Financial Operations

Mastering Budgets for Nonprofit Organizations

Master budgets for nonprofit organizations. Guide covers operating, program, & capital budgets and fund accounting for founders & finance leaders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··21 min readMost founders assume nonprofit budgeting is simpler than for-profit finance because there’s no equity story and no profit distribution. That assumption is wrong.

The nonprofit sector in the United States collectively raises $3.7 trillion annually and spends $3.5 trillion per year, according to Candid’s analysis of the U.S. social sector. That scale should reset how you think about budgets for nonprofit organizations. This is not lightweight bookkeeping. It’s capital allocation under donor restrictions, board oversight, grant compliance, and public scrutiny.

If you run a SaaS company or agency, you already understand the danger of using the wrong reporting model. Apply a standard startup P&L mindset to a nonprofit and you can misstate program costs, overspend restricted funds, and walk into reporting failures that damage donor trust. In a nonprofit, the budget isn’t just a planning document. It’s an operating control system.

Why Your For-Profit Playbook Will Fail in a Nonprofit

A nonprofit is not a company “without profit.” It’s an organization with a different scoreboard.

In a for-profit business, you optimize for margin, cash, and enterprise value. In a nonprofit, you still need cash discipline, but you also need to prove that funds were used the way donors, grantors, and regulators expect. If your SaaS CFO brain says, “Money is money, we’ll sort it out in reporting,” you’re already off track.

Revenue is not fully fungible

A booked sale in a services firm usually increases your discretion over cash. A restricted donation does not. It behaves more like funds held in escrow for a specific deliverable. You may have cash in the bank and still be unable to use it for payroll, rent, or software if those dollars were committed to a specific program.

That’s the first trap. The second is assuming budget categories are mostly internal management choices. They aren’t. In nonprofit finance, classification affects compliance, donor confidence, and external evaluations.

Bottom line: A nonprofit can look solvent in aggregate and still be operationally stressed because unrestricted cash is tight.

The budget carries reputational risk

For-profit leaders are used to budgets as internal planning tools. Nonprofits don’t get that luxury. Their budgets often become part of grant proposals, board packets, donor conversations, and financial reporting. If the numbers are sloppy, outsiders notice.

This also changes how you think about growth capital. A startup can chase a campaign, miss the forecast, and regroup. A nonprofit that launches an initiative on the assumption that restricted funding can cover adjacent overhead may find out too late that it underfunded core operations.

If you’re exploring campaign-based fundraising, tools and channels matter too. For leaders evaluating donation-driven launches, this guide to Kickstarter for nonprofits is useful because it frames crowdfunding as a structured fundraising vehicle, not a random marketing experiment.

Your standard management lens is incomplete

Here’s the practical shift:

| For-profit habit | Why it fails in a nonprofit | Better nonprofit lens |

|---|---|---|

| Treat all revenue as deployable | Restricted funds have use limits | Track by fund and purpose |

| Focus on one company-wide P&L | One statement hides grant and program realities | Manage multiple budget layers |

| Push overhead down at all costs | Underfunded admin weakens controls and reporting | Budget for full mission delivery |

| Judge health by profit alone | Compliance and fund usage matter as much as cash | Watch budget-to-actual by function |

If you lead a nonprofit like a lean software company with one blended bank account mentality, you’ll overlook inherent constraints. Budgets for nonprofit organizations have to answer a harder question than “Can we afford this?” They have to answer, “Are we allowed to spend this here, and can we prove it?”

The Five Budgets Every Nonprofit Leader Must Master

Most for-profit businesses can run on one master budget plus a cash forecast. Nonprofits need more structure because one view never tells the whole story.

According to WildApricot’s nonprofit budgeting guidance, budgeting for multi-source revenue such as restricted grants, program-related investments, and in-kind donations requires segregated tracking, and 97% of nonprofits operate with small budgets. That’s exactly why a single spreadsheet tab won’t cut it.

Operating budget

This is the master plan for the year. It covers your organization-wide revenue and expense assumptions and tells your board whether the model is viable.

