Financial Operations

Controller in Business Guide for SaaS and Agencies

Master the controller in business role with core workflows, KPI dashboards, hire timing, compliance, integrations, and a turnkey onboarding checklist.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··24 min readYour books are closing late. Your investor update gets delayed because revenue isn't reconciled. Your agency margin looks fine until payroll hits and you realize project profitability was overstated. Your SaaS dashboard shows MRR, but you don't fully trust it because billing dates, service periods, and deferred revenue aren't lining up.

That's the point where a controller in business stops being an admin hire and becomes an operating necessity.

A controller gives you clean numbers, a disciplined close process, and financial reporting you can use to make decisions. Without that layer, you're running the company on partial information. If your CTO is also thinking about systems modernization, this guide for CTOs on finance transformation is a useful companion because finance process problems usually show up as both data problems and workflow problems. If you want a practical lens on whether controller support pays off, review this controller services ROI analysis.

Table of Contents

- Understanding Controller Role in Business

- Month-End Close Workflows and Responsibilities

- Key KPIs and Dashboards for Finance Leaders

- When to Hire or Outsource with Role Comparisons

- Security Compliance and Tech Integrations

- Actionable Hiring and Onboarding Checklist

- Conclusion and Next Steps

Understanding Controller Role in Business

Your revenue is climbing, cash is tight, and investors want clean monthly numbers. The founder asks a simple question: “Can we trust these reports?” If nobody clearly owns accounting quality, the answer is no. A controller fixes that.

A controller is the senior finance operator responsible for accurate financial statements, accounting discipline, and the controls that keep errors from reaching the board, lenders, or tax filings. Robert Half describes the role as the company's chief accountant and senior management leader overseeing daily accounting operations, financial statement accuracy, and compliance in its overview of the controller role and responsibilities. The same guidance notes that controllers are commonly expected to hold credentials such as CPA or CMA.

For founders, the practical value is straightforward. You get numbers you can act on, not numbers you need to second-guess.

What the role actually covers

The controller owns the accounting engine. NetSuite's financial controller role overview lays out the scope clearly: close management, reporting, internal controls, budgeting support, tax coordination, audit support, and oversight of the accounting team.

That scope matters because the controller sits in the gap where many scaling companies break. Bookkeeping records activity. CFO work sets strategy. The controller turns raw transactions into reliable reporting, documented processes, and review discipline.

A strong controller usually owns:

- Financial reporting: Monthly statements that are accurate, timely, and consistent with GAAP or your reporting standard.

- Accounting operations: Supervision of AP, AR, payroll inputs, expense controls, and balance sheet reconciliations.

- Internal controls: Approval rules, segregation of duties, policy enforcement, and documentation that stands up in diligence.

- Compliance support: Audit prep, tax coordination, and clean records for lenders, investors, and insurers.

- Management reporting: Clear variance analysis and reporting packages that help the CEO or CFO make decisions faster.

If you want a practical reference for how controller ownership connects to accounting discipline, use this month-end close process flowchart as the operating baseline.

Why the role pays for itself earlier than founders expect

Founders usually wait too long.

In SaaS and agencies, the first finance hire after bookkeeping is often a controller or outsourced controller, not a CFO. That is the right call in most cases because reporting accuracy and close discipline create the base layer for pricing, hiring, cash planning, and board reporting. A part-time CFO cannot compensate for weak accounting operations.

The ROI shows up in fewer missed invoices, cleaner revenue recognition, tighter expense review, and less rework during audits, tax filings, and due diligence. It also shows up in speed. When the controller catches cutoff errors, misclassified spend, or deferred revenue mistakes before reports go out, leadership avoids bad decisions based on bad data.

My recommendation is simple. If your SaaS company is crossing low seven figures in ARR, or your agency has enough volume that one person can no longer review billing, payroll, and reconciliations with care, install controller coverage. Start outsourced if transaction volume is still moderate. Hire in-house once complexity, team size, and reporting demands become constant.

Where founders get this wrong

The mistake is hiring for software familiarity instead of ownership.

A candidate who only “knows QuickBooks” is not enough. You need someone who can design controls, review work, enforce deadlines, and explain what changed in the numbers and why. If the person cannot spot revenue cutoff issues, accrual gaps, or broken approval paths, you still do not have a controller. You have a senior bookkeeper.

Reporting structure matters too. If you have a CFO, the controller should report there. If you do not, the controller often reports directly to the founder or CEO and acts as the top finance operator day to day.

