Financial Operations

Due Diligence Reports: An Investor-Ready Preparation Guide

Learn how to prepare investor-ready due diligence reports. Our step-by-step guide covers financials, SaaS metrics, red flags, and includes a checklist.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··18 min readMost advice on due diligence reports is backwards. It tells you to gather everything, upload everything, and wait for the buyer to ask questions. That approach slows deals, weakens credibility, and gives the other side control of the story.

A strong due diligence report isn't a document dump. It's a decision file. It should show why your business is worth the price, where material risks sit, what you've already done to manage them, and why the remaining risks are acceptable. LSEG's description of a due diligence report is useful here because it frames the report as a thorough, evidence-based review of ownership, financial health, legal obligations, regulatory exposure, and risk. That's a gatekeeping tool, not a Dropbox folder.

For founders in the $500K to $20M range, the practical challenge is simple. You're still running the company while someone else asks for board materials, revenue support, contracts, tax records, product documentation, employment files, and customer data all at once. If you prepare reactively, the process starts exposing weak close processes, inconsistent KPI definitions, and missing approvals. If you prepare strategically, the same process can support valuation.

Table of Contents

- Stop Collecting Documents and Start Building Your Narrative

- The Anatomy of an Investor-Ready Virtual Data Room

- Mastering the SaaS Financial Schedules Investors Scrutinize

- Running a Disciplined Due Diligence Process

- How to Find and Fix Red Flags Before They Kill Your Deal

- Your Investor-Ready Action Plan

Stop Collecting Documents and Start Building Your Narrative

Founders often assume due diligence reports should be exhaustive. That's the wrong standard. The right standard is whether the report gives a buyer enough evidence to validate the investment case and understand the downside.

A useful framing comes from Neotas on due diligence reports. It notes that experienced acquirers begin with a testable deal thesis and stress-test downside scenarios, rather than treating diligence as a box-checking exercise. That changes how you prepare. You don't go deepest everywhere. You go deepest where the transaction risk sits.

Lead with the deal thesis

If you're a SaaS company, your thesis may be recurring revenue durability, efficient expansion inside existing accounts, or a defensible niche with low implementation friction. If you're an agency, it may be client retention, margin quality, and a bench that doesn't depend on one founder. If you're a professional services firm, it may be contract renewability and delivery consistency.

Your due diligence report should support that thesis with evidence.

Practical rule: If a buyer can't tell within the first few pages why your business is attractive, they'll spend the rest of diligence looking for reasons to discount it.

That means your executive summary shouldn't read like an index. It should answer four questions:

-

Why this business now

Show the commercial logic. Explain what's working and why it's repeatable. -

What are the core risks

Name them directly. Customer concentration, founder dependence, contract gaps, security controls, or margin volatility. -

What have you already fixed

Buyers trust businesses that identify their own flaws before someone else does. -

What remains open and manageable

Not every issue must be resolved before diligence starts. But every issue needs an owner, a status, and a plan.

Founders who want a cleaner starting point should also tighten their recurring reporting before the process begins. A buyer's first impression often comes from the same materials your board or investors already review. If those materials are thin or inconsistent, start by improving your startup investor reporting and board financials.

Use a six-folder structure

Narrative without proof is spin. Proof without structure is chaos. Strong due diligence reports sit in the middle. They organize evidence so the buyer can verify your claims quickly, without forcing your team into endless clarification cycles.

The Anatomy of an Investor-Ready Virtual Data Room

A buyer starts forming a valuation view before the first diligence call. The data room is often the first hard evidence they see. If the room is disorganized, incomplete, or full of duplicate files, they assume the underlying controls are disorganized too.

That is why an investor-ready VDR needs to do more than store documents. It needs to show how ownership, financial performance, customer quality, legal exposure, and operating discipline fit together. A good room shortens review cycles. A bad one creates extra questions, wider reps and warranties, and more pressure on price.

