Financial Operations

The Cash Flow Statement Template in Excel Your SaaS or Agency Can’t Live Without

Download our free cash flow statement template in Excel to forecast your runway, manage cash flow, and make smarter financial decisions.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readProfit doesn't pay the bills—cash does. As a founder, CEO, or finance leader, you're judged on growth, but you survive on liquidity. This guide, complete with a powerful cash flow statement template in Excel, will move you from reactive panic to proactive control, giving you a true picture of your company's financial health so you can make confident decisions about its future.

Why Your P&L Is Lying About Your Cash Position

As a leader at a growing SaaS or services firm, you live and die by your numbers. But are you watching the right ones? Most fixate on the Profit and Loss (P&L) statement. It shows revenue, expenses, and that holy grail: net income. The problem? Your P&L can paint a beautiful picture of profitability while your bank account is dangerously close to zero.

This disconnect is a leading cause of failure for otherwise successful businesses. A P&L built on accrual accounting records revenue when it’s earned, not when the cash actually hits your bank account. For SaaS and professional services firms, this creates a massive and dangerous blind spot.

"A profitable company can absolutely go bankrupt. It happens all the time when a business can’t pay its bills, even if the income statement shows a healthy profit. Managing cash flow isn't just a good habit; it's a crucial survival skill for any business owner." — David Worrell, Fractional CFO, Fuse Financial Partners

The Accrual Accounting Trap

Let's say your digital agency signs a $120,000 annual contract in January, which you bill quarterly. Your P&L proudly displays $10,000 in revenue each month. But in reality, you only receive a $30,000 cash payment every three months. This timing gap is where you get into trouble. You still have to make payroll, pay rent, and cover software subscriptions every single month, regardless of when your clients pay you. For a deeper look, see our guide on what is accrual accounting.

From Paper Profit to Real-World Cash

The cash flow statement closes this gap. It cuts through the noise of non-cash items like depreciation and focuses exclusively on the money moving in and out of your business. It's designed to answer three critical questions:

- Cash from Operations: Is your core business—the engine of your company—actually generating or consuming cash?

- Cash from Investing: How much are you spending on long-term assets like equipment, property, or acquisitions?

- Cash from Financing: Are you taking on debt, repaying loans, or bringing in capital from investors?

By understanding these three levers, you shift from just looking at profitability to truly managing your company’s financial health. It’s the only way to accurately measure your cash runway and avoid the dreaded surprise of an empty bank account.

Customizing Your Cash Flow Statement for Maximum Insight

A generic template is a starting point. To get real value, you must shape our Excel cash flow template to the unique rhythm of your SaaS or agency business. We’re moving beyond simple data entry to build a true command center for your company’s cash.

