Financial Operations

SaaS Financial Metrics: The Founder's Guide for 2026

Master the essential SaaS financial metrics for 2026. Our guide covers MRR, LTV:CAC, churn, NRR, and more with formulas, benchmarks, and actionable steps.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··23 min readA SaaS company can post impressive top-line growth and still be structurally unhealthy. The benchmark that should reset your thinking is this: for SaaS companies generating $10M in ARR in 2024, the average valuation multiple is 5.5x, or about $55M, and that multiple is the lowest in three years because buyers and investors now reward efficient revenue scaling, not growth at any cost, according to Lucid's 2024 SaaS financial benchmarks.

If you're running a business between $500K and $20M in revenue, that's the entire game. Investors aren't giving you credit for messy dashboards, inflated ARR, or hand-wavy LTV assumptions. They want clean recurring revenue, credible retention, and proof that your go-to-market engine returns cash, not just pipeline updates.

Most founders still watch the wrong numbers. They look at the bank balance, celebrate booked revenue, and quote LTV:CAC like it's enough. It isn't. The SaaS financial metrics that matter most at your stage are the ones that tell the truth about cash efficiency, retention quality, and whether your revenue model holds up under scrutiny.

Table of Contents

- Why Most SaaS Founders Misread Their Financial Health

- Mastering MRR and ARR Your North Star Metrics

- Your Engine of Growth Churn Net Retention and Growth Rate

- Are You Buying Profitable Growth LTV CAC and Payback Period

- Beyond Revenue The Rule of 40 and Burn Multiple

- How to Measure and Reconcile Your Metrics

- Common SaaS Accounting Mistakes and How to Fix Them

- When and How to Outsource Your SaaS Financial Stack

Why Most SaaS Founders Misread Their Financial Health

Your P&L doesn't tell you what you think it tells you.

A subscription business lives and dies on timing. Cash comes in on one schedule, revenue gets recognized on another, customer contracts renew on another, and sales spend usually lands before revenue shows up. That's why a founder can celebrate a record month and then run straight into a cash squeeze weeks later.

The problem gets worse when you treat standard bookkeeping reports like operating dashboards. A clean income statement matters, but it won't tell you whether churn is wiping out expansion or whether your acquisition engine is buying customers too expensively. And your bank balance is not a KPI. It's a lagging symptom.

The most common misread

Founders often say some version of this: revenue is up, cash is still in the account, and pipeline looks solid. That sounds fine until you inspect the revenue mix and realize a chunk of the “good month” came from annual prepayments, implementation fees, or services work that doesn't repeat.

If you run SaaS, agency, or professional services models with recurring components, you need a second language on top of accounting. You need recurring revenue metrics, retention metrics, and unit economics that tie back to the books.

Practical rule: If your operating decisions rely more on booked revenue than recurring revenue movement, you're managing optics instead of economics.

Why accounting treatment matters

Often, many teams drift into sloppy reporting. They count cash received as revenue earned, pull one-time onboarding into MRR, or ignore deferred revenue. Then they present those numbers to lenders or investors and get torn apart in diligence.

If your team needs a cleaner foundation for revenue timing, read ASC 606 revenue recognition for recurring revenue businesses. You don't need to become an accountant, but you do need to understand why recognized revenue and collected cash are not interchangeable.

Here are the warning signs that you're reading the business wrong:

- You celebrate collections as growth. Annual prepayments improve cash now, but they don't mean monthly revenue momentum improved.

- You report one revenue number to everyone. Sales, finance, and leadership should agree on bookings, billings, recognized revenue, and recurring revenue. If those terms blur together, your forecasts will too.

- You trust the bank balance. Cash can hide problems for a while. Retention weakness and inefficient CAC eventually show up anyway.

The founders who scale cleanly stop asking, “Did revenue go up?” They ask, “Did recurring revenue quality improve, and did we do it efficiently?”

