Financial Operations

LLC Conversion to C Corporation: Your 2026 Guide

Llc conversion to c corporation - Convert your LLC to C corporation seamlessly in 2026. Understand the process, tax impact, and financial operations with our

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··20 min readYou're ready to close a financing, hire senior talent, or clean up a cap table that has outgrown your original LLC structure. Then the main issue arises. The filing is the easy part. The hard part is everything that breaks right after the conversion if finance, payroll, banking, contracts, and tax reporting aren't lined up in advance.

That's why an LLC conversion to C corporation status should be treated as an operating change, not just a legal change. If you only focus on the state filing, you can still end up with failed payroll runs, rejected vendor payments, mismatched 1099s, broken investor reporting, and a due diligence trail that gets ugly fast.

Table of Contents

- The Moment Every Scaling Founder Faces

- The C Corp Conversion Decision Framework

- Choosing Your Conversion Path

- The Step-by-Step Conversion Playbook

- Post-Conversion Financial Operations The Mess No One Talks About

- Your Investor-Ready Conversion Checklist and Next Steps

The Moment Every Scaling Founder Faces

You get the term sheet. Economics look good. The investor is aligned. Then you hit the closing conditions and see the requirement that your LLC convert into a Delaware C corporation before money wires.

That moment catches a lot of founders off guard because the LLC worked fine when the business was simpler. Pass-through taxation felt efficient. Member units felt manageable. Governance was lightweight. Then growth changed the equation.

For SaaS firms, agencies, and professional services businesses, the pressure usually arrives at the same time. You want a cleaner equity structure, you need stock-based compensation that future hires understand, and you need an investor-friendly governance model that institutional capital recognizes immediately. The legal mechanism matters here. A true LLC-to-C-corp conversion is often handled as a statutory conversion or merger under state law, and in Delaware-style conversions the company typically files a Certificate of Conversion and a Certificate of Incorporation so the business continues without dissolving and restarting, as explained in The Tax Adviser's discussion of conversion mechanics.

Why investors push for the corporate form

A C corporation gives you a cleaner platform for:

- Preferred equity financing: Investors want a structure built for institutional rounds.

- Option grants and stock compensation: Employees, executives, and board members understand shares and option pools faster than LLC profit-interest structures.

- Governance: Board approvals, stock issuances, and investor rights fit a familiar framework.

- Exit planning: Buyers, later-stage investors, and diligence teams usually prefer a standard corporate package.

If you've already reached the point where you need stronger finance infrastructure, you'll recognize this as part of a broader maturity shift. The same inflection point often triggers a decision about when to hire a bookkeeper, controller, or CFO.

Most founders think the entity change is about legal paperwork. In practice, it's about whether your company is organized in the way investors and operators expect once the stakes get real.

The C Corp Conversion Decision Framework

The right time to convert is usually not the day your lawyer sends formation documents. It is the month you realize your LLC is starting to break your finance stack. The warning signs are practical: an investor asks for a clean cap table, payroll needs stock comp set up correctly, your tax preparer starts asking how member capital accounts will map into shares, and no one on the team has a clean answer.

A founder should make this call with three questions in mind. First, are you raising institutional capital on a real timeline. Second, will you need standard equity grants for hiring. Third, can your team handle the accounting, payroll, and reporting cleanup that starts right after the conversion is approved.

The tax and structural rationale for C corps

The legal filing gets the attention. The harder part is what changes underneath it.

An LLC is often efficient early because income and loss pass through to the owners, and the governance can stay flexible. A C corporation trades some of that simplicity for a format investors, payroll providers, auditors, and equity platforms already know how to process. That matters once you are issuing stock, approving option grants, and producing investor reporting on a deadline.

Here is the practical comparison.

| Factor | LLC (Limited Liability Company) | C-Corporation |

|---|---|---|

| Investor readiness | Often requires more explanation and custom diligence | Standard fit for venture and institutional financing |

| Equity administration | Profit interests and member units are harder to value and track | Common stock, preferred stock, and options fit standard workflows |

| Tax profile | Income generally passes through to members | Corporation files its own return, and dividends can be taxed again at the owner level |

| Governance | Flexible, but often drafted from scratch | Board approvals and stockholder actions follow a familiar pattern |

| Finance operations | Simpler at the start | Better fit for audited financials, option tracking, and formal reporting |

| Administrative load | Lower early burden | Higher annual maintenance and document discipline |

If your LLC agreement has special allocations, uneven vesting terms, or side arrangements between members, fix those before conversion. Counsel that handles business formations and contracts can spot issues that later turn into stock issuance errors, tax basis confusion, or investor diligence delays.

