Financial Operations

Get Investor-Ready: Financial Reporting Package Examples

Explore 5 financial reporting package examples for SaaS, agencies & growing businesses. Get templates, metrics & checklists for investor-ready financials.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··26 min readStop Flying Blind: Your Financial Reports Are Lying to You

If you're running a $5M business off a standard QuickBooks P&L, you're missing the context that drives decisions. A proper monthly package doesn't stop at revenue and expense lines. It combines the income statement, balance sheet, and cash flow statement, then adds executive summary, budget-versus-actual analysis, comparative views, and KPI reporting so you can review decision-ready numbers instead of raw accounting output, as outlined in this overview of financial reporting packages.

That difference matters because one month in isolation doesn't tell you much. Jirav's guidance puts it bluntly: “a single month of data is useless out of context,” and modern monthly packages solve that by comparing current results to budget, prior period, prior year, and often forecast, as described in this financial report sample discussion. If you're trying to scale, hire, fundraise, or just avoid a cash surprise, context is the report.

You don't need more reports. You need the right package for the decision in front of you. Below are practical financial reporting package examples for founders and finance leaders who need clearer answers, faster. If you're also worried about what the statements may be hiding, read a guide to spotting financial risks.

Table of Contents

- 1. Example 1. The Foundational Monthly Financial Package

- 2. Example 2. The SaaS Unit Economics Package

- 3. Example 3. The Agency and Services Profitability Package

- 4. Example 4. The 13-Week Cash Flow Forecast Package

- 5. Example 5. The Investor Due Diligence Package

- 5 Financial Reporting Packages Compared

- From Reporting to Results. Your Next Steps

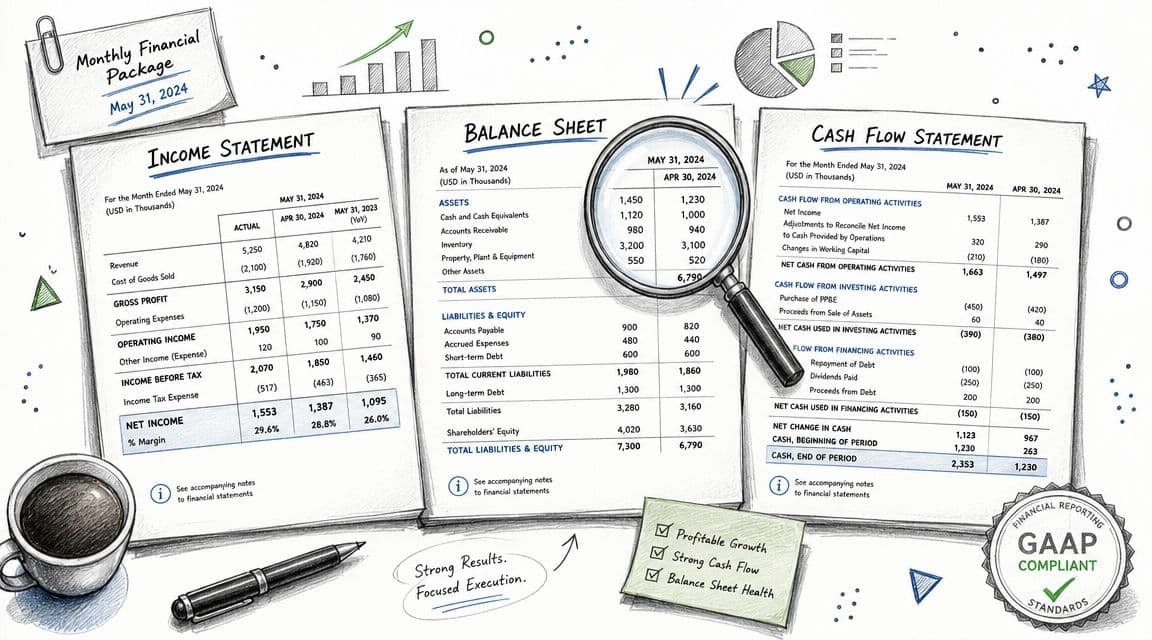

1. Example 1. The Foundational Monthly Financial Package

Founders rarely run into trouble because they lack a dashboard. They run into trouble because they trust a dashboard built on bad monthly reporting. Build the baseline package first, or every KPI that follows will mislead you.