Use a six-folder structure

| Folder | Key Documents | File Naming Example |

|---|---|---|

| Corporate | Certificate of incorporation, bylaws, board consents, shareholder agreements, cap table, entity structure | CORP_2026-01_Cap_Table.xlsx |

| Financial | Monthly financials, general ledger, bank statements, tax filings, AR aging, AP aging, deferred revenue schedules | FIN_2026-03_Monthly_Financials.pdf |

| Commercial | Top customer contracts, pipeline summary, pricing policies, renewal terms, customer concentration analysis | COMM_2026-Q1_Top_20_Customers.xlsx |

| Product & IP | Product roadmap, architecture overview, code ownership docs, trademark or patent records, security policies | IP_2026-02_Code_Assignment_Agreements.pdf |

| Team & HR | Org chart, offer letter templates, contractor agreements, bonus plans, handbook, retention plans | HR_2026-03_Org_Chart.pdf |

| Legal | Material contracts, litigation summary, compliance policies, privacy terms, insurance, regulatory correspondence | LEGAL_2026-01_Material_Contracts_Index.xlsx |

This layout works because it matches how deal teams divide the work. Legal counsel goes straight to authority, contracts, and exposure. Financial diligence teams test earnings, working capital, and revenue support. Commercial reviewers want to understand concentration, retention, and the terms behind reported sales. Product and HR materials answer a different question: can this business keep delivering after the deal closes?

For founders, the practical benefit is speed. A clear structure lets the buyer verify your story without dragging management into constant clarification calls.

Make file naming boring and consistent

Messy naming slows diligence more than founders expect. If the room includes files called final, final v2, and final approved, the buyer does not know which one to rely on. Then they ask for confirmations in writing, which costs time and introduces avoidable friction.

Use one naming pattern across the room:

[CATEGORY]_[YYYY-MM or YYYY-Q#]_[DOCUMENT_NAME].[filetype]

Examples:

- Board deck as

FIN_2026-Q1_Board_Deck.pdf - Sales tax filing as

FIN_2026-02_Sales_Tax_Return.pdf - MSA template as

LEGAL_2026-Standard_MSA_Template.pdf

Keep the names plain. Include dates. Mark drafts and executed versions clearly. If a contract is unsigned, say so in the file name or index. If a file has been replaced, archive the old version instead of leaving both active.

Teams cleaning up years of shared-drive sprawl usually get stuck at classification first, not naming. If you are sorting mixed PDFs, scans, and contracts before upload, this guide to classifying documents for creators is a useful operational reference for grouping files before you name and index them.

Add an index and retention logic

The strongest data rooms have a master index. It should list the file name, folder, owner, date range covered, approval status, and a short note if the item needs context. That note matters. For example, if a key customer contract is operating on an expired papered term but auto-renewed in practice, flag it and explain the status upfront. Silence makes it look hidden. Context makes it manageable.

Retention discipline matters too. Many companies either overload the room with stale material or leave obvious gaps across prior years. Both create work for the buyer and raise questions about process maturity. Before loading historical records, compare your archive against a clear business record retention approach so you know what belongs in the active room, what should stay in backup storage, and what should be excluded.

A clean VDR signals that management can produce support quickly, explain exceptions directly, and control the process under pressure.

A few operating rules make a measurable difference in practice:

-

Create a read-first folder

Include the executive summary, org chart, cap table, monthly financial package, KPI definitions, diligence request tracker, and any memo that explains known issues. -

Assign a clear owner to each folder

Finance should own Financial. Legal should own Legal. The CTO or product lead should own Product & IP. One person should still control final upload rights and version approval. -

Use status labels consistently

Mark files as draft, final, executed, or superseded. Buyers care about the difference. -

Explain exceptions in writing

Missing signatures, customer side letters, tax notices, and policy gaps should have a short cover note. The goal is to frame the issue before the buyer frames it for you. -

Set permissions deliberately

Some materials belong in a restricted folder until the process is serious enough. That usually includes employee compensation detail, sensitive customer pricing, and source code access.

The trade-off is straightforward. A heavily curated room takes more work up front, but it reduces noise, preserves credibility, and gives you better control over the narrative. Treating the VDR like a storage closet does the opposite. Buyers stop trusting the package before they finish reviewing it.

