Financial Operations

What Is Your Cost of Debt? A Founder's Guide to Lowering It

Learn to calculate your pre-tax and after-tax cost of debt with real examples. Discover how it impacts valuation and how to lower it for your business.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··15 min readYour debt isn't just a financing tool. It's a valuation input, a diligence signal, and a tax-adjusted cost that follows you into every major decision.

That's not abstract finance talk. In the U.S., debt service has grown large enough to compete with major budget priorities. Treasury data shows gross national debt reached $34.4 trillion by February 2024 after rising from $10.3 trillion at the end of FY 2008, and the Congressional Budget Office projected debt held by the public would rise from 99% of GDP in 2024 to 116% in 2034, and potentially 172% by 2054 under current law. By July 2023, annualized servicing costs were $726 billion, or 14% of total federal spending, and in 2024 federal interest payments surpassed spending on both Medicare and national defense, according to the U.S. Treasury historical debt record and related federal projections. If debt cost can reshape federal priorities at that scale, it absolutely affects your company's flexibility at founder scale.

For SaaS companies, agencies, and professional services firms, the mistake is usually the same. You treat debt as a line item on the P&L instead of a lever that changes valuation, cash flow, and negotiating power.

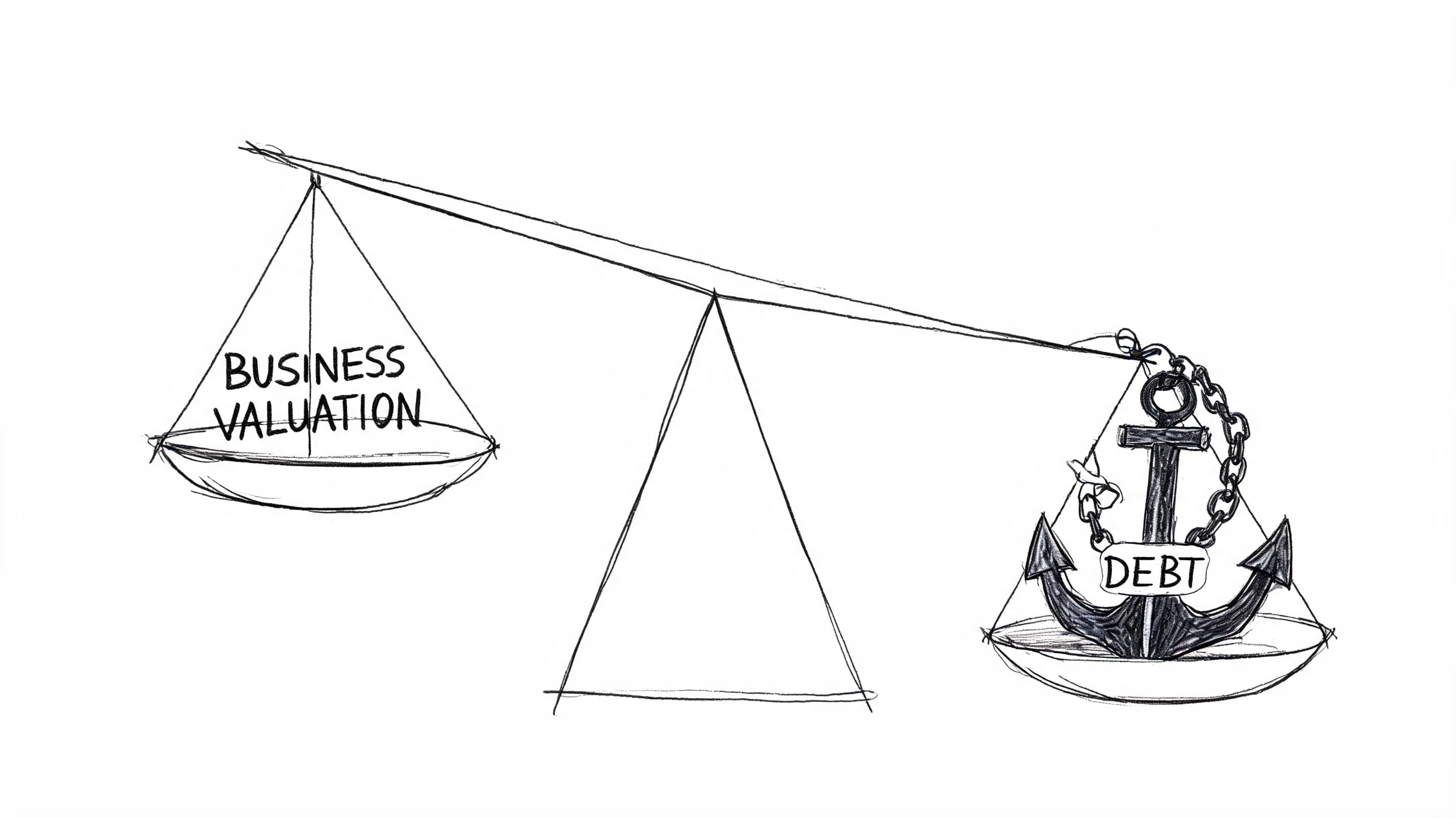

Your Cost of Debt Is Hurting Your Valuation

If you're raising capital, preparing for an acquisition, or trying to refinance, your cost of debt is already part of the conversation, whether you track it or not.

A founder usually looks at debt and asks one question: “What's the rate?” Investors and lenders ask a different one: “What does this debt say about risk?” That second question is the one that affects your multiple.

Why lenders and buyers care

Debt with a high true cost signals weak control somewhere in the business. Maybe collections are slow. Maybe gross margins are unstable. Maybe reporting is late and lenders are pricing uncertainty into the deal. Whatever the cause, the result is the same. Risk goes up, flexibility goes down, and your valuation takes the hit.

That matters even more if you're a founder who expects the next round, recap, or sale process to reward growth alone. It won't. Buyers and investors also price operational discipline. If your financing structure looks messy, they assume the rest of the finance function may be messy too.

Practical rule: If you can't explain your cost of debt in plain English, a buyer will assume you're not managing it.

The damage goes beyond interest expense

