Financial Operations

What Is Revenue Recognition Principle: A Founder's Guide

Discover what is revenue recognition principle (ASC 606), its 5-step model, key pitfalls, and why it's vital for your business. Essential guide for founders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readIf you're asking what is revenue recognition principle, you're already asking the right question a little later than most founders should.

Revenue recognition isn't bookkeeping trivia. It's the rule that decides whether your financials tell the truth or tell a flattering story that falls apart in diligence. For a SaaS company, agency, or professional services firm between $500K and $20M in revenue, that difference matters every month.

A lot of founders still think, "We got paid, so that's revenue." That's cash thinking. Investors, lenders, auditors, and serious buyers don't use that logic. They want to know when you earned the revenue by delivering the service or transferring control of the product.

That gap gets dangerous fast when you sell annual software contracts, prepaid retainers, implementation projects, support packages, or usage-based plans. You can look profitable on a cash basis while your actual GAAP numbers say something very different.

Practical rule: Cash in the bank is not the same thing as revenue on the income statement.

Why Revenue Recognition Can Make or Break Your Business

More than 40% of public company audits flagged revenue-related issues after ASC 606, and restatements can cost businesses in the $500K to $20M range millions in market capitalization and wreck investor trust, according to NetSuite's revenue recognition overview.

That should get your attention.

Your bank balance can lie to you

Say you collect a full annual software contract in January. Your cash jumps immediately. If you book all of it as January revenue, your P&L looks fantastic for one month and distorted for the next eleven.

That leads to bad decisions:

- You overspend on hiring because the month looked stronger than it really was.

- You overstate growth in board decks and investor updates.

- You miss margin issues because implementation labor and recognized revenue no longer line up.

- You walk into diligence exposed when someone asks for deferred revenue rollforwards and contract support.

This matters most when your contracts aren't simple

Revenue recognition gets messy when you sell more than one thing in a contract. That's normal for growing companies.

A few common examples:

| Business model | What founders often book | What actually needs review |

|---|---|---|

| SaaS | Annual invoice as upfront revenue | Subscription revenue over the term, plus separate treatment for setup or support |

| Agency | Deposit as immediate revenue | Revenue as work is performed |

| Professional services | Signed SOW as revenue certainty | Revenue based on the specific deliverables and timing |

| E-commerce subscription | Customer charge as same-day revenue | Revenue when each promised box or shipment is delivered |

Wrong revenue creates downstream damage

If your recognized revenue is wrong, your KPIs are wrong. MRR, ARR, gross margin, deferred revenue, and runway all get distorted.

Revenue recognition isn't an accounting cleanup issue. It's a management reporting issue, a fundraising issue, and a credibility issue.

Founders usually feel the pain when one of three things happens: fundraising starts, an audit starts, or cash gets tight. By then, fixing the problem is slower, more expensive, and more disruptive than it should've been.

What Is the Revenue Recognition Principle Really

The short answer is simple. The revenue recognition principle says you record revenue when you earn it, not when you get paid.

Under ASC 606, which governs revenue recognition under US GAAP and is converged with IFRS 15, revenue is recognized when control of promised goods or services transfers to the customer, in an amount that reflects the consideration you expect to receive. In plain English, you book revenue when you've delivered what you promised.

Stop thinking like a checkbook

A founder using cash-basis logic sees payment and calls it revenue. Accrual accounting doesn't work that way.

If you need a refresher on the broader accounting framework, this guide on what is accrual accounting is worth reading. Revenue recognition sits inside that discipline.

Here's the practical difference:

| Situation | Cash-basis thinking | Revenue recognition thinking |

|---|---|---|

| Client prepays annual SaaS subscription | "We made the sale today" | "We earn it over the service period" |

| Agency collects a project deposit | "That's this month's revenue" | "It's revenue as work gets completed" |

| Customer prepays for support and setup | "It's one contract, book it all" | "Separate the promises and recognize each when earned" |

What you are really measuring

You're not measuring collections. You're measuring performance.

If your company promises software access for a year, you haven't earned the full contract value on day one. If your agency signs a website build with strategy, design, and launch support, you need to determine whether those pieces are separate promises or one combined obligation.

That's where founders get tripped up. The principle itself is straightforward. The application requires judgment.

Controller's view: Revenue recognition is the discipline that forces your financials to match the actual delivery of value.

