Financial Operations

R&D Tax Credits: Unlock Savings for SaaS & Agencies 2026

Unlock significant cash savings with R&D tax credits. SaaS & agency founders: identify qualifying activities, calculate savings, and claim correctly in 2026.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readMost founders treat R&D tax credits like a tax project. That's the wrong frame. This is a funding lever.

The federal credit has been around since 1981, and annual federal credits now exceed $12 billion according to Alliantgroup's overview of the credit's evolution. That tells you two things. First, this isn't a niche loophole. Second, the companies that document well keep using it year after year.

For SaaS companies, agencies, and technical service firms, the practical question isn't whether the rules are complex. They are. The critical question is whether you're willing to leave a legitimate, non-dilutive source of cash on the table because your books, payroll coding, and project records are messy.

Your Guide to the R&D Tax Credit

Federal R&D credits now represent billions of dollars a year in claimed tax value across U.S. businesses. Founders still miss them for a simple reason. Their accounting does not translate product work into a defendable tax position.

If you pay engineers, developers, technical product staff, or implementation teams to solve technical problems, review this credit before year-end close, not after the return is drafted. The credit can reduce income tax liability dollar for dollar, and ADP notes that many companies see credit value in the range of 6% to 10% of qualified spend. Qualified small businesses may also apply up to $500,000 annually against payroll tax liability under current rules, according to ADP's R&D tax credit guide. For an early-stage SaaS company burning cash, that is not a technical tax detail. It is runway.

Here is the mistake I see across startup portfolios. Finance teams track payroll by department, not by qualifying activity. Product and engineering teams document work in Jira, GitHub, Slack, and client statements of work, but nobody maps that record set back to wages, contractor costs, and project timelines. By tax time, the company may have done qualifying work all year and still lack a claim file that holds up under scrutiny.

That gap matters even more for agencies and hybrid service businesses. If your team builds internal tools, client delivery automation, custom integrations, or proprietary reporting workflows, your books need to separate routine service labor from technical experimentation. If that split is messy, start by tightening your accounting system for agencies and technical service firms.

Use this framework.

- Profitable company. Apply the credit to reduce current income tax liability.

- Pre-profit startup. Evaluate the payroll tax offset election and confirm you meet the small business rules.

- Scaling company with weak records. Fix payroll coding, project tracking, and contractor support before you file.

My recommendation is simple. Treat the R&D credit as a bookkeeping workflow first and a tax form second. If your chart of accounts, payroll mapping, and project documentation are clean, the claim gets faster, stronger, and easier to defend. If they are not, the credit becomes an expensive cleanup exercise.

Some founders also pair credits with grants and other non-dilutive funding. If that is part of your capital plan, explore Documind's grant advice and make sure the same finance records can support both applications.

Eligibility for SaaS and Agency Businesses

R&D tax credits aren't just for biotech labs or manufacturers. If you run a SaaS business, a productized agency, or a technical services firm, the issue is whether your work meets the IRS test, not whether your office has lab equipment.