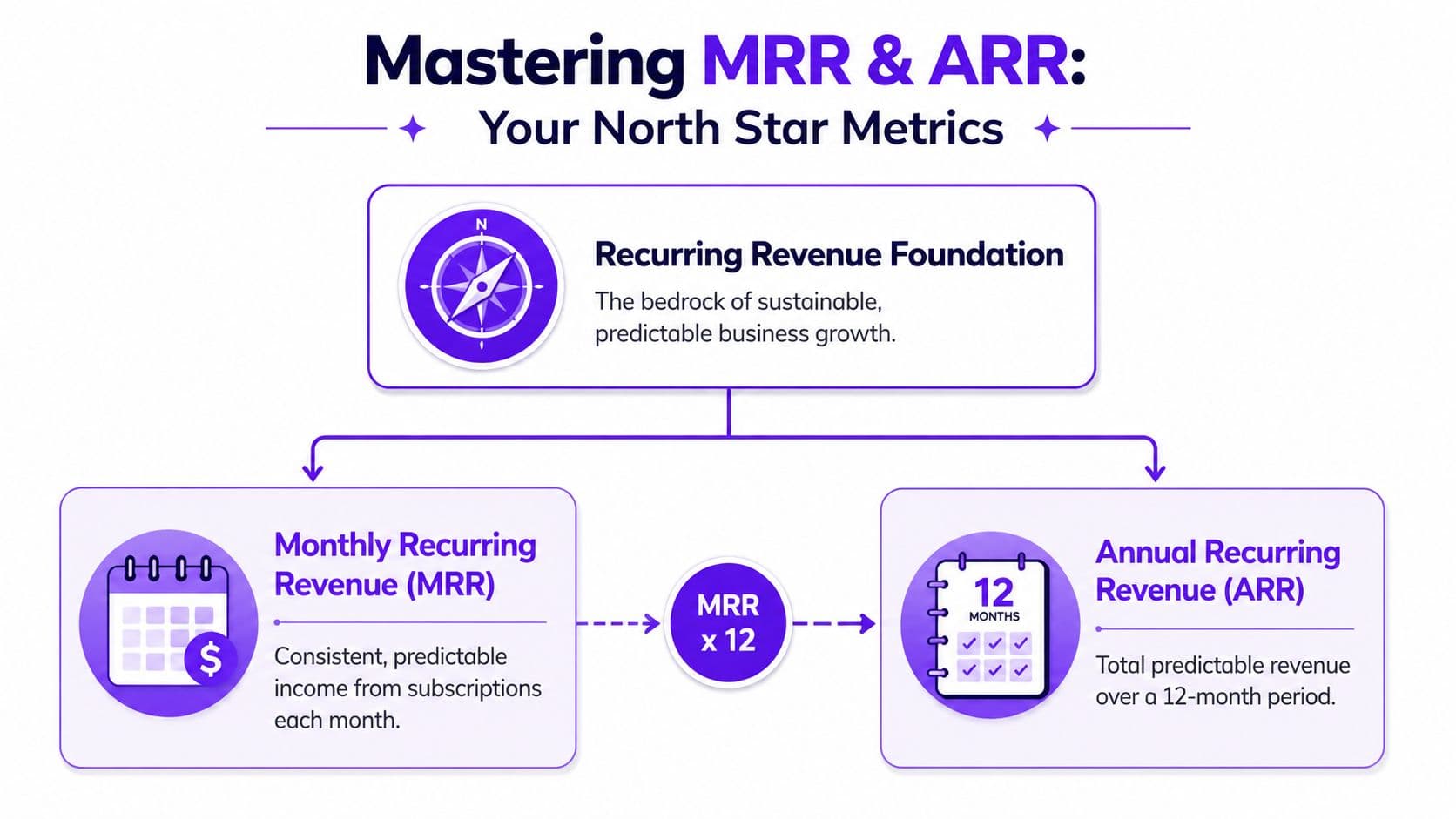

Mastering MRR and ARR Your North Star Metrics

MRR and ARR are your operating spine. If these numbers are wrong, everything built on top of them is wrong too.

Monthly Recurring Revenue tells you what your subscription engine is producing each month. Annual Recurring Revenue gives you the annualized view. The relationship is simple. ARR = MRR x 12. But the discipline is not simple, because most companies contaminate these numbers with revenue that should never be there.

What belongs in MRR and what does not

Count only revenue that is recurring, contractual, and expected to repeat.

Include:

- Recurring subscription fees. Standard monthly or annual software subscriptions, normalized to a monthly amount.

- Committed platform fees. Fixed recurring charges that renew as part of the customer contract.

- Recurring retainers. If you're a digital agency or professional services firm with contracted recurring service revenue, keep it separate from SaaS MRR if the business is hybrid, but track it with the same rigor.

Exclude:

- Setup and onboarding fees. These are one-time by definition.

- Consulting projects. Useful revenue, but not recurring revenue.

- Implementation work. Especially dangerous in hybrid models because it inflates perceived momentum.

- Variable usage and pass-through charges. If the amount isn't predictable and committed, don't call it MRR.

If you need a more formal framework, use this guide to annual recurring revenue and how to annualize it correctly.

A lot of founders first understand recurring revenue through creator businesses and memberships. This explainer on predictable income for creators is a useful parallel because it shows why consistency matters more than occasional spikes.

A simple MRR waterfall example

The MRR waterfall is the cleanest way to show what changed in a month.

Assume you start the month with $100,000 MRR.

During the month:

- You add $12,000 in new MRR from new customers.