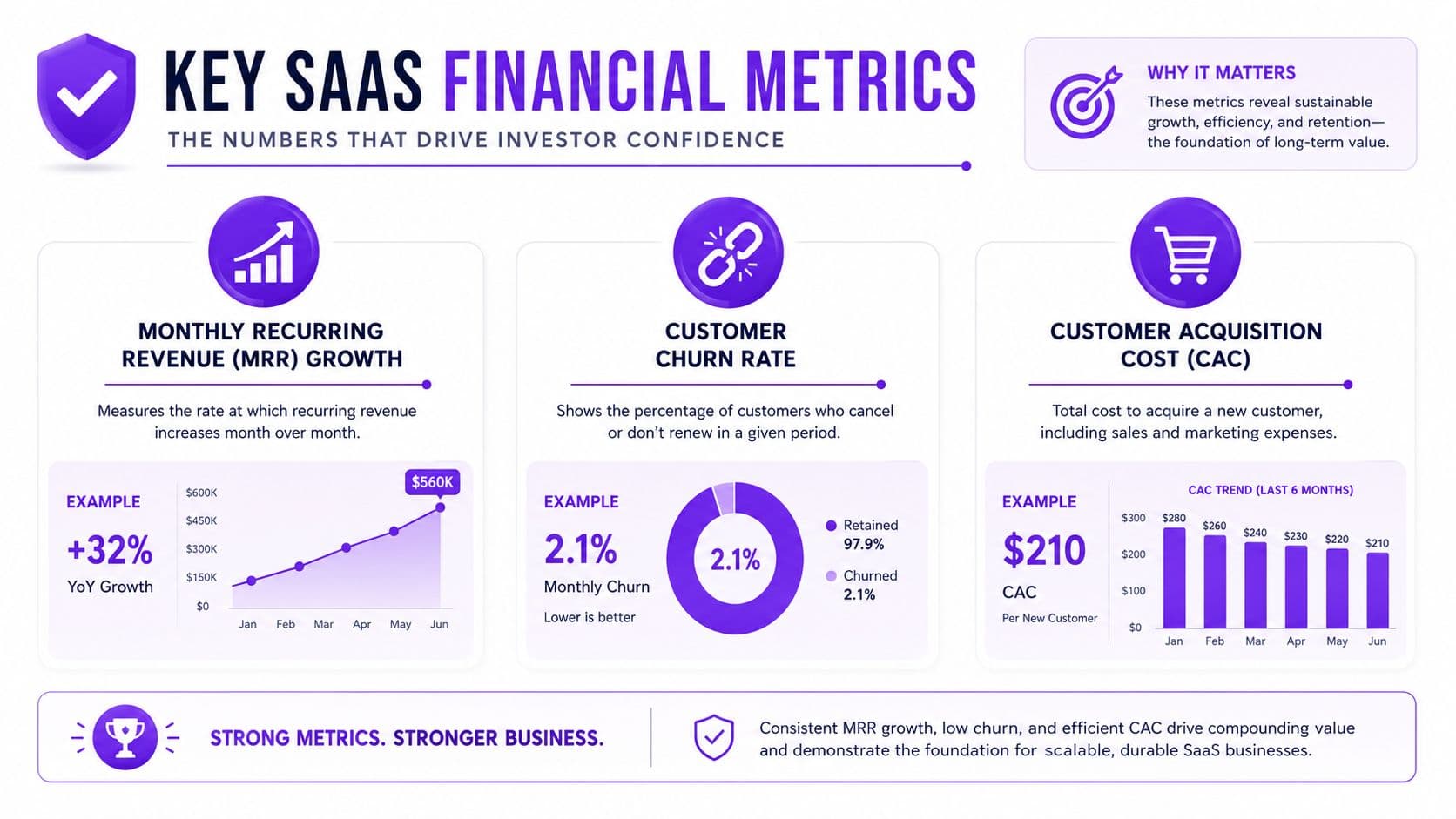

Mastering the SaaS Financial Schedules Investors Scrutinize

For a recurring revenue business, investors often move past the income statement quickly. They want the schedules that explain the engine underneath it. If those schedules don't reconcile cleanly to the books, the rest of the diligence process gets harder.