This package is the control center for any business model. SaaS companies need it before layering on CAC and churn. Agencies need it before judging client or team profitability. If the base numbers are wrong, the model-specific analysis is worthless.

Build the core set first

Start with a disciplined monthly package built from three statements and a short operating summary. The three statements have to tie together. The cash flow statement begins with net income and adjusts for non-cash charges and working capital changes, which is why the three-statement example from Corporate Finance Institute mirrors how serious finance teams structure reporting.

Your baseline package should include:

- Income statement: Revenue, cost of sales if applicable, gross profit, operating expenses, EBITDA if you track it, and net income.

- Balance sheet: Cash, receivables, prepaid expenses, payables, accrued liabilities, debt, deferred revenue, and equity.

- Cash flow statement: Cash from operations, investing, and financing.

- Executive summary: Five to ten lines on results versus plan, what changed, and what management is doing next.

- Comparatives: Current month, previous month, year-to-date, budget, and the same month last year.

Keep the package short. Keep the commentary sharp. A founder should be able to read it in ten minutes and know where cash went, what margins did, and which line items need action.

One rule matters more than the rest.

If the balance sheet is not reconciled, do not present the package.

That means bank accounts tied out, receivables aged, payables reviewed, debt balances confirmed, and payroll liabilities matched to filings. For service firms with messy revenue recognition or pass-through costs, clean classifications matter even more. If that is your situation, review this guide to accounting for agencies before you finalize your monthly package.

A lender, board member, or buyer will test this immediately. They will not stop at revenue growth. They will ask why receivables increased faster than sales, why accrued expenses fell, or why deferred revenue moved against bookings. If you cannot answer from the package, you do not have a reporting package. You have a printout.

For implementation, use your accounting system for the ledger, then build a repeatable close calendar around it. Assign owners to each reconciliation. Lock the close date. Standardize your chart of accounts so the same expense does not bounce between categories every month. If you need a cleaner close and review process, use financial reporting best practices from Jumpstart Partners. If you are also handling statutory reporting deadlines, Preparing UK company accounts for 2026 covers the filing side.

How to interpret it like an operator

Read this package for movement, not presentation quality. A good operator looks for links between the statements and asks one question over and over: what changed, and does it help or hurt cash?

Use a simple example. Say the month shows:

- Revenue: $400,000

- Net income: $40,000

- Accounts receivable increase: $60,000

- Accounts payable decrease: $20,000

- Depreciation: $10,000

Operating cash flow starts with the $40,000 profit. Add back $10,000 of depreciation because it is non-cash. Subtract the $60,000 increase in receivables because customers have not paid yet. Subtract the $20,000 drop in payables because you paid vendors faster than you incurred new bills.

Operating cash flow = $40,000 + $10,000 - $60,000 - $20,000 = negative $30,000.

That is the kind of calculation founders need to see every month. Profit looked healthy. Cash went backwards.

Write the commentary the same way a CFO would explain it to a board:

- Revenue finished on plan, but collections slowed and receivables rose by $60,000.

- Net income was positive at $40,000, yet operations used $30,000 of cash after working capital movements.

- Management action: tighten invoice follow-up, review customer payment terms, and delay non-core spending until collections normalize.

That style works because it connects result, cause, and action. No jargon. No filler.

A solid foundational package does one job well. It gives you a clean monthly view of profit, balance sheet health, and cash conversion so you can build the right next layer for your business, whether that is SaaS unit economics, agency client margins, cash forecasting, or investor diligence.

