Financial Operations

SOC 2 Type II Compliance: A Founder's Guide for 2026

Your complete guide to SOC 2 Type II compliance. Learn the costs, timeline, and readiness steps to pass your audit and win enterprise deals. For SaaS founders.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readIf you sell into larger accounts, stop treating SOC 2 Type II as a security side quest. It's a revenue qualification issue. According to Gartner's 2024 Security Compliance Report, 78% of enterprise clients now require SOC 2 Type II before they'll engage a vendor, as cited by Metomic's summary of the report.

For founders and finance leaders in the $500K to $20M range, that changes the conversation. SOC 2 Type II compliance isn't about impressing auditors. It's about getting through procurement, reducing diligence friction, and showing buyers and investors that your controls function as intended in practice.

Table of Contents

- Why SOC 2 Compliance Is Now a Non-Negotiable

- What Is SOC 2 Type II and How Is It Different

- The 5 Trust Services Criteria Explained

- Your 9-Month SOC 2 Type II Readiness Timeline

- Budgeting for SOC 2 and Choosing an Auditor

- How Financial Processes Support Your SOC 2 Audit

- Your Next Steps Toward a Clean SOC 2 Report

Why SOC 2 Compliance Is Now a Non-Negotiable

78% of enterprise buyers now require SOC 2 Type II before they will fully engage a vendor. If you sell into larger accounts, this is a revenue gate, a finance issue, and a valuation issue.

Founders usually feel the pain in sales first. Procurement asks for the report. Legal pauses the contract. Security sends follow-up questions your team cannot answer with clean evidence. A competitor with a current Type II report moves ahead because the buyer can clear risk faster.

Treat SOC 2 as part of your go-to-market infrastructure.

A clean report shortens diligence, reduces friction in vendor review, and gives your sales team a document buyers already trust. It also signals that the company is run with discipline. That matters to investors. During fundraising or acquisition diligence, weak controls raise questions about revenue quality, data handling, contract enforceability, and management maturity. A clean SOC 2 report does the opposite. It supports the case that your operation can scale without breaking.

This is a finance and operations project, not just a security project

Too many founders hand SOC 2 to IT and expect a fast audit. That approach fails because auditors test how the business operates. They look at approvals, access reviews, onboarding and offboarding, vendor management, incident response, change control, and evidence retention. Several of those controls sit with finance and operations, not engineering.

If your close process is sloppy, customer billing is inconsistent, access changes are undocumented, or vendor approvals happen in Slack with no audit trail, you create audit exceptions and buyer doubt. Finance leaders should own part of this work because processing integrity starts with disciplined records, clear approvals, and repeatable workflows. If your basics need work, tighten them now. Strong operational hygiene starts with reliable bookkeeping and documented processes, which is why founders often need to review their startup bookkeeping services before the audit starts.

The companies that get through SOC 2 cleanly do the boring work early

They define ownership. They document who approves what. They keep evidence in one place. They fix gaps in HR, finance, and vendor management before the auditor arrives.

One overlooked example is data handling. Security teams focus on tools, but auditors also want to see that the business knows what data it holds, who can access it, and how it should be handled. That is why implementing a data classification policy is not just a security exercise. It affects contract reviews, employee training, finance system access, and retention practices across the company.

The bottom line is simple. If enterprise sales, fundraising, or strategic diligence matter this year, SOC 2 Type II belongs on the company operating plan, with executive ownership, budget, deadlines, and cross-functional accountability.

What Is SOC 2 Type II and How Is It Different

SOC 2 Type II is an independent attestation that your controls were not only designed appropriately, but also operated effectively over time. The framework was developed in 2010 by the AICPA and evaluates controls across Security, Availability, Processing Integrity, Confidentiality, and Privacy, according to HIPAA Journal's explanation of SOC 2. Security is the only mandatory criterion for every SOC 2 report.

Type I is design and Type II is proof

Use a simple mental model.

Type I is the blueprint. It shows your controls are designed at a specific point in time.

Type II is the operating record. It shows those controls were effective over an audit period.

That difference matters because buyers don't care that you wrote a policy. They care that you followed it, logged it, reviewed it, and can prove it.

| Attribute | SOC 2 Type I | SOC 2 Type II |

|---|---|---|

| Audit focus | Control design at a point in time | Design and operating effectiveness over time |

| Buyer confidence | Limited | Higher |

| Best use | Early readiness signal | Enterprise procurement and deeper diligence |

| Evidence burden | Lower | Higher |

| Commercial value | Often temporary | Usually what serious buyers want |

What buyers actually care about

For a buyer, Type I says, “We built the controls.” Type II says, “We ran them consistently.”