What investors test first

They usually start with five items:

-

MRR and ARR waterfall

Starting recurring revenue, plus new, plus expansion, less contraction, less churn, equals ending recurring revenue. -

Revenue recognition support

Your SaaS bookings view and your GAAP revenue view need a clear bridge. If you claim compliance with ASC 606, you need the support, not just the label. -

Deferred revenue schedule

This shows how cash collected differs from revenue recognized. -

Customer cohort behavior

Buyers want to see whether growth comes from new logos alone or whether existing customers expand. -

CAC and payback logic

Even if you're not selling a venture growth story, buyers still want to know whether acquisition spend is disciplined.

Clean SaaS metrics aren't a presentation issue. They're an accounting issue first, and a credibility issue second.

If you need a practical outside reference focused on transaction prep, this guide for SaaS M&A preparation is worth reviewing because it pushes founders to tie metrics back to source systems and diligence questions.

Worked examples that expose weak reporting

Use simple schedules that reconcile to the ledger. Here's a basic MRR waterfall.

| MRR Waterfall Example | Amount |

|---|---|

| Beginning MRR | $80,000 |

| New MRR | $12,000 |

| Expansion MRR | $6,000 |

| Contraction MRR | ($3,000) |

| Churned MRR | ($5,000) |

| Ending MRR | $90,000 |

That schedule tells a clearer story than a generic “revenue grew this month” statement. It also gives the buyer specific follow-up areas. Are churned accounts concentrated in one segment? Is expansion tied to annual repricing or actual product adoption?

Now take net dollar retention. One clean way to calculate it is:

(Starting period revenue from existing customers + expansion - contraction - churn) / starting period revenue from existing customers

Worked example:

- Starting period revenue from the cohort: $100,000

- Expansion from that same cohort: $15,000

- Contraction from that cohort: $5,000

- Churn from that cohort: $10,000

Calculation:

($100,000 + $15,000 - $5,000 - $10,000) / $100,000 = $100,000 / $100,000 = 1.0

So NDR is 1.0x, or 100%.

That result means your existing customer base replaced all lost revenue through expansion, but didn't create net expansion above the starting base. That's not necessarily bad. It just means your growth story depends more heavily on new customer acquisition than on installed-base growth.

Now look at LTV:CAC with a simple worked example.

- Average monthly gross profit per customer: $1,500

- Average monthly customer churn rate used for this internal model: 5%

- Estimated LTV using a simple steady-state shortcut:

$1,500 / 0.05 = $30,000 - CAC: $10,000

Calculation:

$30,000 / $10,000 = 3.0

LTV:CAC is 3.0x.

That tells a buyer your customer acquisition economics are acceptable under this model, assuming the churn and gross profit inputs are reliable. If your churn input is sloppy, the ratio is fiction. That's why buyers ask for source support, not just KPI snapshots.

How to present the schedules

The best packages do three things well:

-

Define every metric once

Put definitions in a KPI memo. State whether churn is logo churn or revenue churn, whether CAC includes salaries, and how you treat discounts. -

Bridge metrics to accounting

MRR is an operating metric. Revenue is an accounting output. Show the tie-out. -

Package trends with commentary

Don't upload spreadsheets without context. Explain one-time events, pricing changes, major customer movement, or billing system migrations.

For many founder-led teams, the reporting gap is packaging, not raw data. A proper financial reporting package gives buyers the numbers, the definitions, and the tie-outs in one place so your controller isn't answering the same questions repeatedly.