Hire for judgment first. Technical accounting, process discipline, and team management come next. Tool knowledge matters, but it is nowhere near the top of the list.

Month-End Close Workflows and Responsibilities

A late close is not a scheduling issue. It's an operating problem. If your team can't close quickly, it usually means responsibilities are fuzzy, reconciliations are delayed, and review happens too late.

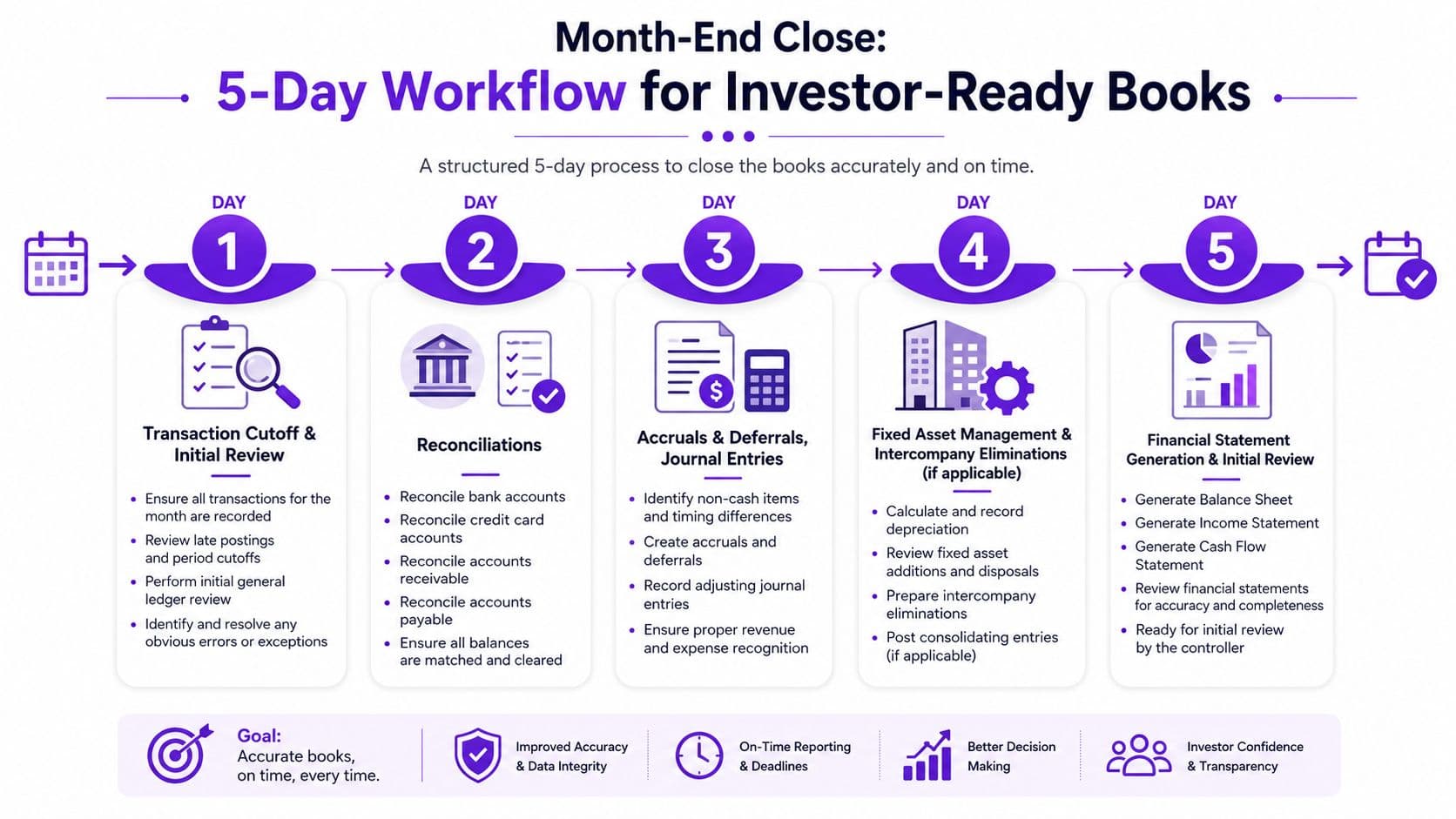

Glencoyne puts the bar where it belongs for a scaling SaaS company: a high-performance controller is expected to own the full-cycle close and drive a 5-day close timeline, with finalized financial statements available by the 10th to 15th of the following month in its guide to the SaaS financial controller role.