- Existing customers expand by $8,000.

- Downgrades reduce MRR by $3,000.

- Churn removes $7,000.

Your ending MRR is:

| MRR movement | Amount |

|---|---|

| Starting MRR | $100,000 |

| New MRR | $12,000 |

| Expansion MRR | $8,000 |

| Contraction MRR | ($3,000) |

| Churned MRR | ($7,000) |

| Ending MRR | $110,000 |

That means your ARR at month end is:

$110,000 x 12 = $1,320,000 ARR

This is the report your leadership team should review every month, not just the top-line accounting revenue number.

A clean MRR waterfall does two jobs at once. It shows whether growth came from new sales or expansion, and it exposes whether churn is eroding the business underneath the surface.

A quick visual overview helps align everyone before the monthly review.

If your board deck shows ARR but cannot explain the monthly movement that built it, you're presenting a headline without the engine.

Your Engine of Growth Churn Net Retention and Growth Rate

Investors give premium valuations to SaaS companies that keep growing after the initial sale. New bookings get attention. Retention determines whether that growth is durable or expensive.

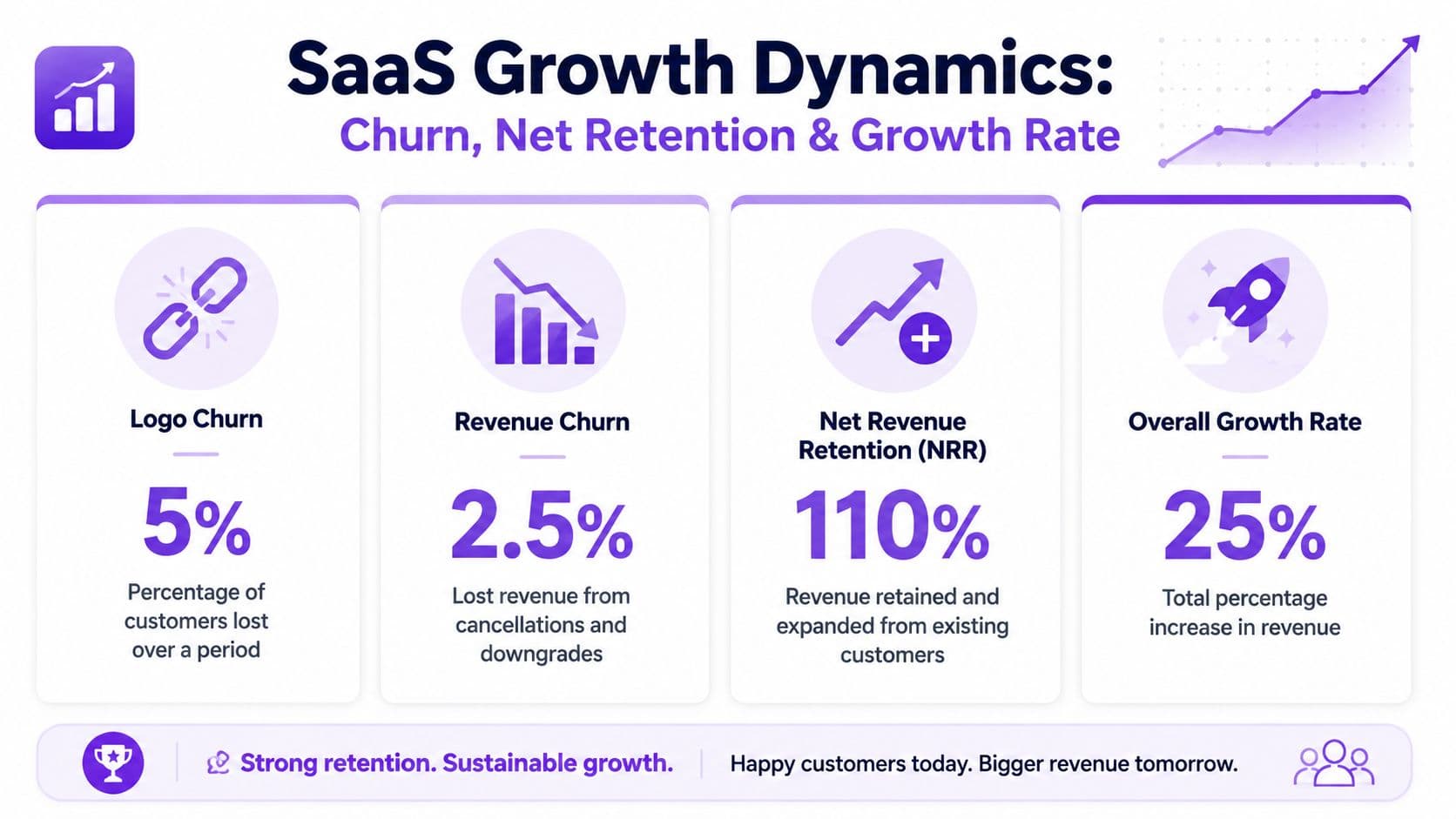

That is why Net Revenue Retention belongs on the first page of your board deck. If NRR is below 100%, your existing customer base is shrinking in revenue terms. You are refilling a leaking bucket. If NRR is 110%, you have a solid business. If it is 120% or better, you have the kind of expansion profile that gets investors interested fast.