A simple analogy

Think about a custom software build.

If a client pays you upfront for discovery, implementation, and twelve months of platform access, you haven't done all that work the day the wire hits your account. Some of that value transfers immediately. Some transfers over time. Some depends on what the contract states and whether those services are distinct.

That's why "what is revenue recognition principle" isn't a textbook question. It's a contract question, an operations question, and a reporting question.

The misconception founders need to drop

The most common mistake is believing revenue recognition is only for big public companies.

It isn't.

If you're running a $500K to $20M business and you use annual prepaids, retainers, project milestones, or bundled contracts, you already need a defensible policy. Waiting until an audit or fundraise is lazy finance. It also gets expensive.

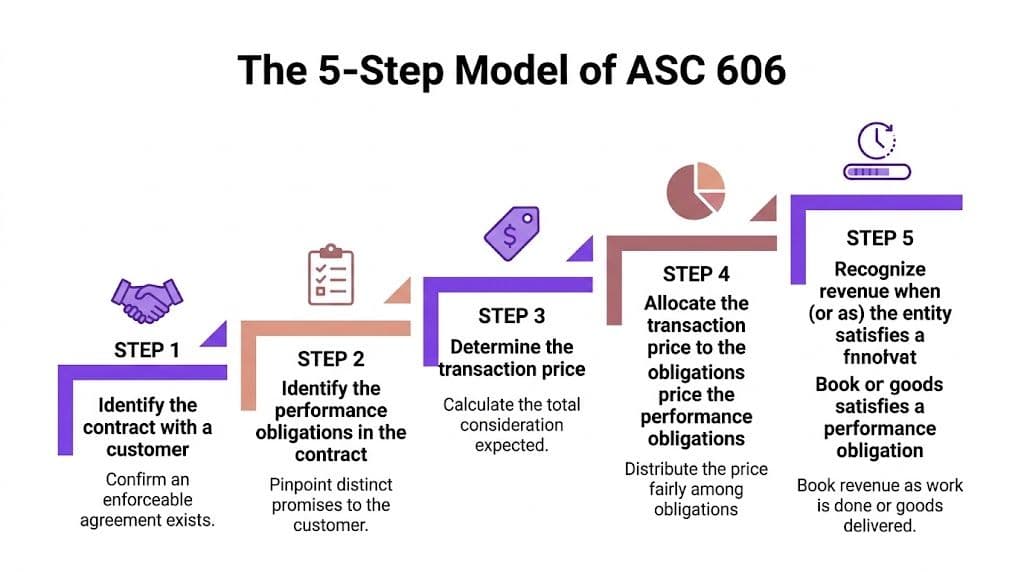

The 5 Step Model of ASC 606 Explained

ASC 606 uses a five-step model. The framework sounds clean on paper. The pain shows up in real contracts.

If you want a deeper technical breakdown alongside this article, read what is ASC 606 revenue recognition.

The ASC 606 Five-Step Revenue Recognition Model

| Step | Key Question | Common Challenge for SaaS/Services |

|---|---|---|

| 1. Identify the contract | Do you have an enforceable agreement with commercial substance and probable collection? | Sales starts service before finance confirms the contract terms |

| 2. Identify performance obligations | What distinct promises did you make? | Bundling setup, subscription, support, and training into one bucket |

| 3. Determine transaction price | What consideration do you expect to receive? | Handling usage fees, credits, discounts, or refunds |

| 4. Allocate transaction price | How much of the price belongs to each obligation? | Missing or weak standalone selling price support |

| 5. Recognize revenue | When is each obligation satisfied? | Booking too much upfront instead of over time |

Step 1 Identify the contract

ASC 606 starts with an enforceable contract. That means the arrangement has commercial substance, each party's rights are identifiable, payment terms are clear, and collection is probable.

This matters more than founders think. A signed proposal in a shared drive isn't enough if the agreement changed in email, the customer hasn't approved the order form, or payment terms are so loose that collectability is questionable.

For a SaaS company, a valid contract is often the order form plus the master service agreement. For an agency, it may be the statement of work and change orders. Finance needs the final version, not a sales summary.

Step 2 Identify performance obligations

At this point, serious judgment starts.

A performance obligation is a distinct promise to transfer a good or service. In SaaS, that often means separating the subscription from non-recurring services if the customer can benefit from each on its own and the promises are separately identifiable.

