Financial Operations

Month End Close Process Flowchart: A 5-Day Guide

Create an effective month end close process flowchart with our 5-day guide. Learn to streamline tasks, automate reconciliations, and close books faster.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readMost month-end close advice is built for a neat, single-system business that barely exists in practice. That's why it breaks down the moment your company adds Stripe, Shopify, Gusto, QuickBooks, a CRM, and contract-based revenue recognition. The result is a close that drags, numbers you don't trust, and leadership decisions made on stale information.

The cost of that mess is measurable. According to a 2025 survey by Financial Executives International, companies that implement a standardized flowchart with defined roles and timeframes report a 40% improvement in cash flow visibility and detect an average of $47,000+ in errors per client annually. Without one, companies take an average of 10+ days to close, while only 22% of mid-sized firms achieve a 5-day or faster close (Financial Executives International data referenced here).

If you run a SaaS company, digital agency, or professional services firm in the $500K to $20M range, your close process isn't back-office admin. It's operating infrastructure. A real month end close process flowchart gives you clean handoffs, faster reconciliations, and reporting you can hand to investors, lenders, or auditors without apology.

Table of Contents

- Why Your Disorganized Close Is Costing You Growth

- The Core Components of an Investor-Ready Flowchart

- Your Day-by-Day Plan for a 5-Day Close

- How to Build and Visualize Your Close Flowchart

- Avoiding Pitfalls and Integrating Automation

- From Flowchart to Financial Clarity and Control

Why Your Disorganized Close Is Costing You Growth

A company that closes late runs late. The longer your books stay open, the longer leadership waits to spot margin erosion, collection risk, hiring overruns, and revenue leakage. By the time you review the numbers, the month you needed to fix is already gone.

That delay costs growth.

A disorganized month end close process flowchart creates more than accounting friction. It slows operating decisions, weakens forecast accuracy, and forces founders to manage from bank balance instead of reliable reporting. In scaling companies, that problem gets worse fast because the close has to pull data from billing platforms, payroll systems, expense tools, CRM workflows, and the general ledger. If those handoffs are unclear, your reporting turns into manual cleanup.

Slow closes lower decision quality

Once the close drifts past a week, the business starts making avoidable mistakes:

- Cash risk stays hidden: You catch overdue receivables, failed collections, or rising vendor spend after cash is already tight.

- Revenue gets misstated: SaaS teams miss contract changes, usage adjustments, refunds, and deferred revenue movements if billing and accounting are not tied together cleanly.

- Errors last longer: Reconciliation issues in payroll, A/R, prepaid expenses, and accrued liabilities sit in the ledger until review happens.

- Leaders stop trusting the numbers: If every monthly package gets revised, the board deck becomes a debate about accuracy instead of performance.

Practical rule: If leadership waits for “final-final” numbers before making decisions, financial control is weak.

A proper flowchart fixes this by assigning ownership, sequence, review points, and system dependencies. It shows which tasks happen before month-end, which inputs come from each platform, and where the period locks. If you need a baseline before building that map, start with these month-end close best practices.

The financial cost shows up in real operating decisions

A 10-day close is not normal. It signals weak process design.

Here is what that looks like in practice. A SaaS company ends the month believing gross margin is 74%. Eight days later, finance finishes deferred revenue and contractor accruals, and actual gross margin lands at 68%. If leadership approved paid acquisition spend, new hiring, or sales commissions based on the wrong number, the business just made real cash decisions off bad data.

The same pattern hits agencies, ecommerce brands, and services firms. If project costs, inventory adjustments, or payroll allocations arrive late, the P&L you review is stale before it is even published. That is why a close flowchart for a scaling company cannot be a generic checklist. It has to account for automation debt across multiple systems and, where relevant, compliance requirements such as SaaS revenue recognition.

What founders usually get wrong

Founders often treat the close as a reporting task. It is a control system.

It tells you whether customer acquisition is still paying back on time, whether service delivery is eroding margin, whether revenue is being recognized correctly, and whether departmental spending is following plan. If that system is messy, every board conversation downstream gets weaker.

Clean books do more than explain the past. They let you act while the month still matters.