2. Example 2. The SaaS Unit Economics Package

Many SaaS companies fail for the same reason. Revenue grows while the cost to get and keep that revenue grows faster.

That is why a standard monthly package is not enough for a subscription business. GAAP statements show what happened. A SaaS unit economics package shows whether growth is worth funding. If your CAC is rising, gross margin is thin, or churn is wiping out new bookings, the headline revenue number will hide the problem until cash gets tight.

This package should sit on top of your core financials and answer four questions fast. Are we adding profitable recurring revenue? Are customers staying long enough to pay back acquisition cost? Is expansion offsetting churn? How much cash pressure does this growth model create?

What goes into the SaaS version

Build the package around the metrics that drive value in a recurring revenue model:

- MRR movement schedule: Beginning MRR, new MRR, expansion MRR, contraction MRR, churned MRR, ending MRR.

- Gross margin by revenue type: Software margin separate from onboarding, support, and other service-heavy work.

- CAC view: Sales and marketing spend tied to new customer adds and new ARR or MRR.

- Payback calculation: CAC divided by monthly gross profit from a new customer cohort.

- Retention metrics: Gross revenue retention and net revenue retention.

- Sales efficiency: New ARR compared with sales and marketing spend.

- Cash view: Current burn, runway, and the near-term collection risk behind the growth plan.

One rule matters more than any dashboard design choice. Every SaaS KPI must reconcile to the ledger. If your CRM says one MRR number, Stripe says another, and the accounting system says a third, stop polishing charts and fix the data pipeline.

A common failure point is implementation revenue. Founders count every signed customer as proof the model works, but the actual situation can be ugly. A company can add logos quickly and still destroy margin if onboarding takes too many unbilled hours, support is underpriced, or annual contracts are booked before cash is collected.

A worked SaaS calculation

Use a simple example.

Assume this month shows:

- Sales and marketing spend: $50,000

- New MRR added: $10,000

- Beginning MRR: $100,000

- Expansion MRR: $3,000

- Churned MRR: $4,000

Ending MRR is:

$100,000 + $10,000 + $3,000 - $4,000 = $109,000

That matters because the business did not really grow by the full $13,000 of new and expansion revenue. Net MRR growth was $9,000 after churn. A founder who only looks at bookings will overestimate momentum and hire too early.

Now check acquisition efficiency. If you spent $50,000 to add $10,000 of new MRR, you spent 5x one month of new MRR to get those customers. That is not automatically bad, but it is incomplete. You need the margin view.

If those customers produce an 80% gross margin, monthly gross profit from that new MRR is:

$10,000 x 80% = $8,000

Simple payback is:

$50,000 / $8,000 = 6.25 months

That is a useful operating metric. It tells you how long new customers take to repay acquisition cost before overhead. If payback starts stretching from six months to nine or twelve, growth is getting more expensive even if ARR still looks good.

Benchmarks that actually help

Do not stuff the package with vanity metrics. Use a small set of benchmarks that changes decisions.

For an early-stage SaaS business, a shorter CAC payback period usually gives you more room to reinvest. Higher gross margin gives you more tolerance for acquisition spend. Strong net revenue retention can cover for moderate logo churn. Weak retention kills the model, no matter how good top-of-funnel numbers look.

That is the point of the package. It separates healthy growth from purchased growth.

How to write the commentary

The commentary should read like a CFO note to the CEO or board, not a BI tool export. State result, cause, and action.

Use this template:

- MRR increased from $100,000 to $109,000, driven by $10,000 of new MRR and $3,000 of expansion.

- Churn removed $4,000 of MRR, which reduced net growth to $9,000 and weakened retention.

- Sales and marketing spend of $50,000 produced 6.25-month payback at 80% gross margin.

- Management action: review churn by cohort, tighten ICP targeting, and reprice onboarding work that is depressing margin.

That last point matters. Commentary should tell management what to do next.