Why revenue churn matters more than logo churn

Logo churn answers a sales question. Revenue churn answers a finance question.

Losing five $200 accounts is annoying. Losing one $20,000 account can wreck your quarter. That is why experienced operators track customer count churn, but they manage the business using revenue retention.

You need to isolate four movements inside the installed base:

- Renewals. Customers stay at the same spend level.

- Expansion. Customers increase spend.

- Contraction. Customers cut seats, usage, or plan level.

- Churn. Customers leave and revenue drops to zero.

If your team still blurs these together, fix that first. Use a clean GRR vs NRR framework for subscription businesses so everyone uses the same definitions in board reporting, forecasting, and compensation discussions.

A worked NRR example

Start with a cohort that produces $100,000 in recurring revenue at the beginning of the period.

During the period:

- Expansion adds $25,000

- Contraction removes $5,000

- Churn removes $10,000

Ending revenue from that same starting cohort is:

$100,000 + $25,000 - $5,000 - $10,000 = $110,000

NRR is:

$110,000 / $100,000 = 110%

That is healthy. It is not elite.

Use this interpretation table internally:

| NRR range | What it says |

|---|---|

| Below 100% | Your existing customer base is shrinking in revenue |

| 100% to below 120% | Retention is decent, but expansion is not yet strong enough to create standout compounding |

| 120% or higher | Existing customers are driving meaningful growth and signaling strong product value |

When NRR drops below 100%, new sales become churn replacement. Growth looks better on the surface than it is in cash terms.

Churn and growth rate need to be read together

A 30% growth rate built on poor retention is fragile. A 30% growth rate with strong NRR is far more valuable because future revenue starts from a larger, more stable base.

This matters even more for companies in the $500K to $20M range. At that stage, founders often lean too hard on top-line growth because it sounds good in a fundraising update. Investors will still ask the harder question: how much of next year's revenue is already protected inside the current customer base?

For hybrid SaaS models, be strict about segmenting the analysis. Subscription retention, usage-based expansion, and services revenue do not behave the same way. If you mix them together, your growth rate looks cleaner than the business is.

What founders usually get wrong

Three mistakes keep showing up:

- They mix new sales into NRR. NRR only measures revenue from customers you already had at the start of the period.

- They hide contraction. Downgrades are an early warning sign for product value, pricing fit, and customer health.

- They celebrate growth without asking where it came from. Expansion growth is worth more than growth purchased through aggressive acquisition because it usually carries better margins and better cash efficiency.

Founders also spend too much time arguing about LTV assumptions while ignoring retention mechanics they can control this quarter. That is backwards. Fix churn, improve expansion, and your cash metrics improve with them.

