Financial Operations

How to Calculate Cash Burn: A Founder's Practical Guide

Learn how to calculate cash burn (gross and net) and runway. A step-by-step guide for SaaS and agency founders with examples from QuickBooks and Xero.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··16 min readMost founders track revenue more closely than cash. That's backward. A business can post a decent month on paper and still run into a cash crunch because burn is a cash question, not an accounting-profit question.

The practical benchmark is monthly. Burn is usually tracked as a monthly metric, then paired with runway. One standard example: a business with $10 million in cash and a $500,000 monthly burn has 20 months of runway, as shown in this monthly burn and runway example. That's why serious operators don't ask, “Are we profitable on the P&L?” They ask, “How much cash did we consume this month, and how long does that leave us?”

If you want to know how to calculate cash burn correctly, start with cash movements, not accounting noise. Then translate that number into decisions about hiring, pricing, collections, and fundraising timing.

Table of Contents

- Calculate Gross and Net Burn The Right Way

- Convert Your Burn Rate into Cash Runway

- Find Your Burn Numbers in QuickBooks Xero and Stripe

- Refine Your Burn for SaaS and Agency Models

- Avoid These Common Cash Burn Calculation Mistakes

- Your Burn Rate Is High Now What

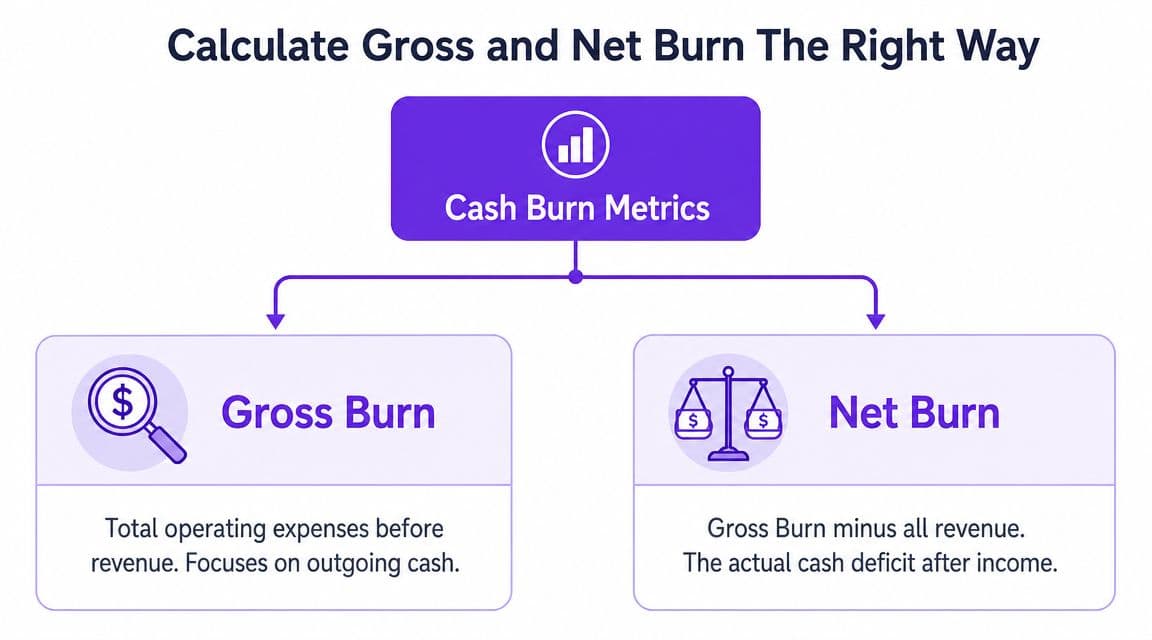

Calculate Gross and Net Burn The Right Way

Start with the two numbers that matter

There are two burn metrics you need to separate immediately.

Gross burn is your total monthly cash operating expenses. Think payroll, contractor spend, software subscriptions, rent, paid media, and other cash costs required to run the business. Net burn is cash outflows minus cash inflows. That's the number that tells you whether cash is leaving the building after customers pay you.

According to this cash burn overview from Defacto, cash burn is typically calculated in two forms: gross burn equals total monthly cash expenses, and net burn equals cash outflows minus cash inflows. The same source gives a simple example where a company starts the month with €500,000 and ends with €400,000, producing a €100,000 net burn for that month.

