Financial Operations

Finding Your Exit Strategy Consultant: A 2026 Guide

Select an exit strategy consultant for your SaaS or agency. Get pricing, timelines, and deliverables to ensure a successful 2026 exit.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··17 min readMost founders talk about exit like it's a future transaction. It isn't. It's a present operating discipline. One published source says 84% of business owners lack a formal exit strategy, while 73% of privately held U.S. businesses want to transition ownership in the next decade (exit-planning readiness gap for owners). That gap is the whole reason an exit strategy consultant exists.

If you run a SaaS company, agency, or professional services firm, your biggest risk isn't just low valuation. It's building a business that only works because you're still in the middle of every sale, delivery handoff, pricing decision, and client rescue. Buyers don't pay top dollar for founder dependence. They discount it, structure around it, or walk.

Table of Contents

- Why Most Founders Are Unprepared for a Successful Exit

- Choosing Your Exit Advisor

- Preparing Your Company for Scrutiny

- The Exit Engagement Roadmap and Timeline

- Building a Business That Can Exit Without You

- Your First Step Toward a Successful Exit

Why Most Founders Are Unprepared for a Successful Exit

Most founder-led service businesses are not sale-ready when the opportunity shows up.

That includes good businesses. I'm talking about SaaS companies with sticky revenue, agencies with healthy margins, and firms that have grown fast through founder hustle. They still fail the test buyers care about most. Can this company keep performing after the founder steps out of the center of it?

That is the gap founders miss. Exit readiness is not just revenue growth or a headline valuation. It is transferability. If your relationships, pricing logic, sales process, delivery oversight, and financial judgment sit in one person's head, the buyer is not acquiring a durable asset. They are acquiring your continued involvement.

A company can look strong and still fail diligence

Founders often confuse momentum with readiness. Buyers do not.

They ask plain, expensive questions:

- Are the financials accurate, timely, and consistent

- Can revenue be traced by customer, contract type, and margin

- Does the management team own key decisions without founder intervention

- Will customer retention hold if the founder exits

- Do contracts, controls, and reporting stand up under scrutiny

If those answers are weak, price drops. Terms get tighter. Timelines slip.

For service businesses, founder dependency is usually the biggest value leak. In agencies, that shows up when the founder owns the top client relationships, approves every proposal, and steps in to save delivery. In SaaS, it shows up when enterprise renewals, product direction, and key hiring decisions still route through the founder. Buyers see that risk immediately.

Practical rule: If the business needs you to close deals, calm clients, approve exceptions, and explain the numbers, you do not have an exit-ready company. You have a founder-powered job with some enterprise value attached to it.

A strong exit strategy consultant works on that problem before any sale process starts. The job is to expose valuation leaks early, tighten reporting, clean up decision rights, and turn tribal knowledge into processes another operator can run. That is how you build a founder-proof exit instead of hoping a buyer will ignore the risk.

The Cost of Waiting

Poor preparation rarely kills a deal in one dramatic moment. It shows up in buyer protections.

Expect earnouts, holdbacks, retrading, deeper diligence requests, and lower confidence in the forecast. Buyers pay full value for earnings they believe will continue. They discount earnings tied to a founder, a few concentrated accounts, weak close processes, or undocumented delivery systems.

This is why serious preparation starts with finance and operations, not pitch decks. Get the monthly close under control. Standardize KPI definitions. Document account ownership and handoffs. Put contracts in one place. Clarify who owns pricing, approvals, and customer escalation. Then review the kind of detail that appears in due diligence reports for M&A and finance work, because that is the level of scrutiny your business will face.

You should also spend time with credible business exit strategy insights for owners, but do not stop at theory. Readiness is built in the ledger, the org chart, the contract file, and the operating cadence. That is where exits are won or discounted.

Choosing Your Exit Advisor

Not every advisor who talks about exits does the same job. That matters because hiring the wrong person too early creates noise, bad incentives, and wasted time.

