Financial Operations

How Do I Calculate Alternative Minimum Tax

Learn how do i calculate alternative minimum tax with this step-by-step guide for founders. Understand AMT triggers like ISOs & minimize your 2026 tax

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··14 min readIf you're asking how do I calculate Alternative Minimum Tax, you're usually already in the danger zone. AMT doesn't show up when your finances are simple. It shows up when your income, deductions, or equity comp stop behaving like a normal W-2 tax return.

For founders and executives, the primary problem isn't the math. It's the cash trap. You can trigger AMT from a paper gain, especially with stock options, and owe tax before you've turned that gain into cash. That's the kind of mistake that wrecks planning right when your company is gaining momentum.

Why the Alternative Minimum Tax Is a Trap for Founders

Most founders think tax gets complicated when they sell. That's too late. AMT often becomes a problem earlier, when you exercise options, stack deductions, or run into tax rules that treat your “good” tax planning as a red flag.

Why founders get hit harder

You're more exposed to AMT than a typical employee because your compensation and tax profile usually include items the regular tax system and AMT system treat differently.

A founder's common setup often includes:

- Equity compensation: Incentive Stock Options can create AMT income even when regular tax ignores the exercise.

- High state taxes: If you live in a high-tax state, deductions that help under regular tax may not help under AMT.

- Business asset purchases: If you use accelerated depreciation, AMT may force a different calculation.

- Lumpy income: A large bonus, liquidity event, or one-time gain can push a normal year into AMT territory fast.

That's why I don't treat AMT as a tax-prep issue. I treat it as a planning issue. If you wait until your return is being prepared, you've already lost your best options.

Bottom line: AMT is a parallel system designed to claw back some tax benefits that look perfectly normal under your regular return.

The founder mistake that creates the pain

The usual mistake is simple. You focus on valuation, exercise timing, and ownership percentage, but you ignore personal tax modeling. Then the tax bill lands after year-end, when the shares are still illiquid and the company cash isn't your personal ATM.

If your world includes options, founder stock, or nontrivial deductions, you need the same discipline in personal tax modeling that you already apply to your P&L. Founders who understand how tax reporting works for corporate filings usually grasp this quickly. Parallel systems create surprises when you assume one set of rules controls everything.

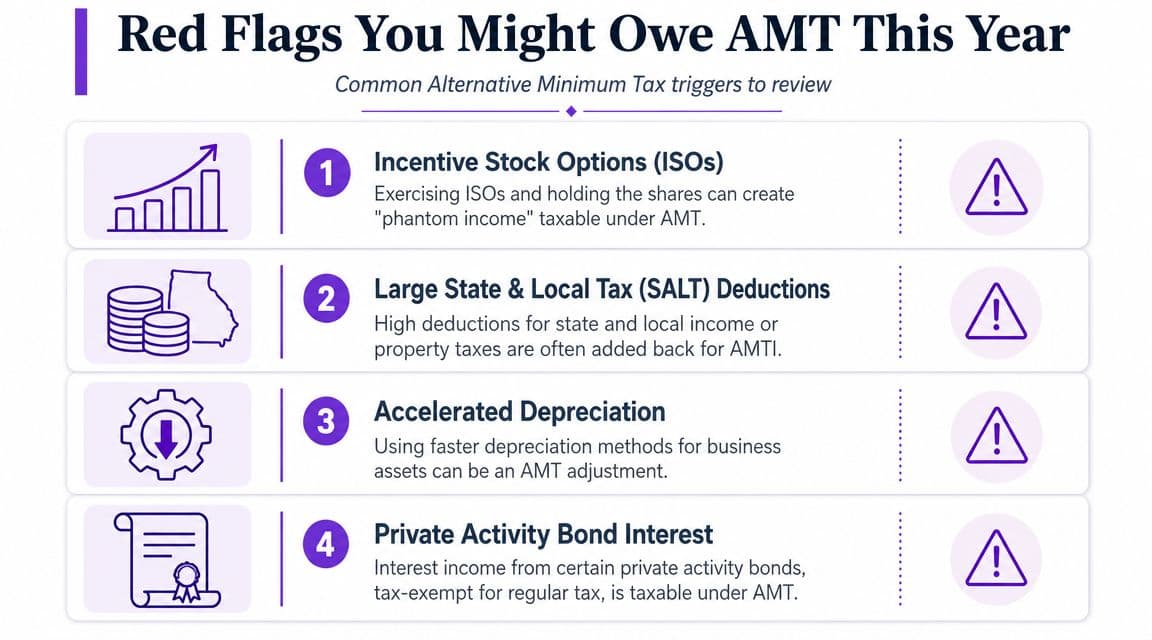

Red Flags That You Might Owe AMT This Year

AMT doesn't usually arrive out of nowhere. It leaves clues. If any of these apply to you, stop guessing and run the math.