A documented close process matters more than almost any finance tool upgrade. If your team needs a reference model, this month-end close process flowchart is the standard to work from.

What the controller owns

The controller is the quarterback of the close. That doesn't mean they post every entry themselves. It means they assign work, enforce deadlines, review output, and make sure the financial statements are final, not provisional.

Core ownership includes:

- Cutoff discipline: Revenue, expenses, payroll, and vendor bills land in the right period.

- Reconciliation review: Bank, credit card, AR, AP, and clearing accounts are tied out.

- Adjusting entries: Accruals, deferrals, prepaid expenses, payroll entries, and depreciation get posted.

- Variance review: Material swings are explained before statements go out.

- Final package: Balance sheet, income statement, cash flow statement, and management notes are ready.

A practical five-day close cadence

Below is the cadence I recommend for founder-led businesses between early scale and mid-market maturity.

| Day | Primary focus | Controller responsibility | Team inputs |

|---|---|---|---|

| Day 1 | Transaction cutoff and ledger review | Lock the period, confirm data completeness, identify missing items | Operations, billing, payroll |

| Day 2 | Reconciliations | Review bank, credit card, AR, and AP reconciliations | Staff accountant, bookkeeper |

| Day 3 | Journal entries | Approve accruals, deferrals, payroll entries, and adjustments | Accounting team |

| Day 4 | Asset and entity review | Review depreciation, prepaid schedules, intercompany activity if relevant | Senior accountant |

| Day 5 | Statement prep and management review | Finalize statements, investigate variances, issue reporting pack | Founder, CFO, department leads |

Practical rule: If your close depends on one heroic person remembering everything, you don't have a close process. You have a monthly fire drill.

What breaks the close

The same problems show up over and over:

- Revenue cutoff is unclear: Common in SaaS, retainers, and milestone billing.

- Payroll entries are late: Agencies and service firms often lag here.

- Reconciliations happen after review: That reverses the proper order.

- Department heads don't submit data on time: Finance ends up waiting on everyone else.

- No close checklist exists: Work gets repeated, skipped, or finished out of sequence.

A controller fixes this by turning tribal knowledge into a repeatable workflow. They create checklists, owners, deadlines, and review standards. That's what allows the business to produce investor-ready books without drama.

Key KPIs and Dashboards for Finance Leaders

Finance dashboards fail when they mix vanity metrics with bad accounting. Your controller should own the accounting logic behind the dashboard, especially in SaaS where revenue timing matters.

Ridgeway Financial Services is direct on this point. In SaaS companies from $500K to $20M revenue, the controller is the primary expert for implementing ASC 606 revenue recognition workflows, and that work prevents misreported MRR and ARR metrics that can lead to audit failures in its controller role in SaaS companies analysis.

If you want a benchmark list of the metrics finance should own, use this SaaS financial metrics guide as your working checklist.