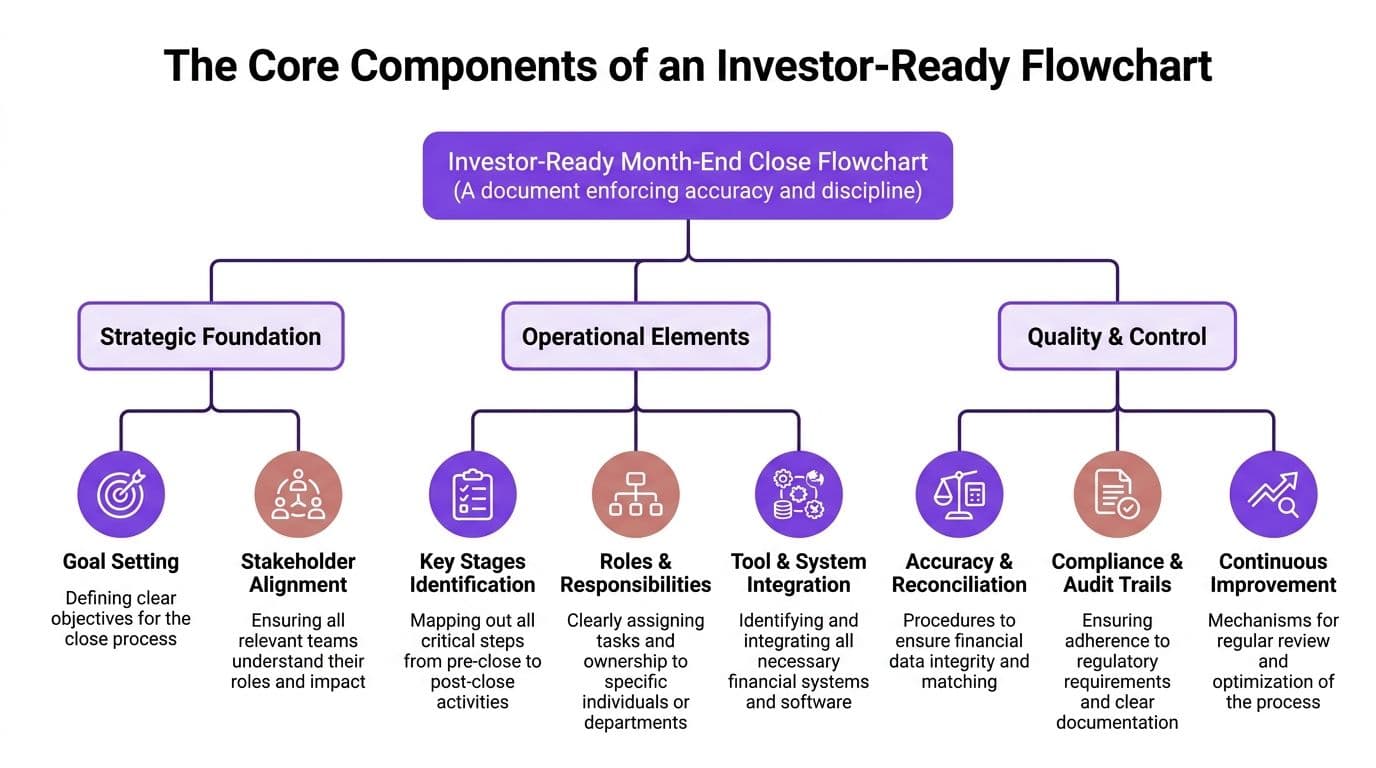

The Core Components of an Investor-Ready Flowchart

An investor-ready month end close process flowchart should answer four questions in seconds. What happens first, who owns it, which system supplies the data, and what review happens before the number hits the financials. If your flowchart cannot answer those four questions, it will not hold up under board scrutiny, lender diligence, or audit testing.

Four layers every flowchart needs

I build close flowcharts for scaling companies with four layers, not three. The extra layer matters because fast-growing teams rarely fail on task lists alone. They fail at control points between disconnected tools.

| Layer | What it should show | Why it matters |

|---|---|---|

| Phases | Pre-close, close, post-close | Prevents teams from cramming all work into the first week |

| Roles | Preparer, reviewer, approver | Removes handoff confusion and review bottlenecks |

| Systems | Source systems, general ledger, reporting tools | Shows where data breaks across platforms |

| Controls | Reconciliations, approvals, exception checks, period lock | Protects the accuracy of board and investor reporting |

The phase layer sets timing. Contract changes, accrual inputs, invoice cleanup, and payroll review should start before the calendar flips. Waiting until Day 3 to chase missing inputs is how a 5-day target turns into an 11-day close.