Know which advisor you actually need

Some founders need a strategist. Some need a deal runner. Some need both, but not at the same time.

| Advisor Type | Primary Focus | Best For | Typical Fee Structure |

|---|---|---|---|

| Exit strategy consultant | Readiness, valuation gaps, transferability, tax and personal planning coordination | Founders who aren't immediately going to market and need preparation first | Retainer, project fee, or advisory fee |

| M&A advisor | Buyer outreach, positioning, process management, negotiation | Companies that are ready to run a sale process | Success fee, sometimes with a monthly retainer |

| Business broker | Listing and sale of smaller businesses | Simpler owner-led businesses with straightforward transfer structures | Commission-based, often success-oriented |

| CPA or tax advisor | Tax planning, deal structure, entity implications | Owners who need tax modeling and transaction structuring support | Hourly or project-based |

| Outsourced finance lead | Reporting cleanup, KPI accuracy, close process, diligence support | Companies with weak financial infrastructure | Monthly retainer or fixed-scope engagement |

If you're still founder-dependent, don't start with a broker. Start with readiness work. For many businesses in the lower middle market, the biggest value creation happens before any buyer sees the company.

For finance-function support before an exit, a practical reference point is understanding what CFO services consulting can and can't do compared with controller-level execution.

Questions worth asking before you hire anyone

Don't ask vague questions like “How many deals have you done?” Ask questions that expose their process.

- Industry fit: Have you worked with SaaS, agencies, or recurring-revenue service firms where founder dependency affects value?

- Readiness method: How do you assess earnings quality, reporting gaps, customer concentration, and management depth before discussing valuation?

- Financial rigor: Do you build financial models, perform market analysis, and run SWOT analysis as part of planning, or do you jump straight to sale prep?

- Buyer lens: How do you evaluate whether the business is transferable without the founder?

- Coordination: How do you work with tax, legal, and finance teams when the owner's goals conflict with transaction speed?

If an advisor can't clearly explain their readiness process, they probably don't have one.

Red flags that should end the conversation

Some warning signs are obvious. Others sound polished until you've lived through diligence.

- Guaranteed valuation talk: Anyone promising a specific number before a real review is selling confidence, not advice.

- Quick-sale pressure: If they push buyer outreach before a readiness assessment, they're optimizing for transaction volume.

- No operating depth: If they can't talk cleanly about revenue recognition, margin analysis, or management continuity, they won't help you fix what buyers flag.

- Founder worship: If they frame your personal relationships as the main asset, they're missing the core issue. Buyers want company-level durability.

- Compensation opacity: If fees, referral economics, or success incentives aren't clear, assume conflict until proven otherwise.

The right exit advisor helps you build negotiating power before negotiations start. The wrong one drags you into market before the business is ready.

Preparing Your Company for Scrutiny

Buyers don't buy your story first. They buy your evidence first.

If your P&L changes after every close, your balance sheet has stale accounts, and your revenue reporting doesn't tie to contracts, you're not ready for serious diligence. The fix isn't glamorous. It's disciplined financial and operational cleanup.

The records buyers expect to see

An exit-ready company can answer basic questions fast, cleanly, and consistently. That means you need organized records across finance, legal, operations, customer data, and team structure.

Use this as a practical checklist:

- Financial statements: Monthly P&L, balance sheet, and cash flow statements that reconcile and tell the same story.

- Revenue detail: Revenue by product line, service line, customer, contract type, and delivery model.

- Margin visibility: Gross margin by client, channel, or service category. Agencies and services firms often miss this and pay for it later.

- Legal support: Signed customer agreements, vendor contracts, employee documents, IP assignments, and open disputes.

- Operational proof: Documented SOPs, system maps, approval workflows, and delivery handoff processes.

If you need a concrete buyer-side checklist, review this financial due diligence checklist for growing companies. It's the kind of material that forces founders to confront where the file cabinet, CRM, accounting system, and leadership narrative don't line up.