The KPI set that matters

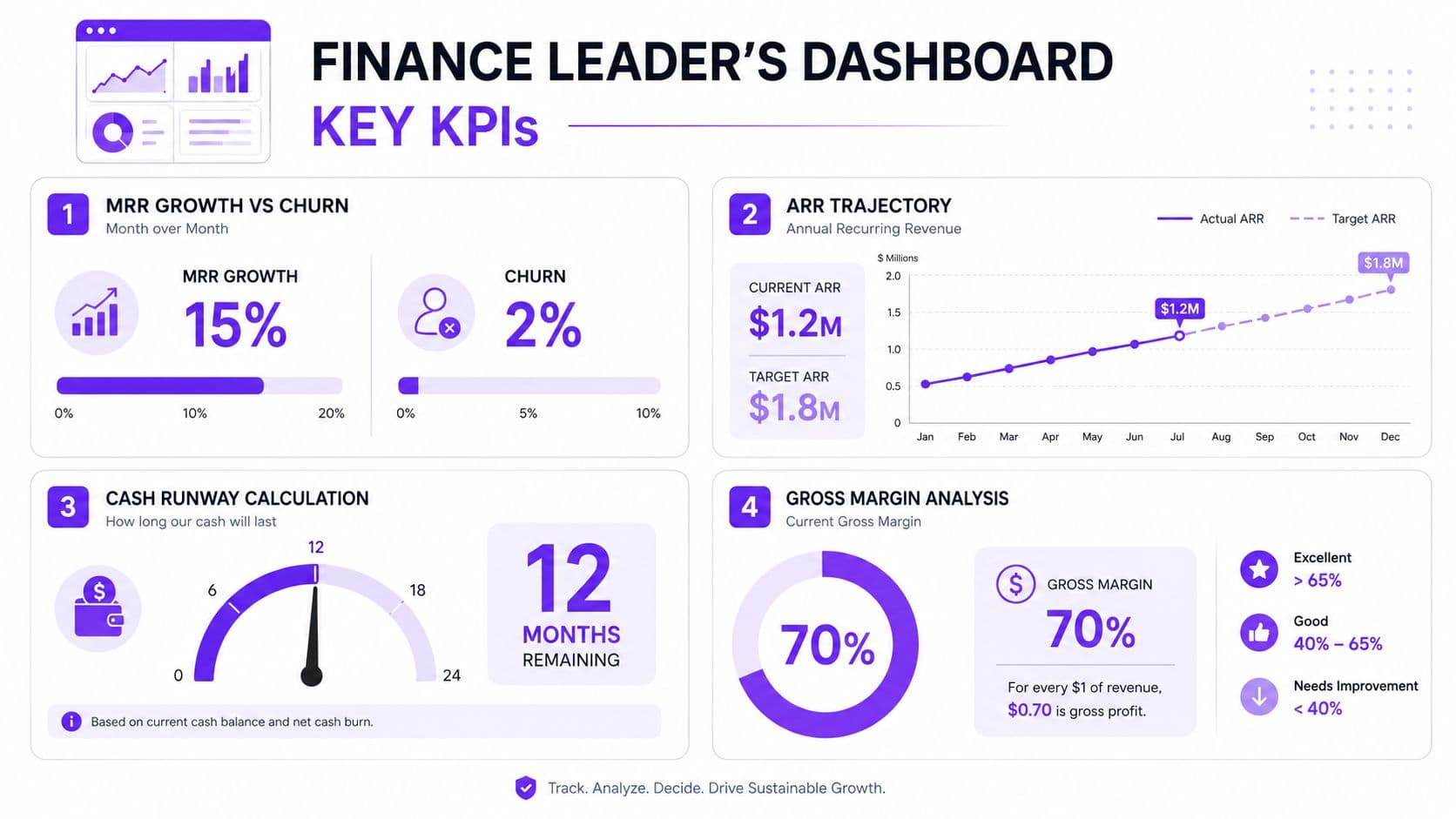

For the businesses I'm advising in this range, four dashboard areas matter most:

- MRR growth versus churn

- ARR trajectory

- Cash runway

- Gross margin

These numbers only help if the accounting underneath them is right. If deferred revenue is wrong, MRR can be overstated. If payroll allocation is sloppy, gross margin is fiction. If AP timing is messy, runway is misleading.

Here's a useful primer before you redesign your dashboard:

Worked examples with real numbers

The infographic above includes a sample dashboard with these figures: MRR Growth at 15%, Churn at 2%, ARR at $1.2 million with a target of $1.8 million, Cash Runway at 12 Months Remaining, and Gross Margin at 70%. I'll use those exact figures to show how a founder should read them.

| KPI | Example number | How to interpret it |

|---|---|---|

| MRR growth | 15% | Growth is healthy only if revenue recognition is consistent and churn isn't hidden |

| Churn | 2% | Low churn supports compounding growth, but only if contract timing is mapped correctly |

| ARR current | $1.2 million | This is your current recurring revenue run rate |

| ARR target | $1.8 million | Your planning gap is $600,000 |

| Cash runway | 12 months | You have one year before current cash is exhausted at the present burn rate |

| Gross margin | 70% | You retain $0.70 before operating expenses for each $1.00 of revenue |

Now the worked calculations.

- ARR gap calculation: $1.8 million target minus $1.2 million current ARR equals $600,000 of additional ARR required.

- Gross profit example: At a 70% gross margin, a business generating $1.2 million in ARR retains $840,000 in gross profit and incurs $360,000 in direct cost.

- Runway planning example: If your dashboard says 12 months remaining, your controller should tie that to current cash and monthly net burn and then reconcile it to actual cash movement, not spreadsheet assumptions.

If your MRR and ARR dashboard doesn't reconcile back to the general ledger and deferred revenue schedule, it's a marketing report, not a finance report.