If growth is outpacing collections or annual prepay assumptions are slipping, pair this package with a 13-week cash flow forecast for SaaS cash planning. Unit economics tell you whether the model works. Cash forecasting tells you whether you can afford the path.

For a practical metric framework, review Jumpstart's guide to unit economics.

3. Example 3. The Agency and Services Profitability Package

Agency margins usually leak in plain sight. The company P&L can look fine while one retainer drains partner time, revision rounds, and unbilled strategy work. If you sell time, expertise, or deliverables, client-level margin is the report that matters.

Build this package to show profit by client, project, service line, and delivery team. A founder needs one view. Account leads need another. Operations needs a third. The point is simple. Reporting should match the decision you need to make.

What the package must show

Start with five cuts of the same work:

- Revenue by client and project: Retainers, project fees, pass-through charges, and any write-offs or credits.

- Direct labor cost by account: Payroll cost allocated from timesheets, including taxes and benefits if you want true delivery cost.

- Gross margin by client: Revenue less direct labor, contractors, and any delivery software tied to the account.

- Realization: Billed value compared with the value of hours worked, especially on fixed-fee engagements.

- Utilization by role or team: Productive hours against available hours, so you can see whether low margin comes from pricing, staffing, or idle capacity.

If your team does not submit daily timesheets, your margin report is guesswork.

That sounds harsh. It is also true. Agencies often call a client "high value" because invoices get paid on time. Then they finally allocate strategist time, leadership review, and revision cycles, and the account turns into the weakest margin in the portfolio.

The worked calculation

Use one simple client example and make the math visible.

Say Client A pays a monthly retainer of $30,000. During the month, your team logs 120 hours. Your blended direct labor cost is $100 per hour, so direct labor is $12,000. Add $3,000 of contractor support and account-specific software. Gross profit is:

$30,000 revenue - $12,000 direct labor - $3,000 direct costs = $15,000 gross profit

Gross margin is:

$15,000 / $30,000 = 50% gross margin

Now add realization. If those same 120 hours carry an internal billable value of $300 per hour, the worked value is $36,000.

$36,000 worked value - $30,000 billed = $6,000 underbilling

That $6,000 gap tells you more than the top-line retainer number ever will. The client is profitable today, but only because your pricing has not caught up with delivery effort. If hours rise again next month, margin drops fast.

How to interpret the numbers

Use clear thresholds. Founders need rules, not trivia.

- High revenue, low margin: Reprice the account, cut scope, or change staffing mix.

- Low realization on fixed-fee work: Your scoping process is weak, or the client is getting free revisions.

- Low utilization across a team: You have excess capacity, weak scheduling, or too many senior people doing junior work.

- Strong client margin but weak company margin: Overhead is too heavy, or account teams are carrying non-client work that never gets assigned.

A stable retainer is not the same as a healthy retainer.

The fastest way to improve an agency P&L is usually not "sell more." It is fixing the bottom quartile of accounts. One underpriced client can absorb the profit from two well-run ones.

Commentary template for the monthly package

Write the note like an operating review, not a spreadsheet export. State the result, the cause, and the action.

Use language like this:

- Client A generated $30,000 of revenue and $15,000 of gross profit, for 50% gross margin.

- Realization fell because the team delivered 120 hours against a retainer priced closer to 100 hours of work.

- Revision cycles and senior review time drove the overage, especially in strategy and creative.

- Management action: reprice the retainer at renewal, cap revision rounds, and shift production tasks to lower-cost roles.

That last line is the whole point. A profitability package should force a decision.

For firms tightening client-level reporting, Jumpstart's agency accounting guide is useful because it connects timesheets, delivery cost allocation, and margin review in a service business. If weak project controls or inconsistent client documentation are already showing up in your numbers, use this financial due diligence checklist for service businesses and agencies before the problems surface in a sale process or investor review.

Warning sign: If an account lead says a client is strategically important but cannot show client-level gross margin and realization, that account is running on opinion, not evidence.

