Financial Operations

What Does Cooking the Books Mean: Spotting Fraud in 2026

Discover what does cooking the books mean. Learn to spot fraud with real examples and protect your business from its consequences in 2026.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··14 min readCooking the books means intentionally altering official accounting records to deceive or mislead. That conduct has destroyed companies at massive scale, including Enron, which filed for bankruptcy in 2001 after revealing around $30 billion in debt and losses tied to fraudulent accounting practices.

If you run a business in the $500K to $20M range, the phrase can sound like something that happens in public companies with giant legal teams and Wall Street analysts. That's the wrong takeaway. In smaller companies, book-cooking often starts with a founder trying to make a lender comfortable, a sales leader pushing finance to recognize revenue early, or a bookkeeper burying expenses to hit a target.

Fraud rarely arrives dressed like fraud. It often shows up as “just this month,” “we'll true it up next quarter,” or “the bank only needs the numbers to look clean for underwriting.” That mindset is how a reporting problem turns into a legal problem.

Table of Contents

- Why Cooking the Books Is a Risk You Cannot Ignore

- The Anatomy of Financial Deception

- Four Common Recipes for Cooking the Books

- The True Cost of Financial Misconduct

- Red Flags How to Spot Trouble In Your Own Company

- How to Build a Fraud-Resistant Finance Function

Why Cooking the Books Is a Risk You Cannot Ignore

The plain-English answer to what does cooking the books mean is simple. It means changing the numbers so outsiders believe something false about the business. Merriam-Webster's definition of cook the books ties that phrase directly to deceptive accounting, and it points to Enron's collapse and the governance reforms that followed, including the Sarbanes-Oxley Act of 2002.

That matters even if you're private, founder-led, and nowhere near a public filing. Banks, investors, buyers, and board members still rely on your financial statements to decide whether to trust you with capital, credit, and strategic options.

Small-company fraud is usually disguised as urgency

At your size, nobody says, “Let's commit accounting fraud.” They say:

- Pull revenue forward: “Book the annual deal now. We already have the signed agreement.”

- Push costs out: “Leave that vendor bill in next month. Cash hasn't left the bank yet.”

- Clean up later: “We'll fix the balance sheet after fundraising.”

- Help the deal close: “The lender just wants a cleaner EBITDA view.”

Each of those moves changes the story your numbers tell. If the story is knowingly false, you're not managing optics. You're manufacturing evidence.

Practical rule: If a reporting choice exists mainly to change how a lender, buyer, investor, or tax authority sees the company, treat it as a fraud risk immediately.

This is why CEOs need more than bookkeeping. You need a system that proves the numbers are real. A disciplined quality of earnings review does exactly that by forcing revenue, expenses, liabilities, and adjustments to stand up to scrutiny before a banker or acquirer does it for you.