What a controller should challenge

A strong controller doesn't just publish a dashboard. They pressure-test it.

They should ask:

- Is booked revenue being confused with recognized revenue?

- Are churn and expansion measured on the same contract logic every month?

- Do agency project margins include the actual delivery labor cost?

- Does cash runway reflect payables timing and payroll cadence?

For SaaS, ASC 606 holds particular importance. The controller maps billing cycles to service periods and keeps deferred revenue accurate, so the dashboard reflects earned revenue instead of invoiced cash. That's the difference between a finance team that informs decisions and one that produces attractive noise.

When to Hire or Outsource with Role Comparisons

You hit $1.2 million in ARR, sales are working, and cash still feels tighter than it should. Then month-end slips, deferred revenue is wrong, payroll entries need cleanup, and your board deck turns into a manual reconstruction project. That is the point where founders usually ask the wrong question. The question is not whether you can survive a little longer without controller capacity. The question is how much avoidable error, delay, and rework you are already paying for.

Use a simple rule. Hire controller capacity before finance mistakes start taxing growth. In SaaS and agencies, the cost of waiting shows up fast in revenue recognition errors, missed accruals, weak project margin reporting, payroll cleanup, and a close process that keeps stretching. Those problems do not stay in accounting. They distort pricing, hiring, runway decisions, and lender or investor confidence.

John Galt Finance lays out a practical benchmark in its fractional CFO decision framework. Under $750K in revenue, a bookkeeper plus outsourced controller support is usually enough. Around $1M and above, finance complexity starts justifying more formal oversight, especially once you have recurring revenue, multiple service lines, or growing headcount.

Cost gives you the second trigger. Rusty Hale has noted that a full-time controller starts to make sense when outsourced bookkeeping spend passes $8,000 per month, with full-time controller compensation in major U.S. tech markets often running from $150,000 to $220,000 or more, and fractional controller support often landing in the $5,000 to $15,000 monthly range. Treat those numbers as a management threshold. Once you are paying that much for outsourced accounting labor, you are buying volume. You should start buying ownership.

Crossing that threshold without controller oversight often leads to expensive errors in revenue recognition, payroll, and close quality. Those errors eat into the gains that created the growth in the first place.

A decision rule founders can actually use

Use this sequence:

- Under $750K revenue: Keep a strong bookkeeper. Add outsourced controller review for close, reconciliations, and reporting discipline.

- Around $1M revenue: Assess close speed, deferred revenue accuracy, payroll complexity, and management reporting quality. If any of these are breaking, add controller capacity now.

- When outsourced accounting spend exceeds $8,000 per month: Move to a dedicated controller model, fractional or full-time depending on workload.

- When lenders, investors, audits, or regular board reporting enter the picture: Put a controller in place before adding more strategic finance layers.

Founders also need to separate workload from title. A controller fixes reporting infrastructure. A CFO uses that infrastructure for capital allocation, fundraising, and planning. If you need help choosing between those roles, this CFO vs controller breakdown gives the right comparison.

If your company already uses outside specialists in adjacent functions, outsourced finance will feel familiar. The same logic that supports external infrastructure support can support external controllership until the workload justifies an internal hire. This overview of IT outsourcing services in Saskatchewan shows the same operating model. Buy expertise first. Bring it in-house when utilization is high enough.

Role comparison table

| Role | Cost Range | Core Responsibilities | Best Fit |

|---|---|---|---|

| Bookkeeper | Usually lowest-cost finance support | Transaction entry, AP support, bank feeds, basic monthly reports | Early-stage companies with simple operations and low transaction complexity |

| Outsourced Controller | Monthly retainer, often below full-time payroll cost | Owns close process, reviews reconciliations, improves controls, keeps reporting accurate | Companies that need discipline and oversight before they need a full internal finance manager |

| Full-Time Controller | Often justified once workload is constant and outsourced spend is already high | Leads accounting, manages close, supervises staff, prepares for audits, improves reporting reliability | Businesses with enough transaction volume, headcount, and reporting needs to support a dedicated owner |

| Fractional Controller | Typically lower than full-time salary, higher than bookkeeping-only support | Builds process, leads close, handles controller-level review without a full-time commitment | SaaS and agencies in the gap between basic bookkeeping and a permanent hire |

| CFO | Highest-cost finance leadership layer | Planning, fundraising support, scenario modeling, board reporting, capital strategy | Companies with stable reporting that now need strategic finance leadership |

Common founder objections

“My bookkeeper can handle it.”