The role layer assigns accountability. A bank reconciliation prepared by staff and reviewed by the controller is a real control. A bank reconciliation "owned by finance" is a recipe for stale cash balances and missed exceptions.

The system layer is where generic templates fall apart. A scaling company might bill in Stripe, track contracts in HubSpot, run payroll in Gusto, recognize revenue in a SaaS subledger, and report from QuickBooks or NetSuite. Your flowchart needs to map every handoff between those tools. If it does not, automation debt stays hidden until one sync breaks and revenue, cash, or deferred balances go wrong. For that mapping to work, your chart of accounts structure should reflect how the business actually earns and spends money.

The control layer forces accounting judgment into the process. As one of our senior controllers often says, a good close flowchart should show where judgment happens, not just where tasks get checked off.

What investor-ready actually looks like

Investor-ready means a reviewer can trace a number from source system to final financial statement without guessing. It also means your close process reflects the rules of your business model.

For SaaS companies, that includes contract review, deferred revenue rollforwards, and ASC 606 revenue recognition checkpoints. For agencies and services firms, it includes WIP, retainers, utilization-based accruals, and project cutoff reviews. For ecommerce brands, it includes inventory adjustments, returns reserves, payment processor clearing, and gross-to-net revenue checks.

Analysts at Numeric found that finance teams with standardized close processes closed faster and with fewer errors than teams relying on ad hoc workflows (Numeric month-end close guide). That result tracks with what we see in practice. Structure beats effort. Throwing more late nights at a broken close does not fix cross-system mapping, missing approvals, or unsupported journal entries.

Your flowchart should include:

- Pre-close controls: Expense cutoff reminders, open contract review, payroll confirmation, source system sync checks, and recurring entry validation

- Close activities: Bank reconciliations, A/R and A/P tie-outs, deferred revenue schedules, accruals, fixed asset updates, and variance review

- Post-close controls: Management review, reporting package release, period lock, support archive, and exception log follow-up

Be specific. "Review revenue" is weak. "Tie subscription bookings, billings, and recognized revenue to the GL before issuing financials" is useful. "Reconcile cash" is weak. "Match bank activity, payment processor settlements, and outstanding transfers before controller review" is useful.

For teams that still rely on spreadsheets for portions of the close, even a basic reconciliation template can help standardize support. One example is One For All Medical Billing, which shows how to structure a bank rec worksheet clearly enough for review.

If the flowchart does not match your operating model, it will fail at the exact moment accuracy matters most.

Your Day-by-Day Plan for a 5-Day Close

A 5-day close is realistic when you stop treating month-end like one giant event. The businesses that hit it consistently break work into daily deadlines, assign owners, and force review discipline. They don't wait until Day 6 to discover payroll is missing, revenue is off, or bank activity didn't sync.

According to OpenView's 2024 SaaS Benchmarks cited here, 60% of SaaS firms that close after the 10th of the month face audit rework costs averaging $12K per quarter. The same benchmark calls for a strict timeline with expense reports by Day 2 and reconciliations by Day 5.

Sample 5-Day Month-End Close Timeline

| Day | Key Tasks | Responsible Role | Status |

|---|---|---|---|

| Day 1 | Freeze prior-month operational inputs, confirm bank feeds, collect missing bills, review open invoices, pull source-system exports | Staff accountant, ops lead | Complete by end of day |

| Day 2 | Finalize expense reports, post recurring entries, review payroll, update prepaid and accrual schedules | Accountant, payroll owner | Complete by end of day |

| Day 3 | Reconcile cash, credit cards, A/R, A/P, and key balance sheet accounts | Senior accountant or controller | Under review |

| Day 4 | Finalize revenue recognition, review deferred revenue, investigate variances, draft financial statements | Controller | Ready for approval |

| Day 5 | Complete final reviews, lock reporting package, issue statements to leadership, close period support file | Controller, CFO, founder as approver | Final |

This schedule works because it separates data gathering from review. It also forces account ownership. If nobody owns deferred revenue, accrued expenses, or intercompany cleanup, Day 5 slips every month.