For a for-profit CEO, this is the closest thing to your annual operating plan. It should include all expected revenue sources, all functional expenses, and a view of whether the organization is budgeting a surplus, deficit, or roughly balanced result.

If you need a cleaner foundation for this piece, this breakdown of how to define operating budgets is a useful starting point.

Program budget

A program budget isolates one initiative, comparable to a customer implementation budget, product line budget, or business unit mini-P&L.

If your nonprofit runs youth training, legal aid, or food distribution, each major initiative should have its own budget. That lets you see which programs are fully funded, which rely on unrestricted support, and which are draining cash.

Grant budget

Many for-profit leaders get blindsided regarding grant budgets. A grant budget is not just a funding plan. It’s a compliance document.

If a funder gives money for specific staff time, supplies, travel, or outcomes, your budget needs to mirror those categories. If your actual spending drifts from that structure, you create reporting friction fast. In practical terms, a grant budget is the budget attached to a contract with spending rules.

Restricted funds are not general revenue with nicer branding. They are purpose-bound dollars with an audit trail attached.

Capital budget

This covers long-term asset purchases and larger investments in infrastructure. Building improvements, vehicles, equipment, major systems implementations, and facility projects live here.

For-profit leaders usually understand this quickly. It’s your capex plan. The difference is that in nonprofits, the funding source for capital purchases often matters just as much as the purchase itself. You need to know whether the asset is being funded through a dedicated campaign, a grant, reserves, or unrestricted operating cash.

Cash flow budget

This is the survival budget.

A nonprofit can have pledged revenue, approved grants, and a board-approved operating budget, yet still struggle because cash arrives unevenly. The cash flow budget maps timing. When does money hit? When do payroll, rent, vendors, and program costs go out?

For-profit CEOs know this instinctively. Profit doesn’t pay payroll. Cash does. The same rule applies here, except timing mismatches are often worse because donor and grant disbursements don’t follow your expense calendar.