Example:

- Software access for a year

- One-time implementation

- Premium support

Those may be three separate obligations. They may not be. It depends on the contract and whether the deliverables stand on their own.

If you throw everything into one line called "platform package," you're asking for trouble.

Distinct promises need distinct accounting. If sales bundles them, finance still has to unbundle them.

Step 3 Determine transaction price

The transaction price is the amount you expect to receive. Fixed fees are easy. Variable consideration is where teams make bad calls.

Usage-based billing, rebates, service credits, and overage true-ups all complicate the estimate. ASC 606 allows expected value or most likely amount methods, but the estimate must be constrained so you don't recognize revenue that later reverses.

This is why usage-based SaaS contracts are often harder than fixed annual plans. Revenue isn't just about the rate card. It's about what you can support at close and defend later.

Step 4 Allocate the transaction price

Once you know the total price, you allocate it across the performance obligations based on standalone selling prices, often called SSPs.

If you don't have observable SSPs, you estimate them. The accepted approaches include adjusted market assessment, cost-plus, or in some cases a residual method.

Founders usually underappreciate this step. Discounting a bundle doesn't mean you can assign the whole discount wherever it's convenient. You need a repeatable method.

A weak SSP policy creates two problems:

- Revenue gets misallocated between services and recurring software.

- Gross margin by product line becomes unreliable.

Step 5 Recognize revenue when or as you satisfy the obligation

Now you book the revenue.

Some obligations are satisfied at a point in time. A delivered product is the cleanest example. Others are satisfied over time, such as a hosted SaaS subscription where the customer receives and consumes the benefit throughout the contract term.

For SaaS, monthly ratable recognition of the hosting obligation is standard. For certain services, over-time recognition applies if the customer simultaneously receives the benefit, or if the work has no alternative use and you have a right to payment for performance completed to date.

Where founders get lost

The five steps aren't hard to memorize. They're hard to operationalize.

The failure points are usually operational:

- Sales contracts don't map cleanly to accounting treatment.

- Billing data doesn't match contract language.

- Upgrades, downgrades, and credits aren't tracked centrally.

- Finance closes revenue with spreadsheets instead of a controlled workflow.

That's when a supposedly simple model turns into recurring cleanup.

Revenue Recognition in Practice With Worked Examples

Theory helps. Math is better.

This section shows how revenue recognition works in the kinds of companies that struggle with it: SaaS businesses with setup fees, agencies with project work, and subscription businesses shipping goods over time.

For a more industry-specific walkthrough, see this guide to revenue recognition in software industry.

Example 1 SaaS contract with annual prepayment and setup

A SaaS company signs this deal on January 1:

- Annual software subscription: $24,000

- One-time setup service: $6,000

- Total contract value billed upfront: $30,000

Assume setup is a distinct performance obligation completed in January, and the subscription is recognized ratably over 12 months.

What happens at cash receipt

When the customer pays upfront:

| Journal entry at cash receipt | Debit | Credit |

|---|---|---|

| Cash | $30,000 | |

| Deferred revenue | $30,000 |

You have cash. You have not yet earned all the revenue.

January revenue recognition

Setup is complete in January, so you recognize the full $6,000 for setup. Subscription revenue for January is $24,000 / 12 = $2,000.

| January revenue entry | Debit | Credit |

|---|---|---|

| Deferred revenue | $8,000 | |

| Setup revenue | $6,000 | |

| Subscription revenue | $2,000 |

Deferred revenue after January is $22,000.

February through December

Each month after that:

| Monthly entry | Debit | Credit |

|---|---|---|

| Deferred revenue | $2,000 | |

| Subscription revenue | $2,000 |

By year end, the contract is fully recognized.

A lot of founders book the full $30,000 in January because that's when Stripe or the wire clears. That's wrong. It inflates early revenue, crushes later comparability, and misstates deferred revenue.

For scaling SaaS firms, deferred revenue often averages 20% to 30% of ARR based on industry benchmarks. Mishandling that balance can badly distort your financial position for investors. I already cited the source for that benchmark earlier in the article, so I won't repeat the link here.

Example 2 Agency project with over-time recognition

A digital agency signs a fixed-fee website and brand project for $40,000.

