Financial Operations

ACH Payment Processor: A Guide for SaaS & Agencies

Choose the right ACH payment processor. Our guide covers fees, timing, and integration for SaaS and service firms to cut costs and improve cash flow.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readYour ACH processor is not a back-office tool. It is a margin decision, a cash flow decision, and a headcount decision.

For SaaS, agencies, and professional services firms between $500K and $20M in revenue, ACH should sit inside the core finance stack, not off to the side. In a recent year, the ACH Network handled tens of billions of payments and tens of trillions of dollars in value. That scale highlights two realities for your business. ACH is already standard financial infrastructure for B2B payments. If your workflow is still card-first for recurring invoices, annual contracts, or larger collections, you are likely paying too much and creating extra cleanup work for accounting.

The bigger issue is operational. The wrong ACH payment processor does not just raise fees. It slows cash application, creates failed payment follow-up work, and turns month-end close into a manual matching exercise across billing systems, bank activity, and the general ledger.

That is why processor selection should be tied to finance outcomes. You need a provider that fits recurring billing, vendor payments, multi-entity reporting, and clean syncs with your ERP and accounting tools. If margin pressure is already showing up in your numbers, start with the payment rail mix. It is one of the faster ways to improve profit margins without adding revenue.

Stop Overpaying for Payments and Wasting 80% on Card Fees

Card-first billing is a margin leak.

If your company collects recurring invoices, annual contracts, or larger retainers by card, you are volunteering for higher processing costs and harder reconciliation. For a business between $500K and $20M in revenue, that is not a minor preference inside payments. It changes gross margin, cash application workload, and the amount of finance labor required to close the books.

What the waste looks like in practice

Run the math on a simple billing mix.

| Scenario | Annual customer payments | Card fee assumption | Processing cost |

|---|---|---|---|

| Card-heavy billing | $1,000,000 | 3% | $30,000 |

| Lower card fee case | $1,000,000 | 2% | $20,000 |

Now compare that with ACH pricing, which is usually structured as a flat per-transaction fee instead of a percentage of revenue. On larger invoices and recurring collections, that pricing model changes the economics fast. If the same $1,000,000 is collected through 100 ACH payments, your total cost can land closer to tens or hundreds of dollars than tens of thousands.

That difference goes straight to EBITDA.

It also affects operations. Card-heavy businesses deal with more fee drag on every successful payment, then still spend finance time matching deposits, fees, disputes, and processor reports back to invoices. ACH does not solve reconciliation by itself, but it gives you a better starting point if your processor supports clean remittance data, customer-level identifiers, and direct syncs into the rest of your finance stack.

Where ACH fits best

Use cards where speed and convenience improve conversion. Use ACH where invoice size, contract value, and repeat billing justify tighter cost control.

That usually means:

- monthly retainers

- annual software contracts

- installment billing

- customer payments above your standard card comfort threshold

- vendor payouts and intercompany movement where audit trail matters

This is the shift many founders miss. Payment rail choice is not only about acceptance. It is about whether finance can scale collections without adding manual work every quarter. Teams applying strategies for financial sector automation already understand the pattern. Standardized payment flows reduce exception handling, speed up reconciliation, and free accounting staff for analysis instead of cleanup.

ACH is standard infrastructure, not a fallback

ACH is already established at national scale, as noted earlier. Treating it as a secondary option is a mistake.

For scaling companies, ACH should be the default path for predictable B2B payments unless card acceptance clearly produces better commercial results. That is the right policy for margin discipline. It is also the right policy for multi-entity finance teams that need cleaner settlement tracking across billing platforms, bank accounts, and the general ledger.

If you want a faster route to better operating profit, start with payment mix before you cut headcount or chase minor software savings. These strategies for improving profit margins belong in the same discussion as your ACH processor decision.