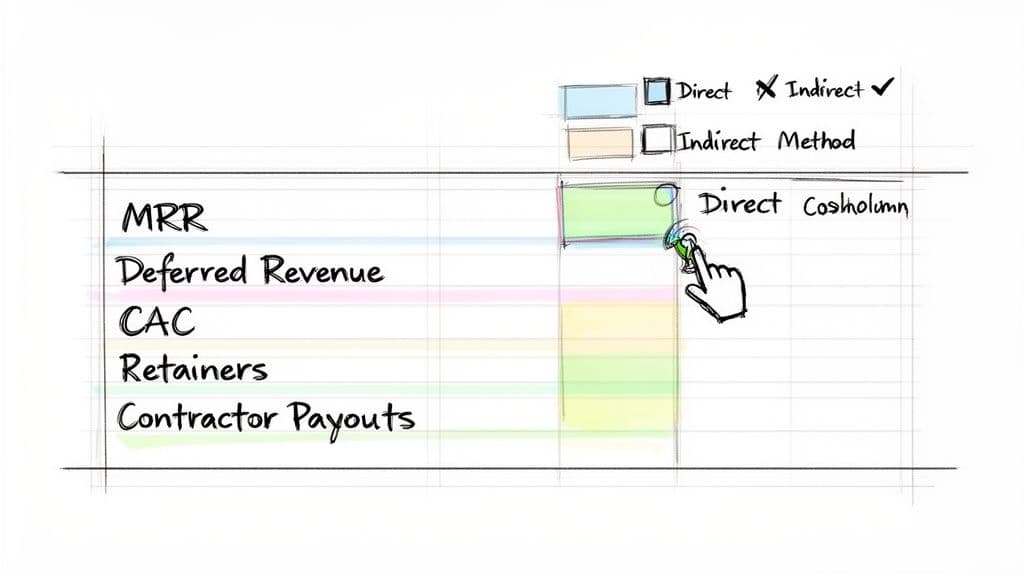

The first decision you'll make is choosing between the direct and indirect methods for tracking your cash from operations. Your accountant will push for the indirect method for GAAP compliance, but for founders and CEOs, the direct method offers far better visibility. It tracks the actual dollars moving in and out, giving you an intuitive, real-time feel for your business's pulse.

The Direct vs. Indirect Method: A Founder's View

This isn't just an accounting detail; it fundamentally changes how you see your business. The indirect method starts with net income and works backward with non-cash adjustments, which is confusing and abstract for anyone who isn't a CPA. The direct method is concrete. It’s reality. It answers the simple, vital questions: How much cash did we actually collect from customers this month? How much did we pay our team and our vendors?

| Feature | Direct Method | Indirect Method |

|---|---|---|

| Starting Point | Actual cash receipts (e.g., cash collected from customers) | Net Income from P&L |

| Clarity for Founders | High. Easy to see exactly where cash came from and went. | Low. Abstract adjustments are hard to link to real activity. |

| Primary Use | Operational management and internal decision-making. | External financial reporting and GAAP compliance. |

| Key Insight | Reveals the direct cash-generating power of your core business. | Shows reconciliation between net income and cash flow. |

When you choose the direct method in your template, you’re building a tool for management, not just for compliance.

Make the Template Your Own

A powerful cash flow statement mirrors the unique drivers of your business. Our template is designed for you to add the specific line items that matter to your SaaS company or digital agency.

For a SaaS company, get more granular than just "revenue." You need to add rows for:

- Cash from New MRR: The actual cash you collected from brand-new subscriptions.

- Cash from Renewal MRR: Cash from existing customers who renewed their plans.

- Customer Acquisition Costs (CAC): The real cash you burned on sales and marketing.

- Deferred Revenue Changes: Critical for tracking cash received for annual contracts that hasn't been recognized as revenue yet.

A digital agency or professional services firm has different levers and should track items like:

- Cash from Project Retainers: Upfront payments received at the start of an engagement.

- Milestone Payments Received: Cash collected when you hit specific deliverables.

- Contractor and Freelancer Payouts: A major cash outflow that must be tracked separately from employee payroll.

- Client Reimbursable Expenses: Cash you spent on behalf of clients that you’ll invoice for later.

By adding these custom line items, your cash flow statement transforms from a static report into a diagnostic tool. You can immediately see the impact of a new marketing campaign on your CAC cash burn or how a shift to annual contracts boosts your upfront cash position.