A tax example that actually changes the decision

Founders usually ask whether the C corp will cost more in taxes. Sometimes yes. Sometimes no. The answer depends less on the entity label and more on whether the business distributes cash or keeps reinvesting it.

Assume the company generates $1,000,000 of profit.

If it remains an LLC, that income generally passes through to the members, whether or not the company distributes the cash. That creates a common headache for scaling teams. Owners may owe tax on earnings they never received, while the company is trying to preserve cash for hiring or product development.

If it converts to a C corporation, the company files its own tax return. If profits stay in the business to fund growth, the founder may prefer that structure despite the corporate tax layer. If profits are paid out regularly, the second layer of tax on dividends becomes a real cost and should be modeled before anyone signs conversion documents.

The operational point is easy to miss. The tax structure changes how cash planning works after the conversion. It affects distributions, payroll mix, owner compensation, and board expectations around retained earnings.

Ownership continuity also matters. If the original LLC members do not end up with the required level of stock ownership after the reorganization, the conversion can trigger tax results the founders did not expect. In such instances, rushed side letters, advisor grants, and pre-close promises can cause expensive problems.

What usually gets underestimated

The primary cost is often not the filing. It is the cleanup.

Teams that wait too long usually inherit four problems at once. They have to translate LLC ownership economics into a stock ledger, rebuild historical equity records for diligence, reset payroll and tax accounts under the new entity, and explain the whole transition to investors using reports that were never designed for corporate equity. None of that is hard in isolation. All of it gets expensive when done under a financing deadline.

This is why I tell founders to look at the conversion as a finance systems project. If the company is already discussing option pools, board approvals, or future preferred rounds, the cap table needs to work in a corporate format before the first investor asks for it. A detailed review of capitalization table software for growing companies helps expose where ownership records, vesting schedules, and approval trails are still too loose for a C corp.

A good decision framework is simple: convert once the company needs corporate equity, investor-grade reporting, and a cleaner reinvestment structure, and before the ownership history becomes hard to reconstruct. That timing usually saves more money than delaying for one more quarter of LLC simplicity.