You exercised ISOs and held the shares

This is the big one for startup operators.

When you exercise Incentive Stock Options, the spread between the strike price and the stock's value at exercise often doesn't hit your regular tax immediately. But AMT can treat that spread as income anyway. That's why founders end up with what people call phantom income. You owe tax on value you haven't monetized.

If you exercised this year and didn't sell before year-end, assume AMT is on the table.

Your state and local tax deductions are large

Founders in high-tax states often get blindsided here. A deduction that helps under the regular system can get added back for AMT purposes.

That doesn't automatically mean you owe AMT. It does mean your regular tax return is not a reliable proxy for your AMT exposure.

Your business uses accelerated depreciation

This matters most if you own a business with meaningful equipment, infrastructure, or other depreciable assets.

The IRS Form 6251 instructions make clear that depreciation differences must be adjusted separately for AMT, including current-year depreciation and capitalized amounts. The practical takeaway from the IRS instructions for Form 6251 is straightforward: you can't estimate AMT accurately with a rough marginal-rate shortcut.

Some deductions get added back. Some items are timed differently. AMT is a line-item exercise, not a cocktail-napkin estimate.

You hold interest from private activity bonds

This isn't the most common founder trigger, but it matters if your personal portfolio includes municipal bond exposure structured in a way that creates AMT income.

If your advisor has ever described part of your bond income as tax-exempt, don't assume that means tax-exempt under AMT too.

Quick red flag checklist

| Red flag | Why it matters for AMT |

|---|---|

| ISO exercise with no same-year sale | The exercise spread can become AMT income |

| Large SALT deductions | Amounts allowed or useful under regular tax may be added back |

| Accelerated depreciation | AMT may require a different depreciation calculation |

| Private activity bond interest | Income can be tax-exempt for regular tax but taxable for AMT |

What to do if you see two or more red flags

Don't wait for April. Build a current-year tax estimate and compare scenarios now. If you already manage quarterly estimated taxes for your business, apply that same discipline to your personal AMT exposure.

The mistake is thinking AMT is a filing problem. It's a forecasting problem.