If your books are messy, fix your underlying transaction hygiene before you obsess over formulas. Founders who get disciplined about managing cash disbursements usually get cleaner burn reporting fast, because they stop letting vendor payments, reimbursements, and timing errors blur the picture.

Practical rule: Track both metrics every month, but manage the business off net burn.

A lot of founders also trip over basic bookkeeping structure. If your chart of accounts is inconsistent, your burn calculation will be inconsistent too. This quick guide to basic formulas of accounting is worth reviewing if your finance stack still feels improvised.

A simple worked example

Use a monthly period. Don't switch between weekly, quarterly, and monthly numbers unless you enjoy bad decisions.

Here's a clean example:

| Item | Monthly cash amount |

|---|---|

| Payroll | included in gross burn |

| Software | included in gross burn |

| Rent and overhead | included in gross burn |

| Marketing spend | included in gross burn |

| Total cash operating expenses | $120,000 |

| Cash collected from customers | $80,000 |

| Net burn | $40,000 |

The math is simple:

- Gross burn = total monthly cash operating expenses

- Net burn = cash outflows minus cash inflows

- In this example, $120,000 - $80,000 = $40,000 net burn

That tells you something useful immediately. Your company isn't just “spending a lot.” It's consuming $40,000 of cash each month after customer cash receipts.

If you only track gross burn, you'll overreact. If you only track revenue, you'll underreact.

One more practical recommendation. Don't rely on a single month if your collections are uneven. Defacto notes that some teams use a three-month trailing average to smooth one-time expenses or delayed customer payments in runway planning, as noted in that earlier source. That's the right move for founders who run agencies, services firms, or SaaS businesses with annual prepaids landing unevenly.

Convert Your Burn Rate into Cash Runway

Runway sets your decision deadline

Runway tells you how long your cash lasts at your current net burn. That number should drive hiring, sales targets, and cost cuts.

The formula is simple:

Cash runway = cash balance ÷ monthly net burn

If you have $1,000,000 in cash and your monthly net burn is $50,000, you have 20 months of runway. If you have $300,000 in cash and burn $20,000 per month, you have 15 months.

| Cash balance | Monthly net burn | Runway |

|---|---|---|

| $1,000,000 | $50,000 | 20 months |

| $300,000 | $20,000 | 15 months |

You can also back into runway from actual cash movement. If cash dropped from $150,000 on January 1 to $90,000 on March 31, you burned $60,000 over three months, or $20,000 per month. That approach is useful when you want a quick check against what QuickBooks, Xero, or Stripe activity suggests.

Treat runway like an operating trigger

Founders get in trouble when runway sits in a deck instead of running the business. Put clear thresholds around it.

At 12 months, freeze nice-to-have spending and tighten collections.

At 9 months, decide whether you are cutting burn, raising capital, or pushing pricing harder.

At 6 months, act. Headcount plans, vendor contracts, and owner draw decisions should already be changing.

That is the value of runway. It forces timing.

Use net burn, not gross burn, for this calculation. Gross burn tells you how expensive the company is to operate. Net burn tells you how fast cash is leaving the bank. For SaaS companies with annual prepaids or agencies with lumpy client payments, use a trailing average and then test a downside case where collections come in late.

Ask these four questions every month:

-

What is today's true cash balance?

Use cash you can spend now. Exclude restricted cash and undrawn fantasy. -

Is net burn rising for a good reason?

A planned sales hire is one thing. Slower collections and bloated payroll are another. -

What happens if customer cash slips for 30 to 60 days?

Run a short-term forecast, not just a static runway calculation. A 13-week cash flow forecast template and process will show pressure earlier than your month-end reports. -

What is the action date, not just the runway number?

If you have 8 months of runway and fundraising will take 6, your deadline is now.

If you need a budgeting framework alongside runway planning, this strategic guide for UAE businesses is a useful reference.

Runway is not a vanity metric. It is your clock. Use it before it forces the decision for you.