For teams still managing reconciliations manually, even a simple structured worksheet can help standardize support. A resource like this bank reconciliation Excel template from One For All Medical Billing is useful when you need a cleaner starting point for account support before moving into a more automated workflow. If your close is consistently slipping because reconciliations lag, dedicated reconciliation services usually solve the root problem faster than adding more meetings.

A worked cost calculation for a late close

Use the OpenView benchmark as a management lens, not just an audit lens.

If a company closes after the 10th and falls into the group facing audit rework costs averaging $12K per quarter, the annualized cost is straightforward:

- $12,000 per quarter

- 4 quarters per year

- $12,000 × 4 = $48,000 per year

That's $48,000 per year in rework cost tied to a late close.

Now compare that with the operational effect of fixing the timeline. A 5-day close gives leadership the numbers roughly five days earlier than a 10-day close. That means you get an earlier shot at fixing pricing errors, chasing overdue receivables, questioning margin drops, or tightening spending before another week of bad assumptions passes through the business.

You don't need a complex ROI model to see the point. If poor close discipline can cost $48,000 annually in rework alone, the process deserves attention.

Close speed isn't vanity. It's control over when you discover mistakes.

Common objection from founders

The usual objection is, “We're too small for a formal close flowchart.”

That's backwards. Smaller companies feel bad close discipline faster because fewer people are catching mistakes. One controller, one bookkeeper, and one founder can't rely on tribal knowledge when revenue is growing and the software stack is expanding.

Another objection is, “Our close is delayed because the business is complex.” Complexity is exactly why you need a day-by-day operating plan. Without one, every exception becomes an excuse.