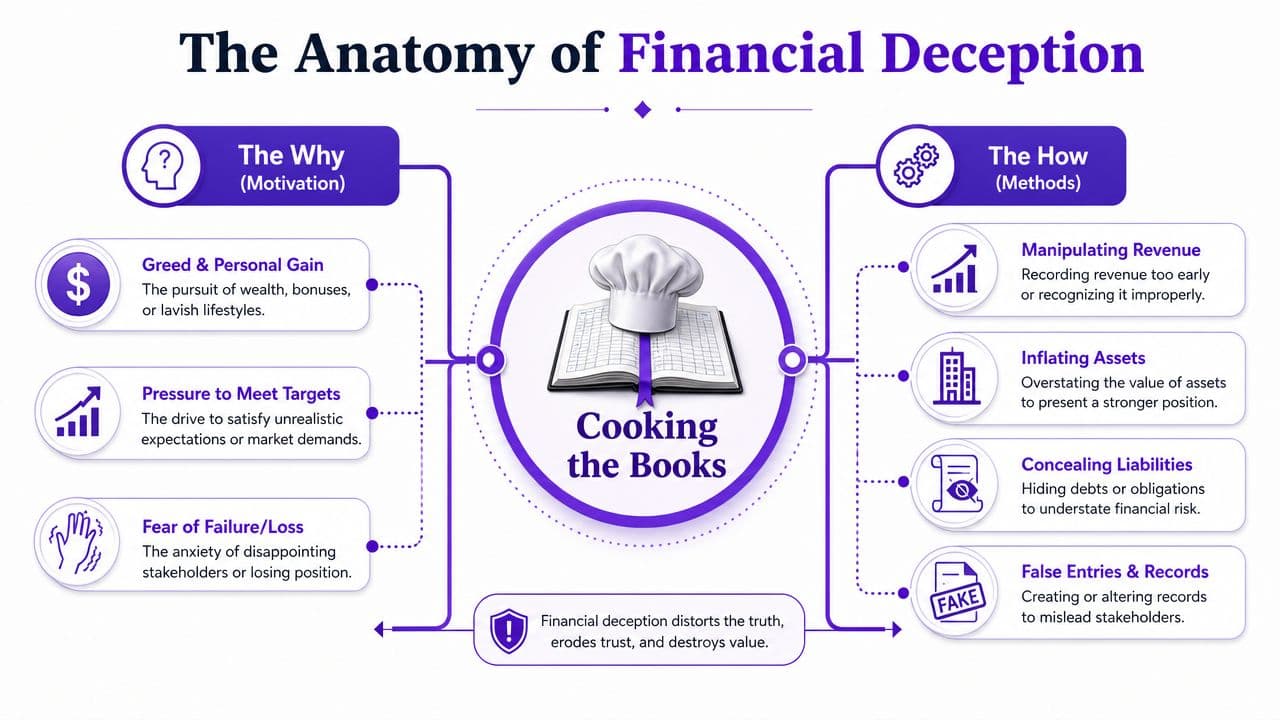

The Anatomy of Financial Deception

Most founders assume cooking the books means stealing cash. That's too narrow. Cambridge's explanation of cook the books makes the broader point: it includes intentionally changing accounting numbers, such as inflating revenue, delaying expenses, and otherwise misleading lenders, investors, or tax authorities.

The line is intent, not aggressiveness

Some accounting decisions involve judgment. Fraud starts when judgment becomes a tool for deception.

A legitimate judgment call asks, “What treatment best reflects economic reality?” A fraudulent one asks, “What number do we need other people to believe?” That difference is everything.

Here's where CEOs get into trouble. You hear a finance employee say revenue was booked “a little aggressively,” or that expenses were “timed for presentation.” If the purpose was to make results look stronger than they really were, stop treating it as style. Treat it as falsification.

Why people do it

The motivations are boring and predictable:

- Debt pressure: You need covenant compliance or a cleaner borrowing profile.

- Fundraising pressure: You want stronger margins, growth, or deferred revenue optics.

- Comp pressure: Bonuses or commissions depend on reported results.

- Fear: The team knows missing plan will trigger layoffs, investor conflict, or founder embarrassment.

None of these motivations makes the act understandable in a legal sense. They only explain why smart people rationalize bad decisions.

A company doesn't drift into clean reporting. Someone chooses discipline every month.

That's why I push founders to understand the transaction flow, not just the headline P&L. If you don't know how invoices, cash receipts, payroll entries, accruals, and reconciliations hit the books, you've handed too much authority to whoever controls your ledger. A strong grasp of double-entry bookkeeping in accounting gives you a practical way to pressure-test whether reported results map to real business activity.

Four Common Recipes for Cooking the Books

Fraud has patterns. In smaller businesses, the same few schemes show up again and again. US Legal Forms' overview of cooking the books lists common schemes including inflating revenue, hiding expenses, misrepresenting debts, and creating false payroll or bank records. It also states clearly that these acts are treated as fraud and can trigger civil claims, fines, and imprisonment, especially when executives approve them.

1. Aggressive revenue recognition

This is the most common problem I see in SaaS and service businesses. A team closes a multi-period contract and books too much of it immediately because the company wants better growth, better margins, or a stronger fundraising deck.

Here's a simple example. A SaaS company signs a 3-year, $36,000 contract. The service is delivered evenly over the term, so the correct Year 1 revenue is $12,000. If someone books the full $36,000 in Year 1, they've inflated revenue by $24,000.