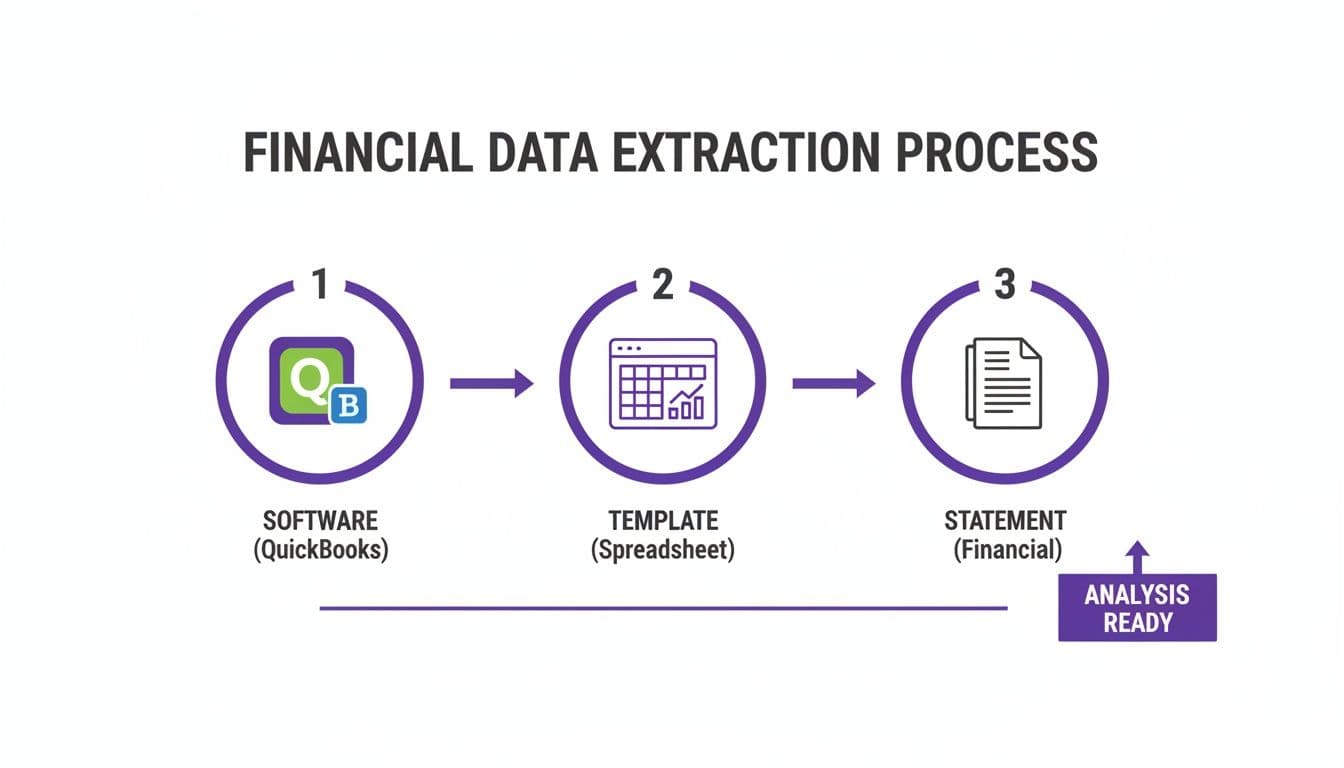

Pulling and Mapping Data from Your Financial Stack

An empty template is just a spreadsheet. Its real power comes from feeding it accurate data, and this is where most founders get tripped up. You have data in QuickBooks, transactions in Stripe, and statements from your bank, but making them all play nicely in your cash flow statement template in excel is a chore.

The challenge is translating your accrual-based accounting software into the cash-based reality you need to manage your bank balance. Your QuickBooks P&L shows revenue when it's earned, but your cash flow statement only cares about the actual cash collected. They're two different languages.

A Worked Example for a $2M ARR SaaS Company

Let's walk through how a SaaS company with $2M in ARR would populate its cash flow from operations for a single month.

Imagine these are the numbers for January:

- Monthly Recurring Revenue (MRR): $166,667

- New Sales Closed (Annual Contracts): $25,000 billed upfront

- Accounts Receivable (Start of Month): $50,000

- Accounts Receivable (End of Month): $40,000

- Salaries Paid: $75,000

- Marketing Spend Paid: $20,000

- New Server Purchased (paid with cash): $5,000

Here's how you map this data into the cash flow from operations section using a direct method approach:

| Line Item | Calculation | Cash Impact |

|---|---|---|

| Cash Collected from Customers | $166,667 (MRR) + $25,000 (New) + ($50k - $40k A/R Change) | +$171,667 |

| Cash Paid for Salaries | Direct from bank/payroll provider | -$75,000 |

| Cash Paid for Marketing | Direct from bank/credit card statement | -$20,000 |

| Net Cash from Operations | $171,667 - $75,000 - $20,000 | +$76,667 |

Notice the server purchase isn't on this list. As a long-term asset, it's a capital expenditure that belongs in the Cash Flow from Investing section. This period, it has a -$5,000 impact there. This is a critical distinction that many founders miss. Learning to automate parts of this data mapping can save you dozens of hours a month. You can dive deeper into this in our guide to financial reporting automation.