4. Example 4. The 13-Week Cash Flow Forecast Package

Cash problems rarely start in the cash flow statement. They start in the gap between when you expect money and when it hits the bank. A 13-week cash flow forecast closes that gap. If you run a SaaS company waiting on annual renewals, an agency with lumpy client payments, or any business hiring ahead of revenue, this package belongs in your weekly operating rhythm.

Put bluntly, this report tells you whether you can fund payroll, debt payments, and vendor commitments before the month ends. Founders who skip it end up reacting late and paying for that mistake with rushed layoffs, expensive bridge capital, or supplier issues.

For cash management, the reporting cadence matters as much as the format. Update this package every week from actual bank activity, then revise the next 13 weeks based on what changed. Monthly review is too slow. A stale forecast gives false confidence and leads directly to bad decisions.

What the package must show each week

Use weekly columns, not monthly buckets. Monthly views hide timing risk. Your package should show:

- Beginning cash: Actual bank balance at the start of the week.

- Cash receipts: Expected customer collections, owner funding, debt draws, tax refunds, and any other real cash inflow.

- Cash disbursements: Payroll, rent, software, contractors, debt service, taxes, capex, and one-off payments.

- Ending cash: Beginning cash plus receipts minus disbursements.

- Minimum cash threshold: The point where management action starts.

- Variance to prior forecast: What changed from last week's view, and why.

Use collection dates, not invoice dates. If your largest customer pays 15 days late every quarter, model that behavior. Hope is not a forecasting method.

Here is a simple baseline calculation. Starting cash is $120,000. Week 1 collections are $35,000. Week 1 outflows are payroll of $40,000, rent of $5,000, software of $3,000, and vendors of $12,000. Ending cash equals $120,000 plus $35,000 minus $60,000, which gives you $95,000.

That single line matters because it forces a management call. If your minimum cash threshold is $75,000, Week 1 looks fine. If Weeks 2 and 3 include another payroll cycle before a major customer pays, you may have a problem already.

How this package changes by business model

A SaaS company and an agency should not build the same cash forecast.

For a SaaS company, focus on renewal timing, annual prepayments, sales tax or VAT remittances, cloud infrastructure bills, and hiring plans. One delayed enterprise renewal can distort a full quarter of cash. If a customer owes $90,000 on an annual contract and payment slips from Week 6 to Week 9, your forecast should show the exact cash gap created.

For an agency, collections and payroll timing usually drive the model. Retainers, project deposits, pass-through media spend, freelancer payments, and client concentration matter more than deferred revenue schedules. An agency with $150,000 of monthly payroll and two clients representing 40% of collections needs a tighter weekly process than a business with diversified small invoices.

Use Jumpstart's 13-week cash flow resource if you want a practical template and process. If cash pressure is already exposing messy contracts, weak billing controls, or unsupported balances, run through this financial due diligence checklist for service businesses and agencies before the problem gets in front of a lender or investor.

A short explainer can help your team understand how to keep the model live:

A worked cash forecast calculation

Start Week 5 with $80,000. You forecast $25,000 of collections and $55,000 of cash outflows. That would put ending cash at $50,000.

Now use the actual result. One customer delays payment, so actual cash in is $10,000, not $25,000. Ending cash falls to $35,000.

That $15,000 miss is your warning signal. If your minimum threshold is $40,000, management needs to act that week. The right response depends on the business. A SaaS founder might delay a noncritical hire and pull renewals forward with early-pay outreach. An agency owner might pause contractor spend, collect overdue invoices personally, or renegotiate vendor timing on pass-through costs.

Commentary template for the weekly cash package

Do not attach the schedule with no explanation. Write a short operating note:

- Week 5 ending cash was $35,000 versus a forecast of $50,000.

- The variance came from a $15,000 customer payment delay.

- Cash remains above debt covenant minimums but below our internal buffer of $40,000.