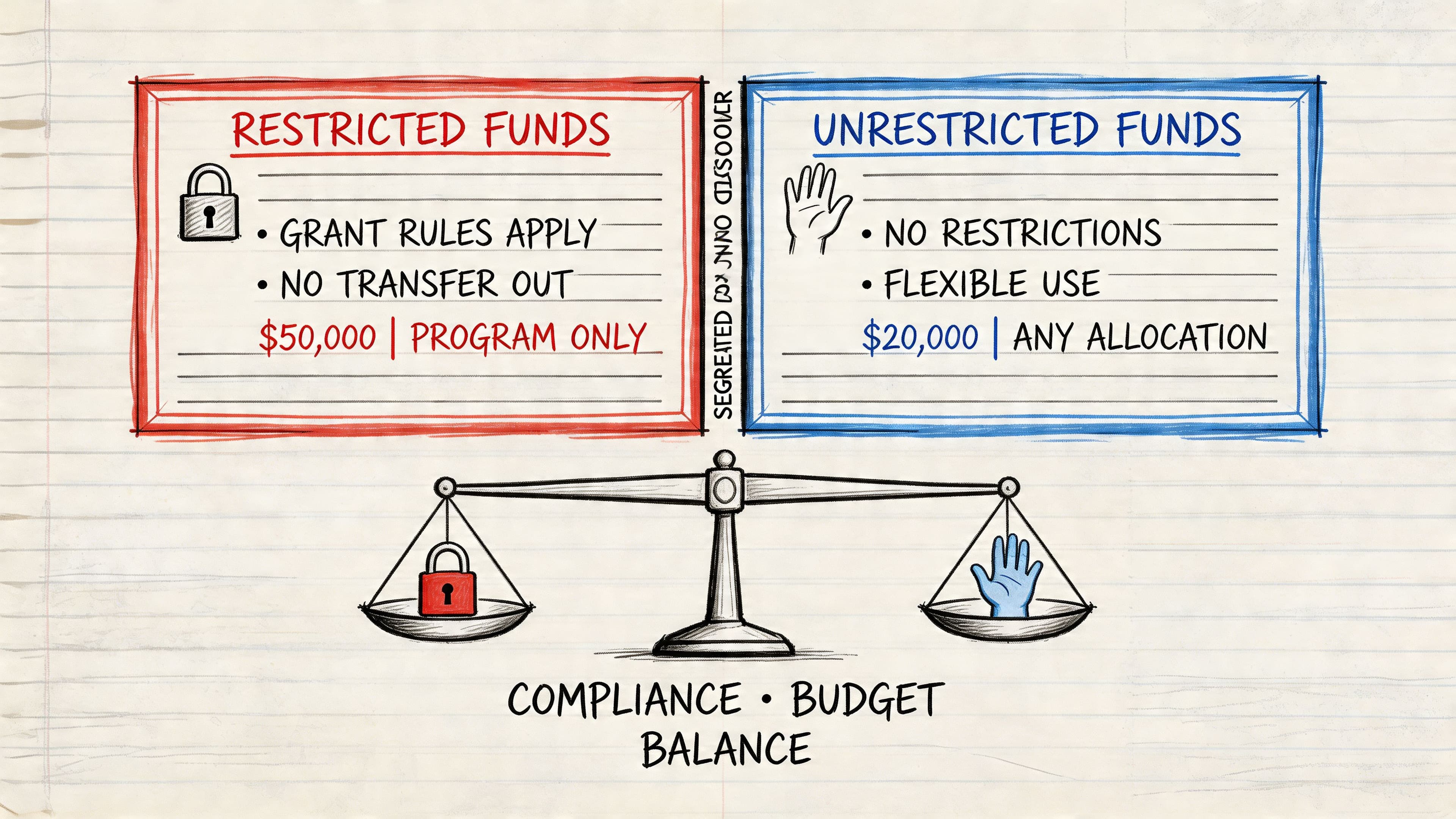

Restricted and unrestricted funds

This isn’t a separate report in every organization, but it is a separate budgeting lens you must master.

Here’s the simplest analogy. Restricted funds are like client prepayments that can only be used for a named scope of work. Unrestricted funds are your general operating dollars. If you blend the two mentally, you’ll make bad decisions even if the bank balance looks healthy.

A quick comparison helps:

| Budget type | What it answers | For-profit analogy |

|---|---|---|

| Operating budget | Is the organization viable this year? | Annual company budget |

| Program budget | What does this initiative actually cost? | Department or product line budget |

| Grant budget | Are we spending according to funder rules? | Contract budget with strict deliverables |

| Capital budget | How will we fund major long-term assets? | Capex plan |

| Cash flow budget | Will cash be there when obligations hit? | Rolling cash forecast |

The leaders who handle budgets for nonprofit organizations well don’t rely on one spreadsheet and hope month-end reporting fills the gaps. They manage these five views together.