Your cost of debt feeds directly into your overall cost of capital. That means it affects how future cash flows are valued. If debt becomes more expensive because your credit profile weakens, the hurdle rate on future decisions rises too. Suddenly a once-attractive expansion plan, acquisition target, or hiring push doesn't clear the bar.

This is why I push founders to treat debt as a strategic metric, not just an accounting output. The same company can look disciplined and financeable, or chaotic and expensive, depending on how well it understands its debt stack.

If you're already thinking about transaction readiness, this connects directly to broader startup valuation work. Your debt cost won't determine the whole number, but it absolutely influences how discerning counterparties judge the business behind the number.

How to Calculate Your Real Cost of Debt

Most founders overcomplicate this, then give up and default to the note rate from the loan agreement. That's sloppy.

The technically preferred method is yield to maturity on your existing debt because it reflects current market pricing, credit risk, and rate conditions. When you don't have market debt data, practitioners commonly estimate pre-tax cost of debt using annual interest expense divided by total debt, and calculate after-tax cost as pre-tax cost × (1 – tax rate), as explained in Wall Street Prep's guide to cost of debt calculation methods.

The formulas you actually need

Use these:

- Pre-tax cost of debt = Annual interest expense ÷ Total debt

- After-tax cost of debt = Pre-tax cost of debt × (1 – tax rate)

That's the clean version. Your real job is making sure the inputs are right. Pull debt balances from your balance sheet. Pull actual interest expense from the P&L. Don't mix annual figures with monthly balances. And don't forget that fees, line utilization patterns, and short-term borrowing pressure can make the headline rate misleading.

If you need a practical companion on how to figure out true borrowing costs, that resource does a good job translating loan language into operating reality.

Sample Cost of Debt Calculations

Below are two worked examples using the approved calculation method. These are examples to show the mechanics. Use your own financial statements for the final number.

| Step | SaaS Co (Term Loan) | Digital Agency (Line of Credit) |

|---|---|---|

| Debt balance | $500,000 term loan | $500,000 line of credit balance |

| Annual interest expense | $27,000 | $27,000 |

| Pre-tax cost of debt | $27,000 ÷ $500,000 = 5.4% | $27,000 ÷ $500,000 = 5.4% |

| Marginal tax rate assumption | Example tax rate selected by the company | Example tax rate selected by the company |

| After-tax cost of debt formula | 5.4% × (1 – tax rate) | 5.4% × (1 – tax rate) |

| What to review next | Covenants, amortization, refinancing windows | Draw timing, fees, reporting requirements |

SaaS example with simple math

Say your SaaS business borrowed $500,000 for infrastructure and related growth investments. Over the year, your income statement shows $27,000 of interest expense.