- Management action: collections lead to call the customer today, defer $8,000 of discretionary spend, and push one contractor payment into next week.

That is the standard. A 13-week cash flow forecast is not an accounting exercise. It is a decision tool.

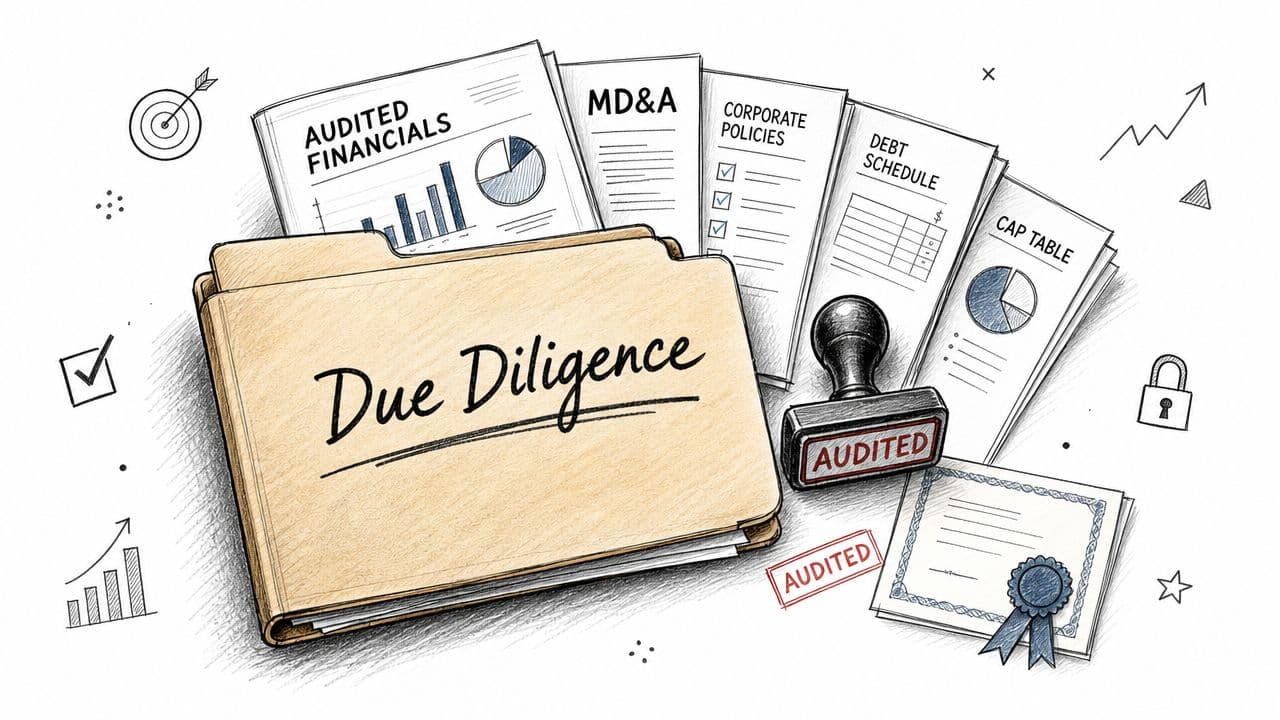

5. Example 5. The Investor Due Diligence Package

Deals slow down for one reason more than founders want to admit. The numbers do not tie.

If you are raising capital or preparing for a sale, your standard monthly package stops being enough. Investors are not looking for a prettier board deck. They want proof that revenue, margins, cash movement, and headcount all reconcile across historical results and the forecast. If they find gaps, they assume the business is harder to control than management says.

That is why the investor due diligence package matters. It turns your finance stack into an evidence file.

Reach Reporting's advisory examples show the level expected once a company moves from bookkeeping to board and investor reporting, including three-way models, budgets, and forecast discipline, as shown in Reach Reporting's case study examples.