One more issue gets ignored far too often. Buyers do look beyond the ledger. Public complaints, unresolved review issues, and reputation risk can affect perceived durability, especially in agency and services businesses. This breakdown of online reputation and business valuation is worth reading before a process starts.

A worked net proceeds example

The number that matters is not headline valuation. It's what you keep.

A published advisory source puts the question plainly: “What am I walking away with, and is it enough to exit now?” It also notes that as buyer scrutiny increased in 2025, headline valuation became a weaker predictor of owner outcome than after-tax proceeds and timing risk (exit planning from all angles for owners).

Here's a simple worked example using round numbers for illustration:

| Item | Example Amount |

|---|---|

| Headline purchase price | $8,000,000 |

| Less debt payoff | $1,200,000 |

| Less advisor and legal fees | $600,000 |

| Less transaction bonuses and closing costs | $200,000 |

| Estimated pre-tax proceeds | $6,000,000 |

| Less estimated taxes | $1,800,000 |

| Estimated net walkaway amount | $4,200,000 |

That example doesn't tell you what your taxes will be. Your tax advisor does that. What it does show is how fast the “big number” turns into the actual number.

Now go one level deeper. Ask yourself:

- Is that net amount enough to fund your post-exit life?

- Does it justify the risk of an earnout or a delayed close?

- Are you selling because the business is ready, or because you're tired?

A founder who knows their net walkaway number makes better decisions than a founder who only knows the top-line offer.

The Exit Engagement Roadmap and Timeline

Founders often imagine exit consulting as a few meetings, a valuation opinion, and an introduction to buyers. Real engagements are more operational than that.

One industry guide recommends starting exit planning two to five years before the planned exit because owners need time to improve financial performance, clean up reporting, and strengthen valuation before a sale or transfer (exit strategy consulting preparation timeline). That timeline is realistic. Anything shorter compresses your options.

What a real engagement looks like

A strong engagement usually follows a phased sequence. One advisory framework describes it as assessment and goal setting, valuation and gap analysis, customized strategy design, pre-sale value enhancement, and exit-execution management (five-phase exit strategy process).

That maps cleanly to what founders experience:

| Phase | What happens | What you should receive |

|---|---|---|

| Assessment | Owner goals, baseline financial review, readiness discussion | Initial findings, issue list, decision priorities |

| Valuation and gap analysis | Financial modeling, market analysis, SWOT analysis, buyer-risk review | Valuation range logic, value-gap summary |

| Strategy design | Exit options, timing, role of founder, tax and legal coordination | Written roadmap with milestones |

| Value enhancement | Reporting upgrades, management depth, contract cleanup, margin work | Operating plan tied to buyer concerns |

| Execution support | Data room prep, buyer questions, diligence support, negotiation coordination | Faster responses, cleaner process, fewer surprises |

A lot of founders underestimate how much value sits in the middle phases. That's where you fix weak controls, normalize earnings, improve reporting cadence, and make the company easier to underwrite.

For companies heading toward a transaction, quality of earnings work before a sale often becomes one of the highest-impact readiness steps because it forces your numbers to survive outside scrutiny.

A helpful overview of the process sits below.

How advisors usually charge

Fee structures vary, but the models are straightforward:

- Retainer: Best for longer planning work where readiness, reporting, and strategy unfold over time.

- Project fee: Useful for a discrete deliverable like readiness assessment, valuation gap review, or diligence prep.

- Success fee: Common when an advisor runs a sale process and is paid when a deal closes.

- Hybrid: A smaller monthly fee plus transaction-based compensation.

None of these models is automatically good or bad. The issue is incentive. If compensation only starts when a deal closes, don't expect deep readiness work unless it's explicitly in scope.