The contract includes strategy, creative production, and launch support. Assume the work is treated as one combined performance obligation recognized over time because the agency measures progress based on work completed.

The client pays:

- $20,000 upfront deposit

- $20,000 on final delivery

Entry when deposit is received

| Deposit entry | Debit | Credit |

|---|---|---|

| Cash | $20,000 | |

| Deferred revenue | $20,000 |

At this point, the deposit is not automatically revenue.

Mid-project recognition

Assume that by month end, the agency has completed 25% of the total project effort. Revenue recognized is 25% x $40,000 = $10,000.

| Month-end entry | Debit | Credit |

|---|---|---|

| Deferred revenue or contract asset | $10,000 | |

| Project revenue | $10,000 |

If the agency has recognized more revenue than it has billed, it may need a contract asset rather than reducing deferred revenue directly. The exact entry depends on billing timing.

Agencies often go wrong by tying revenue to invoice timing instead of actual delivery. That makes monthly performance look erratic and breaks margin analysis.

If your agency revenue spikes when invoices go out instead of when work gets done, your P&L is telling a billing story, not an operating story.

Example 3 Subscription box business

An e-commerce company sells a prepaid 3-month subscription box for $90 on January 1.

The customer is promised one shipment each month for three months. Revenue is recognized when each box ships.

At order date

| Entry on payment | Debit | Credit |

|---|---|---|

| Cash | $90 | |

| Deferred revenue | $90 |

At each monthly shipment

Each box represents $30 of revenue.

| Entry at shipment | Debit | Credit |

|---|---|---|

| Deferred revenue | $30 | |

| Subscription box revenue | $30 |

This is straightforward, but founders still get it wrong when they book all prepaid subscription cash on day one.

What these examples have in common

Different industries. Same principle.

- Cash receipt doesn't control revenue timing

- Performance obligations do

- Deferred revenue is normal

- Bundled contracts require separation and judgment

If your team is doing this in spreadsheets and "fixing it at year end," you're not managing revenue recognition. You're postponing the problem.

Common Revenue Recognition Pitfalls and Red Flags

The biggest revenue recognition mistakes aren't obscure technical issues. They're routine habits that break under scrutiny.

Red flag 1 You book annual deals upfront

This is the classic SaaS mistake.

You invoice for a year, collect cash, and book the whole thing immediately. That overstates current revenue and understates deferred revenue. It also creates ugly trend lines in MRR and ARR reporting.

The fix is simple in concept. Recognize the hosting or subscription element over the service period. The work is operationally harder when contracts start mid-month, include credits, or change during the term.

Red flag 2 You treat bundled contracts as one thing

A contract that includes software, onboarding, training, support, and custom work isn't automatically one performance obligation.

When finance doesn't separate distinct promises, revenue gets recognized on the wrong timeline. That usually shows up as:

- Lumpy revenue with unexplained spikes

- Weak gross margin data by service line

- Audit questions about what was delivered and when

Red flag 3 Variable consideration is handled casually

A 2024 KPMG handbook notes that 40% of SaaS audits flag disputes related to variable consideration. If your pricing includes usage-based fees, credits, rebates, or true-ups, this is a high-risk area.

Founders often do one of two bad things:

- Ignore variability and wait until cash lands.

- Estimate aggressively and recognize too much too early.

Both approaches are sloppy.

To see how practitioners talk through these issues, this walkthrough is useful:

Red flag 4 Contract modifications are an afterthought

Upgrades, downgrades, added users, scope changes, extended support, and revised timelines all affect revenue recognition.

Founders usually see these as sales or delivery changes. Accounting sees them as contract modifications that may require reallocation, prospective changes, or separate treatment depending on the facts.

If your team tracks modifications in Slack and not in a controlled contract process, you're inviting errors.

Red flag 5 You can't support your SSP logic

Standalone selling prices need support. "That's what sales usually charges" isn't a policy.

If you discount heavily, negotiate custom deals, or rarely sell components separately, you still need a defensible SSP approach. Without it, your allocation method is inconsistent and vulnerable in review.

Warning sign: If two finance team members would allocate the same contract differently, your policy isn't mature enough.

Red flag 6 Month-end close depends on heroic spreadsheet work

This is the hidden operational problem behind a lot of technical errors.