Build a package that survives investor questions

A good diligence package is built for reconciliation first and presentation second. Every schedule should connect back to the same underlying numbers. If ARR in the KPI page does not tie to recognized revenue, billings, and deferred revenue, expect a long diligence call and a painful cleanup request.

Include these components:

- Historical monthly financials: Monthly P&L, balance sheet, and cash flow statement for at least the trailing 12 to 24 months, presented on a consistent basis.

- Management reporting package: An executive summary, KPI trends, variance explanations, and commentary on what changed and why.

- Three-statement forecast: A model that starts from the historicals and flows cleanly into projected revenue, expenses, working capital, and cash.

- Support schedules: Revenue recognition, deferred revenue, debt, payroll, equity, cap table, customer concentration, and major contracts.

- Accounting policy notes: Clear definitions for revenue, gross margin, bookings, ARR, EBITDA adjustments, and any non-GAAP metrics used in the deck.

The test is simple. An investor should be able to pick one month, trace revenue from invoice to recognition, see the cash effect, and understand the balance sheet impact without asking your finance lead to rebuild the file live.

A worked example founders actually face

Take a SaaS company pitching a Series A. The founder reports $150,000 in January billings from annual prepay contracts. Cash comes in immediately, but only $12,500 should hit January revenue if the contracts start that month and are recognized over 12 months.

The entries matter:

- Cash received: $150,000

- January recognized revenue: $12,500

- January deferred revenue liability: $137,500

Now look at what investors do next. They compare the P&L, the balance sheet, and the cash flow statement. If January revenue is shown as $150,000 on the P&L while deferred revenue barely moves, they know the accounting is wrong or the reporting is inconsistent. Either way, trust drops.

Many founder models often fall apart. Growth looks strong in the deck, but the accounting support does not hold up under review.

What founders get wrong

The first mistake is treating diligence like document storage. Uploading files into a data room is administrative work. Due diligence is a consistency test.

The second mistake is changing metric definitions midstream. If gross margin excludes hosting in one quarter and includes it in the next, your trend line is useless. If CAC includes founder-led sales in one version of the model but not another, your payback math is fiction.

The third mistake is running separate versions of the truth. One file for management. Another for investors. A third for the audit team. That setup creates reconciliation problems and wastes weeks during a live deal process. Use one governed data set and build different views off it.

Commentary template for the diligence package

Do not send schedules without an operating explanation. Include a short note that answers the next question before it is asked.

- February revenue grew 18% month over month, driven by $42,000 of new annual contracts and stable logo retention.

- Deferred revenue increased by $96,000 because annual prepayments outpaced recognized revenue in the month.

- Gross margin declined from 78% to 74% due to a temporary spike in implementation labor for two enterprise customers.

- Management expects margin to recover above 77% next quarter as onboarding work rolls off and pricing resets on one legacy contract.

That style works because it ties results to drivers and management action.

For process discipline and document prep, Jumpstart's financial due diligence checklist is a useful starting point. Use it to pressure-test completeness, then make your package tighter by reconciling every KPI and forecast assumption back to the financial statements.

A diligence package should answer three questions fast. Are the historicals clean? Does the forecast follow from reality? Can management explain the gaps without improvising? If the answer to any one is no, fix that before you start the process.

5 Financial Reporting Packages Compared

| Package | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊⭐ | Ideal Use Cases | Key Advantages 💡 |

|---|---|---|---|---|---|

| Example 1: The Foundational Monthly Financial Package | Moderate–High 🔄, GAAP knowledge + disciplined month‑end close | Moderate ⚡, accounting team or outsourced Controller, GAAP‑ready software (QuickBooks/NetSuite) | Reliable, audit‑ready financials; single source of truth; trend comparability. ⭐⭐⭐⭐ | All businesses > $500K ARR; baseline reporting for investors and audits | Universally accepted by stakeholders; enables accurate analysis and audit readiness |