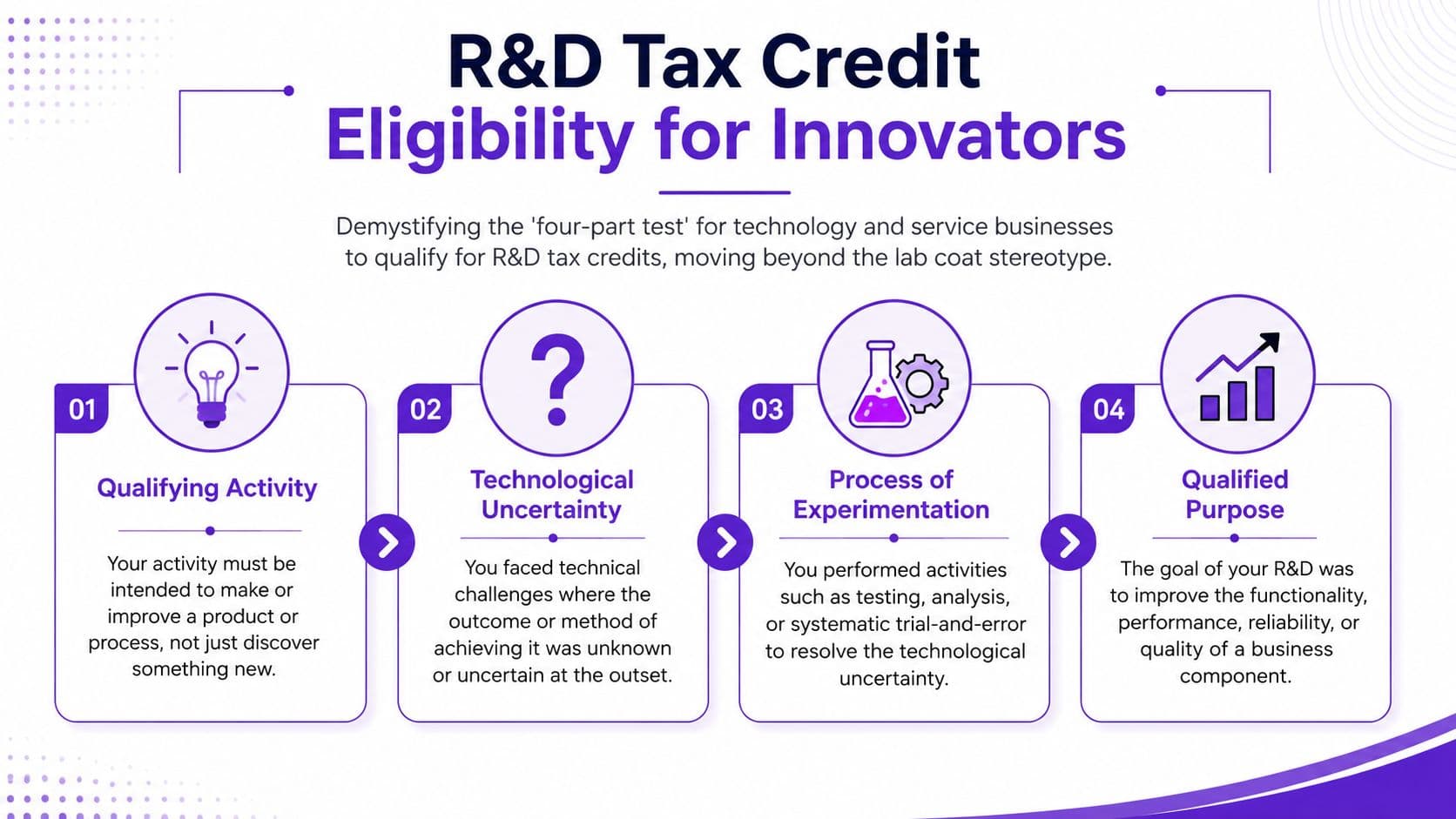

The IRS four-part test under IRC §41 is the core screen. To qualify, your work must be for a permitted purpose, eliminate technical uncertainty, be technological in nature, and involve a process of experimentation. KBKG puts the key point clearly in its guidance: commercial success isn't what substantiates a claim. Evidence of systematic trial-and-error does.

The four-part test in plain English

Permitted purpose

You must be trying to create or improve a business component. For a SaaS company, that can mean a new product feature, a reporting engine, a workflow automation layer, or a performance improvement to your platform. For an agency, it can mean a proprietary tool, internal platform, or custom client-facing system.

Technical uncertainty

At the start, you didn't know whether you could solve the problem or what the best method would be. That's common in software work. Examples include redesigning architecture to handle scale, building an API sync across messy third-party systems, or creating a custom data model that has to balance speed and accuracy.

Technological in nature

The work needs to rely on technical principles such as computer science or engineering. Design taste, copywriting, ad strategy, and routine account management don't qualify on their own. Your engineering sprint does. Your media buying brainstorm doesn't.

A state-specific tax advisor can matter when your team structure and nexus issues complicate the picture. If you're operating in California, this guide to a California tax advisor for startups is a useful parallel resource for sorting state-level complexity alongside the federal rules.

To make this concrete, here's where many agencies get confused. Client service work is not automatically excluded. If your team is building a custom technical solution, facing real uncertainty, and testing alternative methods, parts of that work can qualify. If you're executing a standard website build from an established playbook, it usually won't.