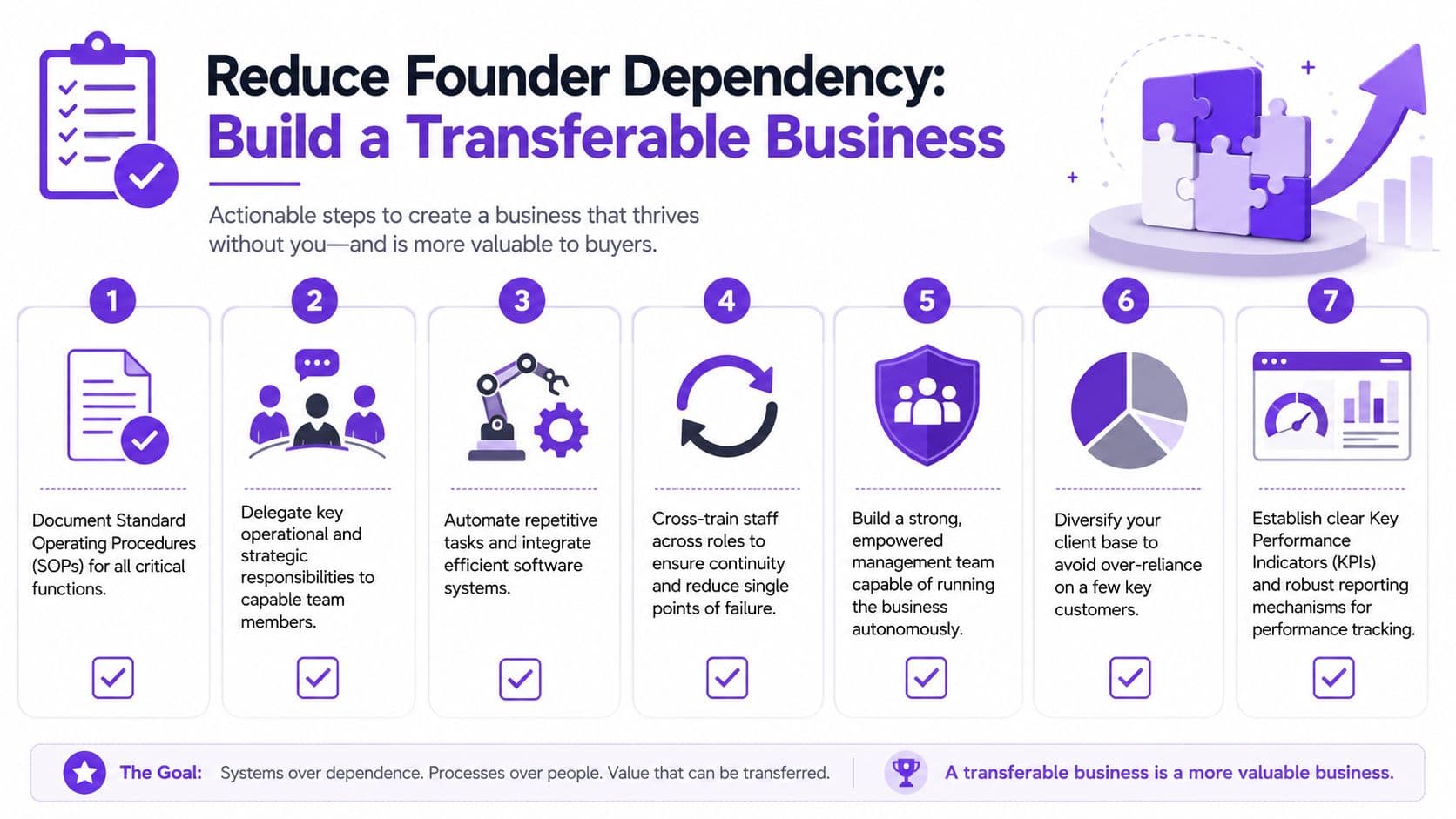

Building a Business That Can Exit Without You

Founder dependence cuts value fast in SaaS, agencies, and other service businesses. If the owner still owns the biggest client relationships, approves every exception, rescues delivery, and explains the numbers, a buyer sees fragile cash flow, not a transferable asset.

Buyers pay for a company that keeps producing after the founder steps out of the center. Bain's guidance on exit planning points to management continuity as a core issue because acquirers want proof the next phase of growth does not depend on one person (Bain guidance on exit planning and management continuity).