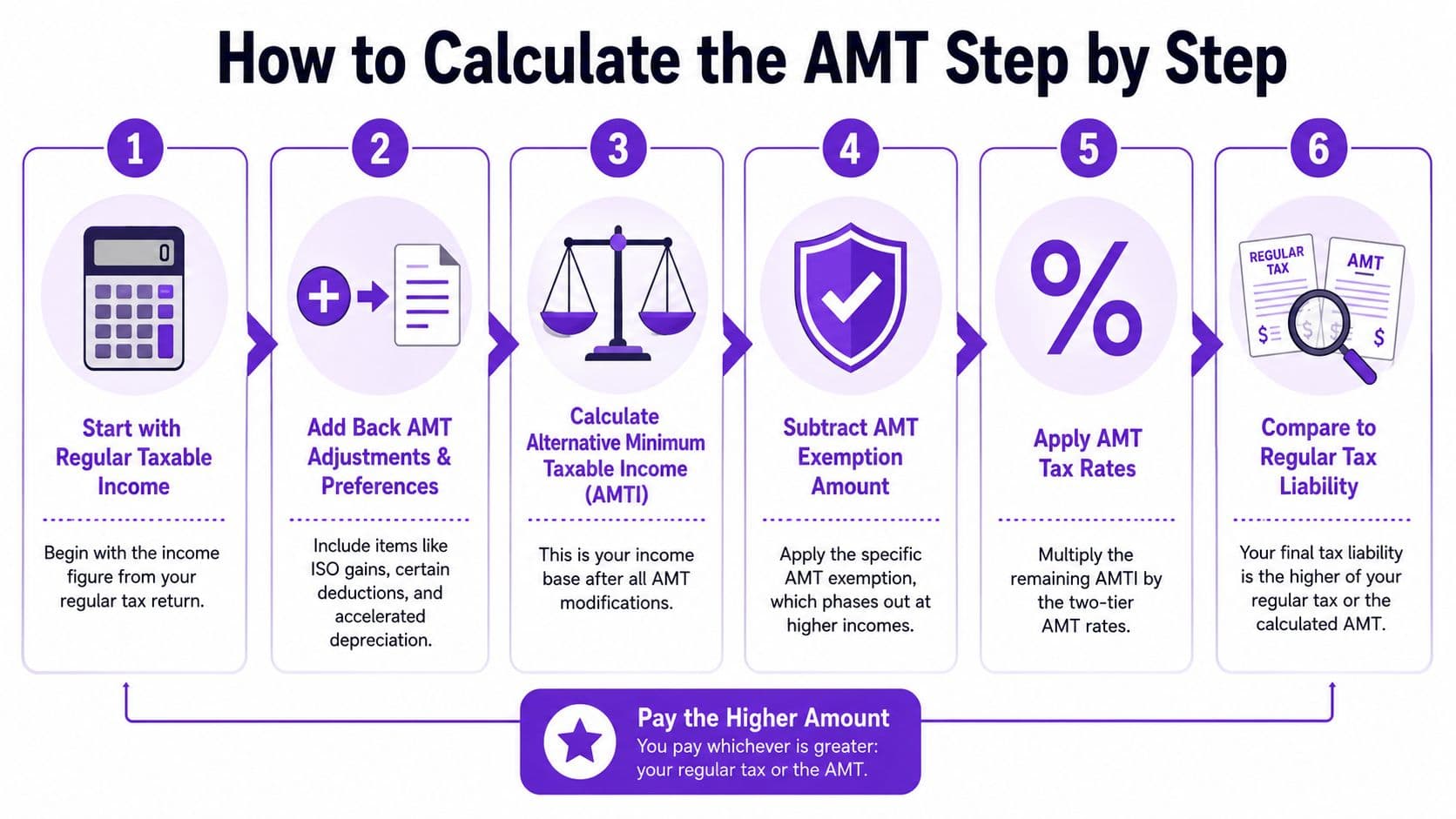

How to Calculate the AMT Step by Step

Founders usually get blindsided by AMT for one reason. The tax return shows one reality, but an ISO exercise or a few AMT adjustments can create a second tax system underneath it.

The calculation itself is not complicated. The inputs are.

The six-step logic

- Start with your regular taxable income

- Add back or modify AMT adjustments and preference items

- Arrive at Alternative Minimum Taxable Income, or AMTI

- Subtract the AMT exemption

- Apply the AMT rates

- Compare the result to your regular tax liability

That is the full framework. If you understand those six steps, you understand how AMT works.

A useful walkthrough sits below.

Step 1 through Step 3

Start with taxable income from your regular return. Then rebuild it under AMT rules.

For founders and executives, the adjustments that matter most are usually the ISO exercise spread, state and local tax deductions that do not help under AMT, private activity bond interest, and depreciation differences. If you run a growing software company, clean books matter here because your tax team needs accurate inputs across compensation, equity activity, and fixed assets. Good accounting for SaaS companies makes this calculation faster and a lot less error-prone.

After those adjustments, you have AMTI.

This is the point where many high earners get the math wrong. They look at regular taxable income and assume it already reflects an accurate economic picture. For AMT, it often does not. An ISO exercise can create a large AMT adjustment even if you did not sell a single share and did not receive cash.

Step 4 through Step 6

Once you have AMTI, subtract the exemption.

For tax year 2025, the exemption is $88,100 for single filers and $137,000 for married couples filing jointly. The exemption also phases out at higher income levels, which matters for founders with large option exercises or liquidity events.

Then apply the AMT tax rates. For 2025, the rates are 26% on the first layer of taxable AMT income and 28% above the threshold, with the exemption reduced as income rises, as summarized in Bench's AMT overview.

The final AMT liability is only paid to the extent tentative minimum tax exceeds regular tax.

Practical rule: Stop asking, “What's my AMT rate?” Ask, “What pushed up my AMTI, and did that push tentative minimum tax above my regular tax?”

