Financial Operations

Branch Accounting: A Guide for Scaling Your Business

Master branch accounting to scale your business. Our guide covers setup, consolidation, software, and audit-readiness for SaaS, agency, and e-commerce leaders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readYour accounting system worked when everyone sat in one office, sold one offer, and ran expenses through one bank account. It breaks the moment you add a second location, a foreign sales team, or even a separate operating unit with different economics.

That break usually doesn't look dramatic at first. It looks like a messy P&L, a debate over whether the London team is profitable, and a close process full of spreadsheet patches. You're still getting financial statements. They're just no longer answering the questions a CEO needs answered.

For SaaS companies, agencies, and professional services firms in the $500K to $20M revenue range, financial segmentation by unit transitions from a retail or banking concept to a control system for scale. If you can't isolate performance by office, team, or country, you're making hiring, pricing, and expansion decisions with blurred data.

Table of Contents

- The Scaling Problem You Don't See Coming

- Red Flags You Need Branch Accounting Now

- Core Concepts and Setup Considerations

- Reporting and Consolidation Workflows

- Mini Case Studies for Modern Businesses

- Software and Investor-Ready Controls

- Your Branch Accounting Action Plan

The Scaling Problem You Don't See Coming

You hire a sales lead in London, keep product and operations in New York, and suddenly your single-entity P&L turns into a black box. Revenue is booked correctly at the top level, but you can't tell which team created it, which office consumed the margin, or whether expansion is working.

This is the issue. The problem isn't bookkeeping volume. The problem is decision blindness.

Branch accounting has been around for a long time. Investopedia's history of branch accounting traces it back to the 14th century, with Venetian banks and merchants using it to manage multi-location operations across a timeline of more than 680 years. The principle hasn't changed. You still need local accountability with centralized financial control.

Why single-entity reporting fails fast

A standard P&L answers one question: did the business make money?

A scaling business needs different answers:

- Which office is profitable

- Which team is overstaffed

- Which region is dragging cash flow

- Whether expansion is creating value or hiding losses

If your U.S. delivery team is subsidizing your new international sales office, your top-line growth can mask a bad operating decision for months.

Practical rule: If managers are responsible for location or team performance, your accounting has to mirror that responsibility.

This gets even more urgent if growth includes distributed locations, licensed operations, or future expansion models. If you're evaluating regional expansion or even franchise development, you need a finance structure that separates unit economics before complexity multiplies.

For founders who already feel this strain, the next step is usually broader than location tagging. It's a reporting architecture problem, not a cleanup problem. That's where a more structured multi-entity accounting approach often enters the conversation, especially once branches, divisions, or country teams stop behaving like one business unit.

Red Flags You Need Branch Accounting Now

You don't need branch accounting because it sounds impressive. You need it when your current setup stops producing clean, decision-ready numbers.

Your managers own results, but your books don't

If you pay commissions, bonuses, or team budgets by office or region, a single undivided P&L creates conflict. Leaders start arguing over shared revenue, shared labor, and who should absorb overhead.

That's not a people problem. It's a structure problem.

You need branch accounting when:

- One team closes work and another team delivers it. Your revenue sits in one line, but your margin lives somewhere else.

- You've opened a second office or country presence. You need separate visibility into payroll, software, travel, and local operating costs.

- Your board or investors ask for performance by location. If you answer with spreadsheet allocations, you're already behind.

You're seeing recurring reconciliation friction

A lot of founders miss this sign because the business still appears to function. Cash is moving. Invoices go out. Payroll runs. But every month, finance has to “figure out” what belongs to whom.

Common signs include:

| Warning sign | What it usually means |

|---|---|

| Transfers between teams or offices are booked inconsistently | You don't have a defined inter-branch structure |

| Shared costs are allocated differently each month | Management reporting isn't tied to accounting design |

| Local expenses get coded to generic overhead | Branch profitability is being understated or distorted |

| You need manual spreadsheets to produce branch P&Ls | Your system is tracking after the fact, not at entry |

If closing the books requires someone to reconstruct branch performance manually, your accounting system has already fallen behind the business.