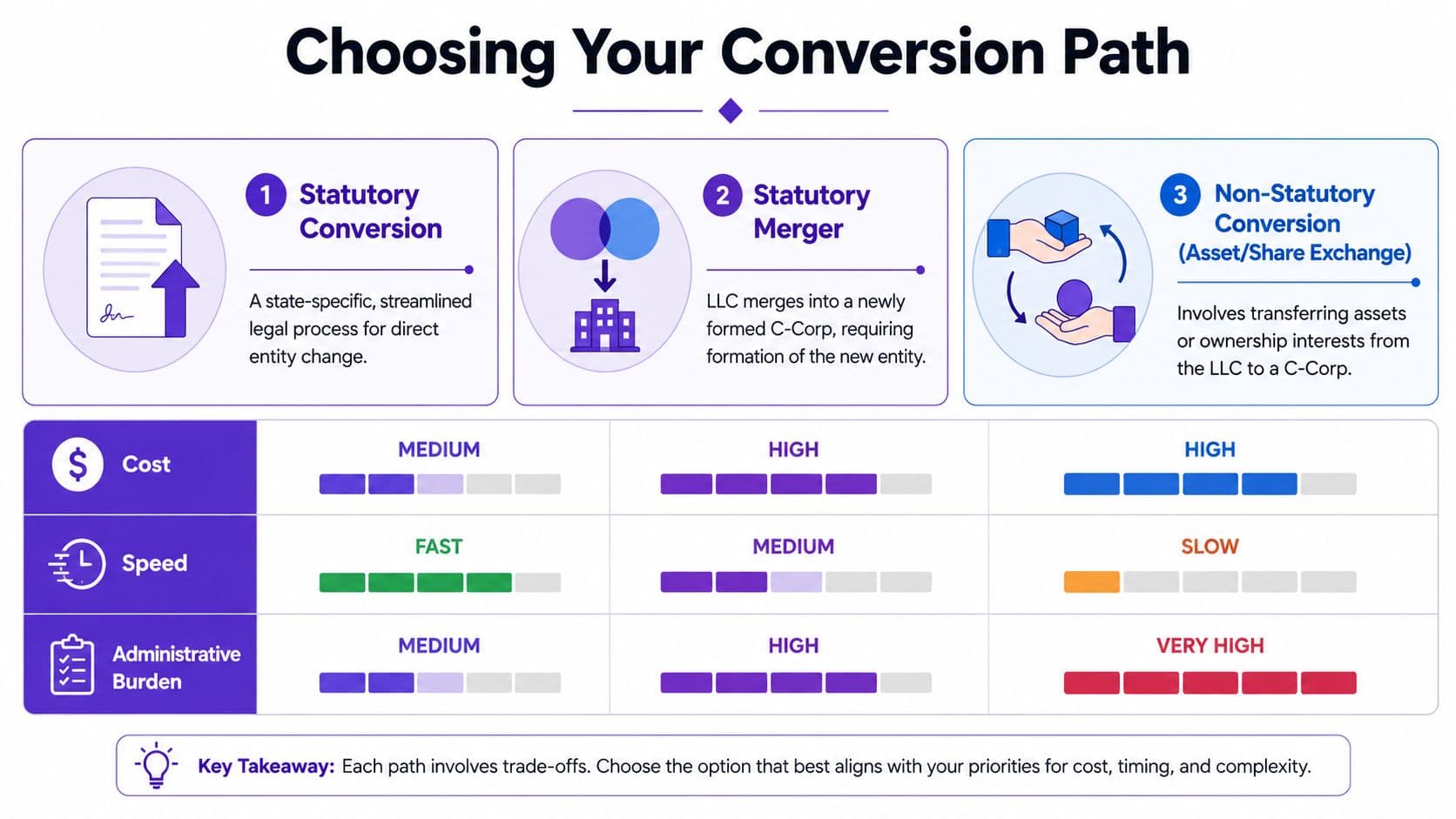

Choosing Your Conversion Path

The legal path sets the tone for everything finance has to clean up after closing. Choose the wrong structure and you can spend weeks fixing payroll registrations, re-papering contracts, and rebuilding ownership records that looked fine in the LLC but do not hold up in a corporate diligence file.

How the three paths differ in practice

An LLC usually becomes a C corporation through one of three routes: statutory conversion, statutory merger, or asset or interest transfer. The filing mechanics matter, but the bigger question is what survives cleanly on the other side. EIN treatment, contract assignment language, payroll accounts, sales tax permits, and historical financial reporting can all change depending on the path.

| Path | What it means in practice | Best use case | Main drawback |

|---|---|---|---|

| Statutory conversion | Direct entity change under state law | States that allow streamlined conversion and companies that want continuity across contracts, banking, and tax records | Finance still has to remap equity, update tax classifications, and confirm every downstream system reflects the new corporation |

| Statutory merger | A new corporation is formed and the LLC merges into it | Direct conversion is unavailable or counsel wants a cleaner entity structure for the next financing | More approvals, more documents, and more chances for vendor, bank, and payroll records to split between old and new entities |

| Asset or interest transfer | Assets or ownership interests are moved into a corporation | A fallback when state law, ownership issues, or deal terms block the other options | Highest administrative burden. Contracts, licenses, basis schedules, and balance sheet accounts often need the most rework |

Statutory conversion is usually the cleanest option when state law allows it. The company keeps its operating history, which reduces disruption in banking, vendor onboarding, and contract continuity. It does not remove the hard part. Finance still has to convert member economics into a stock ledger, reset equity accounts on the balance sheet, and make sure payroll and tax filings switch to the right entity classification on the effective date.

A merger can be the better answer even when it feels heavier on paper. I see this choice when the existing LLC records are messy, ownership terms need to be reset before a round, or counsel wants a new corporate shell with cleaner governance from day one. The extra legal work can save money later if it avoids a broken cap table or conflicting approval history.

When the cleanest path is not available

If your state does not support direct conversion, expect more than extra filing fees. Expect operational drag.

A merger or transfer structure often means:

- a new corporation with separate organizational documents

- new or updated banking, payroll, and tax registrations

- contract consent review for customers, landlords, lenders, and software vendors

- more detailed reconciliation between the LLC trial balance and the opening corporate books

That last point gets missed. If assets move into a new corporation, accounting has to prove what moved, at what value, and how retained earnings or member capital balances translate into corporate equity. If that work is sloppy, your first corporate close turns into a cleanup project. Your first corporate tax return does too. Teams should review what Form 1120 requires from a new corporation before the conversion becomes effective, not after the first filing deadline appears on the calendar.

The expensive path is usually the one that creates ambiguity. Ambiguity around ownership, tax accounts, and opening balances is what slows financings and raises diligence costs.

The Step-by-Step Conversion Playbook

A clean conversion is less about filing forms and more about controlling the cutover date. I've seen founders get the state approval on Friday, then spend the next month fixing payroll, rebuilding the cap table, and explaining to investors why the stock ledger does not match the old LLC ownership records.

That is avoidable if the work happens in the right order.