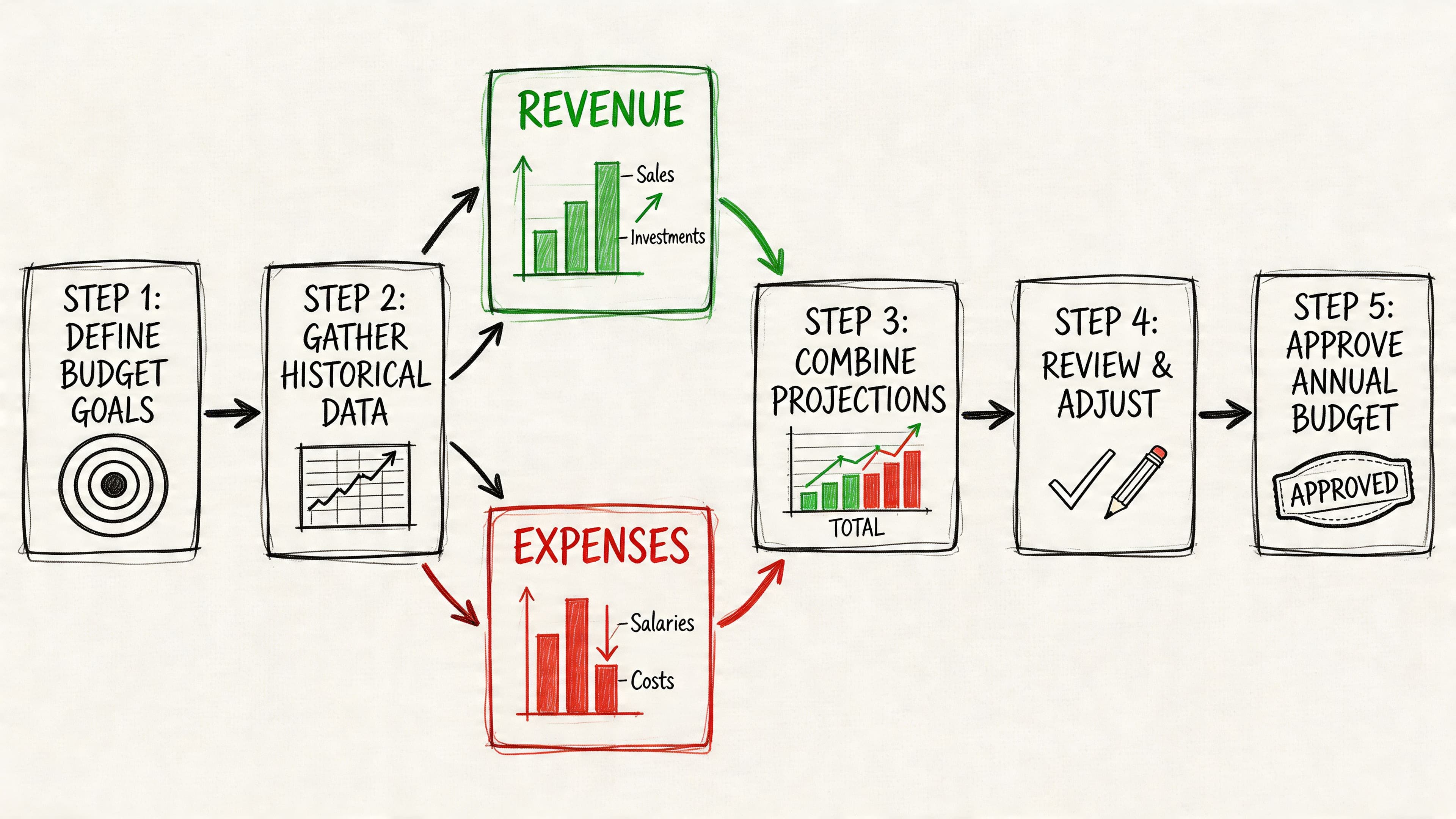

How to Build Your Annual Operating Budget Step-by-Step

A strong nonprofit budget starts with operating reality, not optimism. If you build it from aspirational fundraising and vague overhead assumptions, you’re not budgeting. You’re writing fiction.

According to Aplos’s nonprofit budget guide, nonprofits must categorize expenses by function, and a widely accepted benchmark directs at least 65% of total resources to program costs while overhead should not exceed 35%. That benchmark matters because your budget isn’t credible unless your expense allocation is credible.

Start with revenue you can defend

List revenue by source, not by hope. Break it into major buckets such as grants, individual donations, corporate support, program fees, and other earned income. Then divide each source into two tests:

- Committed or highly visible

- Expected but not yet locked

For-profit leaders often want one top-line target. Don’t do that here. In nonprofits, source quality matters as much as source quantity. A signed grant award is different from an event forecast. A recurring donor base is different from a new campaign assumption.

Use this rule. If you can’t explain why a revenue line belongs in the budget, move it to a stretch scenario.

Build the expense side by function, not just vendor

You still need natural expense categories like payroll, rent, software, contractors, insurance, and supplies. But your final operating budget has to answer a different question: how much supports programs, how much supports management and general, and how much supports fundraising?

That means every significant cost needs a functional home.

A better chart of accounts makes this much easier. If your existing structure is messy, start with a nonprofit chart of accounts template and map your accounts before you lock the budget.

Worked example using a $1 million nonprofit

Take a hypothetical nonprofit with $1,000,000 in annual expenses. We’ll build a clean functional allocation using only expenses, because that’s often a point of confusion for organizations.