| Example 2: The SaaS Unit Economics Package | High 🔄, billing + ledger integrations and cohort modeling | High ⚡, billing system (Stripe/Zuora), BI tools, analyst/engineer time | Actionable unit economics (MRR/ARR, CAC payback, NDR); investor‑grade SaaS metrics. ⭐⭐⭐⭐ | SaaS startups (Series A/B), PLG companies, venture‑backed growth teams | Reveals growth profitability; informs pricing, GTM and fundraising narratives |

| Example 3: The Agency & Services Profitability Package | Medium–High 🔄, project accounting + strict time tracking | Moderate ⚡, time tracking, PM tools, accounting integration, disciplined staff | Client/project profitability, utilization and realization metrics. ⭐⭐⭐ | Agencies, consultancies, professional services with multiple projects | Identifies unprofitable clients/projects; improves pricing and resource allocation |

| Example 4: The 13‑Week Cash Flow Forecast Package | Medium 🔄, weekly updates and cross‑functional assumptions | Moderate ⚡, finance analyst, inputs from sales/ops, forecast model or tool | Near‑term liquidity visibility; early warning of cash shortfalls; scenario planning. ⭐⭐⭐⭐ | Businesses with <12 months runway or volatile cash flows; seasonal operations | Prevents liquidity crises; supports short‑term hiring and spend decisions |

| Example 5: The Investor Due Diligence Package | Very High 🔄, multi‑year audits, legal and control documentation | Very High ⚡, audit firm, CFO/Controller, legal support, months of preparation, significant cost | Institutional confidence, faster diligence, potential for higher valuation. ⭐⭐⭐⭐⭐ | Companies raising Series A+ or preparing for acquisition; large debt financings | Withstands intense investor scrutiny; reduces perceived risk and deal friction |

From Reporting to Results. Your Next Steps

The best financial reporting package examples all share one trait. They turn accounting output into decisions. That's their core purpose.

If you're a founder, start with the foundational monthly package first. Get the three statements right, reconcile the balance sheet, and add a short executive summary with variance commentary. Once that baseline is stable, build the package that fits your operating model. SaaS companies need unit economics tied to the ledger. Agencies need client and project margin visibility. Any business with tight liquidity needs a weekly cash forecast. Companies heading into a raise or sale need a diligence-ready package that reconciles history, KPIs, and forecast logic.

Don't hide behind software. QuickBooks, Xero, NetSuite, Stripe, and your BI tools are only useful if the underlying reporting structure is clean. If the package isn't suited to the audience, if the comparisons aren't there, or if the commentary doesn't explain the movement, you're still flying blind.

One more point matters. Most reporting failures aren't formatting failures. They're control failures. Teams close late, leave accounts unreconciled, mix cash and accrual logic, and present KPIs that don't tie to the books. Fix that and the package gets better fast.

The practical next steps are simple:

- Set the baseline: Finalize your monthly three-statement package.

- Choose one specialized package: SaaS unit economics, agency profitability, cash forecast, or diligence pack.

- Define owners: One person owns close, one owns KPI logic, one owns commentary.

- Review monthly or weekly on a calendar: Reporting only works when the cadence is fixed.

- Write the decisions next to the numbers: Hiring, pricing, collections, scope, fundraising timeline.

“Founders often confuse bookkeeping with financial strategy,” says David, Head of Controller Services at Jumpstart Partners. “Bookkeeping records the past. A strategic financial package helps you build the future. The biggest mistake is waiting until you're in due diligence or running out of cash to build one.”

If you need outside support, Jumpstart Partners is one option for outsourced controller and bookkeeping support for growing businesses, including financial reporting, cash flow visibility, and investor-ready packages.

If your current reports don't tell you where cash is going, which clients or customers are profitable, and what will break next, it's time to fix the system. Jumpstart Partners works with SaaS, agency, and other growing businesses to build cleaner closes, better reporting packages, and tighter financial control.