SaaS revenue recognition example clean vs cooked books

| Metric | Clean Books (Correct) | Cooked Books (Fraudulent) |

|---|---|---|

| Contract Value | $36,000 | $36,000 |

| Contract Term | 3 years | 3 years |

| Year 1 Revenue Recognized | $12,000 | $36,000 |

| Year 1 Unearned Revenue Remaining | $24,000 | $0 |

| Year 1 Expenses | $8,000 | $8,000 |

| Year 1 Reported Profit | $4,000 | $28,000 |

That's not a rounding issue. That's a fake earnings story. The business appears far more profitable than it is, even though cash and economics haven't changed.

If you sell retainers, subscriptions, implementation packages, or prepaid service blocks, get serious about ASC 606 revenue recognition. Most “mistakes” in this area are easy to rationalize and expensive to unwind.

2. Hiding expenses

This one is brutally simple. You delay recording bills, capitalize costs that should be expensed, or leave accrued liabilities off the books until after month-end reporting goes out.

A digital agency can do this by leaving contractor invoices in email instead of entering them into QuickBooks or Xero before close. A services firm can do it by holding payroll-related accruals until the next month. A founder can do it by calling ordinary operating costs “owner advances” or “prepaids” with no support.

The effect is immediate. Profit looks higher. Cash flow appears healthier. Your board deck gets easier to present. None of that changes reality.

If expenses belong to the month, book them in the month. “We'll catch it next close” is how manipulation becomes habit.

3. Misrepresenting debt and obligations

This is common when a company is trying to look financeable. Management leaves liabilities out of the balance sheet, understates what's owed to vendors, or fails to reflect repayment obligations tied to loans, cards, or owner financing.

For example, if your company owes implementation refunds, sales tax, unpaid commissions, or customer credits, those items don't disappear because they're inconvenient. They are obligations. If your financials ignore them, your financial strength, working capital, and runway all look better than they really are.

Lender relationships break quickly. Banks care significantly about whether your liabilities are complete. Once they doubt that, they start doubting everything.

4. False payroll or bank records

This is the most blatant version. Fake employees, manipulated payroll entries, unsupported transfers, altered reconciliations, or bank balances that don't tie out.

In a growing company without segregation of duties, the same person can run payroll in Gusto, record entries in QuickBooks, and complete the bank rec. That setup is convenient. It's also dangerous. If one person controls the transaction, the ledger, and the reconciliation, they can hide a lot.

Use simple controls:

- Separate duties: Billing, cash application, and reconciliation should not sit with one person.

- Review bank recs: The CEO or owner should review completed reconciliations, not just the income statement.

- Tie payroll to headcount: Match payroll reports to actual employees and approved compensation.

- Question manual entries: Especially anything posted late, rounded, or lacking backup.

The True Cost of Financial Misconduct

The consequences aren't abstract. Planergy's explanation of cooking the books states that accounting fraud can lead to criminal charges, financial penalties, and prison time. For a CEO, that means this issue sits far beyond accounting hygiene. It's personal liability.

What a fraud event actually costs you

First, you lose trust with the people who matter most to survival:

| Stakeholder | What they see | What usually happens next |

|---|---|---|

| Bank | Unreliable statements | Tighter scrutiny, delayed approvals, damaged credit relationship |

| Investor | Manipulated performance | Pulled term sheet, repricing, or legal claims |

| Buyer | Weak controls and suspect earnings | Lower valuation, expanded diligence, or dead deal |

| Team | Leadership credibility gap | Turnover in finance, ops, and leadership ranks |

Then the internal damage starts. You restate prior periods. You pay lawyers and outside accountants. You spend management time reconstructing records instead of running the company. Your recruiting gets harder because strong finance hires avoid messy books.

Reputation is usually the longest-lasting loss

Founders often focus on whether they can “fix the numbers.” That's the wrong frame. You can restate a report. You can't easily rebuild a reputation for honesty once lenders, investors, and employees think you manipulated the books.

This short explainer is worth watching because it reinforces how fast financial statement deception turns from internal shortcut to external crisis.

Bottom line: Fraud is a company-ending event for some businesses and a career-ending event for the executives who signed off on it.

Red Flags How to Spot Trouble In Your Own Company

You don't need to be a forensic accountant to spot warning signs. You need discipline, skepticism, and a habit of comparing what the numbers say against what the business is doing.