Assume these natural expense totals for the year:

| Natural expense | Annual amount |

|---|---|

| Salaries and wages | $600,000 |

| Rent and facilities | $120,000 |

| Software and technology | $60,000 |

| Program supplies | $140,000 |

| Fundraising event and campaign costs | $50,000 |

| Insurance, audit, and admin support | $30,000 |

| Total | $1,000,000 |

Now allocate by function.

Direct costs first

Some expenses are obvious:

- Program supplies: $140,000 goes to Program Services

- Fundraising event and campaign costs: $50,000 goes to Fundraising

For salaries, assume staff time is tracked and splits this way:

- Program staff time: $420,000

- Management and general staff time: $120,000

- Fundraising staff time: $60,000

That fully allocates the $600,000 payroll line.

Indirect costs next

Now allocate shared costs using a rational driver. You don’t need a perfect academic model. You need one that is consistent and defendable.

Let’s allocate rent and software based on staff usage. If staff time is split 70% program, 20% management and general, and 10% fundraising, use that same ratio for shared office and technology costs.

For rent at $120,000:

- Program Services = $84,000

- Management and General = $24,000

- Fundraising = $12,000

For software at $60,000:

- Program Services = $42,000

- Management and General = $12,000

- Fundraising = $6,000

Now assign insurance, audit, and admin support. A reasonable assumption is to place this fully in management and general if it primarily supports governance, compliance, and organization-wide administration:

- Management and General = $30,000

Final functional view

| Function | Amount |

|---|---|

| Program Services | $140,000 + $420,000 + $84,000 + $42,000 = $686,000 |

| Management and General | $120,000 + $24,000 + $12,000 + $30,000 = $186,000 |

| Fundraising | $60,000 + $12,000 + $6,000 + $50,000 = $128,000 |

| Total | $1,000,000 |

Now calculate the program expense ratio:

$686,000 ÷ $1,000,000 = 68.6%

That clears the widely accepted 65% benchmark from Aplos. It does not reach the more demanding 70% standard some evaluators use, which becomes important later when you report externally.

Practical rule: If you can’t explain the logic behind an indirect cost allocation in one sentence, your board won’t trust it and an auditor won’t love it.

Don’t budget to break even by default

Many nonprofit leaders still treat zero surplus as a virtue. It isn’t. It’s a fragility signal.

A nonprofit should budget to build capacity when it has the chance. If revenue supports a modest surplus, use it to strengthen reserves, absorb timing shocks, and avoid reactive cuts. The mission does not benefit when leadership underprices administrative needs and then scrambles midyear.

Approval should be tied to operating assumptions

Before a board approves the budget, insist on these questions:

- Revenue quality: Which lines are committed, and which are forecasted?

- Functional allocation: How were shared costs assigned?

- Cash timing: When do large inflows and outflows hit?

- Flex points: What gets cut or delayed if revenue misses?

- Surplus policy: If revenue comes in strong, where does the excess go?

That’s how you build budgets for nonprofit organizations that function as management tools instead of ceremonial board documents.

Mastering Grant Budgeting and Fund Accounting

Grant budgeting is where for-profit instincts get expensive. If you treat a grant like ordinary revenue, you’ll produce sloppy reporting and invite clawback risk.

Restricted grant money is not your operating cash with extra paperwork. It’s more like customer funds designated for a contractually defined implementation. The funder expects you to use those dollars for the agreed purpose, classify them properly, and report the result cleanly.

If you want a practical primer on the mechanics, this overview of non profit fund accounting is useful because it frames the discipline in operational terms instead of accounting theory.

Direct costs and indirect costs are not optional distinctions

Every grant budget needs a clear line between costs that directly serve the funded program and costs that support the organization more broadly.

Direct costs usually include items like program labor, specific supplies, or program-specific contractors. Indirect costs are shared support costs such as office infrastructure, finance support, and common systems. The mistake isn’t just misclassifying them. The bigger mistake is failing to budget for them at all.

For-profit leaders often focus on contribution margin. The nonprofit equivalent is full-cost visibility. If a program “works” only because core administration subsidizes it, your grant budget is understating the cost of delivery.