How to Build and Visualize Your Close Flowchart

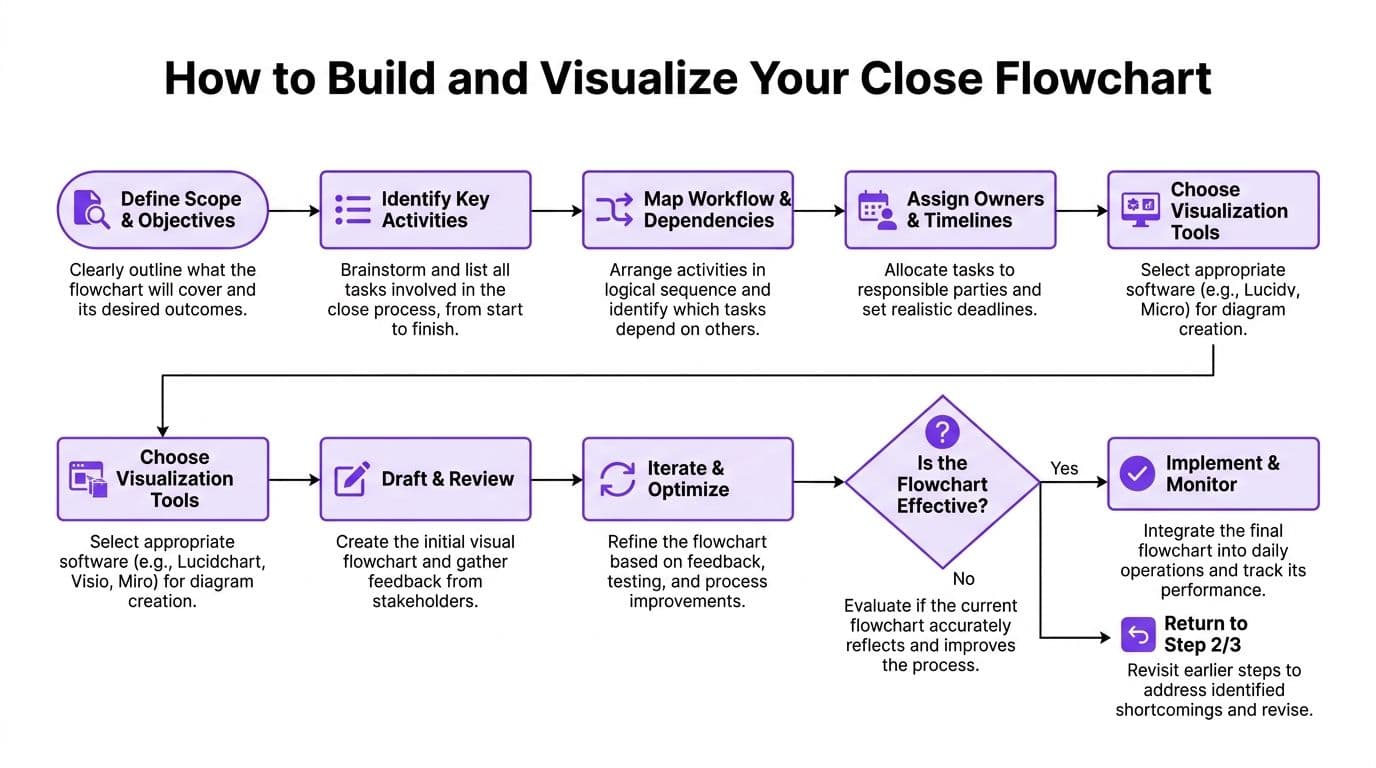

Build the flowchart from the actual close your team runs, not the idealized version sitting in your ERP settings. Scaling companies rarely close inside one system. They close across a patchwork of billing tools, payroll apps, banks, expense platforms, and the general ledger. If your diagram ignores those handoffs, it will fail the first time Stripe, Gusto, Shopify, and NetSuite disagree.

Start with the raw process. Use a whiteboard, spreadsheet, Miro board, or Lucidchart. Put every task in sequence based on when the work happens. Then add the dependency behind it. Revenue review waits on billing exports, contract changes, and any usage file tied to invoicing. Payroll entries wait on approved payroll reports and benefit deductions. Cash reconciliation waits on bank feeds and any manual transfers that have not cleared yet.

Build the map before you beautify it

Your first draft should show five things clearly:

-

Recurring tasks

Include bank reconciliations, credit cards, accrued expenses, payroll, deferred revenue, fixed assets, debt, sales tax, and reporting package prep. -

Named owners

Assign a person or role to each step. “Accounting” is too vague to hold anyone accountable on Day 3. -

Dependencies

Mark what has to finish before the next task can start. -

Review points

Identify where the controller, finance lead, or founder signs off. -

System touchpoints

List the source systems feeding the ledger, such as QuickBooks, Xero, NetSuite, Stripe, Shopify, Gusto, or BambooHR.

Decision points matter just as much as task boxes. Your flowchart should answer practical questions under pressure. If A/R does not tie to the subledger, who investigates it? If payroll accruals move more than your materiality threshold, who reviews the variance? If a contract amendment hits on the last day of the month, does it change current-period revenue or next month's schedule? SaaS companies need this level of specificity because revenue recognition errors do not stay isolated. One bad contract mapping can distort MRR, deferred revenue, and board reporting in the same close.

A ready-made month-end close checklist template can speed up the first draft if your team is still pulling steps from memory.

A walkthrough helps if your team needs a visual reference before building its own process:

The lock sequence is a required control

A critical control many teams skip is the mandatory Lock A/R, Lock A/P, Close Period sequence. As noted earlier, teams that skip period locks create avoidable variance issues because staff can still edit customer balances, bills, and journals after review is supposed to be complete.

That sequence protects the integrity of the month:

- Lock A/R: Freeze receivable activity so no one adds a late invoice or edits customer balances after review.

- Lock A/P: Stop bill changes and expense postings from shifting the period after reconciliations are done.

- Close Period: Preserve support, confirm the audit trail, and block further posting to the month.

Controller's rule: If people can still post after draft financials go out, the close is still open.

Keep the final flowchart readable in under a minute. One page is enough for the high-level map. If you need more detail, link each box to a task-level SOP. That is how mature finance teams handle real-world complexity without turning the close into a diagram nobody uses.