Your pre-tax cost of debt is:

$27,000 ÷ $500,000 = 5.4%

Now apply your company's marginal tax rate:

After-tax cost of debt = 5.4% × (1 – tax rate)

If you don't know your marginal tax rate, don't guess from your effective tax rate on last year's return. Ask your CPA or finance lead for the actual marginal rate used in planning. For WACC and capital budgeting, that distinction matters.

Your lender prices risk today, not the story you told six months ago. Use current balances and current interest expense.

Agency example with a line of credit

Now take a digital agency that uses a revolving line to bridge payroll while waiting on client collections. Same debt balance. Same annual interest expense. Same arithmetic.

$27,000 ÷ $500,000 = 5.4% pre-tax cost of debt

But this agency's real borrowing profile may be more fragile than the SaaS company's, even with the same calculated rate. Why? Because revolvers often come with utilization pressure, tighter monthly reporting, and exposure to working capital swings. If a few clients pay late, the agency leans harder on the line. That changes the practical burden of the debt even if the formula output looks identical.

That's why I tell founders to calculate the number, then interrogate the structure.

Where founders get this wrong

A few mistakes show up constantly:

- Using the coupon rate only. That ignores what the market says your debt costs now.

- Using average debt loosely. Pull the actual debt figure that matches the period of interest expense.

- Ignoring the balance sheet. If you can't reconcile debt cleanly, your calculation is already compromised. Use a tight balance sheet review process before you trust the answer.

- Skipping fees and restrictions. The formula gives you the accounting cost. It does not capture the whole operating burden.

The formula is easy. The discipline to use accurate inputs is where founders separate themselves.

Why This Number Shapes Your Company's Future

A lot of finance content stops after the formula. That misses the point.