SaaS and agency examples that often qualify

-

SaaS platform work

Building a new recommendation engine, redesigning system architecture for reliability, or experimenting with database structures to improve performance. -

Agency technical delivery

Creating a proprietary attribution model, custom analytics pipeline, or complex middleware that stitches together platforms with unstable or incomplete APIs. -

Internal-use software

Developing internal tooling for scheduling, forecasting, provisioning, or QA where the team had to solve technical uncertainty.

Here's a practical accounting angle. If your team can't isolate those projects in the GL, job-cost reports, or payroll allocations, your eligibility may be real but your claim will still be weak. That's why project-based bookkeeping matters, especially for agencies. If you're cleaning up that side of the house, review this breakdown of accounting for agencies.

Later in the process, technical stakeholders usually ask for a simpler walkthrough than the tax memo. This short video does that well:

The credit rewards disciplined experimentation. It doesn't require a blockbuster product launch.

How to Calculate Your Potential Credit

Founders usually ask the same question first. "How much is this worth?"

For planning purposes, use a simple operating estimate before your tax team runs the formal computation. One practical benchmark is an estimated federal credit of about 7% of qualified research expenses under an ASC-style planning model. That's not your filed result. It's a rough planning tool so you can decide whether the exercise deserves attention now.

What goes into qualified research expenses

The categories that commonly matter are:

- Qualified wages for employees directly performing, supervising, or supporting qualified research

- Qualified supplies used in experimentation

- Qualified contract research in the eligible category

That means your developer payroll often drives the largest piece of the claim. Supervisors can count too when they're directly overseeing qualified work. Contract spend can matter, but only if it's captured cleanly and tied to actual technical projects.

Sample R&D tax credit calculations

| Company Profile | Annual Revenue | Qualified Wages | Qualified Supplies | Qualified Contract Research | Total QREs | Estimated Federal Credit (~7%) |

|---|---|---|---|---|---|---|

| Digital agency | $1,000,000 | $180,000 | $20,000 | $50,000 | $250,000 | $17,500 |

| SaaS company | $5,000,000 | $900,000 | $100,000 | $200,000 | $1,200,000 | $84,000 |

| Technology firm | $20,000,000 | $3,000,000 | $300,000 | $700,000 | $4,000,000 | $280,000 |

These examples are illustrations for planning. They show why founders should care. Even a modestly sized claim can fund hiring, extend runway, or reduce pressure on collections and cash reserves.

Worked examples founders can use

A digital agency with $250,000 of total qualified research expenses would estimate a credit of $17,500 at a 7% planning rate. That's not life-changing by itself. But for a business with tight cash conversion and founder-led finance, it absolutely pays for the effort if the records are solid.

A SaaS company with $1,200,000 of qualified research expenses would estimate $84,000. That's the kind of number that starts affecting how you think about product hiring and tax provision planning.

Decision lens: If your technical payroll is meaningful and you've never done an R&D study, run a back-of-the-envelope QRE model this quarter. Don't wait for year-end.

The challenge isn't arithmetic. It's confidence in the inputs. If your payroll mapping is weak, your estimate is fiction. If you want a framework for whether stronger finance support pays for itself, this analysis of controller services ROI is worth reading before you start the claim process.