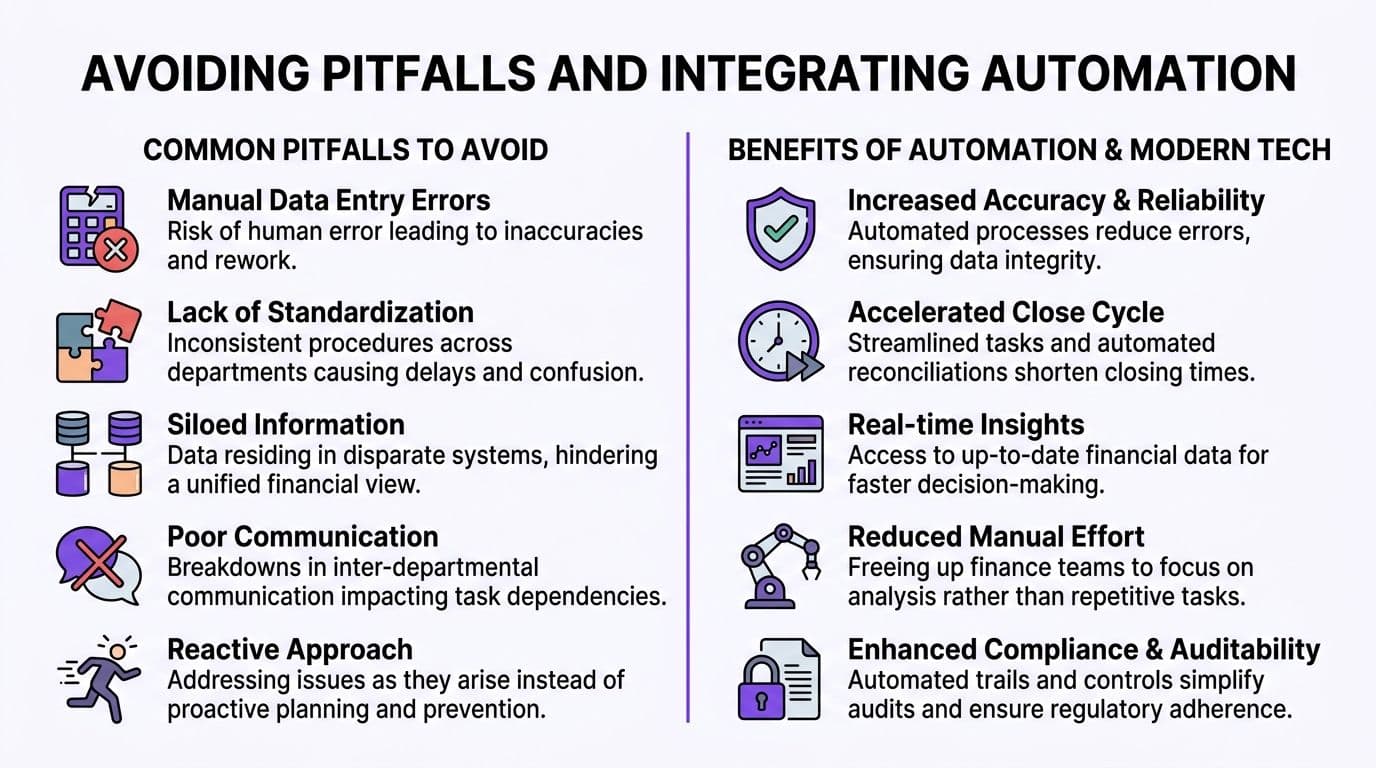

Avoiding Pitfalls and Integrating Automation

Close problems usually start long before Day 1. They start when a company outgrows the process it built at $2 million in revenue and keeps forcing that same process to work at $10 million or $30 million. More entities, more billing tools, more payment rails, more payroll complexity, and more compliance requirements turn a basic checklist into a source of reporting risk.

The expensive part is not the extra work. It is the delay and the bad decisions that follow. If your controller and accounting team spend 20 extra hours a month exporting CSVs, fixing mappings, and chasing cross-system variances, that is real cost. At a blended finance labor cost of $75 to $125 per hour, you are spending $1,500 to $2,500 a month just to recreate information your systems should already agree on. That is before you count leadership meetings built on numbers that later change.

Generic public guides also create a blind spot by ignoring automation debt and industry-specific compliance. A scaling SaaS company does not just need a box that says "review revenue." It needs a flow that ties contracts, billing events, deferred revenue, and the general ledger together in a way that supports ASC 606. An agency needs client profitability and payroll allocation to reconcile cleanly. An e-commerce business needs payment processor clearing, returns, and inventory cutoff handled in the same process, not in side spreadsheets.