Only if your needs are still basic. Bookkeeping handles transaction processing. Controllership handles close ownership, controls, reporting integrity, and accounting judgment. Those are different jobs.

“I'll wait until we're bigger.”

That usually means you will clean up preventable mistakes later at a higher cost. Preferred CFO makes the case in its article on the role of the financial controller in growing business operations. Early controller structure helps companies avoid scaling bad processes into larger problems.

“I need a CFO, not a controller.”

If the books are late, inconsistent, or full of manual fixes, you need a controller first. Strategy built on unstable numbers is expensive guesswork.

Security Compliance and Tech Integrations

A founder usually notices the control problem too late. Refunds post to the wrong month, payroll access sits with former employees, Stripe fees drift out of sync with the ledger, and cleanup burns a week of close time. That is the cost of treating security and systems as an IT task instead of a controller responsibility.

A controller owns the reliability of the finance environment. That means permissions, approvals, audit trails, and system mappings that keep bad data out of the books in the first place. Paro makes the same point in its analysis of what controllers do, describing controllership as stewardship over internal controls and financial data handling aligned with SOC 2 Type II and similar security expectations.

For SaaS companies and agencies, early controller ROI shows up fast. One preventable revenue mapping error, duplicate vendor payment, or payroll coding issue can wipe out months of savings from delaying the hire. An outsourced controller usually makes sense before a full-time seat if your stack is growing more complex but your transaction volume still does not justify a dedicated in-house owner.

Controls first, integrations second

Finance teams create risk when they connect tools before setting control rules. Start with ownership. Then connect systems.

Your controller should define:

- Access control: Who can create vendors, change customer billing settings, approve payments, edit the chart of accounts, or post journals.

- Approval paths: Required signoff for AP, payroll changes, credits, refunds, write-offs, and off-cycle payments.

- Documentation standards: Support for manual journal entries, unusual balance sheet movements, and changes to revenue treatment.

- Review cadence: Reconciliations, exception review, lock dates, and a close checklist with named owners.

- Data retention: Contracts, invoices, payroll records, and approval support stored in one consistent system.

If you handle taxpayer data or other regulated financial records, tighten these controls early. Teams that need a practical explanation of access, storage, and audit requirements should review guidance on how to navigate IRS Pub 1075 regulations. The takeaway is simple. Sensitive data requires tighter permissions, clearer logging, and stronger evidence of review.

How the stack should connect

The accounting system should stay the system of record. Every other tool should feed it through reviewed mappings and controlled syncs.

| System category | Common tools | What the controller should enforce |

|---|---|---|

| General ledger | QuickBooks, Xero, NetSuite | Clean chart of accounts, locked periods, mapping review |

| Payments and billing | Stripe, Shopify, Square | Sync review, payout reconciliation, fee classification |

| Payroll and HR | Gusto, BambooHR | Payroll journal review, employee change controls, benefit coding |

| Revenue support | Contract and subscription systems | Contract terms mapped to revenue recognition policy |

| Reporting | KPI dashboards and management packs | Reconciliation back to ledger balances |

Automation cuts manual entry. It does not replace review.

Stripe can speed billing data flow into QuickBooks, but someone still needs to reconcile payouts and classify fees correctly. Gusto can push payroll journals automatically, but the controller still needs to verify department coding, benefits, and employee change approvals. NetSuite handles more complexity, but weak mappings produce bad reporting just as efficiently as good mappings produce clean reporting.

A clean integration without a control owner moves mistakes faster.

This is also where the outsource versus in-house decision gets practical. If your SaaS company or agency runs on QuickBooks or Xero, uses Stripe plus a payroll system, and needs tighter close discipline more than full-time staff management, a fractional controller is usually the better buy. Once the stack includes heavier approval volume, multi-entity structure, or constant system exceptions, the case for an in-house controller gets stronger because review cannot stay part-time for long.

This is the model firms like Jumpstart Partners use, providing outsourced controller services built around systems like QuickBooks, Xero, NetSuite, Stripe, Shopify, Square, Gusto, and BambooHR. For the compliance side of that work, review this SOC 2 Type II compliance resource against your current finance stack permissions, admin roles, and audit trail settings.