Common Misconception: "Stripe Payouts are Cash from Customers"

This is a classic error. A lump-sum payout from Stripe is not your cash from customers. That payout is a bundled deposit from dozens of individual customer payments, minus Stripe's processing fees. You must reconcile it against the specific invoices in QuickBooks to get a true picture of cash from customers and accurately book your payment processing fees.

Red Flags When Mapping Your Data

As you pull numbers, watch for these common warning signs. Ignoring them leads to a flawed forecast and disastrous decisions.

- Growing A/R Balance: If your accounts receivable is consistently growing faster than your revenue, you're getting worse at collecting cash. This is a major drag on your liquidity. According to OpenView's 2024 benchmarks, SaaS companies should aim for a Days Sales Outstanding (DSO) of less than 45 days. If yours is climbing, it's a problem.

- Stripe/Bank Balance Mismatch: Is your Stripe balance ballooning but your actual bank account isn't? You have payout issues or you're not transferring funds regularly. Don't count money in your payment processor as operational cash until it's in a bank account you can spend from.

- Negative Cash Flow from Operations: If your P&L shows a profit but your operations are consistently burning cash, you have a working capital problem. This is an urgent signal to investigate your billing cycles, collection efforts, and expense management.

Once you have clean data in Excel, you might need it for banking. For instance, you can create SEPA transfers and direct debits directly from your Excel files, turning your financial model into an actionable payment tool.

Build Your 13-Week Cash Flow Forecast to See the Future

Getting your historical data clean is half the battle. The real power comes from using that foundation to look forward. For short-term financial planning, the 13-week cash flow forecast is the single most important tool in your arsenal. It gives you a full quarter of visibility into your future cash position.

This isn’t a high-level annual budget. It's a granular, week-by-week roadmap of every dollar coming in and going out. It lets you spot cash crunches months in advance, make smarter spending decisions, and run your business from a position of control.

A Realistic Calculation for SaaS Cash Inflows

Let’s get specific. Imagine your SaaS business has $100,000 in MRR, a 2% monthly gross churn rate, and your sales team is on track to add $10,000 in new MRR this month.

A naive forecast might project next month's cash as $108,000. That's dangerously optimistic.

Here’s how a controller actually calculates it:

- Starting MRR: $100,000

- Projected Churn: $100,000 * 2% = -$2,000

- New MRR Added: +$10,000

- Ending MRR: $108,000

- Failed Payment Adjustment: Assume a 5% delinquency rate on first payments for new deals. Your immediate cash from new MRR is closer to $10,000 * (1 - 5%) = $9,500.

- Factored-in Inflow: Your realistic projected cash inflow from subscriptions is closer to $98,000 + $9,500 = $107,500, and that’s before accounting for payment processing delays.

This is the level of detail that makes a forecast useful. For a deeper look, check our complete guide to building a bulletproof 13-week cash flow forecast.

Projecting Your Cash Outflows

Forecasting outflows is more straightforward. Go line-by-line through your P&L and bank statements to map out all expected cash payments for the next 13 weeks.

Break them down into clear categories:

- Payroll & Benefits: Your largest, least flexible expense. Know the exact date and dollar amount of every payroll run.

- Rent & Utilities: Fixed costs that are easy to plug in.

- Software Subscriptions: Your monthly SaaS stack—Salesforce, Slack, HubSpot.

- Marketing & Ad Spend: Base your projection on your planned budget, but know it’s the first lever to pull if cash gets tight.