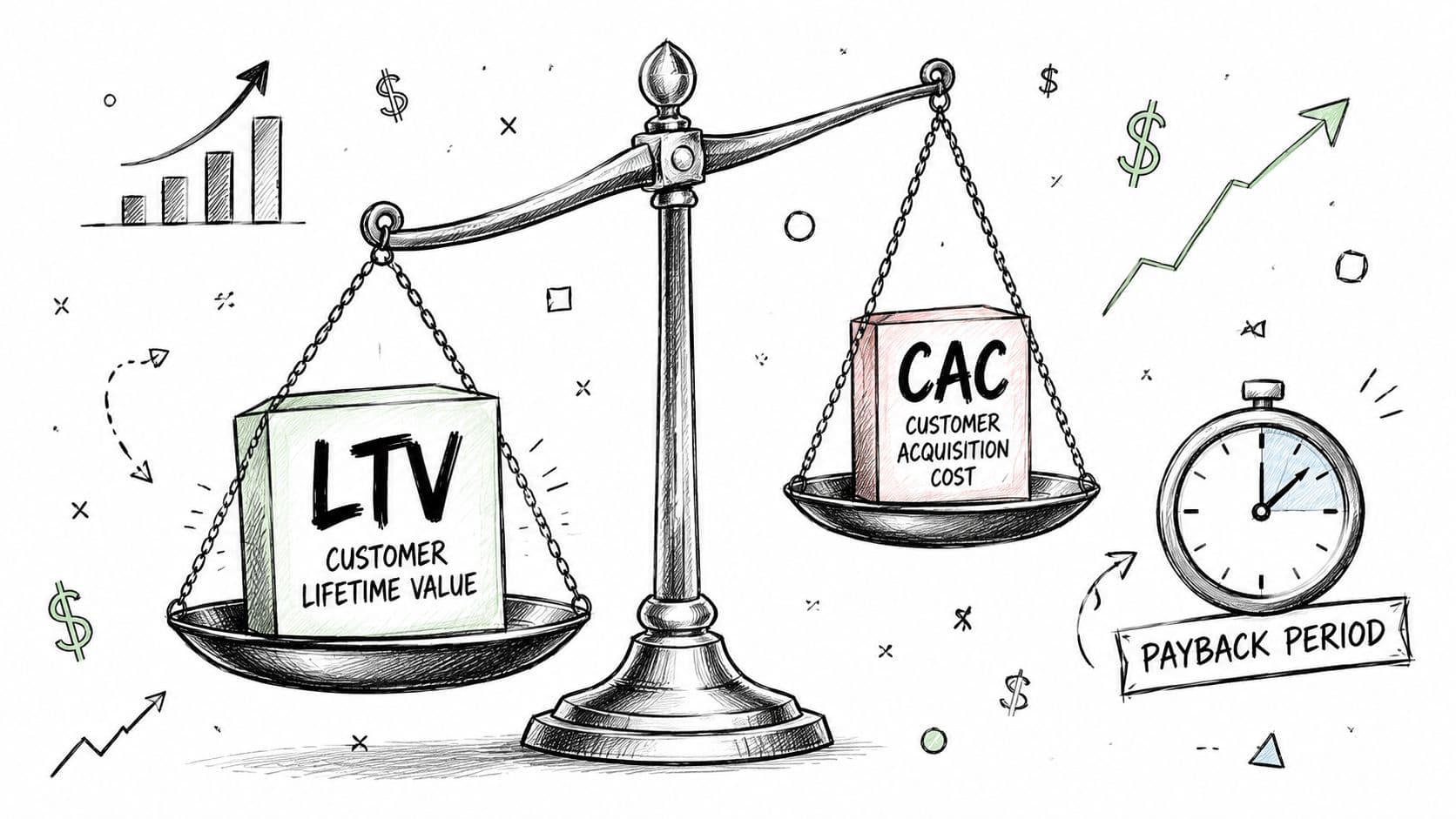

Are You Buying Profitable Growth LTV CAC and Payback Period

A business can post a 3:1 LTV:CAC ratio and still run out of cash. That is why founders in the $500K to $20M range should stop treating LTV:CAC as the headline metric for growth efficiency.

I use a stricter standard. CAC payback period matters more than LTV:CAC for operating decisions because payback shows how quickly sales and marketing spend returns as gross profit you can reinvest. Investors still want to see LTV:CAC, but they trust cash recovery speed more than a lifetime value model built on churn assumptions that can change in one bad quarter.

How to calculate CAC and LTV

Start with clean acquisition math.

If you spend $50,000 on sales and marketing and win 100 new customers, your CAC is:

$50,000 / 100 = $500 CAC

If average customer lifetime value is $1,500, then:

LTV:CAC = $1,500 / $500 = 3:1

That clears the standard benchmark many SaaS investors expect to see. The problem is that this ratio can look healthy while the business stays cash-hungry.

If your team needs tighter definitions and reporting discipline, keep this guide to unit economics for subscription businesses in your finance stack.

Why CAC payback beats LTV:CAC at your stage

Payback is the cash-truth metric.

Aleph's analysis of SaaS metrics that matter argues that operators should put more weight on CAC payback period because it measures capital efficiency in real time. That is the right standard for companies that cannot afford to wait 18 months to learn whether growth was efficient.

Here is the simple version. If CAC is $500 and a new customer contributes $100 per month in recurring revenue, simple payback is:

$500 / $100 = 5 months

That number is useful immediately. You can compare paid search against outbound, compare SMB against mid-market, and see whether discounting is buying volume at the cost of slower cash recovery.

A long payback period creates real operating stress. You hire ahead of revenue, increase burn, and depend on future rounds or a credit line to cover the gap. A modeled LTV number will not protect you from that.

For businesses in your stage range, I recommend using these rough guardrails:

| Metric | What good looks like | What founders should do |

|---|---|---|

| LTV:CAC | 3:1 or better | Keep it as a secondary check, not the main decision tool |

| CAC Payback Period | Shorter is better, with channel-level visibility | Review monthly by segment, channel, and sales motion |

| High ratio, slow payback | Paper efficiency, weak cash efficiency | Cut spend in channels that recover too slowly |

What investors look for and what costs you money

Investors do not just ask whether a customer is profitable over time. They ask how much cash you burn before that customer becomes productive.