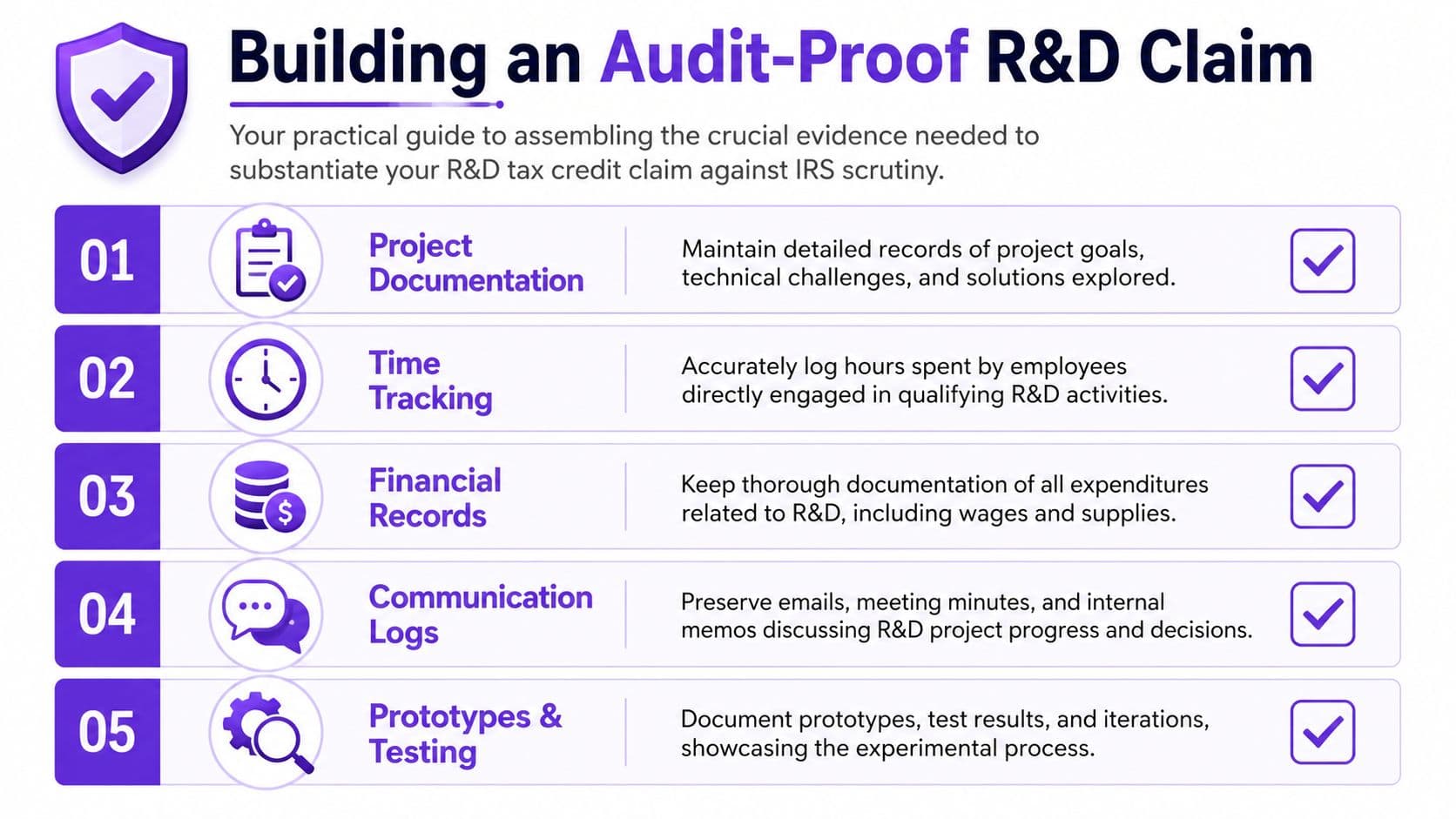

Essential Documentation for an Audit-Proof Claim

An R&D claim stands or falls on documentation. Not your enthusiasm. Not your product roadmap. Not your founder story.

The IRS test is evidence-based, so your file needs to show who worked on what, what technical uncertainty existed, what alternatives were tested, and how the underlying costs tie back to the work. If you build that package as you go, the claim is manageable. If you try to recreate it after the books are closed, it turns into expensive archaeology.

What your file should contain

Technical project records

Keep project briefs, sprint plans, engineering tickets, architecture notes, Git-based release records, QA logs, and test results. These documents help show the permitted purpose, the technical uncertainty, and the process of experimentation.

Time and payroll support

You need payroll records tied to employees involved in qualified work. For many companies, this means job-role mapping plus a defensible time allocation methodology. If you don't track time by project, create a contemporaneous process now. Retroactive estimates are weaker.

Expense support

Capture supply and contractor costs in accounts that map cleanly to projects. If you bury testing tools, cloud sandbox costs, and contractor invoices inside generic expense buckets, you'll struggle to support your QRE calculation.

A practical checklist for finance leaders

- Project-level naming discipline. Use consistent project codes across Jira, Asana, Monday.com, or your engineering tracker and mirror those codes in accounting where possible.

- Meeting records with substance. Save technical meeting notes that reflect design alternatives, failed approaches, and decision points.

- Version evidence. Keep prototypes, alpha releases, test environments, and documented iteration history.

- Contractor backup. Retain statements of work, invoices, and deliverable descriptions that show technical work, not just vague "development services."

- Payroll tie-out. Reconcile claimed wage amounts back to payroll reports and the general ledger.