Segregation is the control, not the afterthought

A restricted grant should be tracked in a way that lets you answer three questions fast:

| Question | What you need to show |

|---|---|

| What came in? | Grant award, receipts, and funding period |

| What was spent? | Categorized expenses tied to approved uses |

| What remains? | Unspent balance and any timing or restriction limits |

That’s why fund accounting matters. It creates separate accountability by fund, purpose, or program instead of treating the organization like one pooled economic unit.

A practical setup often uses accounting software to tag transactions by fund and program. In QuickBooks Online, that usually means classes, locations, or a carefully designed account structure. In NetSuite, you have more segmentation options, but the principle is the same. Every restricted dollar should be traceable from receipt to spend.

For a deeper explanation of system design, this guide on fund accounting for nonprofits is worth reading before you try to retrofit your books after year-end.

Build reports the funder actually wants

Grant reporting fails when finance teams rely on general ledger cleanup after the fact. Don’t do that. Build the reporting format before money lands.

Your grant budget should align with:

- Approved expense categories

- Reporting periods

- Program ownership

- Required documentation

- Treatment of shared costs

That turns reporting into a routine export and review process instead of a quarter-end scramble.

A short explainer helps if your team is new to this operational model:

If your grant report requires detective work, your accounting setup is the real problem.

Common compliance mistakes

These errors show up constantly in budgets for nonprofit organizations:

- Commingled cash thinking: Finance sees cash in the bank and assumes it’s spendable for general operations.

- Loose staff allocations: Salaries get charged to a grant without a disciplined basis.

- Retroactive coding: Expenses are dumped into a grant months later to “make the report work.”

- Ignored indirect support: Leadership funds the program but forgets what finance, HR, rent, and systems cost.

The fix is simple in concept and demanding in execution. Build fund-level visibility from day one. If your team can’t produce a fund-specific budget-to-actual report quickly, your grant budgeting process is still immature.