Compliance pressure is rising

Branch accounting also becomes mandatory when tax, audit, and reporting expectations get more granular. This is especially true once you operate across states or countries, or once outside stakeholders want branch-level support.

A useful gut check is simple:

- Can you produce a branch-level P&L without rebuilding the numbers manually?

- Can you explain intercompany or inter-branch balances clearly?

- Can you defend how shared expenses are assigned?

- Can you isolate branch tax exposure and revenue activity?

If those answers are no, your finance function has outgrown basic bookkeeping. That usually means you've also outgrown a reactive close process. A good starting point is understanding the broader signs you've outgrown your bookkeeper, because branch accounting problems rarely show up alone.

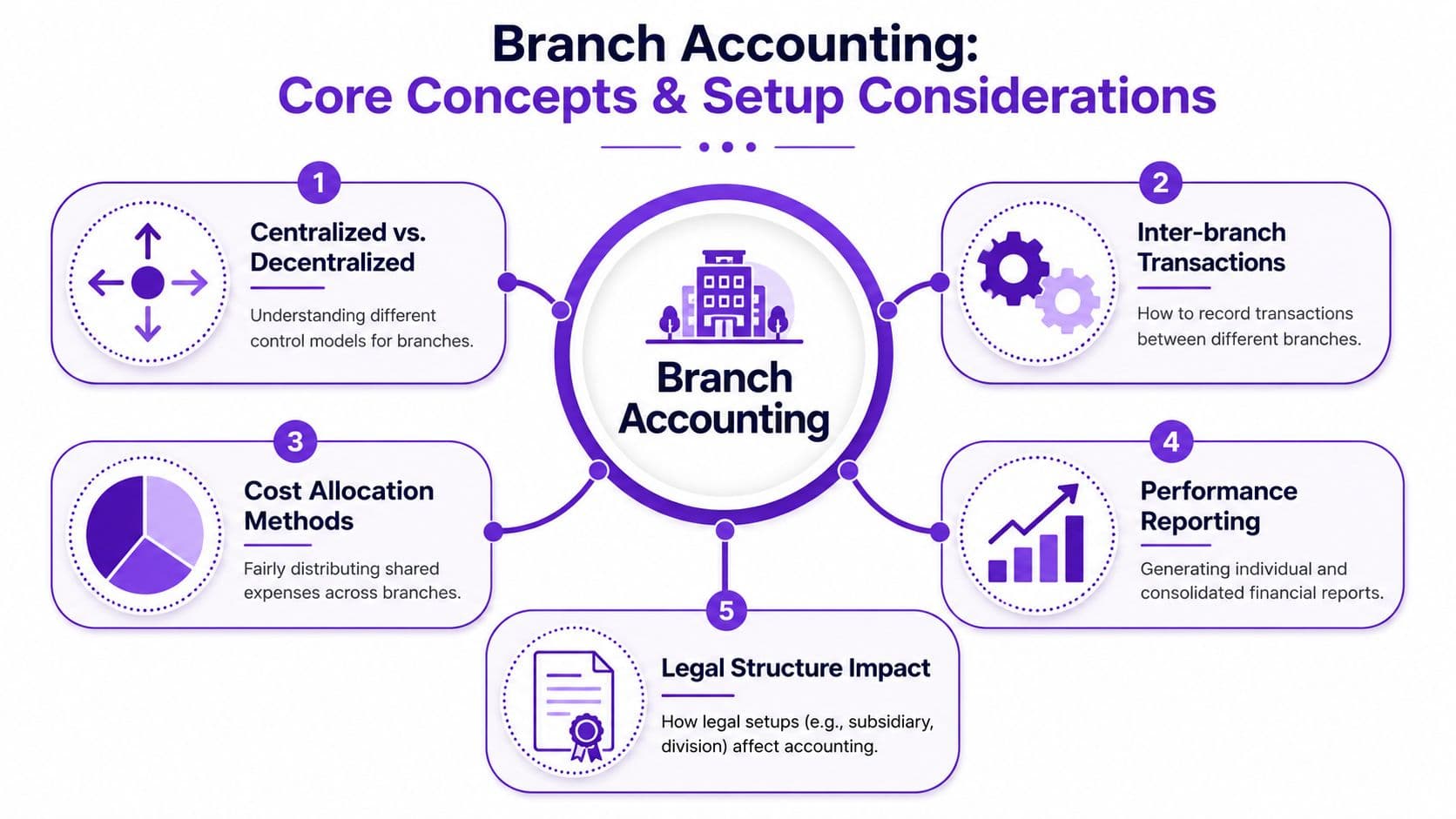

Core Concepts and Setup Considerations

A good branch accounting setup is simple to describe and hard to fake. You need a chart of accounts that supports segmentation, a clean method for internal transfers, and rules that prevent people from inventing branch logic inside spreadsheets.

Start with the accounting architecture, not the reporting wish list.

Build the structure before you build reports

Your first decision is whether branches will keep separate books or whether the head office will control the records centrally. For most companies in this size range, centralized control works better because it reduces inconsistency.

That setup depends on three core elements:

-

Location-aware accounts

Your base chart of accounts should stay clean. Don't create endless duplicate accounts like “Software Expense London” and “Software Expense NYC” unless your system requires it. Use a consistent branch or location dimension wherever possible. -

Inter-branch or head office clearing accounts

If one branch pays for another branch's expense, or head office funds local operations, you need designated accounts for those entries. Otherwise cash movement gets mistaken for expense or revenue. -

Rules for shared-cost allocation

Rent, software, insurance, and leadership payroll often serve more than one branch. Decide the method in advance. Use a repeatable basis tied to how the business operates.

If your account list is already chaotic, fix that first. A structured chart of accounts is the foundation. Without it, branch reporting is just organized guesswork.

A worked example for a SaaS branch setup

Assume you run a U.S. SaaS company with a new EU sales office. In one month:

- The U.S. entity invoices a customer $120,000 annual subscription and $20,000 implementation.

- Under ASC 606, the subscription revenue is recognized $10,000 per month, while the $20,000 implementation fee is recognized at the point in time the work is completed, creating $110,000 of deferred revenue at signing that declines by $10,000 each month according to DualEntry's SaaS accounting example.