Three mistakes keep hurting founders here:

- They calculate CAC too narrowly. If you exclude sales salaries, commissions, agency fees, and program costs, your payback number is fiction.

- They use revenue instead of gross margin to judge recovery. A company with 70% gross margin recovers CAC more slowly than the same company at 85%, even with identical ARR growth.

- They report one blended payback figure. Enterprise, self-serve, partner-led, and outbound channels should not be lumped together.

If your paid channel has a 6-month payback and outbound has a 15-month payback, the blended average hides the problem and encourages overspending in the wrong place.

Practical rule: if LTV:CAC looks strong but cash gets tighter each quarter, trust the payback analysis first.

Founders often defend long payback by saying growth takes patience. That argument falls apart when the company needs outside cash to finance every new dollar of ARR. Profitable growth is not about booking revenue at any cost. It is about recovering acquisition spend fast enough to fund the next round of growth without choking the business.

Beyond Revenue The Rule of 40 and Burn Multiple

You need two investor-grade lenses after you've cleaned up recurring revenue and unit economics. The Rule of 40 tells you whether growth and profitability are balanced. Burn Multiple tells you how much cash you're spending to create new ARR.

These aren't vanity metrics. They shape valuation, fundraising conversations, and whether your operating model looks disciplined or reckless.

How to apply the Rule of 40 correctly

According to The SaaS CFO's Rule of 40 guidance, the Rule of 40 is met when annual growth rate plus EBITDA margin equals 40 or higher. The article gives a clean example: 30% annual growth plus 10% EBITDA margin equals 40.

That sounds simple, but hybrid revenue models create confusion.

If you have subscription revenue plus onboarding fees, implementation, or consulting services, don't throw everything into the same bucket and call it a Rule of 40 score. The reason is straightforward. Non-recurring revenue can inflate the appearance of profitability, especially if services work carries different cost structure or timing.

Axial's discussion of key SaaS metrics points out that hybrid and vertical SaaS companies often misapply the Rule of 40 because EBITDA can be distorted by onboarding fees or implementation services. That's exactly right. For internal management and for investor conversations, calculate your growth and profitability on the recurring business first, then separately show how services affect total company results.

Use this comparison:

| Revenue model | Better Rule of 40 approach |

|---|---|

| Pure subscription SaaS | Use recurring revenue growth and EBITDA margin directly |

| Hybrid SaaS plus services | Isolate recurring revenue performance, then show services separately |

| Vertical SaaS with setup-heavy deals | Strip out one-time revenue effects before presenting the score |

Burn Multiple is the investor reality check

Burn Multiple is brutally clear. It asks one question: how much net burn did it take to generate net new ARR?

According to Klipfolio's SaaS benchmark summary, the target Burn Multiple is less than 1x, 1x to 2x is generally acceptable, and above 2x signals a severe cash burn problem.

Use the article's worked math:

- Net burn: $500k

- Net new ARR: $400k

- Burn Multiple: $500k / $400k = 1.25x

That falls in the acceptable range.

Now the red-flag version:

- Net burn: $800k

- Net new ARR: $400k

- Burn Multiple: $800k / $400k = 2.0x

That is a warning signal.

If you need a tighter operating grasp on cash pressure underneath this metric, keep a burn rate and runway calculation framework in your monthly reporting pack.

Burn Multiple strips away storytelling. It shows whether your revenue engine justifies the cash it consumes.

Founders often push back here and say, “We're investing aggressively.” Fine. Then prove the investment is efficient. Burn without conversion is not strategy. It's drift.

How to Measure and Reconcile Your Metrics

The biggest reporting problem in growing SaaS companies isn't formula design. It's data discipline.

Organizations already have the raw inputs somewhere. Stripe holds billing events. QuickBooks or Xero holds the accounting record. Your CRM tracks customer starts and expansions. The problem is that these systems don't agree automatically, and founders often accept near-enough numbers until diligence starts.

Where the numbers should come from

Use the billing system to identify subscription movements. Use the accounting system to tie those movements back to recognized revenue, cash, deferred revenue, and expense classifications.

A practical setup looks like this:

- Stripe or your billing platform for subscription plan changes, invoice activity, renewals, downgrades, and churn events.

- QuickBooks, Xero, or NetSuite for the general ledger, deferred revenue, expense mapping, and month-end close.

- CRM for acquisition source, customer start date, and expansion ownership.

- Payroll and HR systems for sales and marketing compensation inputs that feed CAC.