Actionable Hiring and Onboarding Checklist

A founder usually feels the pain before the org chart catches up. The close slips. Cash questions take too long to answer. Revenue reports need manual fixes. By the time leadership says, "we need a controller," the business has already paid for the delay through bad forecasts, missed billing issues, and preventable cleanup work.

Hire for ownership first. Technical accounting matters, but a controller earns their keep by shortening the close, preventing reporting errors, and forcing consistency across billing, payroll, expenses, and metrics. In SaaS and agencies, that return shows up fast because small classification mistakes can distort margin, churn, utilization, or deferred revenue decisions for an entire month.

As noted earlier, once outsourced bookkeeping costs move past the $8,000 per month threshold, you should seriously test the economics of a full-time controller instead of stacking more vendor hours onto a messy process.

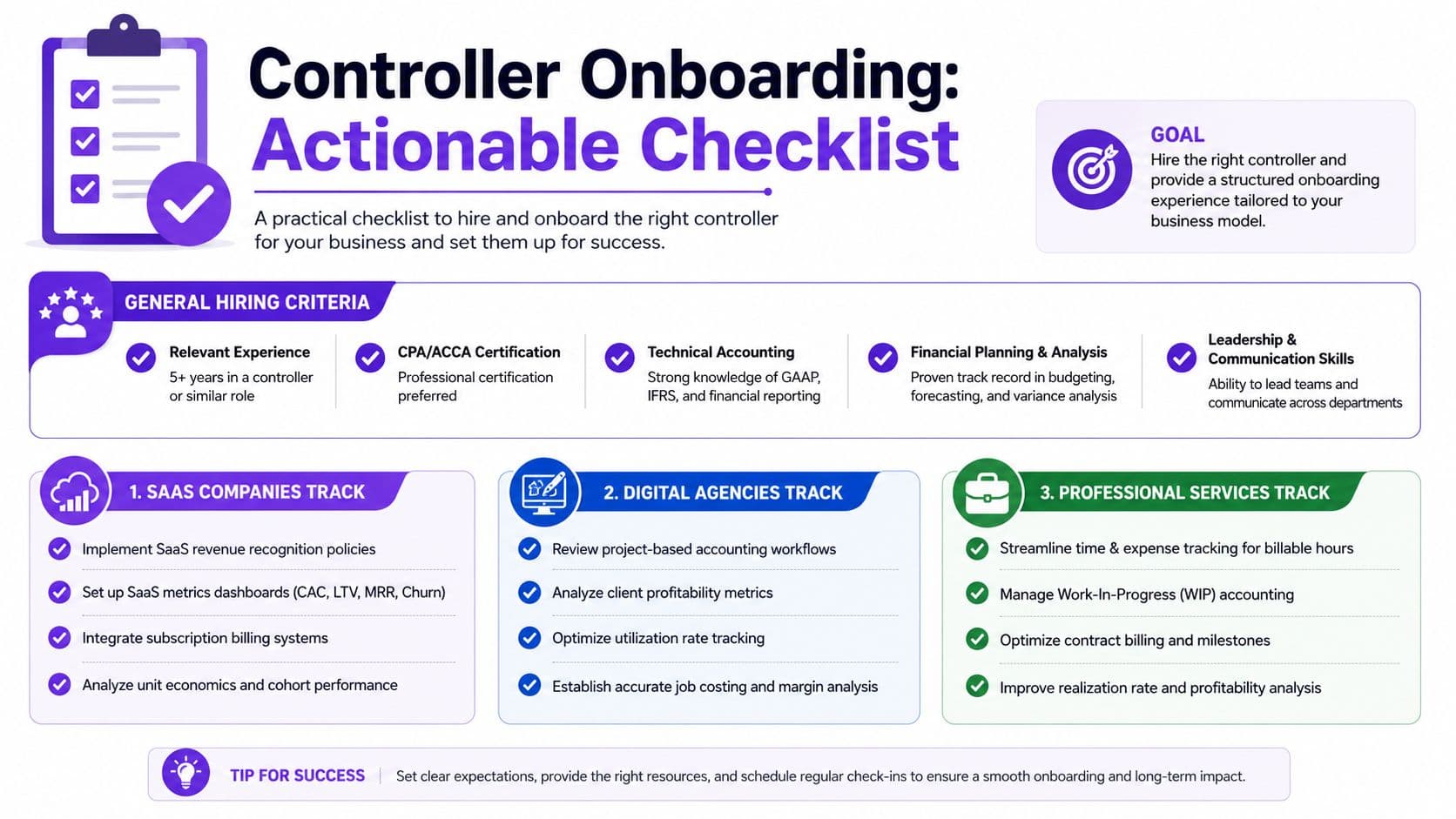

Hiring criteria that actually matter

Start with candidates who have run the work, not just supported it.