- The EU branch earns the commission expense related to that deal.

Here's what many companies get wrong: they book the full sale in one place, book the commission somewhere else, and never connect branch economics to revenue recognition timing.

A cleaner branch view looks like this:

| Item | U.S. head office | EU branch |

|---|---|---|

| Cash received at signing | Records receipt | No direct entry unless local collection applies |

| Deferred revenue | Records liability of $110,000 | No direct liability if branch is dependent |

| Monthly subscription revenue | Recognizes $10,000 | Branch reporting reflects credited performance logic if used internally |

| Implementation revenue | Recognizes $20,000 on completion | Branch may carry selling cost, not revenue, depending on policy |

| Sales commission | May allocate to branch P&L | Expense sits in EU branch cost center |

That's why branch accounting for SaaS isn't just location tagging. It has to align with revenue recognition.

Later in the process, this video gives a useful visual overview of how teams think about branch accounting in practice:

Foreign currency is where weak setups fail

If you have a foreign branch, manual accounting gets dangerous fast. Foreign branch accounting requires the head office to revalue intercompany receivables and branch assets at period-end exchange rates under GAAP and IFRS, and expert analysis notes that without automated ERP-driven currency revaluation, manual adjustments can introduce up to $15K to $25K in period-end errors per foreign branch. That's why automation matters for ASC 830 and IAS 21 compliance, as explained in this foreign branch accounting analysis.

If your team is revaluing balances in Excel, stop. That process doesn't scale, and it doesn't survive audit scrutiny.

Reporting and Consolidation Workflows

Once the setup is right, the monthly workflow should become boring. That's the goal. Good branch accounting removes interpretation from the close.

For most businesses in this range, the practical model is a dependent branch system. The head office keeps control of the books, and the branch operates with financial accountability but not a separate general ledger.

The dependent branch model is usually the right one

In a dependent branch system, the head office maintains a single consolidated Branch Account. Under this approach, the head office debits opening assets to the Branch Account, credits liabilities, and the difference reflects branch net worth. For companies with multiple dependent branches, this centralized method can improve month-end close speed by 30% to 40% when the ERP enforces strict validation rules, according to Phocas Software's discussion of branch accounting.