How ACH Transactions Work and Impact Your Cash Flow

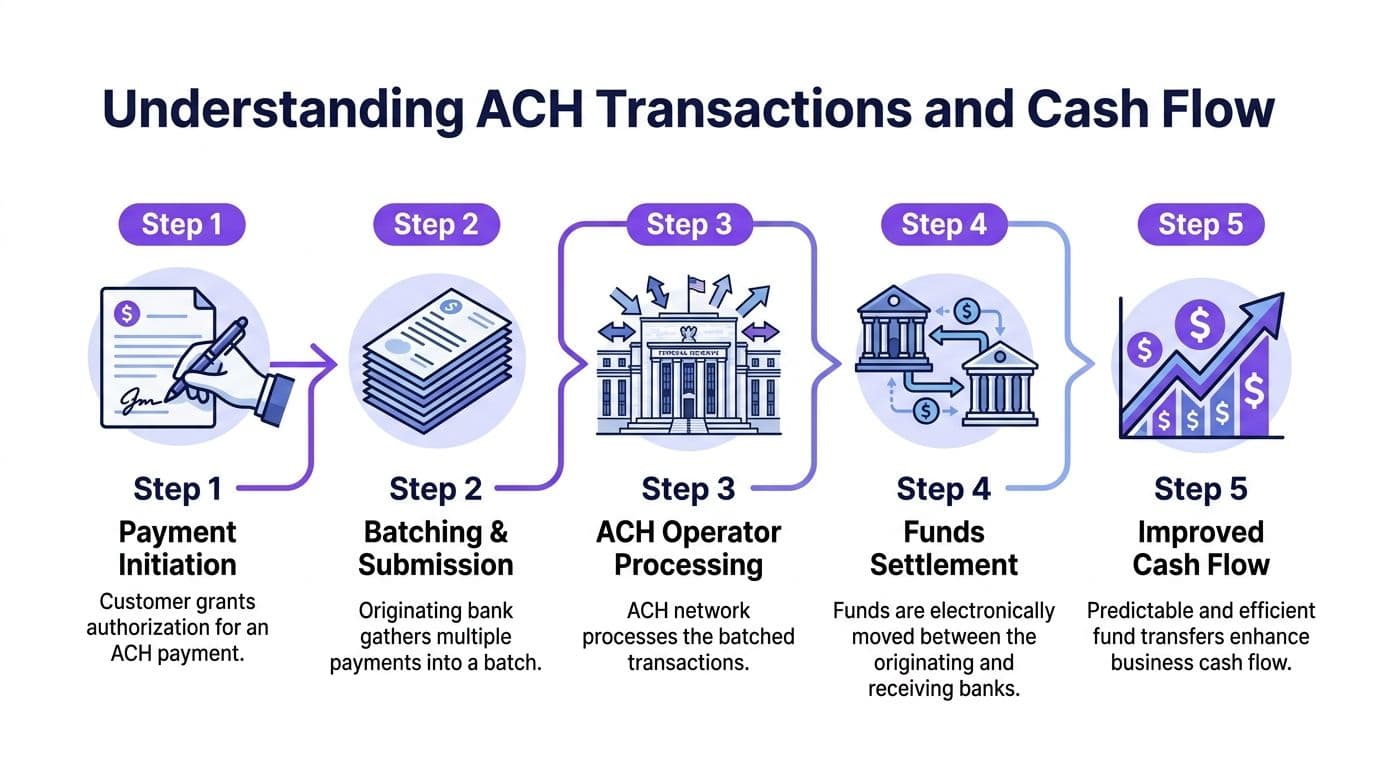

ACH works like a scheduled freight system, not an on-demand courier. That distinction matters because your cash flow forecast depends on it.

With cards, authorization feels immediate. With ACH, your processor gathers transactions into batches, sends them through an ACH Operator, and the receiving bank posts them on that schedule. According to Plaid's ACH processing overview, ACH processing commonly happens three to six times per day, and if a payment misses the processor's or operator's cutoff, it typically settles on the next business day.

The five players and steps that matter

You don't need to memorize payments jargon, but you do need to understand the flow:

-

Customer authorizes payment

Your customer approves a debit from their bank account. -

Your processor or originating bank creates the batch Timing starts to matter operationally at this stage.

-

The file goes to an ACH Operator

The operator routes the transactions through the network. -

The receiving bank gets the entry

The RDFI receives and posts the transaction. -

Settlement hits your books and your bank

This is when accounting and cash reporting need to align.

Why cutoff times hit finance harder than founders expect

A missed cutoff doesn't just delay funds. It distorts your reporting if your team books cash too early, applies receipts to the wrong date, or tells leadership that a large customer payment has landed when it's still in flight.