When revenue schedules live in disconnected spreadsheets, every new contract, amendment, or billing exception creates manual risk. You stop doing accounting policy and start doing spreadsheet triage.

If any of these sound familiar, don't argue with the standard. Fix the workflow.

Your Implementation and Controls Checklist

Revenue recognition gets manageable when you stop treating it like an annual audit project and build it into monthly operations.

A 2024 KPMG handbook notes that 40% of SaaS audits flag disputes related to variable consideration, and that automated ASC 606 workflows in platforms like NetSuite or Xero can reduce close times by 3 to 5 days and bring error rates below 1% according to the KPMG revenue recognition handbook.

Process checklist

Start with policy, not software.

- Write a revenue recognition policy: Document how you identify contracts, performance obligations, transaction price, SSP allocation, and timing of recognition.

- Create a contract review workflow: Finance should review signed order forms, SOWs, renewals, and amendments before month-end.

- Define SSP support: Use a repeatable method and keep the backup. If SSPs are estimated, document the logic.

- Map common deal types: Annual SaaS, implementation bundles, prepaid retainers, milestone projects, and usage-based plans should each have a standard treatment.

- Set a modification protocol: Every upgrade, downgrade, credit, extension, and scope change needs accounting review.

Systems checklist

If your contracts are getting more complex, your accounting stack needs to catch up.

| System area | What good looks like | What breaks down |

|---|---|---|

| Billing | Stripe, Shopify, or invoicing platform feeds clean data | Manual exports and rekeying |

| Accounting | QuickBooks, Xero, or NetSuite configured for deferred revenue | Revenue booked from bank feeds |

| Integrations | Contract and billing data flows into accounting reliably | Sales and finance using different source files |

| Automation | ASC 606 schedules update with amendments | Spreadsheet schedules maintained by hand |

If you're evaluating tools or process redesign, it also helps to review how teams simplify financial compliance when ERP controls, automation, and audit support need to work together.

Controls checklist

Controls aren't bureaucracy. They're what keep one bad contract from infecting your reporting.

- Reconcile deferred revenue monthly: Tie opening balance, billings, recognition, and ending balance.

- Review exceptions separately: Usage-based contracts, credits, nonstandard discounts, and custom terms deserve their own review queue.

- Lock contract documentation: Finance should work from final executed agreements, not screenshots or email summaries.

- Approve manual journals: Revenue-related entries should have review and support before posting.

- Audit the close process: Use a formal review list like this checklist for auditors so your backup is ready before diligence starts.

The practical recommendation

If you have more than a handful of active contracts with different terms, stop relying on memory and month-end improvisation. Build the policy, wire the systems, and enforce the controls.

That's what makes revenue recognition sustainable.

Is It Time to Partner with an Outsourced Controller

There comes a point where DIY accounting stops being scrappy and starts being reckless.

If any of these are true, you've probably reached that point:

- You're above $1M in revenue and still closing from spreadsheets

- You sell bundled contracts with subscriptions plus services

- Your pricing includes usage, credits, or nonstandard terms

- Fundraising, lending review, or an audit is approaching

- Month-end close drags past a week

- You can't explain deferred revenue cleanly

- Sales changes contracts faster than finance can evaluate them

What an outsourced controller should actually fix

Not just bookkeeping. Not just "keeping things organized."

You need someone who can:

| Need | What competent controller support should deliver |

|---|---|

| Revenue accuracy | Clear ASC 606 treatment by contract type |

| Close discipline | A reliable monthly close with documented reviews |

| Investor readiness | Financials that hold up in diligence |

| Systems cleanup | Better use of QuickBooks, Xero, NetSuite, Stripe, and related tools |

| Decision support | Revenue and margin reporting you can trust |

If you're comparing options, this overview of outsourced controller services is a useful place to start.

My blunt recommendation

Don't wait until the audit partner, investor, or buyer finds the weakness for you.

If your business has recurring revenue, bundled services, modifications, or prepaid contracts, you need someone who understands both accounting policy and operational execution. A good outsourced controller closes that gap. A weak one just books journals after the fact.

The right time to fix revenue recognition is before it becomes a diligence issue.

If your team needs investor-ready financials, a faster close, and a cleaner revenue recognition process, talk to Jumpstart Partners. They work with growing SaaS, agency, and services businesses that have outgrown DIY accounting and need controller-level support that holds up under pressure.