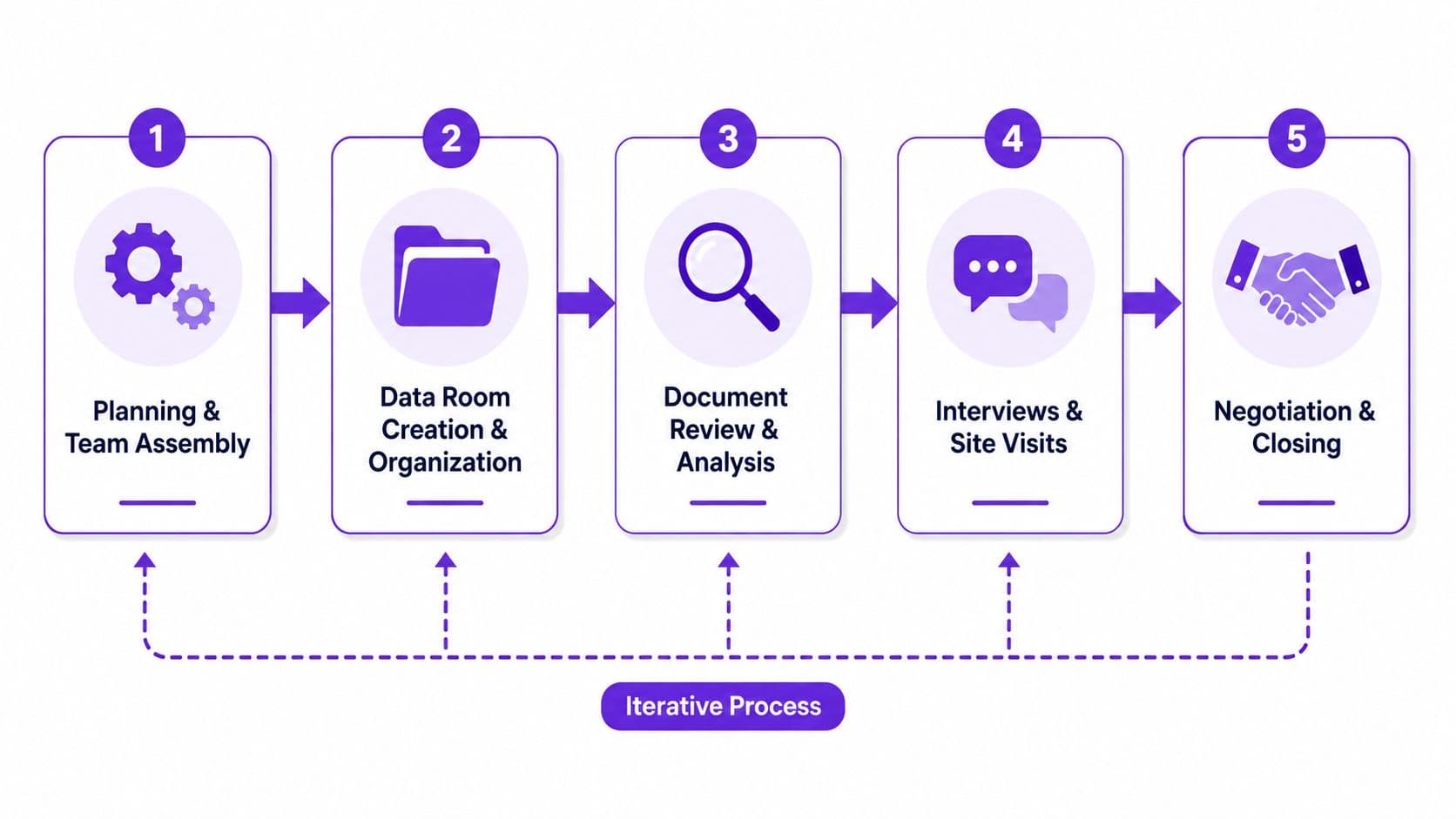

Running a Disciplined Due Diligence Process

Due diligence becomes expensive when nobody owns it. It also becomes dangerous. One industry source notes that full M&A due diligence reports often run 80 to 100 pages, and that poor diligence is implicated in roughly 60% of mismatched M&A outcomes according to Datarooms.org's due diligence report overview. The practical takeaway is simple. Review discipline and traceability aren't administrative niceties. They're controls.

Start with the workflow below.

Put one person in charge

Appoint a deal quarterback. In smaller companies, that's often the CFO, controller, or founder with the strongest financial discipline. Their job isn't to answer every question personally. Their job is to control the process.

That includes:

-

Managing the request list

Every request gets an owner, due date, and status. -

Controlling outbound information

Teams should not respond directly to buyers from their inboxes without central tracking. -

Maintaining one source of truth

If sales sends one customer list and finance sends another, you've just created a diligence issue.

A strong process also needs a review layer before anything is uploaded. If you want a practical template for request management and workstream ownership, a financial due diligence checklist can help your team assign responsibilities before requests start stacking up.