That creates three avoidable problems:

- Forecast noise that makes weekly cash calls less credible

- Collections confusion when AR says paid but bank says not yet

- Customer friction when support promises one timeline and the processor delivers another

A good ACH setup doesn't just move money. It gives your team confidence about when money will actually arrive.

Configure operations, not just technology

Your ach payment processor is partly a software choice and partly an operating discipline. You need clear internal rules for cutoff times, daily review, and exception handling. If you automate billing without redesigning how your team monitors settlement windows, you've only automated confusion.

That's why ACH belongs inside a broader finance workflow design. If you're reworking billing and collections, it helps to study how other teams approach strategies for financial sector automation. The point isn't to add more tools. It's to remove handoffs that create timing errors.

For CEOs, the takeaway is simple. Cash isn't available when the invoice is sent, and it isn't always available when the customer authorizes payment. Cash is available when the batch clears and settles. If you're serious about tighter forecasting, build ACH timing into your cash flow management process.

ACH vs Cards vs Wires A Cost-Benefit Analysis

Payment method is a margin decision. If you let customers default to cards for every invoice, you are choosing higher fees, weaker cash retention, and more revenue leakage than your P&L needs to absorb.

ACH, cards, and wires each have a place. The right choice depends on transaction size, urgency, customer behavior, and how much manual work your finance team can tolerate. For companies scaling through recurring billing, vendor payouts, and multi-entity accounting, the main question is not just speed. It is total cost to collect and total effort to reconcile.

Payment Method Cost and Speed Comparison

| Method | Typical Cost | Settlement Speed | Best For |

|---|---|---|---|

| ACH | Usually a fixed per-transaction fee | Batch-based and processor-dependent | Recurring billing, larger invoices, vendor payments |

| Credit cards | Usually a percentage of payment volume | Fast authorization | Self-serve signup, checkout, smaller transactions |

| Wires | Usually a higher flat fee | Fast bank-to-bank movement | Urgent, high-value, one-time transfers |

A worked example on a $10,000 invoice

As noted earlier in Tratta's analysis, ACH is commonly priced as a low fixed transaction fee, while cards are commonly priced as a percentage of the invoice.

For a $10,000 invoice, the economics are obvious:

| Method | Fee assumption | Estimated fee | Net cash received |

|---|---|---|---|

| ACH | $0.20 per transaction | $0.20 | $9,999.80 |

| ACH | $1.50 per transaction | $1.50 | $9,998.50 |

| Card | 2% | $200 | $9,800 |

| Card | 4% | $400 | $9,600 |

A founder who accepts card payments on every five-figure invoice is usually buying convenience with gross margin.

That can be rational for acquisition. It is a poor default for established B2B accounts, annual contracts, retainer invoices, and other payments where the customer relationship already exists. In those cases, ACH usually produces better unit economics and a cleaner collection process for your finance team. If you are tightening collections, pair payment rail decisions with a stronger accounts receivable management process.

The finance view by use case

Use cards where speed of authorization improves conversion. That includes self-serve signup, low-ticket purchases, and situations where asking for bank details would reduce close rates.

Use ACH for repeatable collections. Monthly retainers, subscription invoices, implementation milestones, and larger customer payments usually belong here because the fee structure is far more favorable as ticket size rises.

Use wires for exceptions. Large one-off transfers, acquisitions, escrow, or urgent same-day movements can justify the cost and manual handling.

This matters even more for firms selling across regions. Teams evaluating cross-border collections may also compare local banking workflows and B2B payment solutions for MENA businesses alongside domestic ACH options.

Common objections, answered clearly

"Cards are easier for customers."

Yes. They are also more expensive for you. Keep that convenience where it drives revenue. Remove it where it only inflates payment costs.

"Wires feel safer for large payments."

They feel controlled because they are manual. They also create more touchpoints, more proof-of-payment chasing, and more reconciliation work.

"ACH is too slow."

Speed matters for urgent transfers. Predictability matters more for routine B2B collections. If you bill on a schedule and manage terms correctly, ACH fits the job better than cards or wires for many transactions.

Controller's view: Match the rail to the economics. Cards help you win business. ACH helps you keep more of it. Wires solve narrow timing problems and should stay rare.

A practical policy works best. Default to cards for acquisition, default to ACH for recurring B2B billing and larger invoices, and approve wires only when urgency outweighs cost and manual effort.