That's why founders should stop asking whether Type I is enough in the abstract. The key question is whether your target customers accept it. In many enterprise buying environments, they don't.

A Type II audit is also performed by a licensed CPA firm, not by a freelance consultant or a self-attestation process. Your auditor wants evidence. Screenshots, access reviews, ticket histories, policy acknowledgments, training records, change logs, and system configurations all matter. If your team doesn't already maintain a reliable audit trail, you'll feel the pain immediately.

A clean SOC 2 Type II report tells the market that your company can execute controls repeatedly, not just describe them convincingly.

The practical takeaway is simple. Don't over-scope the audit, but don't under-scope your credibility either. Start with the promises you make to customers, then map those promises to the right Trust Services Criteria.

The 5 Trust Services Criteria Explained

SOC 2 Type II compliance gets easier when you stop thinking in audit language and start thinking in customer promises. What do you promise clients about security, uptime, accuracy, confidentiality, and personal data handling? Your selected criteria should match those promises.

Security is mandatory

The only mandatory Trust Services Criterion is Security, also called Common Criteria. It requires core technical controls such as role-based access control with least privilege, encryption for data at rest and in transit, and multi-factor authentication for all infrastructure access, according to Aikido's SOC 2 framework overview.

For a SaaS company, this is the foundation. Auditors want to see who has access, why they have it, how it's reviewed, and whether privileged access is protected.

A few controls matter repeatedly:

- RBAC with least privilege: Engineers, support staff, and finance users shouldn't all have the same rights.

- MFA everywhere it matters: Administrative access without MFA is an avoidable problem.

- Encryption in transit and at rest: You need both the control and the evidence.

- Access review records: Auditors don't accept “we review access” without logs, tickets, or approvals.

If duties are mixed carelessly across teams, you create both security and finance risk. This guide to segregation of duties is worth reviewing before you lock your control matrix.

How to choose the optional criteria

The other four criteria are optional, but they're not cosmetic.

| Trust Services Criterion | What it means in practice | Example for a growing company |

|---|---|---|

| Availability | Systems are available as committed | Your app uptime commitments and incident response |

| Processing Integrity | Processing is complete, valid, accurate, timely, and authorized | Billing logic, reporting outputs, workflow accuracy |

| Confidentiality | Sensitive information is restricted and protected | Client files, internal pricing, customer lists |

| Privacy | Personal information is handled according to commitments | User consent, retention, deletion, notice practices |

For Availability, include it if your contracts, SLAs, or customer expectations make uptime part of your product promise.

For Processing Integrity, include it if customers rely on your platform to calculate, route, transform, or report data correctly. This matters more than many founders realize.

For Confidentiality, think beyond vague “we protect data” language. In a multi-tenant SaaS environment, you need controls that separate and protect customer data. Data segmentation, restricted access, and documented handling rules all matter. If your team hasn't done the basics, start with implementing a data classification policy. It forces clarity about what data is sensitive, who can touch it, and how it should be protected.

For Privacy, only include it if you make explicit commitments about personal information handling and can support them operationally.

Don't select all five criteria to look mature. Select the ones you can defend with evidence and that align with what you actually sell.