Operational signs that deserve immediate attention

“Trust, but verify” is not enough in finance. Verify first.

- Cash is weak while profit looks strong: If net income keeps improving but cash stays tight, ask why. In service and SaaS businesses, this often points to premature revenue, unpaid receivables, or liabilities being ignored.

- Results look unnaturally smooth: Real businesses are lumpy. If your margins or month-end numbers always land exactly where the plan needed them, inspect manual journal entries and cut-off decisions.

- Finance staff turns over too fast: Repeated changes in controllers, accountants, or outsourced firms often signal unresolved control issues or pressure from leadership to “make the numbers work.”

- Reports arrive late and with changing explanations: Delayed closes, revised statements, and shifting narratives are not admin problems. They usually mean the underlying records are weak or someone is trying to buy time.

Control failures that create room for fraud

A lot of fraud isn't clever. It survives because nobody checks basic workflows.

Look for these issues:

- One person controls too much: If the same employee can invoice, receive cash, post entries, and reconcile accounts, you have a design problem.

- Manual journal entries lack support: Every non-routine entry should have backup. If it doesn't, assume it needs review.

- Bank reconciliations lag: If you're not reconciling every operating account consistently, your financial statements are built on sand.

- Budget variances are hand-waved away: A proper budget vs actual review forces management to explain deviations with evidence instead of storytelling.

For companies that want a sense of how detection is evolving in financial services, this overview of AI for banking fraud detection is useful. The tools are getting better, but the principle is old-fashioned. Fraud survives where oversight is weak.

Common CEO misconceptions

Founders say the same things when a control issue surfaces:

- “It's just timing.” Sometimes it is. Prove it with documentation.

- “We trust our team.” Trust is not a control.

- “We're too small for real fraud.” Smaller companies are often easier to manipulate because duties are concentrated.

- “Our accountant would tell us.” Only if your process gives them clean data and enough authority to challenge you.

If two or three of these red flags show up together, stop normal operations long enough to investigate. That is not overreacting. That is basic leadership.

How to Build a Fraud-Resistant Finance Function

Fraud prevention is not about paranoia. It's about design. If your system relies on good intentions alone, you don't have a finance function. You have hope.

Build controls that make manipulation difficult

Start with the basics and enforce them every month:

- Separate key duties. The person who sends invoices should not also apply cash and complete the bank reconciliation.

- Require documented approvals. Expenses, journal entries, payroll changes, and refunds need an approver and support.

- Review the balance sheet, not just the P&L. Fraud often hides in receivables, accrued liabilities, deferred revenue, and suspense accounts.

- Force timely close discipline. Late closes create room for backfilling and unsupported entries.

- Mandate time away. When finance staff never step away from the process, concealed issues stay concealed.

Add independent oversight

You need someone with enough authority and distance to challenge the books. That can be a board member with finance depth, an external CPA, or an outsourced controller. For growing companies, financial controls for growing businesses should be treated as infrastructure, not overhead.

If your business is implementing AI-driven workflows across finance, ops, or reporting, governance matters there too. This guide to implementing governance for AI transformation is useful because the same principle applies. Bad controls plus automation just lets mistakes and manipulation move faster.

One practical option is using an outsourced controller service such as Jumpstart Partners, which provides bookkeeping and controller support for growing companies and can add independent review to month-end close, reconciliations, and reporting workflows when you don't have a full internal finance bench.

What to do this week

If you want a concrete starting point, do these five things now:

- Pull your last three month-end closes and inspect manual journal entries.

- Review every balance sheet account with your controller or accountant.

- Match recognized revenue to signed contracts and delivery periods.

- Confirm all debt, payroll, tax, and vendor obligations are recorded completely.

- Document who can create, approve, post, and reconcile transactions in each system you use, including QuickBooks, Xero, Stripe, Gusto, and your bank portal.

If any of that feels unclear, your control environment is weaker than it should be.

If you want an outside review of your reporting process, internal controls, or month-end close, talk to Jumpstart Partners. A focused consultation can help you identify where your books are vulnerable, clean up weak processes, and put reliable financial reporting in place before a lender, investor, or buyer finds the problem for you.