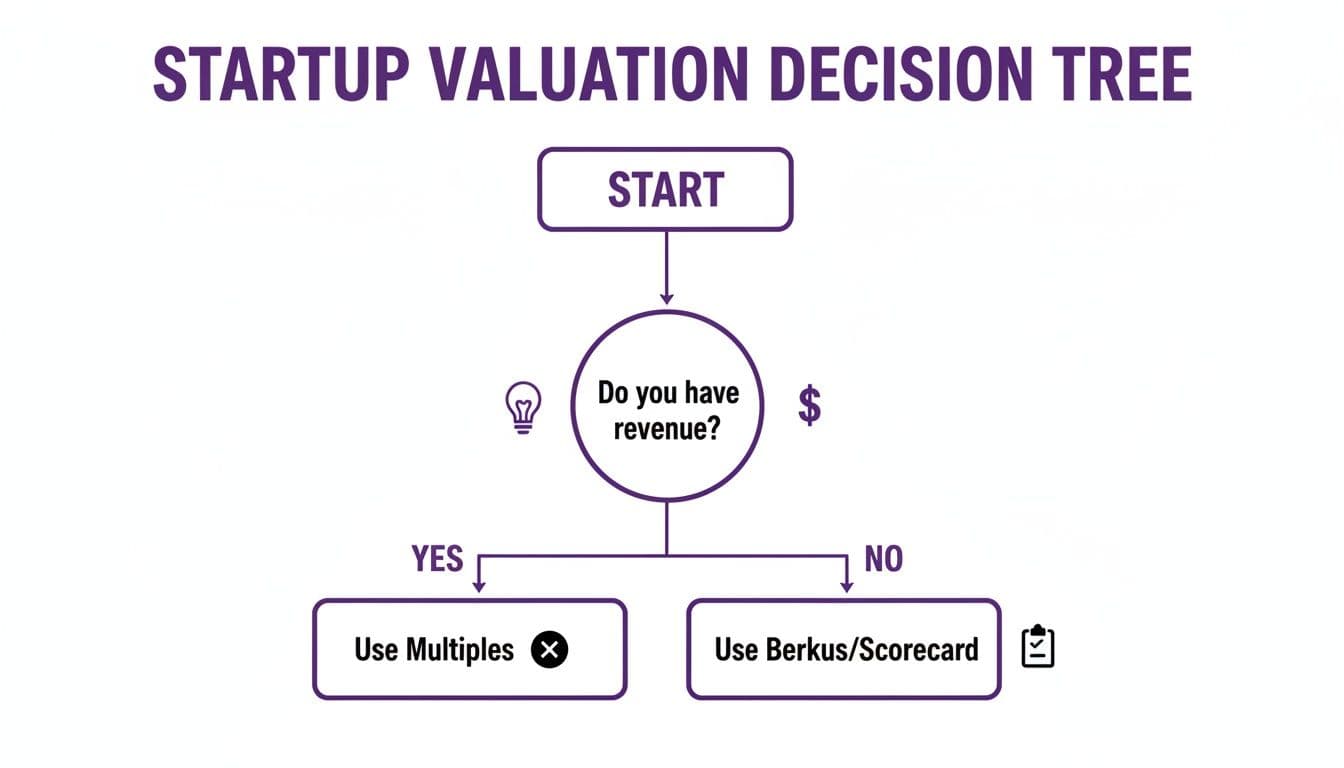

With these numbers in hand, where do you start? The conversation always begins with the ARR multiple.

This decision tree shows the first question any founder or investor will ask. It’s the fork in the road for the valuation of startup companies.

The moment you have real revenue, the entire conversation shifts. You move from telling stories about potential to analyzing hard performance data. This is why multiples become the name of the game.

The Baseline Calculation

First, you need to find a relevant benchmark. You can’t just pull a number out of thin air. According to OpenView's 2024 SaaS Benchmarks, a company with DataOrb’s profile—strong growth and healthy margins—is trading in the 8x to 12x ARR multiple range.

Let's pick a conservative starting point and use a 10x multiple.

- Baseline Valuation = ARR x Multiple

- $2,000,000 (ARR) x 10 = $20,000,000 (Pre-Money Valuation)

This $20 million figure is your anchor. It’s a solid starting point, but the negotiation is just beginning. This is where your other metrics come into play, either justifying a higher multiple or giving investors ammunition to argue for a lower one.

Adjusting the Multiple With Your Metrics

No serious investor will just accept a baseline multiple and write a check. They are going to dig into your operational metrics to build a case for their offer. You have to be ready to defend your numbers.