You also need reporting flexibility. Scheduled monthly dashboards are necessary, but they aren't enough during pricing changes, churn spikes, or fundraising prep. This piece on how ad hoc reporting boosts growth is useful because it captures why one-off analysis matters when the business changes faster than your standard report cycle.

SaaS metric data source and reconciliation cadence

| Metric | Primary Data Source(s) | Reconciliation Frequency |

|---|---|---|

| MRR | Stripe, billing platform, CRM | Monthly |

| ARR | MRR schedule, billing platform, general ledger | Monthly |

| Churn and contraction | Billing platform, CRM | Monthly |

| NRR | MRR movement schedule, CRM, billing platform | Monthly |

| CAC | General ledger, payroll, CRM | Monthly |

| Rule of 40 inputs | General ledger, management reporting | Monthly and quarterly |

| Burn Multiple | Cash flow report, ARR bridge, general ledger | Monthly |

The process that keeps numbers credible

Run this sequence every month:

- Lock customer movement first. Confirm new, expansion, downgrade, and churn events in the billing system.

- Build the recurring revenue bridge. Create the monthly MRR waterfall before you touch the board deck.

- Tie to the ledger. Reconcile billed amounts, cash received, deferred revenue, and recognized revenue in QuickBooks or Xero.

- Recalculate acquisition metrics. Pull actual sales and marketing spend from the books, not budget.

- Review anomalies manually. Big credits, contract restructures, plan migrations, and write-offs need human review.

The founder shortcut is to export a Stripe report and call it done. Don't. Stripe shows billing behavior. Your books show financial truth. You need both.

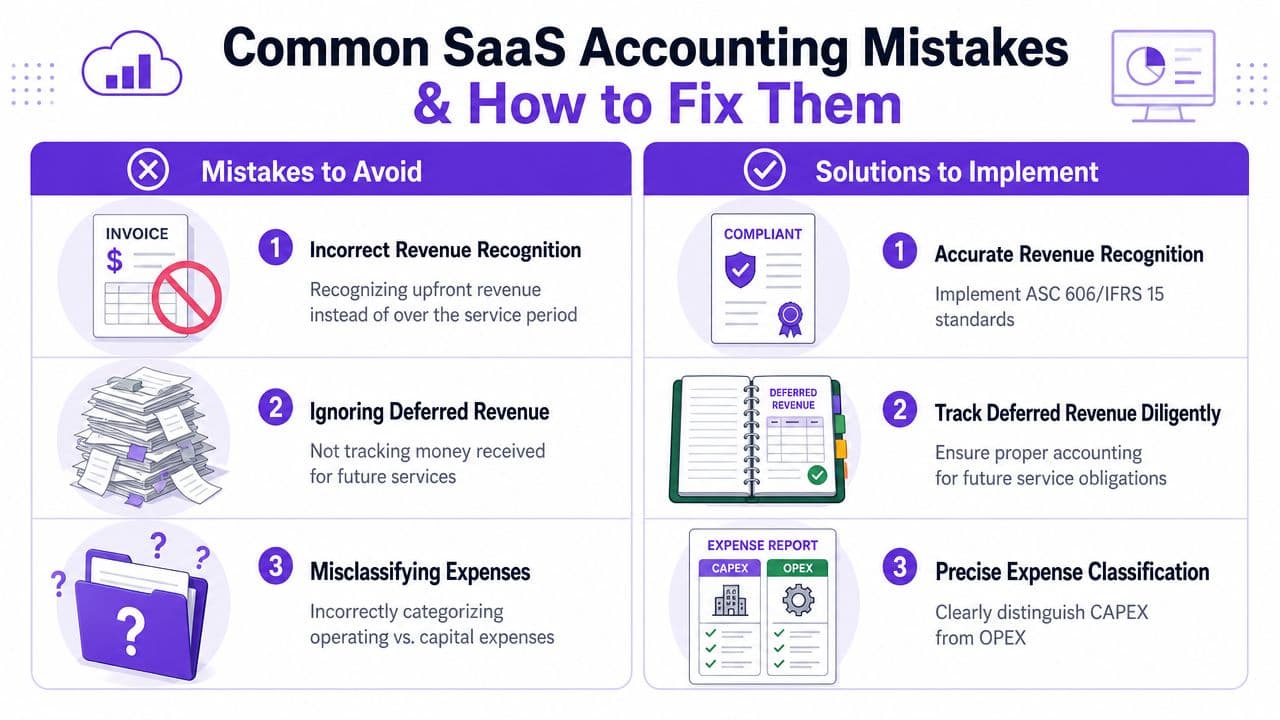

Common SaaS Accounting Mistakes and How to Fix Them

Most bad SaaS reporting isn't caused by fraud. It's caused by shortcuts that become habits.