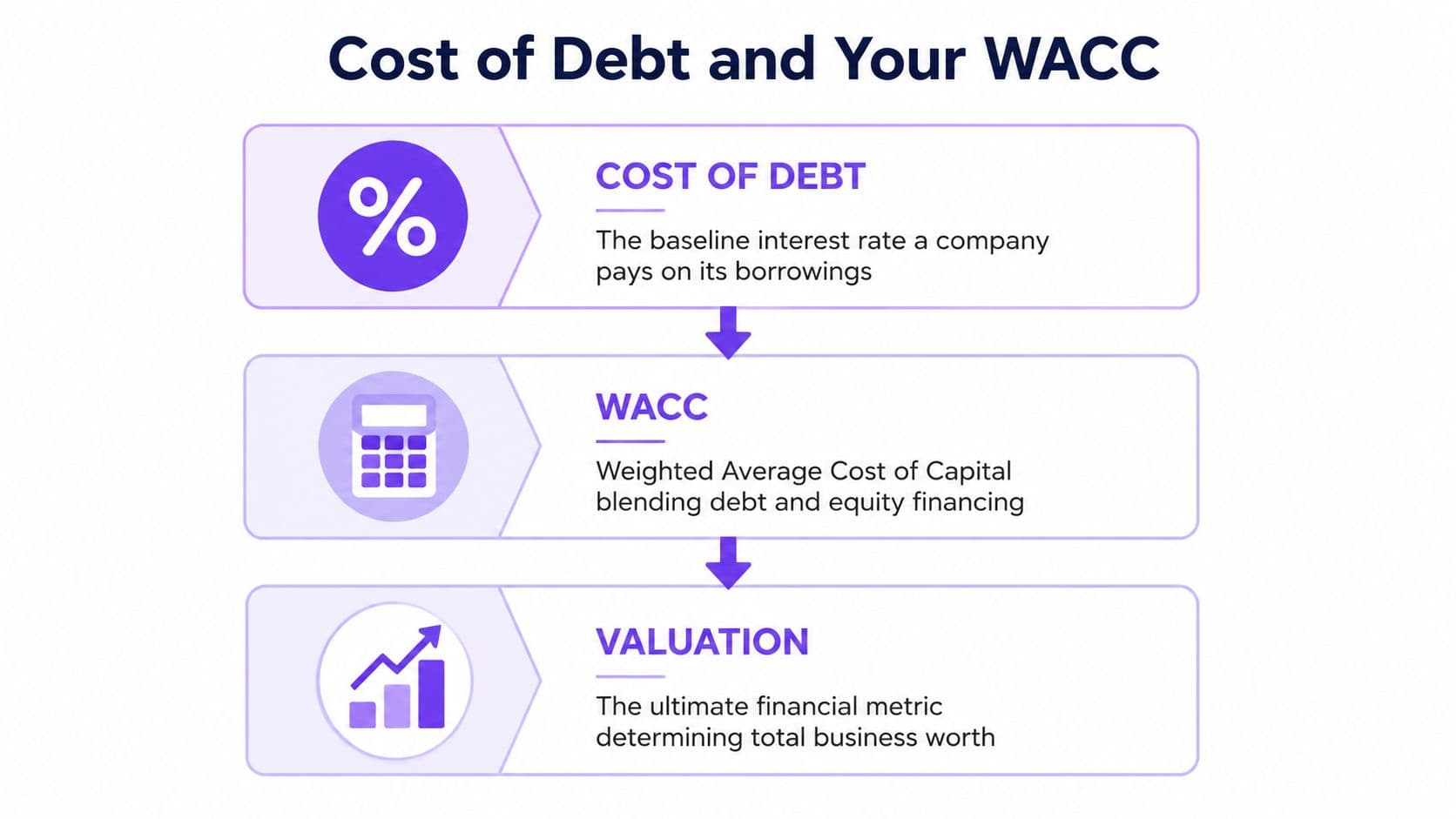

Your cost of debt matters because it becomes part of WACC, and WACC is one of the core inputs behind valuation and capital allocation. If your debt cost rises, your hurdle rate rises. If your hurdle rate rises, fewer projects create value.

WACC is where debt stops being a line item

For valuation and capital budgeting, cost of debt should use the marginal tax rate, not the effective tax rate, because the marginal rate better captures the incremental tax shield in WACC. NYU Stern also notes that borrowing cost should reflect a bond rating plus a default spread over the risk-free rate, which makes it sensitive to both market rates and issuer-specific credit risk, as shown in Aswath Damodaran's valuation materials.

That means two businesses can have the same stated loan rate and still have very different true financing costs in a valuation model. One has clean financials, predictable cash flow, and stronger credit quality. The other has missed forecasts, covenant pressure, and messy monthly closes. Lenders and investors don't treat those companies the same, and they shouldn't.

What this changes in practice

When your cost of debt is high or unstable, you feel it in decisions like these:

| Decision area | What a higher cost of debt signals | Founder consequence |

|---|---|---|

| Fundraising | More perceived financial risk | Harder diligence and weaker negotiating leverage |

| Budgeting | Tighter cash coverage needs | Less room for hiring or growth bets |

| Acquisitions | Higher hurdle rate | More deals fail the return test |

| Forecasting | Greater sensitivity to misses | Smaller margin for error in planning |

The point isn't that debt is bad. The point is that expensive debt shrinks your options.

A lender isn't just evaluating repayment. They're evaluating whether your numbers are stable enough to trust.

Investors read this as a management signal

Knowledgeable investors examine debt structure because it reveals how you run the business. If you know your cost of debt, can explain the drivers, and can show a clean forecast around it, you look controlled. If you hand-wave through it, they assume surprises are hiding somewhere else too.

That's why cost of debt belongs inside your regular planning rhythm, not buried in annual cleanup. It should show up in cash planning, board materials, and scenario analysis. If you're building a forward-looking model, this belongs alongside the rest of your startup financial forecasting process.

Warning The Hidden Costs Beyond the Interest Rate

The interest rate is only the visible part of the bill.

Many borrowers face a larger all-in financing cost once hidden fees and spread are included. Research also shows the burden of debt can spill into other borrowing products, meaning a cheaper stated rate can still become more expensive if it tightens cash flow or access to other credit, according to this analysis of hidden borrowing costs and downstream effects.

The costs founders ignore

A term sheet can look cheap and still be expensive once you operate under it.

Here are the hidden costs I see most often:

- Covenant drag. If your agreement limits debt use, liquidity, or fixed-charge coverage, you lose flexibility. That can stop you from making sensible hires or taking on strategic spend.

- Management time. Monthly lender packages, covenant tracking, and exception reporting take real operator time. If your controller is scrambling every month, that has a cost.

- Refinancing friction. Short maturities and floating structures force you back into the market at the worst possible time.

- Credit spillover. One strained facility can make another lender more cautious, which raises the cost of future capital.

Warning signs in your debt stack

If any of these sound familiar, your cost of debt is probably understated:

| Red flag | Why it matters |

|---|---|

| You only track the note rate | You're missing fees, structure, and credit effects |

| You don't review covenant headroom monthly | Small misses turn into urgent lender conversations |

| Your close process is slow | Lenders interpret delayed reporting as risk |

| You depend on one revolver for routine payroll support | Cash conversion weakness is leaking into financing cost |

Cheap debt can make your operations worse

Founders often optimize for the lowest visible rate and ignore the operating constraints attached to it. That's backwards.