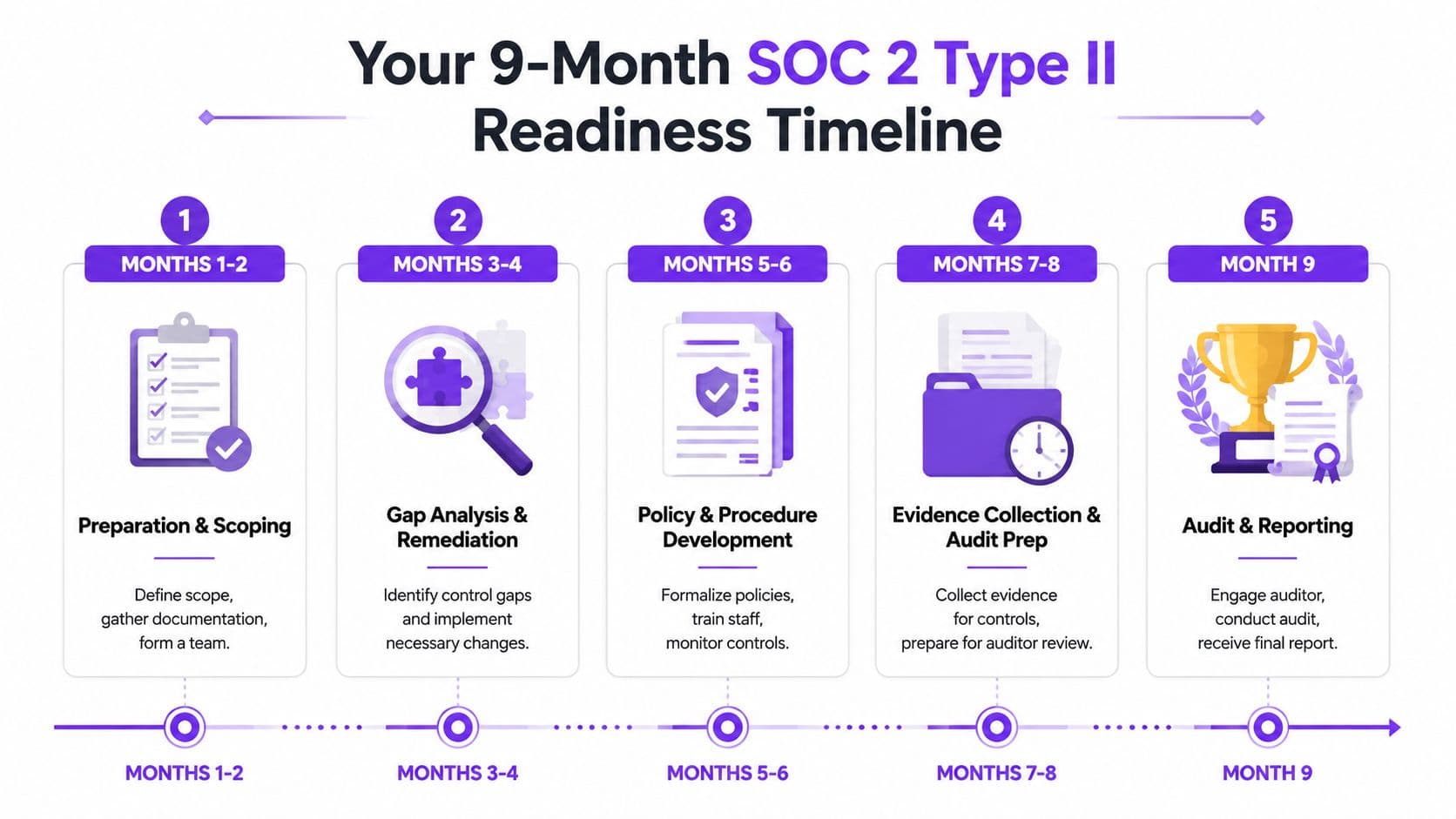

Your 9-Month SOC 2 Type II Readiness Timeline

Most founders underestimate the calendar. They assume the audit starts when they hire the auditor. It doesn't. The hard part starts earlier, when you're building controls and collecting evidence that those controls are operating.

SOC 2 Type II requires you to prove controls operated effectively over a minimum review period of six months, while Type I only covers a point in time, according to Cobalt's SOC 2 guide. That six-month period is the constraint that drives your project plan.

Here's the timeline in one view.

Months 1 and 2 scope the system and find the gaps

Start by defining scope. Which systems are in scope, which teams own them, and which Trust Services Criteria are you pursuing?

Then run a gap analysis. Look at access controls, onboarding and offboarding, vendor management, incident response, device management, logging, backups, change management, and policy coverage. Don't start the observation period while controls are still half-built.

Use this phase to assign owners clearly:

- Security owner: Access, endpoint, infrastructure, and monitoring controls

- Engineering owner: Change management, deployments, code review, and production restrictions

- People ops owner: Background checks, onboarding, offboarding, training acknowledgments

- Finance or operations owner: Billing workflows, approval chains, audit evidence retention

- Executive owner: Budget, deadlines, and cross-functional accountability

If your team needs a practical checklist for assembling records before external review, this audit preparation checklist is a strong starting point.

Months 3 through 9 build evidence before the audit

Once your controls are live, the observation clock starts. That's when your team needs consistency.

A workable founder-level roadmap looks like this:

| Phase | What your team should do | What to avoid |

|---|---|---|

| Preparation and scoping | Define systems, criteria, and owners | Scoping everything “just in case” |

| Remediation | Fix access, policy, and logging gaps | Starting evidence collection before controls are stable |

| Observation period | Run controls consistently and save proof | Manual processes with no owner |

| Audit fieldwork | Respond quickly and accurately to requests | Debating what the policy meant after the fact |

Here's a concrete schedule using the required six-month period. If you begin remediation in January, stabilize controls by March, and begin the observation period in April, your six months run through September. Audit testing and report drafting then follow. That's why a “we need SOC 2 next quarter” request is usually unrealistic unless the groundwork already exists.

The six-month clock starts after the controls work, not when you announce the initiative to the board.

Budgeting for SOC 2 and Choosing an Auditor

Founders usually ask the wrong budgeting question. They ask, “What does the auditor charge?” The better question is, “What will this project cost the business from first gap assessment to final report?”