Let’s put DataOrb’s metrics under the microscope and see how they influence the valuation.

The Good: Metrics That Drive Value Up Your 80% YoY growth rate is fantastic for a $2M ARR company. It screams that you have excellent product-market fit. Even better, your 110% NRR proves you can grow without signing a single new customer. Your existing customers love you so much they're spending more over time.

These two metrics are your power-hitters. They give you the leverage to argue for a higher multiple, pushing you toward the top of that 8x-12x range—to 11x or 12x.

The Bad: Metrics That Drag Value Down Now for a dose of reality. Your Customer Acquisition Cost (CAC) Payback Period is 24 months. That’s a major red flag. It means it takes two full years of gross profit to earn back the money you spent to acquire a customer. This is a common misconception—many founders focus on growth at all costs, but investors care deeply about efficient growth.

An investor will seize on this. They’ll argue it points to an inefficient go-to-market engine, putting downward pressure on your multiple and pulling it back toward the 8x end of the range.

Putting It All Together: A Final Number

This push-and-pull is the heart of any valuation negotiation. The investor opens their argument at an 8x multiple, pointing to the long CAC payback. You fire back by highlighting your elite growth and NRR, making a case for 12x. More often than not, you will meet somewhere in the middle.

| Metric | DataOrb's Performance | Impact on Multiple | Adjusted Multiple |

|---|---|---|---|

| ARR | $2,000,000 | (Baseline) | 10x |

| Growth Rate | 80% (Strong) | Positive | Moves toward 12x |

| NRR | 110% (Excellent) | Positive | Moves toward 12x |

| CAC Payback | 24 Months (Weak) | Negative | Moves toward 8x |

| Final Agreed | (Negotiated Outcome) | Compromise | 9.5x |

After some back-and-forth, you land on an agreed-upon multiple of 9.5x. This would put your final pre-money valuation at $19 million ($2M ARR x 9.5). Knowing exactly how each of these metrics moves the needle is your most powerful tool in the negotiation.

When you're finding comparable companies, getting specific to your niche is crucial. Looking up lists of Fintech SaaS companies, for example, will give you far more relevant benchmarks. And if you need to brush up on the most important metric of all, check out our complete guide to Annual Recurring Revenue.

The SaaS Metrics That Drive Valuations Higher

Investors don’t fund ideas; they underwrite traction proven by numbers. The valuation of a startup, especially in SaaS and professional services, isn't a mystical art—it's a direct function of your key performance indicators (KPIs). Your metrics tell the real story about your company's health and potential to scale.

Understanding these metrics is non-negotiable. It's the language investors speak. Knowing your numbers cold is the only way you can confidently defend your valuation and command a premium.

The bar is higher now. According to Carta's State of Private Markets report, the median time between funding rounds has stretched from 451 days back in 2021 to a staggering 744 days by late 2024—a 65% increase. This shift sends a clear signal: investors are demanding more proof of a scalable, efficient business model before writing the next check. You are expected to show strong, consistent metrics for 18-24 months between raises.

The Metrics That Matter Most

While you track dozens of KPIs, a handful carry the most weight in any valuation discussion. These are the numbers that directly influence the multiple an investor is willing to apply to your business.

-

Annual Recurring Revenue (ARR) & Growth Rate: This is the headline act. ARR provides the baseline value, but your growth rate is what creates excitement and drives a high multiple. Elite growth, often 2-3x year-over-year at the early stages, is a powerful signal of strong product-market fit.

-

Gross Margin: This number reveals the fundamental profitability of your product or service. For a software company, a gross margin below 70% will raise immediate questions about your cost structure or pricing. Elite SaaS companies consistently operate with gross margins of 80% or higher.

-

Net Revenue Retention (NRR): This is a critical indicator of customer health and how "sticky" your product is. NRR measures your ability to grow revenue from existing customers through upsells and expansion, even after accounting for churn and downgrades. A world-class NRR is over 120%.

-

LTV:CAC Ratio: This measures the return on investment of your sales and marketing machine. A healthy LTV:CAC ratio is 3:1 or better. Put simply, for every dollar you spend to acquire a customer, you should be generating at least three dollars in lifetime value from them.

-

CAC Payback Period: This metric shows how quickly you recoup the cost of acquiring a new customer. A shorter payback period signals a more efficient and cash-generative growth engine. The goal for most venture-backed SaaS businesses is a CAC payback period of under 12 months.