Those habits create due diligence pain fast. Your dashboard says one thing, your books say another, and nobody can explain the difference. That's when investors start discounting everything you tell them.

The errors that wreck credibility

Here are the common ones.

-

Problem: pulling one-time fees into MRR. Onboarding, setup, migration, and project fees do not belong in recurring revenue.

The fix: create separate revenue categories for recurring subscriptions, non-recurring services, and implementation. -

Problem: recognizing annual contracts upfront. Cash collection is not revenue recognition.

The fix: defer the unearned portion and recognize it over the service period. -

Problem: under-reporting cost of service. Hosting, support, and delivery tools often get buried in operating expense when they belong in direct cost analysis.

The fix: define a consistent cost policy and apply it every month. -

Problem: using a fantasy LTV. If your LTV model ignores churn shifts, pricing changes, or discounting, it will overstate value.

The fix: use LTV cautiously and lean harder on cash-oriented efficiency metrics.

A practical cleanup checklist

A clean-up project should include:

| Mistake | Immediate correction |

|---|---|

| Revenue timing errors | Rebuild deferred revenue schedules |

| Inflated MRR | Remove all non-recurring items from the recurring base |

| Weak cost mapping | Reclassify direct delivery costs consistently |

| Metric mismatch across systems | Create one monthly KPI package tied to the ledger |

If your business includes agency or service revenue alongside recurring contracts, this guide to ASC 606 compliance for agencies is a useful reference point because the same timing issues show up there too.

Bad accounting doesn't just create messy books. It creates bad decisions because leadership starts steering off distorted numbers.

Once the cleanup is done, protect it with a monthly close checklist and a recurring revenue reconciliation. Otherwise the same errors come back.

When and How to Outsource Your SaaS Financial Stack

Founders usually outsource finance too late. By the time that becomes obvious, cash reporting is slow, board decks need manual repairs, and nobody trusts the same CAC payback number twice.

For a SaaS company in the $500K to $20M range, finance stops being an admin task the moment your decisions depend on cash efficiency instead of vanity ratios. Investors will glance at LTV:CAC, but they will spend real time on CAC payback, burn multiple, revenue quality, and whether your numbers reconcile to the ledger. If your reporting cannot answer those questions cleanly, you have a finance stack problem.

The signs you've outgrown founder-led finance

You should outsource finance when these problems show up:

- The close is too slow to be useful. If you get last month's numbers halfway through this month, you are managing by hindsight.

- Your KPI pack changes depending on who built it. MRR, ARR, deferred revenue, CAC payback, and cash burn should tie out every month.

- You are raising capital or entering diligence. Investors will test retention, payback, burn multiple, and revenue recognition fast. If every metric needs a caveat, they will discount the story.

- You run a hybrid model. Subscription revenue plus services revenue creates more judgment calls around margin, Rule of 40, and revenue timing.

- The founder is still the process owner. If you are the only person who understands billing logic, commission treatment, or forecast assumptions, the system is fragile.

As noted earlier, the valuation backdrop makes this more urgent. Lower multiples punish messy reporting harder because investors have less patience for adjustments and less room for benefit-of-the-doubt underwriting.

What to build at each stage

The right setup depends on stage, not ego.

- Around $500K in revenue. Get clean monthly books, separate recurring from non-recurring revenue, and build one KPI package tied to the general ledger. If you cannot trust MRR, every growth metric built on top of it is compromised.

- Around $2M in revenue. Add deferred revenue schedules, commission treatment, customer cohort reporting, CAC tracking by channel, and a forecast that includes cash runway. This is usually the point where a part-time controller or outsourced CFO starts paying for themselves.

- Around $5M to $10M and above. Build board-ready reporting, department budgets, hiring plans, scenario models, and monthly reporting on CAC payback and burn multiple. At this stage, investors expect clean answers, not finance archaeology.

Do not rush to hire a full in-house team if the business does not need one yet. Start with outsourced bookkeeping plus controller oversight, then add CFO-level support when fundraising, pricing changes, or burn management require better planning. That gives you decision-grade reporting without carrying a six-figure fixed cost too early.

The handoff matters as much as the hire. Set a monthly close calendar. Define metric owners. Write down revenue recognition rules, cost classification rules, and the exact formula for each KPI. If your outsourced team cannot explain how bookings become revenue, how cash burn becomes burn multiple, and why CAC payback changed month to month, keep looking.

If you want an outside read on whether your metrics, revenue recognition, and reporting stack are investor-ready, talk to Jumpstart Partners. Their team works with SaaS, agency, and services businesses in the $500K to $20M range to clean up books, tighten close processes, and build financial reporting you can use for decisions, fundraising, and diligence.