That benchmark matters because founders often overcomplicate the design. They assume every branch needs full accounting autonomy. Most don't.

Keep branches operationally accountable and financially controlled. Those aren't competing goals.

A simple monthly workflow example

Assume your agency headquarters funds a branch with $18,000 for monthly local operations. During the month, the branch generates $30,000 in billings tied to services delivered under that branch's management responsibility and incurs $12,000 in local payroll expense and $3,000 in software and travel.

A centralized workflow would look like this:

| Step | Head office action | Branch reporting effect |

|---|---|---|

| Funding | Record cash sent to branch clearing or branch account | Branch shows available operating support |

| Revenue entry | Record customer billings and recognized revenue under branch segment rules | Branch P&L captures managed revenue |

| Expense entry | Record payroll and operating costs to branch segment | Branch margin becomes visible |

| Close | Reconcile branch account and eliminate internal balances | Consolidated statements stay clean |

In that example, branch operating contribution before shared overhead is $15,000. That's $30,000 minus $12,000 minus $3,000. You can now evaluate that office on facts instead of anecdotes.

If you want useful management reporting, your branch view should feed directly into a consolidated profit and loss statement. If those reports are produced from different logic, they'll diverge every month.

Mini Case Studies for Modern Businesses

Branch accounting gets real when you apply it to modern operating models. Retail examples aren't enough for a SaaS founder with distributed teams or an agency running delivery across cities.

SaaS with a European sales office

A SaaS company at $1M to $10M revenue doesn't get a pass on accrual complexity. According to OpenView's 2024 SaaS Benchmarks, 78% of SaaS companies in that revenue band use accrual accounting to comply with ASC 606, which requires revenue recognition when control transfers, not when cash is collected, as summarized in Sage's guide citing OpenView's 2024 SaaS Benchmarks.

Now layer in a branch.

A customer prepays $18,000 for a 12-month subscription. As Chargebee explains, $1,500 is recognized monthly and $16,500 remains deferred revenue until later months because “Revenue can only be recognized over time as and when the customer benefits from your product and control is transferred,” from Chargebee's SaaS accounting guide.

If your EU branch sourced that customer, your branch P&L needs to reflect sales effort without breaking the company's revenue recognition policy.

A practical branch snippet might include:

- Revenue segment: Subscription revenue attributed by customer owner or region

- Direct costs: Sales commissions, local payroll, travel

- Shared costs: Allocated platform, leadership, and admin overhead

- Balance sheet support: Deferred revenue remains centrally controlled

Agency with teams in two cities

An agency often thinks it has one business because invoices go through one entity. It doesn't. It has multiple economic engines.

If your Chicago team sells strategy and your Austin team executes production, you need to answer three separate questions:

- Which office originated revenue?

- Which office consumed labor margin?

- Which shared costs belong in branch reporting versus corporate overhead?

A branch-level P&L solves this. It also stops bonus disputes, because each office can be measured on a defined basis instead of informal assumptions.

The right branch report doesn't just show revenue. It shows accountability.

E-commerce or DTC with a separate warehouse operation

Even asset-light companies pick up branch accounting needs once physical operations enter the picture. A warehouse in another state changes cost tracking, fulfillment visibility, and tax support.

Historical use of branch accounting shows why. A JSTOR study on Moravian communal settlements documents branch accounting in 1775 and later notes 55,000 members across 156 congregations in the 1980s, a reminder that the model was built to manage dispersed operations under unified reporting.

For a modern DTC brand, that means:

- Separate warehouse labor and occupancy costs from HQ marketing spend

- Track local inventory-related activity cleanly

- Isolate state-level operating performance when tax and logistics differ

The principle is old. The use case is modern.

Software and Investor-Ready Controls

QuickBooks and Xero can handle some branch reporting. They can't magically create branch accounting discipline if your structure is weak.

That's where founders waste time. They blame software for problems caused by design, then keep layering workarounds onto the same bad process.