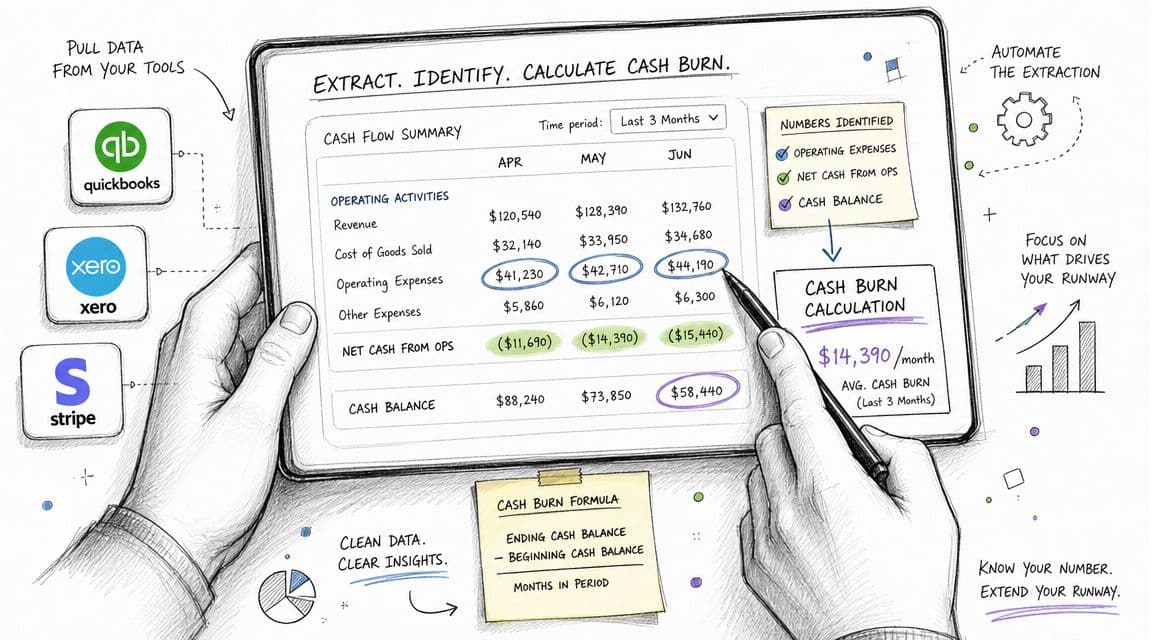

Find Your Burn Numbers in QuickBooks Xero and Stripe

Most burn calculations go wrong before the math starts. The problem isn't arithmetic. It's pulling numbers from the wrong reports.

QuickBooks and Xero first

If you're in QuickBooks or Xero, don't start with the P&L if your goal is to calculate cash burn. Start with cash movement.

The most reliable starting point is your Statement of Cash Flows, specifically the operating section. You're trying to isolate cash used by normal operations, not debt proceeds, owner distributions, or equipment purchases.

Use this process:

-

Run the Statement of Cash Flows for a consistent monthly period

Don't compare a partial month to a full month. -

Focus on operating activity

You want the lines tied to cash generated or consumed by day-to-day operations. -

Strip out financing and investing noise

Loan proceeds, equity injections, and asset purchases matter to total cash, but they don't describe operational burn. -

Cross-check against bank movement

If the report says one thing and your bank balances say another, trust the reconciliation process, not your assumptions.

For founders building better reporting discipline, this walkthrough on how to track business expenses helps tighten the categories that feed your burn number.

A lot of international or multi-entity teams also need budgeting discipline around forecast structure, not just bookkeeping cleanup. If that's your situation, this strategic guide for UAE businesses is a useful reference on how to think about budgeting and forecasting in a more operational way.

Stripe is for cash timing not revenue recognition

Stripe gives you a different piece of the puzzle. It tells you about collections timing.

For burn analysis, the important Stripe views are the ones that show:

- Gross payment volume

- Fees withheld

- Net amounts

- Actual payouts to your bank account

That last one matters most for cash burn. A booked sale isn't cash in the bank yet. A successful charge with a delayed payout can still leave you tight on payroll week.

The founder mistake is treating Stripe revenue as bank cash. It isn't the same thing.

Use Stripe to answer questions like these:

| Question | Stripe view to inspect | Why it matters |

|---|---|---|

| What did customers pay? | Gross volume | Helps explain top-line collection activity |

| What did Stripe keep? | Fees and adjustments | Affects actual cash received |

| What hit the bank? | Payouts | This is the inflow relevant to burn timing |

After you map this once, your monthly process becomes simple: accounting system for the operating cash view, bank accounts for validation, Stripe for inflow timing.

Here's a practical explainer if you want to see a visual walkthrough of cash flow reporting in action:

Build one source of truth

Don't let QuickBooks, Xero, Stripe, and your bank all tell different stories in your management meeting.

Set one monthly close process:

- Lock the period so categories don't keep moving.