A strong claim reads like an operating file, not a tax memo assembled at the last minute.

One more point. Founders often think "audit-proof" means over-documenting everything. It doesn't. It means documenting the right things in a way that ties operations to accounting. If your retention practices are inconsistent, fix them. This guide on how long to keep business records is a useful baseline for tightening policy before you build a formal credit file.

Where documentation usually breaks

The weak spots are predictable:

| Weak area | What goes wrong |

|---|---|

| Product and finance don't coordinate | Engineering knows the story, finance can't support the dollars |

| Payroll isn't allocated | Developer wages are real, but the claim can't isolate qualified time |

| Contractor invoices are vague | You know work happened, but the invoice language doesn't prove what qualified |

| Teams rely on memory | The file gets rebuilt after year-end and credibility drops |

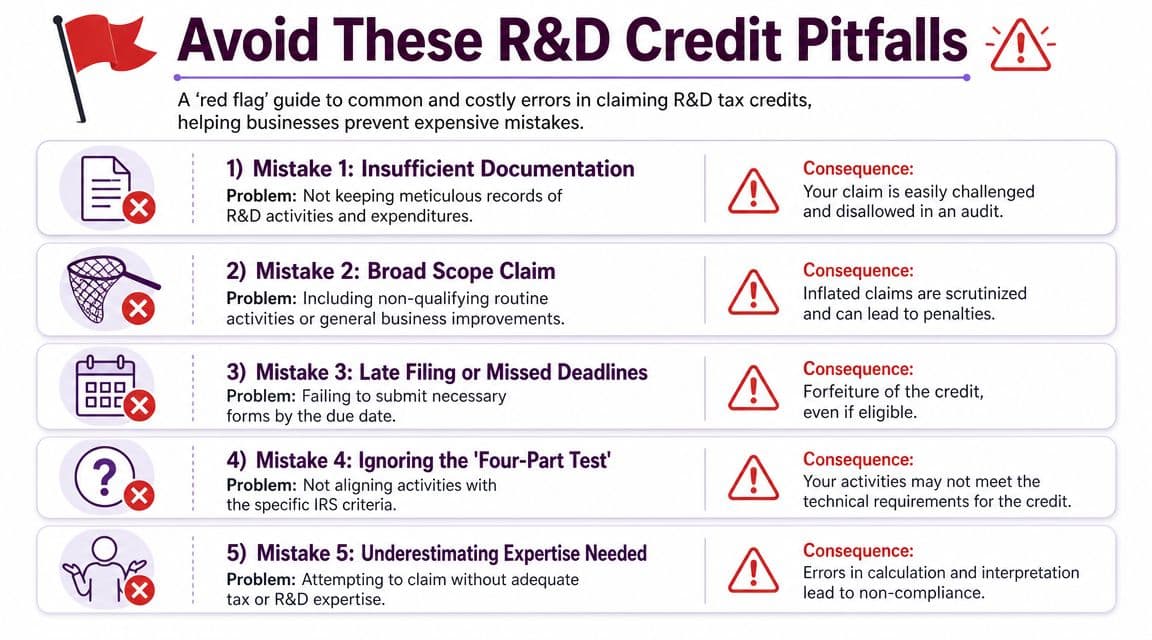

Common Pitfalls and Expensive Mistakes to Avoid

Most bad R&D claims don't fail because the company had zero qualifying work. They fail because the company overreached, under-documented, or ignored the tax interaction that changes the net benefit.

The biggest strategic mistake I see is founders focusing on the gross credit and never modeling the full tax effect. That's sloppy finance.

Mistake one, ignoring the no-double-benefit rule

Under IRC §280C, you must reduce the related deduction by the amount of the credit claimed. Bloomberg Tax also notes that post-2022 Section 174 rules generally require domestic research expenditures to be capitalized and amortized over 5 years, with foreign research over 15 years, which changes the timing of your tax benefit and the way you should model cash impact. Their explanation also highlights that the regular credit and alternative simplified credit can produce different results depending on your fact pattern, so your finance team should model the net effect, not the headline percentage, using Bloomberg Tax's discussion of the R&D credit and deducting R&D expenditures.

That means a founder who says, "Great, we get the credit and still deduct all the expense immediately," is making a bad assumption.