- Relevant experience: Treat 5+ years as the minimum for a true controller role in a growing company. You want someone who has owned close deadlines, reconciliations, accruals, and reporting review.

- Certification: The visual references CPA/ACCA certification. In the US, CPA is still the clearest signal that the candidate can handle technical accounting issues without outside help on every judgment call.

- Operational leadership: The right controller pushes department heads for missing inputs, fixes broken approval habits, and translates accounting issues into business impact.

- System judgment: Good candidates know where automation helps and where review still has to stay manual.

Ask direct questions and listen for process discipline:

- Walk me through your month-end close from day one to final review.

- How do you handle deferred revenue, prepaid expenses, and accruals?

- What controls do you put around payroll changes, vendor setup, and journal entries?

- How do you reconcile dashboard metrics to the general ledger?

- What would you fix in your first 30 days here?

A strong controller answers with steps, owners, review points, and examples. A weak one stays abstract.

First-month onboarding by business model

Give the new controller a specific operating brief. Generic onboarding wastes the first month and delays the payoff from the hire.

SaaS companies track

- Revenue policy first: Document how contracts, billing events, credits, and upgrades flow into revenue recognition.

- Metric definitions: Lock down MRR, ARR, churn, CAC payback inputs, and deferred revenue treatment so reporting stops shifting month to month.

- System checks: Review how billing, payments, and the ledger connect, then identify where exceptions still need manual review.

- Close plan: Set the target close calendar with named owners for reconciliations, entries, and final review.

Digital agencies track

- Project accounting review: Verify how labor, contractors, software pass-throughs, and client reimbursables are coded.

- Client profitability: Build reporting by client, service line, and team so margin problems show up early.

- Utilization discipline: Check time entry compliance and labor allocation rules. Weak time data ruins agency reporting.

- Billing review: Clean up retainers, milestone invoices, write-offs, and revenue cutoffs.

Professional services track

- WIP accounting: Review work-in-progress balances, reserve logic, and invoicing assumptions.

- Time and expense flow: Standardize how billable time and reimbursable expenses hit the ledger.

- Contract milestones: Match invoicing and recognition to actual delivery points.

- Collections reporting: Build AR visibility with named owners and escalation rules.

Red flags during hiring

Ignore these signs and you will hire a senior bookkeeper instead of a controller.

| Red flag | Why it matters |

|---|---|

| Candidate talks only about bookkeeping tasks | They are unlikely to own the accounting function or improve reporting speed |

| No clear close methodology | The business will stay dependent on heroics and late entries |

| Cannot explain controls simply | They will struggle to build compliance outside the finance team |

| Avoids operational details | Good controllers understand how money and data move through the business |

| Focuses on software before process | Tools speed up bad workflows just as easily as good ones |

Hire the candidate who can reduce confusion, enforce deadlines, and explain the numbers in plain English. That is the controller who saves more than they cost.

Conclusion and Next Steps

A controller in business gives you three things that founders regularly underestimate. Accurate books. Faster closes. Better decisions.

That changes how you run the company. You stop using stale numbers. You stop discovering cash issues after the fact. You stop walking into investor or lender conversations with half-finished financials.

The decision framework is straightforward.

First, assess where your finance operation is breaking. Look at close speed, reconciliation quality, metric trust, approval discipline, and reporting consistency. If those are weak, the problem is structural, not temporary.

Second, choose the right model. Under the lower complexity threshold, a bookkeeper plus outsourced controller can be enough. Once workload, reporting demands, and accounting management needs rise, move to a dedicated controller model. If your outsourced bookkeeping cost has already crossed the published threshold covered above, stop delaying the decision.

Third, treat onboarding as an operating rollout, not a hire-and-hope exercise. Define ownership. Set the close calendar. Lock metric definitions. Tighten systems access. Review controls monthly until the new cadence sticks.

If you're serious about building investor-ready reporting and a finance function that supports growth, book a conversation with the team that specializes in outsourced controller support for companies in this range.

If you need help deciding whether you need a bookkeeper, an outsourced controller, or a full in-house finance lead, Jumpstart Partners can help you assess the gap, tighten your close process, and put the right controller structure in place for your stage.