- Contractor Payments: For agencies, this is a major variable outflow tied to project work.

- Debt & Loan Repayments: These principal and interest payments are non-negotiable. Don't forget them.

Once you’ve populated both your projected inflows and outflows for the next 13 weeks, the Excel template calculates your weekly ending cash balance. This is your financial crystal ball.

Warning Signs in Your 13-Week Forecast

Your forecast is your business’s early-warning system. Here are the red flags to watch for and what to do about them.

| Warning Sign | What It Really Means | Your Immediate Action Plan |

|---|---|---|

| Negative Ending Cash in Any Week | An impending cash crisis. You are on track to run out of money. | Accelerate receivables, delay payables, or draw on your line of credit—immediately. |

| Steadily Declining Cash Balance | A consistent burn rate that isn't sustainable, even if your P&L shows a profit. | Scrutinize all discretionary spending. Pause that new hire or cut a marketing channel. |

| Cash Inflows are Heavily Back-Loaded | Most of your cash is due late in the quarter, creating a dangerous mid-quarter cash gap. | Offer early payment discounts to customers or secure short-term financing to bridge the gap. |

This forward-looking view is what empowers you to act decisively. Instead of being blindsided by a low bank balance, you have weeks—or even months—to correct course.

Avoid These Common Errors and Validate Your Statement

A cash flow statement you can't trust is worse than useless—it’s dangerous. Even the slickest Excel template is garbage if the numbers are wrong, leading you to make disastrous decisions based on a false sense of security.

The classic, most common mistake? Confusing profit with cash. Your P&L can shout "$50,000 profit!" while your bank account is quietly bleeding out. Profit isn't cash in the bank.

Your Final Sanity-Check Checklist

Before you share this statement with your board or leadership team, run it through this final sanity check.

- The Golden Rule: Reconcile to the Balance Sheet. This is non-negotiable. The Ending Cash Balance on your cash flow statement must match the cash and cash equivalents line on your balance sheet for the exact same period. If it's off by even a dollar, you have an error. Find it.

- Check Your Non-Cash Adjustments. Using the indirect method? Go back and confirm you've added back all non-cash items. This includes depreciation, amortization, and any stock-based compensation.

- Investigate Large or Unusual Items. See a huge number in your investing or financing sections? Hunt it down. Trace that figure back to a bank statement or loan agreement to confirm its amount and category.

If your ending cash balance doesn't match the balance sheet, the culprit is almost always a miscategorized transaction or a forgotten non-cash adjustment. For a deeper dive, learn how to reconcile bank accounts — it’s an essential skill for financial accuracy.

Red Flags in Your Validated Cash Flow Statement

Once your statement is validated, certain patterns are glaring warning signs that scream for your attention.

| Red Flag | What It Means | Actionable Next Step |

|---|---|---|

| Negative Cash Flow from Operations | Your core business is burning more cash than it generates, even if you are profitable on paper. This points to a severe working capital problem. | Immediately review your accounts receivable aging, billing cycles, and operational expenses. You're bleeding cash somewhere in your core model. |

| Growing A/R Faster Than Revenue | You're getting slower at collecting cash from customers. This ties up vital liquidity and starves the business of cash needed for payroll and growth. | Implement a stricter collections process. Offer early payment discounts or revise payment terms with new clients. Stop letting clients use you as a bank. |

| Reliance on Financing for Operations | You are consistently using debt or equity (financing activities) to cover your day-to-day operational shortfalls. This is not a sustainable long-term strategy. | Re-evaluate your business model's profitability and cost structure. Your core operations must fund themselves; financing is for growth, not survival. |

These aren't just accounting issues; they're strategic threats. According to the 2024 OpenView SaaS Benchmarks, best-in-class companies maintain positive operational cash flow to fund growth internally. If you're consistently in the red here, it’s a clear sign your growth engine is broken.