Mistake two, claiming routine work

Routine bug fixes, basic design refreshes, ordinary implementation, and standard client delivery often get stuffed into the claim because someone wants a bigger number. That's how you create a file that attracts scrutiny.

Use a harder filter:

- Keep it in when the team faced technical uncertainty and tested alternatives.

- Keep it out when the work followed a known process with no meaningful technical experimentation.

- Split mixed projects instead of treating the whole project as qualified.

Mistake three, making the wrong payroll tax election

Loss-making startups love the payroll tax offset. Sometimes that's the right move. Sometimes it isn't.

If you're near breakeven, expecting taxable income soon, or anticipating a financing event that changes your tax position, you should model whether using the credit against payroll taxes now is better than preserving credits for future income tax use. The wrong election isn't fatal, but it's often expensive in opportunity cost.

Warning sign: If nobody on your team has built a simple side-by-side model for payroll offset versus carryforward, you're making a tax election blind.

Mistake four, running the claim on dirty books

A messy ledger leads to inflated wages, missed contractor exclusions, and unsupported allocations. If you have uncategorized payroll journals, duplicate vendors, or developer time that never maps to projects, fix the accounting before you size the claim.

QuickBooks cleanup is often the first real step, not the last. If your books are carrying old errors, duplicate coding, or broad expense buckets, start with a proper QuickBooks cleanup service review before you ask anyone to defend the numbers.

How Outsourced Controllers Streamline Your R&D Claim

The R&D credit has been around for decades. Founders still lose it for a simple reason. Their books cannot support the story their tax advisor is trying to tell.

For SaaS companies and agencies, the problem is rarely the tax form. The problem is the finance stack underneath it. If payroll is coded by department instead of project, if contractors sit in one broad expense bucket, or if nobody closes the books on time, your claim turns into a manual reconstruction exercise. That costs time, fees, and credibility.

An outsourced controller fixes the operating mechanics that make the claim defensible.

What a controller should build before the tax study starts

A controller should set up a monthly process that ties technical work to clean financial records. That means engineering, product, delivery, payroll, AP, and the general ledger all use the same project structure and naming rules. It also means your finance team can answer basic audit questions in minutes instead of rebuilding support from old Slack threads and half-finished spreadsheets.

| Finance system | Why it matters for the claim |

|---|---|

| Project-based expense tracking | Connects qualified work to actual spend |

| Payroll mapping by employee and project | Supports wage allocations you can defend |

| Contractor coding rules | Separates qualified technical work from general outside services |

| Monthly reconciliations | Catches missing payroll entries, duplicate vendors, and miscoded costs before year-end |

| Document retention workflow | Keeps invoices, sprint records, and accounting support tied to the same project file |

That is the gap generic tax guides miss. The credit is won or lost in bookkeeping discipline, payroll mapping, and monthly close quality.

Why outsourced support works better

Year-end cleanup is expensive. A controller-led process built during the year is cheaper and stronger.

Good outsourced controller support sets up the chart of accounts, project classes, payroll allocation logic, close checklist, and document retention rules before the tax specialists calculate the credit. That sequence matters. If you start with the study, you usually end up paying someone to translate messy books into a number you still may not be able to defend.

One practical option is outsourced controller services, especially for SaaS and agency businesses that need project coding, cleaner month-end reporting, and finance controls that hold up under tax review.

If your team is buried in manual receipt capture, invoice coding, and AP rework, the benefits of accounting automation for small businesses are worth reviewing before you tighten the R&D workflow. Better automation improves coding consistency and gives the controller cleaner inputs to work with.

What I would have a founder do this quarter

- Create an R&D project list for the current year, not just at tax time.

- Map employees to projects using payroll data that matches how work was staffed.

- Separate contractors by role and scope so technical work is not mixed with general service spend.

- Close the books monthly and review project-level P&L detail while the facts are still fresh.

- Store support in one place with payroll reports, invoices, Jira exports, Git activity, and project notes tied to the same jobs.

- Hand the tax advisor a clean package instead of asking them to reverse-engineer your ledger.

This is how finance teams cut claim friction. Clean books reduce CPA fees, shorten the study timeline, and improve the odds that the credit survives scrutiny.

If your SaaS company or agency has technical payroll, messy project coding, or no clear documentation trail, talk to Jumpstart Partners. They can help get the books, payroll allocations, and monthly controls into shape so an R&D credit claim is based on evidence instead of estimates.