How to Select an ACH Payment Processor

Choose your ACH processor like you would choose a controller hire. Optimize for control, visibility, and scale. A low fee means nothing if your team loses days every month cleaning up settlements, returns, and entity-level reporting.

For a company in the $500K to $20M range, processor selection is an operating model decision. It affects DSO, close speed, customer billing reliability, and how many manual workarounds your finance team carries into the next year. If you run recurring billing, vendor payouts, or multiple entities, the wrong setup creates friction in every downstream workflow.

What matters in selection

Use this order of operations.

-

Reconciliation design

Start here. You need clear settlement reports, return codes, fee detail, and transaction IDs that tie back to invoices and ledger activity. If finance cannot trace money from invoice to bank deposit, month-end gets slower and cash reporting gets less reliable. -

Fit with your billing model

Subscription billing, usage billing, installment plans, and one-time invoicing do not behave the same way. Pick a processor that supports your collections logic without custom patches. -

Multi-entity support

Separate entities need separate bank accounts, reporting views, permissions, and clean audit trails. If the platform forces your team into manual tagging or off-platform spreadsheets, skip it. -

Bank verification and risk controls

Good verification reduces returns and support tickets. It also shortens the time from signup to first successful debit, which improves cash conversion. -

Exception handling

Returns, rejects, revoked authorizations, and bank account updates need clear workflows. Hidden logs and vague status labels create customer service problems and accounting errors.

Single processor or orchestration layer

The core question for scaling firms is whether to consolidate to one processor or use a middleware layer that coordinates several systems.

Use one processor when billing is simple, your entity structure is straightforward, and AR sits in one system. Add orchestration when collections, vendor payments, and accounting live in separate tools or separate business units. If your team is already stitching together billing data, bank activity, and ERP entries by hand, buying another point solution will not fix the problem. You need cleaner payment architecture.

A practical rule looks like this:

| Situation | Better fit |

|---|---|

| One entity, one billing motion, limited exceptions | Single ACH processor |

| Multiple entities, mixed billing models, separate AP and AR systems | Middleware or orchestration layer |

| Heavy reconciliation work across billing, ERP, and bank data | Processor plus accounting workflow redesign |

Regional requirements can change the answer. If you sell or collect outside the US, payment rail decisions get more complex. This overview of B2B payment solutions for MENA businesses is useful context for teams comparing domestic ACH design with regional banking workflows.

Red flags

Walk away if you see any of these:

- No exportable reporting for settlements, fees, reversals, and returns

- Weak entity separation across accounts, permissions, or reporting

- Unclear underwriting timeline that puts implementation at risk

- No defined retry logic for failed debits

- Thin accounting integrations that push your team into CSV imports every month

If the demo focuses on payment acceptance and barely touches ledger impact, you are buying convenience for sales, not control for finance.

Processor selection should sit inside a broader receivables design. Teams that document accounts receivable management workflows before implementation make better decisions on posting logic, retries, collections ownership, and exception handling.

Here's a useful walkthrough to ground the evaluation in product reality:

One recommendation. Do not let the payments team choose the processor alone. Bring in the controller, the billing owner, and the operator responsible for close. They will live with the reconciliation burden, cash timing issues, and reporting gaps long after implementation ends.

Integrating ACH with QuickBooks Stripe and Xero

Integration is where good ACH strategy either becomes a smooth close process or turns into accounting cleanup.

The biggest mistake I see is posting ACH receipts directly to revenue or cash the moment the payment is initiated. That creates timing errors because initiation and settlement aren't the same event. Your books need to reflect that difference.

The right accounting workflow

Use a clearing account.

When the customer initiates an ACH payment, post it to an ACH clearing account, not straight to your operating bank account. When the funds settle, clear that balance into cash. This one step prevents false cash balances and reduces reconciliation noise.

A simple workflow looks like this:

-

Invoice is issued

AR is open. -

Customer authorizes ACH payment

Reduce AR. Increase ACH clearing. -

Processor settles funds

Reduce ACH clearing. Increase bank cash. -

Processor fees or returns are posted

Book them separately and tie them to the processor report.