What transferable value looks like

Transferable value shows up in daily operations. Clients trust account leaders other than the founder. Sales stages move without owner intervention. Delivery follows documented handoffs. Reporting closes on time, and department heads can explain performance without waiting for the founder to interpret the numbers.

Use a simple test. Let the business run for two weeks with limited founder involvement. Then check what broke. If approvals stacked up, proposals stalled, clients asked for the owner, and the KPI meeting lost direction, the company is still organized around the founder.

That is not an M&A problem. It is an operating model problem.

For founders still carrying controller, operator, and decision-maker duties at the same time, it helps to understand what a company controller owns in a growing business. A surprising amount of founder dependence starts with finance never being built into a real function with clear ownership, cadence, and controls.

Buyers can replace a founder over time. They do not want to buy a company and then rebuild the management system from scratch.

A founder dependency checklist

Fix founder dependence in layers. One senior hire will not solve it if the business still routes decisions, context, and relationships through the owner.

- Document real SOPs: Write down how pricing gets approved, how deals move from sales to delivery, how change orders are handled, and who owns escalations.

- Shift customer ownership to the company: Put account managers, delivery leads, and functional leaders in front of clients long before a sale process starts.

- Delegate decision rights: Managers need authority limits, approval rules, and scorecards. Task delegation without decision rights keeps the founder in the loop.

- Strengthen revenue transferability: Clean contracts, disciplined renewals, clear scope control, and visible retention trends make recurring revenue easier to underwrite.

- Cross-train key roles: A business with one indispensable operator has the same transfer problem under a different name.

- Install leader-owned reporting: Weekly KPI reviews should run on a fixed cadence with metrics each department leader can explain and defend.

- Reduce concentration risk: Heavy dependence on a few clients, one rainmaker, or one acquisition channel will lower confidence and price.

- Build a second layer of management: Sales, operations, delivery, and finance each need a clear owner with accountability that survives founder absence.

This discipline matters in internal transitions too. The Exit Planning Institute notes that few family businesses make it cleanly across multiple generations (Exit Planning Institute value acceleration and succession data). Different ownership path, same operating lesson. If the business cannot run without the founder before the transition, the transition gets harder, slower, and less valuable.

Your First Step Toward a Successful Exit

A successful exit doesn't begin with a buyer list. It begins with financial clarity.

You need numbers that close on time, reconcile cleanly, explain performance, and support decisions. You need reporting that separates signal from noise. You need to know whether the business produces transferable cash flow or just founder-powered revenue. Without that foundation, an exit strategy consultant is working with guesswork.

Here's the simplest way to think about the path:

| Priority | What to fix first | Why it matters |

|---|---|---|

| Financial accuracy | Timely close, reconciled statements, revenue detail | Buyers test credibility before price |

| Operational proof | SOPs, org clarity, delegated accountability | Transferability drives confidence |

| Economic visibility | Margin analysis, cash flow insight, net proceeds modeling | You need to know if an exit is worth taking |

| Diligence readiness | Contracts, data room discipline, support files | Slow answers create buyer doubt |

| Founder independence | Management continuity and customer ownership | Reduces key-person risk |

If your books are late, your KPIs don't tie out, or your margin by client is a guess, don't start shopping for buyers. Fix the finance layer first. That gives you better options whether you sell, recapitalize, transfer to internal leadership, or hold and grow.

The right exit strategy consultant can guide the process. But no consultant can compensate for sloppy financials, undocumented operations, or a founder who still sits in the middle of everything.

Start where the impact is highest. Clean reporting. Reliable close. Cash flow visibility. Decision-grade numbers. Then build the rest of the exit plan on top of that.

If you want help getting the finance side exit-ready, Jumpstart Partners is a practical first call. Their outsourced controller team works with SaaS, agencies, and service businesses that need clean monthly closes, investor-ready reporting, KPI visibility, and due diligence support before a transaction is on the table. If you want more options later, get your numbers right now.