Regular tax versus AMT treatment

| Item | Regular Tax Treatment | AMT Treatment |

|---|---|---|

| Taxable income base | Starts from regular taxable income | Recalculated after AMT adjustments |

| ISO exercise spread | Often not current regular taxable income at exercise | Can be included in AMTI |

| State and local tax deductions | May reduce regular taxable income | Often added back in AMT calculation |

| Depreciation | Regular tax method applies | AMT may require a separate depreciation adjustment |

| Final liability | Regular tax calculation | Only paid to the extent tentative minimum tax exceeds regular tax |

Worked Example A SaaS Founder's AMT Calculation

Let's make this concrete with a founder-style fact pattern.

Alex is a SaaS founder. She has $200,000 of salary. During the year, she exercises 50,000 ISOs with a $1 strike price when the company's value for exercise purposes is $6 per share. She also pays $25,000 in state income taxes.

This is the exact kind of scenario where AMT creates a nasty surprise.

Step one, calculate the ISO spread

The AMT-relevant spread is:

- Stock value at exercise: $6

- Strike price: $1

- Spread per share: $5

- Shares exercised: 50,000

- AMT adjustment from ISO exercise: $250,000

Under regular tax, that ISO exercise spread is not the same immediate problem. Under AMT, it becomes central.

Step two, build Alex's AMTI

Start with Alex's regular taxable income proxy from salary. Then layer in the AMT items.

| Calculation component | Amount |

|---|---|

| Salary income | $200,000 |

| ISO AMT adjustment | $250,000 |

| State tax amount that doesn't help under AMT | $25,000 |

| Estimated AMTI before exemption | $475,000 |

This simplified example ignores other moving parts so you can see the engine clearly.

At this point, Alex looks like someone with a normal founder salary on paper and a very different AMT profile in reality.

Step three, subtract the exemption and apply AMT rates

Assume Alex is single and use the 2025 exemption amount of $88,100 from the IRS rules cited earlier.

- AMTI: $475,000

- Less AMT exemption: $88,100

- AMT tax base: $386,900

Now apply the AMT rates described earlier:

- First $239,100 at 26%

- Remaining $147,800 at 28%

That creates a tentative minimum tax of:

- $239,100 × 26% = $62,166

- $147,800 × 28% = $41,384

- Tentative minimum tax = $103,550

Step four, compare to regular tax

Now compare that tentative AMT result with Alex's regular tax liability.

To keep the example grounded without inventing unsupported regular-tax bracket details, assume her prepared regular tax liability on the return comes out to $45,000 based on the full return mechanics.

That means:

- Tentative minimum tax: $103,550

- Regular tax liability: $45,000

- AMT owed: $58,550

That's the danger. Alex created a tax bill driven mostly by option exercise economics, not by cash she received.

The founder lesson isn't “don't exercise options.” It's “never exercise options without a tax model beside the cap table.”

If you run a subscription business and already track metrics carefully, you should bring the same rigor to your personal taxes. The discipline you use in SaaS accounting systems and revenue visibility should also show up in equity-comp planning.