- Reconcile bank and Stripe timing differences before reporting burn.

- Record owner draws, debt, and one-offs separately so you don't confuse operating burn with capital activity.

- Use the same report package every month so trend comparisons mean something.

If you want an outside team to own that reporting process, one option is Jumpstart Partners, which provides outsourced controller and bookkeeping support for businesses using tools like QuickBooks, Xero, and Stripe.

Refine Your Burn for SaaS and Agency Models

A generic burn formula is fine for a textbook. It's not enough for a SaaS company or an agency.

SaaS founders need to separate cash from service obligations

SaaS businesses often collect cash before they deliver service over time. That creates a trap. Your bank balance can look stronger than your underlying monthly economics.

Say you collect an annual prepayment from a customer. Cash improves immediately. That helps liquidity. But if you treat that one payment as proof that monthly burn is solved, you'll overestimate stability. You still need to fund payroll, support, product work, and customer success across the service period.

Use two lenses:

- Cash lens for immediate liquidity and runway

- Operating lens for whether recurring collections are keeping pace with recurring cash needs

This is why SaaS cash forecasting needs to account for billing cadence, payment processing fees, churn, renewals, and expected collection timing. If you want a more customized framework, this guide on SaaS cash flow forecasting is the right companion to your burn model.

A prepaid annual contract improves cash today. It does not erase the cost of serving that customer tomorrow.

Agencies need to obsess over timing

Agencies and professional services firms have the opposite problem. Revenue can look healthy while cash gets squeezed by timing.

You invoice after milestones. Clients pay late. Payroll still lands on schedule. Media spend, freelancers, and software vendors still want payment. Burn becomes a working-capital issue fast.

This is exactly why Stripe's burn-rate guidance says runway is more meaningful for businesses with lumpy receipts when it's paired with a 13-week cash forecast, especially for agencies or e-commerce firms, in this Stripe resource on burn rate. The same source notes that Carta's 2024 State of Private Markets showed median startup burn multiples stayed near 1x, which has pushed more attention onto near-term liquidity. It also asks the better question: how much of burn is structural versus timing-driven, and what changes if collections slip by 15 to 30 days.

That's the frame smart operators use.

| Business model | What usually distorts burn | What to do |

|---|---|---|

| SaaS | Annual prepaids, churn, processor fees | Separate collection timing from recurring service costs |

| Agency | Delayed receivables, milestone billing, payroll cycles | Run a weekly cash forecast, not just a monthly burn report |

If you run an agency, your monthly burn number should never stand alone. Pair it with a weekly collections view, expected payroll dates, and large vendor commitments. That's how you avoid the awful surprise of “profitable quarter, empty bank account.”