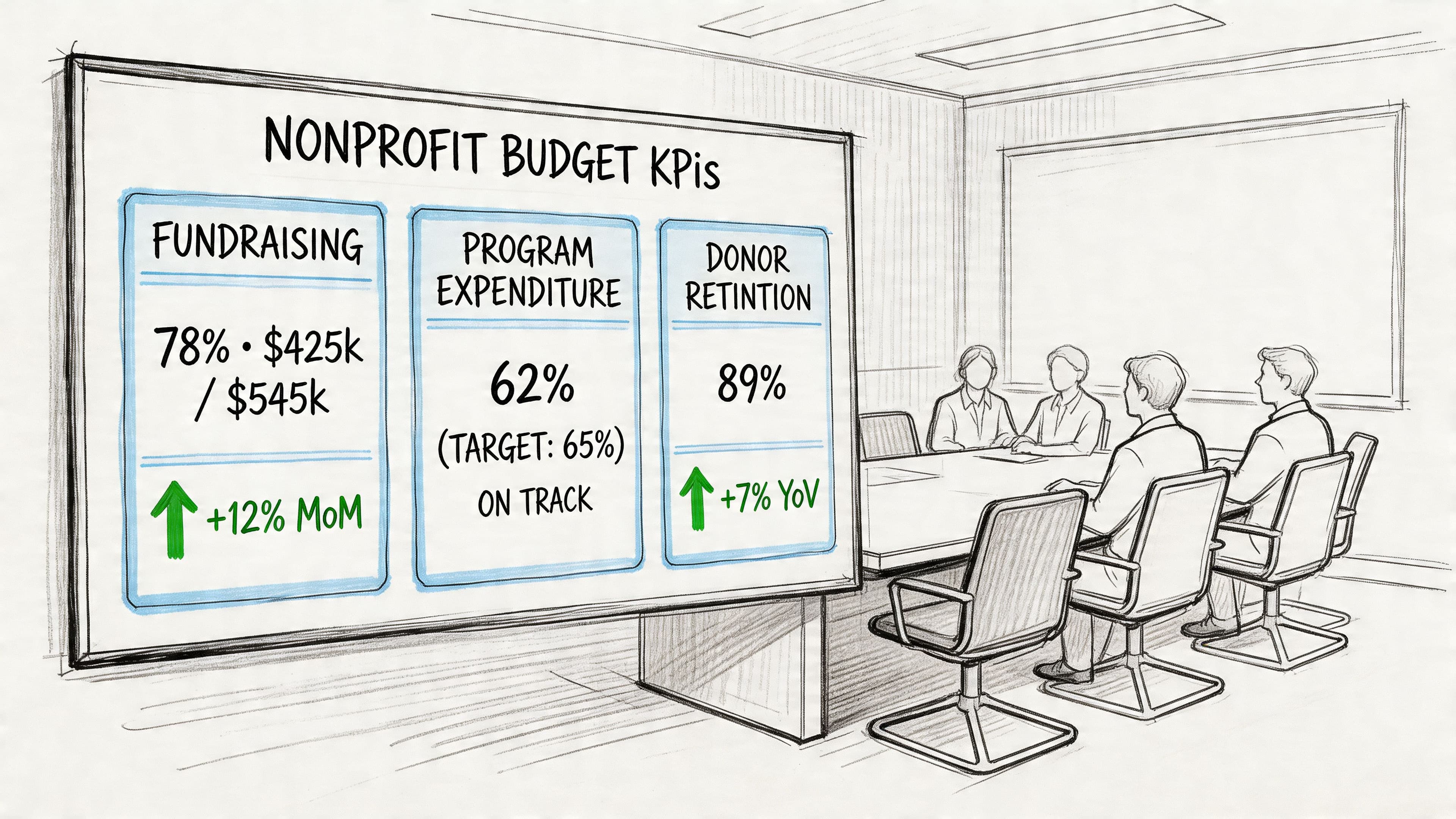

Reporting KPIs to Your Board and Donors

Board reporting should help people govern. Donor reporting should help people trust you. Most nonprofit financial packets fail both tests because they’re bloated, backward-looking, and light on decision-useful metrics.

The most useful board package is not the longest one. It’s the one that ties budget, actuals, and operational implications together on one page first, then supports the story with detail.

Start with budget versus actual

Your first report should be a clean budget-to-actual by month and year-to-date. Not just totals. Variances with explanation.

A strong version answers four things:

- Where are we ahead of budget?

- Where are we behind?

- Is the issue timing or performance?

- What action are we taking?

If you need a reference point for how to frame that report, this article on actuals vs budget lays out the discipline well.

The KPI that outsiders notice first

Among external efficiency metrics, the most visible one is the program expense ratio. According to Syracuse University’s summary of nonprofit spending benchmarks, Charity Navigator generally gives full credit to organizations with a program expense ratio of 70% or more, while the BBB Wise Giving Alliance recommends 65% or higher.

That means your board should see this ratio regularly, not once a year after the books are closed.

Use the formula already established earlier:

Program Services Expenses ÷ Total Expenses = Program Expense Ratio

If your ratio drifts down, don’t hide it. Explain why. Maybe you invested in finance infrastructure. Maybe fundraising ramped for a campaign. Maybe program timing changed. Context matters.

A board dashboard should be brutally simple

Here’s a practical one-page dashboard structure:

| Dashboard line | What to show | Why it matters |

|---|---|---|

| Budget vs actual revenue | Year-to-date budget, actual, variance | Shows if funding assumptions are holding |

| Budget vs actual expenses | Same view by function | Exposes overspend and underdeployment |

| Program expense ratio | Current period and year-to-date | Supports stewardship narrative |

| Cash position | Current cash and near-term pressure points | Prevents surprises |

| Restricted fund status | Major restricted balances and usage | Highlights what cash is actually available |

| Key narrative notes | Short management commentary | Gives the board a decision frame |

Don’t overload with vanity metrics

For-profit boards often get crowded dashboards full of ratios no one uses. Nonprofit boards can fall into the same trap.

Use only metrics that support governance. If a board member can’t act on it, it belongs in an appendix. Donors also don’t need ten pages of accounting detail. They need confidence that you manage resources responsibly and understand the economics of your mission.

Board standard: Every variance should come with an explanation and an action, not just a number.