According to Linford & Co., Type II audits can exceed $80,000 with total costs surpassing $145,000. That total matters more than the audit invoice because remediation, tooling, and internal labor often drive the pain.

What the budget really looks like

For a $5M ARR SaaS company, use the verified ceiling numbers as a planning anchor, not a fantasy lowball.

Here's a worked budgeting frame with real numbers you can use:

| Budget line | Example amount |

|---|---|

| External audit fees | $80,000 |

| Additional remediation, tooling, internal support, and project costs | $65,000 |

| Total program budget | $145,000 |

That arithmetic is straightforward. $80,000 + $65,000 = $145,000.

A second calculation matters just as much. If a clean report requires spending 20% extra, the math on a $145,000 program is $29,000 more, bringing the total to $174,000. If it requires 30% extra, that is $43,500 more, bringing the total to $188,500. That doesn't mean you should spend blindly. It means you should compare the extra spend to the cost of exceptions showing up in customer diligence or fundraising.

Another practical calculation: if audit fees are $80,000 out of a $145,000 total, the non-audit portion is $65,000. That means the auditor's invoice is only part of the story. The rest sits inside your systems, people time, and remediation backlog.

Red flags when choosing an auditor

Not every CPA firm is a fit for a software or services business. Ask direct questions and listen for direct answers.

- Weak sector experience: If the firm can't explain SaaS architecture, cloud tooling, or multi-tenant risk in plain language, move on.

- Guaranteed pass language: A real auditor doesn't guarantee outcomes.

- Vague evidence standards: If they can't tell you what evidence they typically expect, you'll pay for confusion later.

- No explanation of exceptions: You need a firm that can explain findings clearly, not bury them in jargon.

- Poor project discipline: Slow communication during scoping becomes painful during fieldwork.

A founder should also know who is allowed to perform the work. SOC 2 audits are done by CPA firms, not generic compliance advisors. If you want a primer on the broader auditor selection process, this article on auditing a business helps frame the diligence questions.

How Financial Processes Support Your SOC 2 Audit

SOC 2 Type II compliance is not just an IT control exercise. It reaches directly into finance operations.

That connection is often missed, which is a mistake. There is a documented gap in explaining how Processing Integrity and data classification support financial accuracy and workflows such as ASC 606 revenue recognition, as described by Optro's SOC 2 framework guide.

Processing integrity starts in finance operations

If your billing data changes without approval, your revenue schedules shift without review, or your customer records are edited without logs, you have more than an accounting issue. You have a control issue.

Auditors look for evidence that important business processes are controlled, repeatable, and traceable. In finance, that often includes:

- Revenue recognition workflows: Who approves contract terms, who enters data, and how changes are logged

- Billing system change management: What changed, who approved it, and when it went live

- Restricted access to payroll and financial systems: Not everyone needs admin rights in QuickBooks, Xero, Stripe, or NetSuite

- Documentation retention: Policies, approvals, reconciliations, and issue resolution records

What your finance stack should already document

A disciplined finance function generates useful audit evidence naturally. A weak one creates panic at evidence-request time.

For example, if your controller can show documented close procedures, reconciliation sign-offs, role-based permissions in financial systems, and approval trails for contract or pricing changes, you're in a stronger position. If your records live in inboxes and memory, you're not.

Clean financial operations often give you some of the best evidence for Processing Integrity because they show how data moves, who approves it, and how errors are caught.

If your team needs a plain-English checklist mindset for retaining records and support materials, Reworx Recycling's audit documentation guide is a helpful operational reference, even outside formal compliance contexts.

Your Next Steps Toward a Clean SOC 2 Report

The founders who handle SOC 2 well treat it like a company-wide operating project with revenue implications. The ones who handle it poorly treat it like an isolated security task and then wonder why audits drag and deals stall.

Narendra Sahoo put it clearly: “SOC 2 is no longer optional in 2025 for SaaS companies targeting enterprise clients because it builds trust, reduces breach risk, and streamlines sales cycles”, as quoted in his LinkedIn article on SOC 2 for SaaS.

Do these three things next:

- Define your scope. Pick the Trust Services Criteria that match the promises you make to customers.

- Run a real gap analysis. Identify missing controls, missing evidence, and weak ownership before the clock starts.

- Prepare your financial controls first. Revenue recognition, billing changes, approvals, access rights, and documentation discipline should be tight before you hire the auditor.

A clean report doesn't start with fieldwork. It starts with operational maturity.

Before you hire an auditor, ensure your financial controls are ready. Jumpstart Partners helps growing companies tighten close processes, document key workflows, and build the financial control foundation that makes SOC 2 readiness far less painful. Let's talk.