Stripe versus standalone ACH processors

If you use Stripe for ACH, the advantage is convenience. Billing, collection, and payment status often live in one ecosystem. That can work well for SaaS firms with straightforward subscription logic.

If you use a standalone ACH processor, you usually get more control over bank debit workflows, processor specialization, or payment routing. The tradeoff is that accounting design matters more because data is coming from multiple systems.

That's where your stack decisions need discipline:

- QuickBooks Online works well when you keep the chart of accounts clean and use dedicated clearing accounts.

- Xero can handle the same workflow, but only if bank rules and payment mappings are configured intentionally.

- Stripe helps with payment event visibility, but you still need ledger rules for settlement timing.

Book the economic event when it happens. Not when the dashboard first looks successful.

What to standardize before go-live

Before you turn ACH on, lock these down:

- Naming conventions for payment methods and clearing accounts

- Return handling rules so failed debits reverse the right invoice or customer balance

- Daily ownership for settlement review

- Month-end tie-out process between processor reports and the general ledger

If your team is still tightening invoicing workflow, this guide on creating invoices in QuickBooks is a practical companion because ACH works best when invoice structure is clean before payment collection begins.

One operational note. If you want outside support designing this workflow, firms like Stripe implementation partners, outsourced controllers, and finance systems consultants can help map processor data into the ledger. Jumpstart Partners, for example, works on controller and bookkeeping workflows for businesses using platforms such as QuickBooks, Xero, Stripe, and related finance tools.

Your ACH Implementation and Optimization Checklist

Most ACH rollouts fail in boring ways. Not because the processor breaks, but because nobody defines ownership, timing rules, or what happens when payments fail.

Implementation checklist

Use this sequence:

-

Choose the workflow first

Decide whether ACH will handle subscriptions, invoices, vendor payouts, or all three. Don't buy software before deciding the operating model. -

Confirm underwriting requirements early

Processor onboarding can stall if ownership documents, bank details, or business verification are incomplete. -

Map the ledger before the first live payment

Set up clearing accounts, fee accounts, return handling, and entity-level mapping before launch. -

Define customer-facing payment rules

Decide where ACH is the default, where cards remain available, and how authorization language appears. -

Run a controlled pilot

Start with a small set of known customers or internal transactions so finance can test posting and settlement behavior.

Reducing payment failures and disputes

You will have returns. Plan for them.

Build a simple workflow around three categories:

| Failure type | What your team should do |

|---|---|

| Insufficient funds | Retry based on your policy and notify the customer clearly |

| Unauthorized debit | Pause future debits and review authorization records |

| Bad account data | Update bank details and re-verify before retrying |

Don't treat returns as one-off support issues. Treat them as a measurable process.

Here's the operating rhythm I recommend:

- Daily review of new settlements and returns

- Weekly review of failed-payment patterns by customer segment

- Month-end review of clearing-account aging and unapplied cash

The best ACH process isn't the one with no failures. It's the one where failures are contained, visible, and resolved fast.

If your close process still depends on heroic cleanup, tighten that first. This month-end close checklist template is useful because ACH only improves operations when your accounting cadence is already disciplined.

Make ACH Your Competitive Advantage

Most founders think of ACH as a cheaper way to get paid. That undersells it.

A well-chosen ach payment processor gives you lower payment costs, cleaner collections, more predictable cash timing, and a finance stack that scales without constant manual intervention. That matters when you're trying to improve EBITDA, shorten close, and show investor-ready financials.

It also matters because ACH is not fringe infrastructure. According to Nacha's ACH payments fact sheet, the modern ACH Network processed 35.2 billion payments valued at $93 trillion in 2025, and it reaches all U.S. bank and credit union accounts. At that scale, reliability and compliance are not optional. They're table stakes.

The companies that benefit most from ACH don't just turn it on. They design around it. They choose where ACH should replace cards. They build reconciliation into the ledger. They create rules for settlement timing, retries, returns, and multi-entity reporting. That discipline improves financial visibility and reduces friction as the business grows.

If you're still treating payment processing as a tactical tool, you're leaving margin and operational efficiency on the table.

If you want help designing an ACH workflow that improves cash visibility and month-end accuracy, talk to Jumpstart Partners. They work with growing SaaS, agency, and service businesses on controller, bookkeeping, and finance system processes that connect billing, reconciliation, and reporting into a usable operating model.