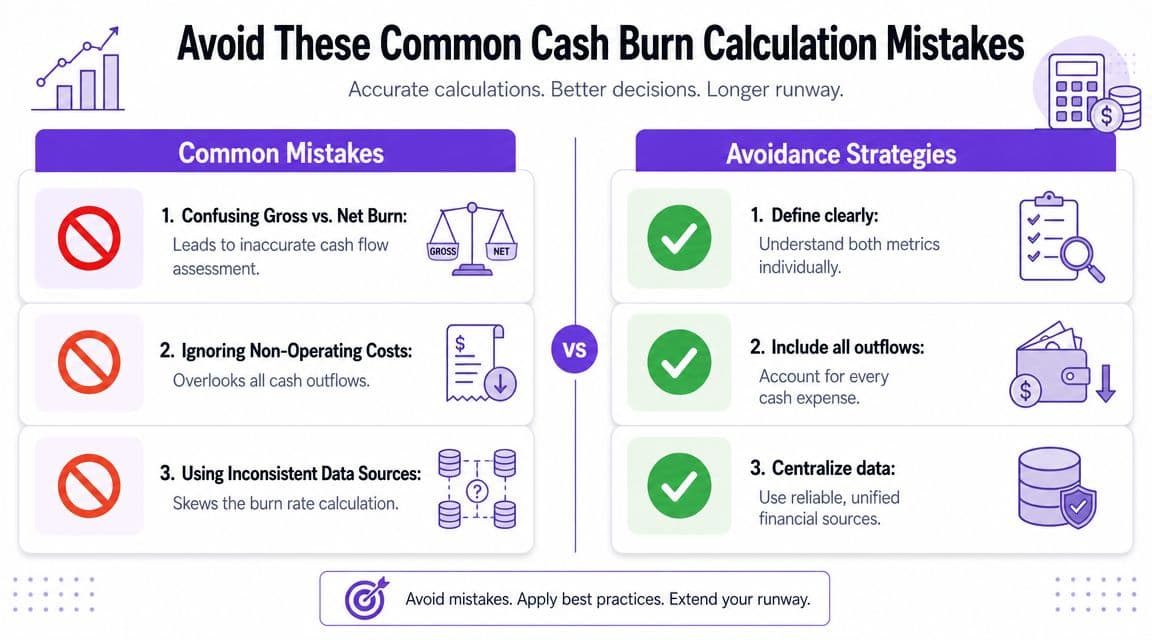

Avoid These Common Cash Burn Calculation Mistakes

Bad burn reporting creates fake confidence. That's more dangerous than bad news.

Red flags that distort burn

The biggest mistake is mixing accounting profit with cash burn. They are not the same thing. Workday's guidance is clear on this point in its cash burn calculation article: net burn can be positive even when EBITDA looks healthy, and the reverse can also be true, because burn is a cash-flow metric, not an accrual-profit metric.

That same Workday source also makes another point founders miss all the time: exclude non-cash items such as depreciation and amortization from gross burn because they don't use cash and will inflate the metric if you leave them in.

Here are the warning signs I watch for:

- You're using the P&L as the main source. That tells me you're probably mixing accruals, deferred items, and non-cash expenses into a cash metric.

- You included depreciation or amortization. Those belong in accounting profit analysis, not burn.

- Your burn jumps around because of annual bills. Insurance, retainers, sponsorships, and true-ups can wreck one month and flatter the next.

- Your reporting includes debt proceeds with customer cash. Borrowed cash extends runway. It doesn't mean operations improved.

Clean burn reporting removes non-cash noise and separates operating cash from financing cash.

A fast audit checklist

Use this checklist before you present burn to your board, lender, or leadership team:

| Check | What good looks like |

|---|---|

| Time period | Same monthly cut-off every time |

| Data source | Cash flow and bank-reconciled numbers |

| Expense treatment | Non-cash items excluded |

| One-offs | Clearly identified, not buried |

| Inflows | Actual cash receipts, not just invoiced revenue |

If any of those fail, fix the process before you trust the conclusion. Founders often want a more advanced dashboard when what they need is a cleaner number.

Your Burn Rate Is High Now What

A high burn rate isn't a math problem. It's a management problem.

Cut timing problems first

Don't start with layoffs because the burn number looks ugly. Start by separating timing pressure from structural overspend.

Look at receivables, billing speed, customer payment behavior, payroll timing, and vendor terms. A business can feel cash-starved because collections are slow, not because the cost base is broken.

Start here:

- Tighten invoicing discipline so bills go out immediately, not when someone remembers.

- Push on collections with owner-level follow-up for major accounts.

- Review software and subscriptions and cut tools no one uses.

- Renegotiate payment timing with vendors where possible.

- Pause discretionary spend until the cash picture stabilizes.

If you need a practical framework, this guide on how to improve cash flow is the right next move.

Fix the model not just the symptoms

Once you've handled timing, deal with the business model.

For SaaS, that usually means pricing, retention, customer acquisition efficiency, and gross margin discipline. For agencies, it usually means utilization, project scoping, change-order enforcement, and invoice timing. In both models, founders get in trouble when they defend every expense as “growth” without proving the cash return.

Ask these questions:

- Which costs directly support current revenue

- Which costs are bets on future growth

- Which costs exist because no one cleaned up the operating model

- Which customers or service lines create revenue but strain cash

That analysis is where real burn reduction happens. Not in broad panic cuts.

When to bring in outside finance help

DIY finance stops working when you can't trust your monthly numbers.

Bring in outside help when:

- Month-end close drags and leadership spends more time arguing about the data than acting on it

- Cash forecasting is unreliable and you don't know what the bank balance will look like in the coming weeks

- You're preparing for fundraising, debt, or diligence and need burn and runway reported cleanly

- Your tools don't agree and nobody owns the reconciliation process end to end

You don't need more dashboard screenshots. You need timely books, reconciled cash, and a forecast that lets you act before cash gets tight.

If your team needs cleaner burn reporting, tighter monthly closes, or a usable cash forecast, talk to Jumpstart Partners. They work with SaaS, agencies, and other growing businesses to turn messy books into decision-ready financials.