Workarounds are fine until they aren't

If you have one legal entity and a small number of internal branches, you can often start with:

- QuickBooks classes or locations for branch-level income and expense tracking

- Xero tracking categories for office or team segmentation

- Managed allocation schedules for shared overhead

- Standardized month-end branch reconciliations before consolidation

That can work for a while. It stops working when foreign currency, deferred revenue complexity, or inter-branch transactions become routine.

Here's the practical comparison:

| Situation | Likely fit |

|---|---|

| One entity, simple location reporting | QuickBooks or Xero with disciplined dimensions |

| Multiple countries, currency revaluation, intercompany complexity | ERP with stronger native controls |

| Investor diligence, audit prep, granular branch tax support | System with robust audit trail and consolidation workflow |

Investor readiness is a controls issue

Software matters, but controls matter more.

If you're preparing for diligence, your branch process needs:

- Defined approval rights for branch spending

- Segregation of duties between payment initiation, coding, and review

- Locked allocation methods for shared costs

- Documented close checklists for branch reconciliations

- Audit-ready support for tax and branch-level reporting decisions

Poor branch design can lead to significant expenses. According to CohnReznick, 72% of public business entities face expanded tabular reconciliation requirements for effective tax rates in 2025 due to misaligned branch-level tax disclosures, which raises the stakes for getting branch reporting right, as noted in CohnReznick's accounting standards update for 2025 and beyond.

If you sell physical goods alongside service or SaaS revenue, integration quality matters too. For brands struggling with order and inventory sync, Spot Inventory Sync addresses Shopify inventory issues in a way that highlights the larger point: operational systems have to feed finance cleanly, or branch reporting degrades fast.

A lot of this becomes easier when you automate recurring reporting logic and reduce manual reconciliation work. Stronger financial reporting automation doesn't replace branch accounting design, but it does make that design usable at scale.

Your Branch Accounting Action Plan

A CEO usually sees the problem too late. The board asks for branch-level margin by country, your VP Sales wants CAC payback by office, and diligence requests a revenue walk from contract to invoice to legal entity. Your team exports one company-wide P&L, then starts rebuilding reality in spreadsheets.

That is the point to fix the model.

For SaaS companies and agencies, branch accounting is not about store tills or bank counters. It is about knowing which team drives revenue, which office burns cash, and whether your ASC 606 process matches how work is sold, delivered, and billed across locations. If you cannot answer those questions in five business days, your finance stack is already behind your growth.

Do these five things next

-

Run a branch visibility test

Take the last two closed months and ask for branch-level revenue, gross margin, payroll, and operating expense by office, team, or country. If the answer requires manual spreadsheet rebuilds, your reporting structure is broken. -

Define the economic units that matter

Set branch reporting based on accountability, not org chart aesthetics. For an agency, that usually means office, client service team, or region. For SaaS, it often means country, sales hub, implementation team, or support center. -

Tie revenue recognition to delivery reality

SaaS and service businesses break here all the time. Sales may sit in London, implementation in New York, and billing in a US entity. Under ASC 606, you need a clean rule for who owns the contract, who fulfills the performance obligation, and how branch-level reporting reflects that activity without inventing fake revenue. -

Choose centralized books with branch reporting

This is the right model for most high-growth companies under $100 million in revenue. Keep one controlled close process, one chart of accounts, and one approval structure. Report by branch through dimensions, classes, locations, or entity overlays. Do not let each office run its own accounting logic unless there is a real statutory reason. -

Set a deadline before fundraising, audit, or expansion

Give your team 60 to 90 days to implement branch reporting rules, allocation logic, and close ownership. Fixing this during diligence costs more, slows the process, and signals weak finance leadership.

“Founders think branch accounting is only for Starbucks, but it's really for any business that needs P&L accountability by location, team, or country. Once your London sales office and your NYC dev team can't be measured on the same P&L, you need to fix your accounting or you're just guessing who creates value.” Jessica Martin, CPA, Partner at Jumpstart Partners

Branch accounting gives management reporting that matches how the business operates. That is how you get faster decisions, cleaner board reporting, and fewer arguments during audit and diligence.