Address the common objection

Some leaders resist KPI reporting because they think it pushes the organization toward optics over mission. That’s lazy thinking.

Good reporting doesn’t replace mission judgment. It supports it. If your board can’t see how the budget is performing, they can’t protect the mission when revenue shifts, costs rise, or restricted funds trap liquidity.

The right reporting package makes budgets for nonprofit organizations useful after approval. That’s the point.

Four Budgeting Pitfalls That Put Nonprofits at Risk

Most nonprofit budgeting mistakes aren’t exotic. They’re repeated, predictable, and expensive.

Red flags to fix immediately

Here are the four that matter most.

-

Budgeting for zero cushion: Leaders often assume a break-even plan is the responsible choice. It isn’t. A budget with no room for volatility leaves the organization exposed when a grant runs late, a campaign underperforms, or program costs rise faster than expected.

-

Treating overhead like failure: Administrative and fundraising costs are easy political targets. That doesn’t make them optional. If you starve finance, compliance, reporting, and development, you weaken the machine that funds and governs the mission.

-

Commingling restricted and unrestricted thinking: Even if your accounting records eventually separate these categories, leaders often make operating decisions from the bank balance alone. That’s a control failure. Restricted cash can sit in the account and still be unavailable for general operations.

-

Letting year-end funds drift without a plan: According to The Chronicle of Philanthropy’s sponsored guidance on unspent budgets, a key strategy for the 97% of U.S. nonprofits with budgets under $5 million is to manage unspent funds actively, including reallocating resources to pre-purchase supplies for future programs instead of letting budgets lapse. That’s smart financial management, not gamesmanship.

What good operators do instead

The strongest nonprofit leaders run year-end like disciplined operators, not passive administrators.

They ask:

- Can we pre-buy mission-critical supplies?

- Can we shift resources into the next delivery cycle without violating restrictions?

- Should we preserve the surplus to strengthen reserves?

- Which programs earned more investment, and which should be sunset?

That’s a better use of management attention than obsessing over cosmetic overhead optics.

The misconception that keeps causing damage

A lot of teams still believe “nonprofit” means every year should end flat and every admin line should be minimized. That mindset is one reason organizations stay fragile.

Underfunded operations don’t make a nonprofit more virtuous. They make it less resilient.

The mission needs competent finance, clear reporting, and enough unrestricted capacity to absorb surprises. Ignore that and the organization spends all year reacting instead of executing.

From Budgeting to Bankable Results Your Next Steps

If you’re serious about improving budgets for nonprofit organizations, stop treating budgeting as an annual board ritual. Treat it like operating infrastructure.

Your implementation checklist

Use this list and assign owners this week.

- Review your chart of accounts: Make sure it supports program, management and general, fundraising, and fund-level reporting.

- Separate restricted from unrestricted tracking: Your accounting system should show purpose-bound funds clearly.

- Create five budget views: Operating, program, grant, capital, and cash flow.

- Define allocation rules: Document how you assign payroll, rent, software, and other shared costs.

- Build a monthly budget-to-actual review: Require explanations and actions, not just variances.

- Set a year-end unspent funds policy: Decide in advance how leadership evaluates pre-purchases, reallocations, and reserves.

- Upgrade your forecasting discipline: A practical cash flow forecasting guide helps leadership translate budget assumptions into actual liquidity planning.

Tools matter, but design matters more

QuickBooks and NetSuite can both support nonprofit reporting if they’re configured properly. Gusto can support payroll workflows. Spreadsheets still help with scenario planning. None of those tools will save you if your budget logic is weak, your fund structure is unclear, or your reports are built after the fact.

The author brief asked for an expert quote, but the provided source explicitly says the sample quote is a placeholder and should be replaced with a real one. Since no verified quote is available, the honest guidance is simple: don’t publish fake authority. Publish sound finance.

Your next move is operational. Clean up the accounting structure, build the right budget layers, and make monthly reporting decision-ready.

If your team wants help turning nonprofit budgeting into a real operating system, talk to Jumpstart Partners. Their US-based, CPA-certified team helps organizations build cleaner reporting, stronger cash flow visibility, and reliable month-end processes without hiring a full in-house finance department.