"The single biggest mistake founders make in fundraising is treating financial diligence as an afterthought. Investors aren't just buying your story; they are underwriting your metrics. If your numbers are messy, they assume your business is too." — Finance Partner, Leading VC Firm

How You Stack Up: SaaS Valuation Benchmarks

Knowing your own numbers is only half the battle. You also need to know how they compare to the rest of the market. Investors will judge your performance relative to other companies at a similar stage and size.

| Metric | Good Performance | Elite Performance | Why It Matters |

|---|---|---|---|

| Growth Rate (YoY) | 60-80% | 100%+ | The primary driver of high valuation multiples. |

| Gross Margin | 70-80% | 80%+ | Shows the inherent profitability of your business model. |

| Net Revenue Retention | 100-110% | 120%+ | Proves your product is essential and has expansion potential. |

| LTV:CAC Ratio | 3:1 | 5:1+ | Validates the efficiency of your sales & marketing spend. |

| CAC Payback Period | < 18 Months | < 12 Months | Demonstrates how quickly your growth engine can scale. |

Benchmark data is aggregated from sources including OpenView's 2024 SaaS Benchmarks and Bessemer Venture Partners.

These aren't vanity metrics; they are the core components of a defensible valuation. For a deeper dive, explore our guide to the essential SaaS financial metrics that matter.

Valuation Red Flags That Kill Investor Deals

A strong valuation on paper can fall apart in a hurry when an investor starts poking around. During due diligence, they are actively looking for operational sloppiness—for reasons to lower their offer or walk away completely.

Think of this as your pre-mortem analysis. We’re highlighting the most common deal-killing red flags we see every day with businesses in the $500K to $20M revenue range.

Don’t assume a hot market will save you from scrutiny. While competition for deals can inflate valuations, it's operational readiness that gets them closed. You can read more about these private market funding dynamics on Carta.

Messy and Unreliable Financials

This is, without a doubt, the number one deal killer. If you can’t produce clean, accurate, investor-ready financials with a swift month-end close, investors will assume your entire business is just as disorganized.

Nothing destroys credibility faster than numbers that don't tie out or financials that take weeks to prepare. An investor will ask for your P&L, balance sheet, and cash flow statement. If those documents are riddled with errors or based on sloppy bookkeeping, they won't trust any of your other metrics—not your ARR, not your growth rate, not a single thing. It screams that you lack the basic financial controls needed to manage their investment.

Inaccurate Revenue Recognition

For SaaS and subscription companies, this is a particularly bright red flag. Failing to comply with ASC 606, the accounting standard for revenue recognition, signals amateurism and creates a huge, expensive cleanup project. You cannot recognize cash as revenue the moment it hits your bank account.

Here’s a classic example of this common misconception:

- The Mistake: You sign a new customer on a $120,000 annual contract and they pay you upfront in January. You book all $120,000 as revenue in that first month.

- The Reality (ASC 606): You must recognize that revenue over the life of the contract. This means you should only recognize $10,000 per month ($120,000 / 12 months) as you deliver the service.

An experienced investor will spot this discrepancy from a mile away. It completely distorts your monthly growth and profitability, making your entire financial story unreliable.

A Complicated or Undocumented Cap Table

Your capitalization table—the ledger of who owns what in your company—must be pristine. A messy cap table full of verbal equity promises, unsigned stock option agreements, or unresolved founder disputes can stop a deal in its tracks.

Investors need to know exactly what they are buying into. These kinds of issues create legal and financial landmines that no investor wants to inherit. Before you even think about fundraising, get your cap table cleaned up, fully documented, and managed on a professional platform. A clean cap table is a non-negotiable part of passing any financial due diligence checklist.

Unrealistic "Hockey Stick" Projections

Every founder is optimistic—that’s a given. But your financial projections must be rooted in reality. A "hockey stick" growth model that shows exponential growth without a clear, bottom-up plan to get there will shatter your credibility. Investors have seen thousands of these, and they are immediately skeptical.

Your financial model is a story about how your business works. If you forecast doubling your revenue, you must also show the corresponding increase in marketing spend, sales headcount, and customer support costs required to achieve it.

A credible forecast is built on clear, metric-based assumptions. For instance, if you plan to add $1M in new ARR next year, you need to show the math: how many leads you need, your conversion rates, your sales cycle length, and the required sales team to hit that number. Without that underlying logic, your projections are just a fantasy.