Know When to Outsource Your Financial Back Office

That cash flow statement template in excel that felt like a superpower in the early days? It starts to break as you scale. Once your business crosses the $2M revenue mark, financial complexity multiplies, and DIY financial management stops being scrappy and starts being a serious risk.

If you’re spending more than 10 hours a month on bookkeeping, or your month-end close drags past the first week of the next month, those are clear signals you've outgrown your current process. Your time is far more valuable driving growth, not buried in spreadsheets.

The Right Help at the Right Time

Bringing in professional help isn't about giving up control—it's about getting the right expertise to make smarter decisions. But hiring the wrong role at the wrong time is a costly mistake. You need to match the financial hire to your company's stage.

- Bookkeeper: Handles daily data entry, reconciliations, and basic transactions. Hire a bookkeeper when you're tired of the daily accounting grind but don't need complex reporting.

- Controller: Manages the entire accounting function. They oversee the bookkeeper, design financial controls, own the month-end close, and produce accurate, timely financial statements for board meetings.

- Fractional CFO: A high-level strategic partner who uses your controller's reports to guide fundraising, M&A, and long-term capital planning. They focus on "what's next," not "what just happened."

"So many founders jump from a bookkeeper directly to a fractional CFO, creating a massive gap in the middle. A controller is the critical link who ensures the strategic advice from a CFO is built on a rock-solid foundation of accurate data—not guesswork." — Scott Hoover, Founder of Jumpstart Partners

An outsourced finance team gives you access to all these roles, letting you tap into the right level of expertise exactly when you need it without the full-time cost. A strong partner delivers a 5-day month-end close, investor-ready financials, and the deep cash visibility required to scale confidently. When you're ready to explore that option, our guide on choosing an in-house vs outsourced controller can walk you through the decision.

Frequently Asked Questions

When you're a founder, your financials can feel like a maze. Let's cut through the noise and answer the questions that come up time and time again when you're wrestling with your cash flow statement.

What Is the Difference Between the Direct and Indirect Methods?

Think of it this way: the direct method is your bank statement translated into business intelligence. It lists your actual cash inflows and outflows—cash collected from customers, cash paid to suppliers, cash paid for salaries. It shows you exactly where your money came from and where it went. For a founder trying to manage day-to-day operations, this is the superior method.

The indirect method is the one your accountant loves for GAAP compliance. It starts with your net income from the P&L and then makes a series of confusing adjustments for non-cash items like depreciation. While technically correct, it’s not intuitive for making real-world decisions.

How Often Should I Update My Cash Flow Forecast?

There are two parts to this. Your historical cash flow statement gets updated monthly as a standard part of your month-end close.

Your 13-week cash flow forecast is a different beast entirely. It’s your forward-looking radar for short-term liquidity. Best practice is to update it weekly. Every single week, you should roll it forward: drop the week that just passed, add a new week to the end, and refresh your projections with the latest sales data, A/R collections, and upcoming expense payments. This isn't bookkeeping; it's active cash management.

Why Is My Cash Decreasing If My P&L Shows a Profit?

This is the classic "profitable-on-paper, but broke-in-reality" scenario. If your P&L is green but your cash balance is dropping, it’s almost always one of these culprits:

- Slow-Paying Customers: Your revenue looks great on the P&L, but the cash is sitting in your Accounts Receivable, not your bank account.

- Large Capital Investments: Buying new equipment (Capital Expenditures) burns cash but only hits your P&L slowly through depreciation.

- Debt Repayment: Principal payments on a loan are a major cash outflow, but they don't show up as an expense on your P&L at all.

Your P&L shows theoretical profit. Your cash flow statement reveals your ability to make payroll next month. One is an opinion; the other is a fact.

Wrestling with your cash flow statement in Excel quickly becomes a bottleneck as your business grows. When you're ready to trade spreadsheet headaches for an expert-led finance function you can actually trust, Jumpstart Partners is here to help. We deliver a 5-day close, board-ready financials, and the clarity you need to scale with confidence.

Get a Clear Picture of Your Financial Health with Jumpstart Partners