A practical four-week cadence

Week-by-week structure matters because urgency creates mistakes.

| Week | Focus | Output |

|---|---|---|

| Week 1 | Planning and scoping | Deal thesis, folder map, request tracker, assigned owners |

| Week 2 | VDR population | Core corporate, financial, legal, and commercial uploads |

| Week 3 | Q&A management | Responses, reconciliations, follow-up support, issue log |

| Week 4 | Management sessions | Presentation prep, open-item closure, confirmatory materials |

This short explainer is useful context for leaders who haven't run a formal process before:

The process works best when you separate facts, interpretation, and open items. Facts belong in the VDR. Interpretation belongs in the memo, management presentation, or response log. Open items belong in a tracker with dates and owners.

If your team is searching Slack for answers during buyer calls, the process isn't under control.

What fails in practice is informal coordination. Sales answers one way, product answers another, finance tries to clean it up later, and legal inherits the inconsistency. That's how minor issues become valuation discounts.

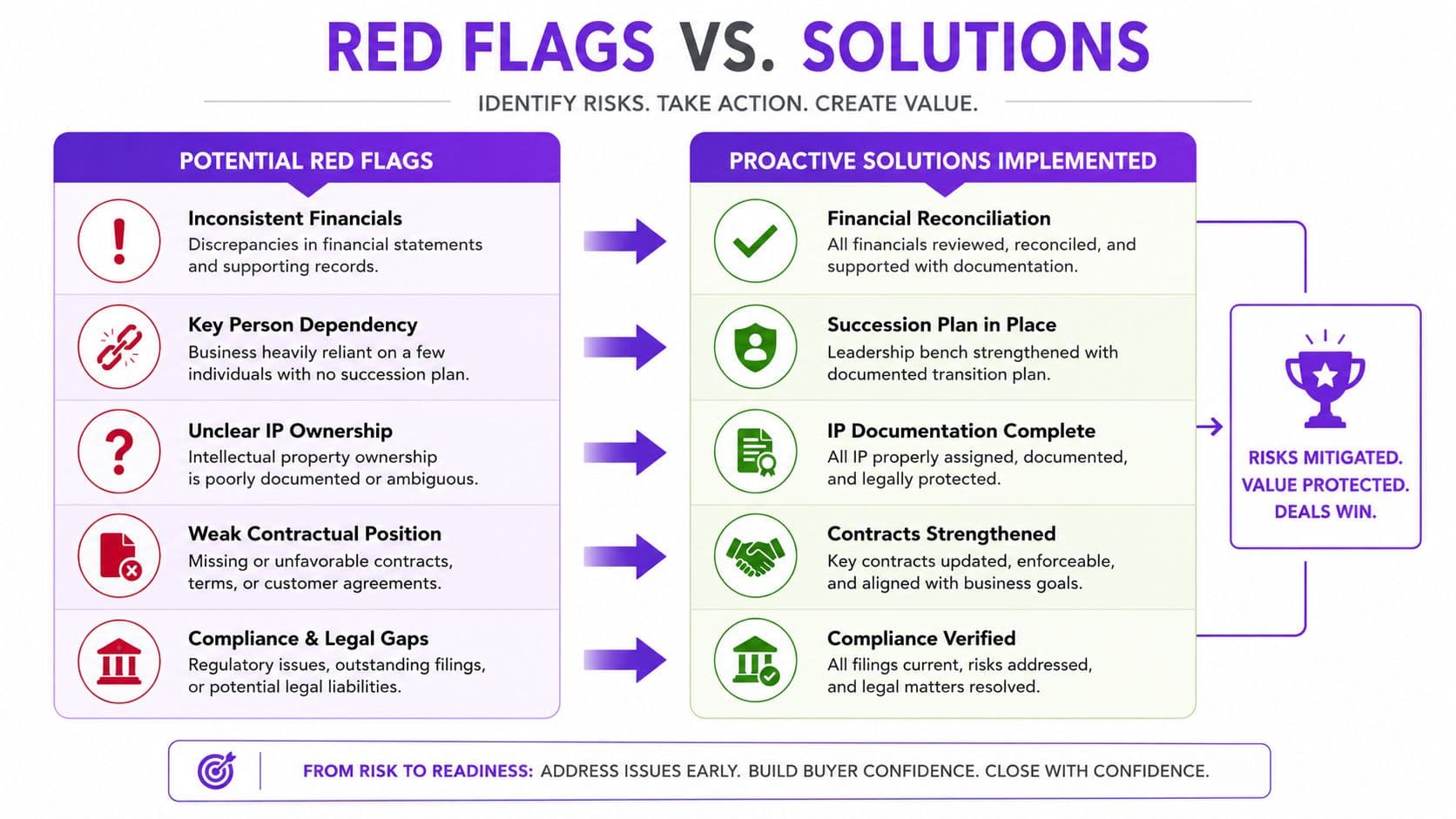

How to Find and Fix Red Flags Before They Kill Your Deal

Every company has flaws. Buyers don't walk away because a business is imperfect. They walk away when management looks surprised by known problems, or when the fix appears larger than the original issue.

Operational diligence is where many founder-led teams get caught flat-footed. SmartRoom's operational due diligence guidance is useful because it highlights recurring failure points beyond the financials, including overlooked IT risks, underestimated cultural integration challenges, and weak post-merger mitigation planning. Those issues regularly shape buyer confidence.

Five issues that change buyer behavior

For companies in your size range, these are the problems I see most often:

- Inconsistent financial reporting

- High customer concentration

- Ambiguous IP ownership

- Messy cap table or equity records

- Key person dependency

A sixth issue deserves more attention than it usually gets. Technical risk. If your product, data model, integrations, or security controls haven't been documented well, run a pre-deal review using a practical technical due diligence checklist so engineering issues don't blindside the transaction.

Red flags and remediation moves

| Red Flag | What It Looks Like | How to Fix It |

|---|---|---|

| Inconsistent financials | Revenue by KPI report doesn't match the GL, prior months are reopened without explanation | Lock close procedures, reconcile KPI schedules to accounting, and document restatements clearly |

| Customer concentration | One or two accounts dominate revenue or gross profit | Show contract durability, pipeline diversity, and segment-level retention trends |