Your Action Plan for a Successful Valuation Discussion

Knowing how valuation works is one thing. Actually getting a great valuation is another. The real work starts long before your first investor meeting. You must get your house in order. This isn't about window dressing; it's about building a bulletproof, data-backed narrative that puts you in a position of strength.

| Action Item | What To Do | Why It Matters |

|---|---|---|

| 1. Assemble Data Room | Create a secure folder with GAAP financials (24 months), KPI dashboard, revenue data, and your financial model. | A clean data room signals operational excellence and makes due diligence smooth, building immediate investor trust. |

| 2. Clean Up Cap Table | Digitize your cap table on a platform like Carta. Ensure all equity grants are documented, approved, and signed. | Removes legal ambiguity and proves you have a clean ownership structure, which is non-negotiable for investors. |

| 3. Build Defensible Model | Create a bottoms-up financial forecast linking growth to specific investments in sales, marketing, and headcount. | Demonstrates you understand the operational levers of your business, turning your "hockey stick" from a guess into a plan. |

| 4. Know Your Comps | Research recent funding rounds and M&A deals for companies similar to yours in size, industry, and growth profile. | Provides the market context to justify your target multiple and anchors your negotiation in reality, not hope. |

| 5. Prepare Your Narrative | Craft a clear story that connects your metrics to your market opportunity and long-term vision. | Your numbers tell what is happening; your narrative explains why it's happening and where you're going next. |

"The single biggest mistake founders make in fundraising is treating financial diligence as an afterthought. Investors aren't just buying your story; they are underwriting your metrics. If your numbers are messy, they assume your business is too. A clean, fast, and accurate financial house isn't a 'nice-to-have'; it's the price of admission to a serious valuation discussion." — Finance Partner, Leading VC Firm

Use a platform like Carta to get your cap table digitized and managed properly. Make sure every single stock grant is documented, approved by the board, and signed.

To land the funding you need, you have to master both your valuation math and the art of the pitch itself. You can learn more about how to pitch to investors to make sure your story hits home.

Startup Valuation FAQs

When it's time to raise capital, a handful of questions pop up in nearly every conversation. As a founder, you need direct, clear answers to navigate these discussions with confidence. Let's break down the most common ones we hear.

What Is the Difference Between Pre-Money and Post-Money Valuation?

These two terms are the bedrock of any fundraising negotiation, and getting them straight is critical for understanding dilution.

Pre-money valuation is what you and your investor agree your company is worth before their money hits your bank account. Post-money valuation is simply the pre-money value plus the new investment. This final number is what determines ownership stakes.

Worked Calculation: Imagine your company has a $10 million pre-money valuation and you take a $2 million investment.

- Post-Money Valuation: $10,000,000 (Pre-Money) + $2,000,000 (Investment) = $12,000,000 (Post-Money)

- Investor's Stake: $2,000,000 (Investment) / $12,000,000 (Post-Money) = 16.67%

Internalizing this math is the first step to mastering how a fundraise will actually impact your cap table.

How Much Dilution Is Normal for an Early-Stage Round?

Giving up equity is part of the game, but how much is too much? In the current market, it's standard for founders to sell between 15% and 25% of their company in a Seed or Series A round. This is the market-accepted sweet spot.

Veering outside this range sends up red flags.

- Diluting less than 15% signals to investors that your valuation is "off-market" or too aggressive, potentially scaring away good partners.

- Giving up more than 25% creates a major headache for you later. It causes significant founder dilution, making it tough to maintain meaningful ownership and control in future rounds.

How Do You Value a Company with Both SaaS and Services Revenue?

This is a classic problem for any business with a mixed revenue model—think agencies adding a product or consultancies building a SaaS tool. Investors will not value all your revenue the same way. They will "unbundle" your income streams and value them separately.

High-margin, recurring SaaS revenue is the star of the show. It’s predictable and scalable, so it commands a premium multiple. On the other hand, lower-margin, non-recurring services revenue is seen as less valuable and gets a much lower multiple.

| Revenue Type | Typical Gross Margin | Typical Valuation Multiple |

|---|---|---|

| SaaS Revenue | 75%+ | 8x - 12x ARR |

| Services Revenue | 30% - 50% | 1x - 2x Revenue |

It is absolutely critical that your financials cleanly separate the revenue, cost of goods sold (COGS), and gross margins for each stream. If you don't, investors will default to a lower, blended multiple, which punishes your high-quality SaaS revenue and tanks your overall startup valuation.

Getting your financials right isn't just for valuation—it's about running a better business. The team at Jumpstart Partners delivers investor-ready financials with a guaranteed 5-day close, so you can walk into any negotiation with confidence. Schedule a consultation to see how we can give you a clear view of your numbers.