A slightly higher stated rate with cleaner terms can be cheaper in practice if it gives you room to manage working capital, fund growth, and avoid constant lender oversight. If your payable process is inconsistent, debt stress gets worse fast. Tightening your accounts payable process often lowers financing pressure before you ever renegotiate a facility.

The real question isn't “What rate did I get?” It's “What did I have to give up to get it?”

A Founder's Playbook to Lower Your Cost of Debt

You do not lower your cost of debt by begging the bank for mercy. You lower it by reducing the risk they see.

That starts inside the business. Better margins, cleaner reporting, tighter collections, and predictable forecasts all feed the same outcome. A lender sees less uncertainty and prices you accordingly.

What actually moves the number

Debt pricing is being repriced in the current higher-rate environment, and even a modest change in perceived credit risk can alter valuation and cash needs. One example shows that with a 4.2% risk-free rate and a 1.2% credit spread, the pre-tax cost of debt is 5.4%, which illustrates how quickly borrowing costs move with market conditions, as described in this overview of rate-driven debt pricing.

That gives you two levers. You can't control the risk-free rate. You can control the spread the lender adds for your company.

Here's the playbook I'd use with a founder:

- Clean up reporting first. If your books close late or require constant rework, fix that before you refinance.

- Stabilize cash conversion. Agencies should tighten receivables discipline. SaaS companies should watch burn, churn-related cash leakage, and contract timing.

- Negotiate structure, not just rate. Push on covenants, reporting burden, and maturity profile.

- Separate temporary debt from permanent debt. Don't use short-term borrowing to fund long-term holes.

- Review fixed versus floating exposure. If you carry variable debt, stress test it under a higher-for-longer scenario.

For a deeper operating view on strategies for managing interest rate risk, that resource is worth reviewing before you choose between fixed and floating structures.

How to walk into a lender meeting

Bring a tighter package than they expect:

- A current balance sheet and clean debt schedule

- A rolling cash forecast

- Covenant calculations with headroom clearly shown

- A short explanation of operational improvements already implemented

That changes the conversation. You stop sounding like a borrower asking for help and start sounding like an operator managing risk.

A lot of founders also benefit from outside finance support here. One option is fractional CFO services, especially when you need lender-ready reporting, covenant modeling, and refinancing prep without hiring a full-time executive.

A short explainer on debt strategy can help frame the discussion internally before you renegotiate:

Get the Financial Control You Need to Reduce Costs

You can't lower what you don't measure. If your debt schedule is outdated, your close is slow, and your lender reporting is assembled by hand, you're paying a risk premium whether the bank says it out loud or not.

Founders frequently encounter frustration at this stage. They want better debt terms, but they haven't built the finance discipline that earns them. Lenders reward visibility, consistency, and control. They punish surprises.

What lenders want to see

They want financials that reconcile cleanly. They want debt balances tied to the balance sheet. They want a forecast that explains where cash goes and how repayment fits inside the plan. And they want this information fast, not after a scramble.

"Founders often see debt as a simple transaction, but lenders see it as a relationship based on risk and data," says Sarah Jennings, CPA and Partner at Jumpstart Partners. "The companies that get the best terms are the ones who can produce audited-quality financials on demand. It proves you have control, and control is the inverse of risk."

That quote gets to the heart of it. The cheapest debt usually goes to the company that looks easiest to underwrite.

The move I recommend

If you're between $500K and $20M in revenue, stop treating finance cleanup as back-office admin. Make it part of your cost-reduction strategy.

Build a monthly process that does these things well:

- Close fast so debt balances, interest expense, and covenant metrics are current

- Track lender requirements before they become a problem

- Model cash flow so you can see refinancing pressure early

- Package financials clearly so banks, investors, and buyers trust the numbers

If you don't have in-house capacity, use an outsourced controller or CFO model. Jumpstart Partners provides outsourced controller and bookkeeping support for SaaS, agencies, and growing businesses, including investor-ready reporting, cash flow visibility, and lender-facing financial packages. The point isn't outsourcing for its own sake. The point is getting reliable numbers into your hands fast enough to improve financing decisions.

Debt gets cheaper when your business becomes easier to trust.

If you want help tightening your reporting, cleaning up your debt picture, and building lender-ready financials, talk to Jumpstart Partners. They work with growing SaaS, agency, and service businesses that need clearer cash flow, stronger controls, and better financial visibility before the next financing decision.