| Ambiguous IP ownership | Contractors wrote code without assignment language, trademarks are incomplete | Collect signed invention assignment and contractor IP agreements, then update the IP schedule |

| Messy cap table | Missing option approvals, unclear share issuances, outdated SAFEs or notes | Have counsel rebuild the equity history before the room opens |

| Key person dependency | Founder owns sales, product, major customer relationships, and hiring | Build second-line management coverage and document delegated responsibilities |

Two remediation moves deserve special attention.

First, quality of earnings discipline. If your P&L moves around every month because of coding errors, timing issues, or inconsistent revenue treatment, buyers will question every other schedule. A clean quality of earnings preparation process helps you normalize earnings, explain add-backs carefully, and remove avoidable surprises.

Second, red flag memos. Don't hide known issues inside folders. Write a concise memo that says: here is the issue, here is when we found it, here is the impact, here is what we fixed, and here is what remains open. Buyers trust remediation more than defensiveness.

Buyers expect imperfections. They discount uncertainty.

What doesn't work is waiting for the buyer to surface a problem you already knew about. That makes the issue look bigger, and it makes management look less reliable.

Your Investor-Ready Action Plan

If you're preparing for a fundraise, acquisition, lender review, or major partnership, treat due diligence reports as a strategic asset, not an administrative afterthought.

Start with these moves this week:

- Appoint a deal quarterback who owns the request list, the VDR, and final outbound responses.

- Create the six-folder VDR structure and standardize file names before you upload anything.

- Load the core documents first. Corporate records, monthly financials, cap table, major contracts, and KPI definitions.

- Build your SaaS schedules so MRR, ARR, deferred revenue, and customer metrics tie back to the books.

- Run a red flag audit across finance, legal, product, IT, and ownership records.

- Write the narrative memo that explains the business, the risks, the fixes, and the remaining open items.

If your books aren't closing cleanly, your schedules don't reconcile, or your team can't produce support quickly, stop pretending you're ready. Fix the finance stack first. That's the foundation for everything else.

One option is Jumpstart Partners, which works with growing SaaS, agency, and service businesses on outsourced controller support, investor-ready reporting, and due-diligence cleanup so finance materials are organized before the pressure starts.

If you're heading into a transaction and want help getting the numbers, schedules, and supporting files into buyer-ready shape, talk with Jumpstart Partners. The goal isn't to upload more documents. It's to give investors a clean, defensible case for your valuation.