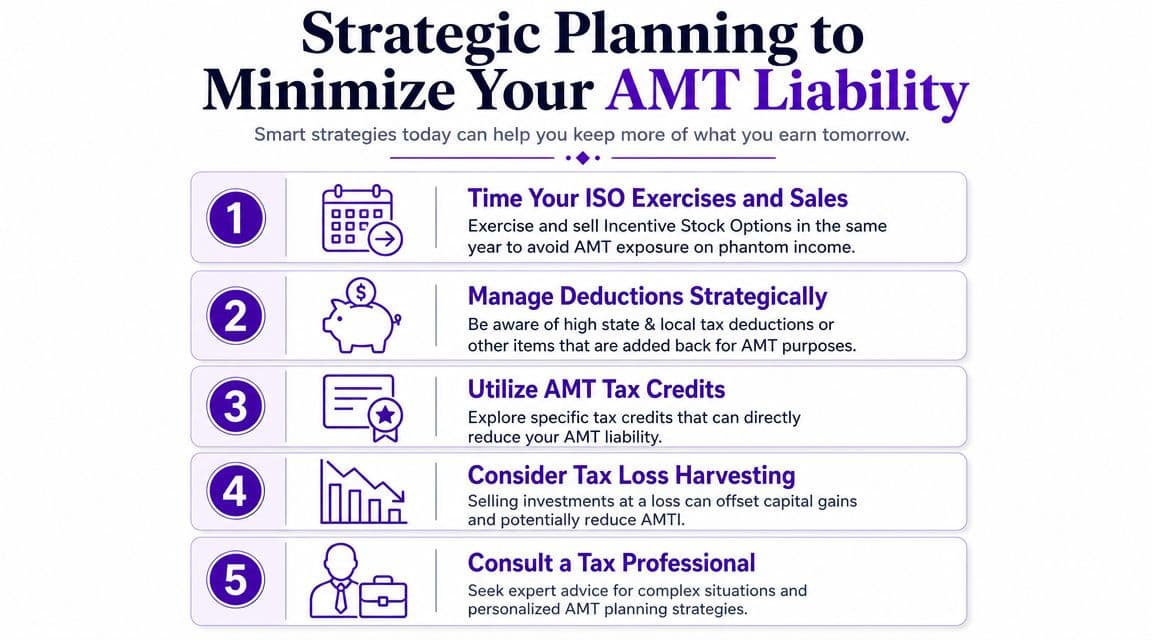

Strategic Planning to Minimize Your AMT Liability

Once you understand the mechanics, the right question changes. It stops being “How bad is the AMT hit?” and becomes “How do I control timing, character, and cash exposure?”

Control the option timeline

If AMT risk is being driven by ISOs, timing is your first lever.

A same-year exercise and sale often changes the tax outcome materially because you're not carrying that paper spread across year-end in the same way. In plain English, you reduce the odds of paying tax on value you still can't spend.

Another strong move is pacing your exercise activity across years instead of doing one oversized block. Founders love decisive moves. Tax planning often rewards controlled sequencing instead.

Manage the other add-backs

Don't focus only on stock options.

You should also review the items that make your AMT income diverge from your regular return. That includes state tax deductions, depreciation methods, and portfolio income with special treatment. If your business claims research incentives, keep those coordinated with the broader tax picture by reviewing related planning items such as R&D tax credits.

Don't waste the AMT credit

Founders often think AMT is always a permanent tax increase. That's wrong in many ISO-driven cases.

If your AMT came from a deferral-style item such as an ISO exercise, you may generate an AMT credit that can help reduce regular tax in future years when the comparison flips back in your favor. That doesn't erase the cash pain today, but it changes the long-term economics.

The best AMT planning doesn't chase tricks. It lines up exercise dates, sale strategy, liquidity needs, and future credit recovery.

A practical planning stack

Use this order:

- First, model exercise scenarios: Compare exercising now, splitting exercises, or pairing exercise with sale.

- Second, stress-test liquidity: Make sure personal cash can absorb a tax bill without leaning on company funds.

- Third, map future recovery: If you expect an AMT credit, build it into your multi-year personal tax plan.

- Fourth, coordinate investing decisions: If you're also managing gains and losses in a taxable portfolio, this wealth-building tax efficiency guide gives a useful framework for thinking about after-tax wealth, not just headline returns.

- Finally, review before year-end: AMT planning is much stronger in November than in March.

When to Stop Calculating and Call a CPA

You can understand AMT without becoming your own tax department. That's the right goal.

The IRS describes AMT as a separate system that starts with taxable income, adjusts it to arrive at AMTI, subtracts the exemption, applies AMT rates, and then compares that result against regular tax. For 2025, the exemption is $88,100 for single filers and $137,000 for married couples filing jointly, according to the IRS AMT overview. That buffer keeps many taxpayers out of trouble, but once preference items stack up, complexity rises fast.

Call a CPA if any of these are true

- You exercised a meaningful block of ISOs: Especially if you held the shares past year-end.

- You're near higher-income AMT territory: The exemption and phaseout mechanics make rough estimates unreliable.

- You own a business with substantial depreciable assets: AMT depreciation adjustments are technical and easy to miss.

- You're dealing with multiple tax systems at once: Founder equity, investment income, business ownership, and state tax issues create interaction effects.

- You need multi-year planning, not just a return: AMT credits, sale timing, and cash planning need scenario modeling.

My advice

Use DIY calculation for awareness. Use a CPA for decisions that affect six figures of taxes or liquidity.

That's especially true if your finances have moved beyond salary and simple deductions. If your situation is growing into a more complex finance function, it helps to work with professionals who understand both tax coordination and broader financial operations, including virtual accounting support for scaling companies.

AMT isn't scary because it's mysterious. It's expensive because smart people assume a quick estimate is good enough. It isn't.

If you want finance support that helps you make better decisions before tax surprises show up, Jumpstart Partners works with growing businesses that need clean books, sharper reporting, and CFO-level financial clarity. When your business finances are tight, your personal tax planning gets easier too.