Red flags that your close process is breaking

Your month end close process flowchart is too weak for your current stage if any of these are true:

- Revenue review is vague: “Check revenue” does not work for SaaS, retainers, usage billing, milestone billing, or contract changes.

- Teams export and re-key data manually: Every CSV handoff creates another chance for duplicate entries, cutoff errors, or mapping drift.

- Reconciliations are isolated: Cash, A/R, A/P, payroll, and revenue are reviewed separately with no tie-out to the final financial package.

- No owner is assigned to system failures: Stripe sync breaks, payroll classes post wrong, or CRM data fails to map, and nobody resolves it until close week.

- The period stays open while reports circulate: Leadership reviews numbers that can still change, which destroys confidence in the first draft.

- One spreadsheet expert holds the process together: That is key-person risk, not a close process.

Where Automation Delivers the Most Value

Automation should remove recurring manual work, tighten controls, and surface exceptions earlier. If it does not do those three things, it is overhead.

Start with the handoffs that break every month. For many companies, that means billing to ledger, payroll to departments, bank and processor activity to cash, and subledger balances to the balance sheet. If you need a stronger reporting stack across disconnected systems, financial reporting automation should be built into the close design, not added after the fact.

Focus on these areas first:

| Automation target | What to automate | Why it matters |

|---|---|---|

| Data ingestion | Pull source data from billing, payroll, banking, and expense tools | Cuts version-control issues and manual file chasing |

| Reconciliation logic | Match bank, subledger, and platform balances automatically | Flags variances before review meetings |

| Revenue workflows | Sync contracts, billing events, and ledger entries | Protects revenue recognition and deferred revenue accuracy |

| Exception handling | Trigger alerts for missing, late, or unusual transactions | Keeps reviewers focused on material issues |

Automation does not replace accounting judgment. It replaces repetitive comparison work so your controller can review exceptions, investigate changes, and make decisions faster.

The priority should match your business model. SaaS companies should start with revenue recognition, deferred revenue rollforwards, and platform syncs. Agencies and services firms should start with payroll allocation, project or client profitability mapping, and A/R cleanup. E-commerce companies should start with processor reconciliation, returns, inventory cutoff, and clearing accounts. If you want to streamline month-end accounting in a way that survives growth, the flowchart has to reflect those operational realities instead of copying a generic month-end template.

From Flowchart to Financial Clarity and Control

A strong month end close process flowchart changes the finance function from reactive cleanup to active control. You stop spending the first half of every month figuring out what happened last month. Instead, you deliver numbers leadership can use while they still matter.

What changes when the close is controlled

The first shift is trust. The founder, CEO, and department leads stop treating the monthly package like a draft. They know the P&L, balance sheet, and cash view were built through a repeatable process with clear reviews and locked periods.

The second shift is speed. Not just close speed. Decision speed. When revenue, expense timing, receivables, and cash are visible earlier, leadership acts earlier.

The third shift is credibility. Investors, lenders, and auditors can tell when a company has discipline. If you want to streamline month-end accounting in a way that supports growth, the process has to match the complexity of your business, not a generic checklist from a search result.

What to do next

If your current close is running long, don't try to fix everything at once. Start with these actions:

-

Map the current process exactly as it exists

Include every task, owner, review point, and system handoff. -

Set a Day 1 through Day 5 deadline for each major workstream

Don't leave timing implied. -

Add the lock sequence to the end of the close

A/R, A/P, then close period. -

Identify your top two failure points

Usually revenue, reconciliations, or cross-platform data mismatches. -

Automate the repeated comparison work

Keep human review for exceptions, approvals, and judgment.

If you do those five things well, your close gets faster, cleaner, and easier to defend. That's what founders and finance leaders need. Not another generic template. A process that holds up under real operating complexity.

If you want help building a close process that works for a scaling company, Jumpstart Partners can help you design, clean up, and run it. Their team supports growing businesses with outsourced controller services, investor-ready reporting, and a disciplined 5-day close process suited for SaaS, agencies, and service firms.