The sequence that keeps deals from slipping

The practical sequence is simple. Confirm who has authority to approve the transaction. Lock the ownership mapping. File the state documents. Build the corporate governance records. Then update every finance, payroll, and tax system that still thinks the LLC exists.

If that order changes, cleanup gets expensive fast.

Use this project plan.

-

Review the operating agreement

Confirm the approval threshold, any notice requirements, and whether the agreement already defines how membership interests convert into corporate stock. If it does not, legal and finance need one written conversion method before anyone signs. -

Approve the plan of conversion Set the effective date, document the equity exchange, and decide how tax basis, capital accounts, and any outstanding founder loans will be treated. During this step, vague language creates future diligence problems.

-

Prepare and file state documents

File the conversion, merger, or formation documents required for your structure and jurisdiction. Match the legal effective date to a finance close date if possible. A month-end cutover is usually easier to reconcile than a mid-month switch. -

Build the corporate records package

Adopt bylaws, appoint the initial board, authorize shares, issue founder stock, and create the stock ledger. If outside investors are coming, make sure the authorized share count, par value, and option pool assumptions work for the next financing, not just for the filing. -

Set up tax, payroll, and banking under the new entity

Update the EIN treatment if required, bank accounts, payroll provider, state tax registrations, AP systems, and vendor onboarding records. Teams that use outsourced small business HR solutions should confirm the legal employer name, payroll tax accounts, and employee benefit enrollments before the first payroll run under the corporation. -

Rebuild the books, not just the entity file

Convert the LLC balance sheet into an opening corporate balance sheet that supportable accounting can defend later. Retained earnings, additional paid-in capital, founder note balances, and any historical distributions need a clear home. If your pre-conversion books are already cluttered, fix them first with a focused QuickBooks cleanup service before you load bad history into the new structure.

A useful walkthrough can help your team visualize the legal mechanics before you start the execution work:

Red flags that create expensive cleanup

The filing date is only one milestone. The operating risk starts right after it.

The first red flag is sloppy equity conversion. If LLC units, profits interests, SAFE side letters, or founder vesting terms do not translate cleanly into stock ownership, the first version of the cap table will be wrong. Fixing that after a financing counsel review costs more than fixing it before filing.

The second is contract exposure. Customer MSAs, leases, debt documents, IP assignments, and software agreements may restrict assignment or require notice. A missed consent can delay invoicing, trigger a lender question, or force re-papering during diligence.

The third is accounting carryover. Founders often assume the old chart of accounts can stay as-is. It usually cannot. Member distributions, partner capital accounts, and LLC equity labels need to be retired or reclassified so the first corporate close and the first Form 1120 tie to the same story.

Watch for these problems:

- Approval gaps: Missing signatures, missing board actions, or inconsistent consent dates can undermine the transaction record.

- Equity mismatches: The legal stock issuances, cap table software, and accounting entries must agree share for share.

- Mid-cycle payroll changes: A payroll run under the wrong entity can create W-2, state withholding, and benefit deduction corrections.

- Bank and vendor lag: If vendors still bill the LLC while the corporation pays the invoice, AP and audit trails get messy.

- Loose opening balances: If no one can explain how LLC equity became corporate equity, investor diligence gets slower and more expensive.

Founders usually focus on getting the conversion approved. Finance should focus on whether the company can close the month, run payroll, issue stock, and answer diligence questions the day after approval. That is the true test.

Post-Conversion Financial Operations The Mess No One Talks About

Most articles stop when the state approves the filing. That's exactly where finance work begins.

The conversion changes how your business shows up in systems, documents, tax reporting, payroll records, and investor materials. If you don't run a coordinated cutover, you end up with one business operating under two identities at once. That confuses banks, payroll providers, vendors, customers, and your own accounting team.

What changes on day one

From a tax-planning standpoint, timing matters beyond the filing date. A mis-timed conversion can forfeit future QSBS eligibility, and the practical method is to model the conversion date, then verify the corporation's balance sheet and capitalization before issuing founder stock or completing an exchange. The same event can also trigger a new EIN and require vendors to issue future 1099s to the corporation rather than the LLC, as described in First Citizens' guidance on LLC-to-C-corp timing and QSBS planning.

That means finance should treat day one like a cutover checklist, not a memo.

| Area | Immediate action |

|---|---|

| Accounting | Close LLC books through the effective date and open C-corp books cleanly |

| Banking | Confirm whether existing accounts can stay or whether new accounts are required |

| Payroll | Move payroll provider records to the new entity and verify tax setup before the next run |

| AP and vendors | Update W-9 information, legal entity name, and remittance details |

| Equity records | Replace member-unit logic with stock records and a formal ledger |

| Reporting | Update monthly board, investor, and management reports to the new entity |

How to prevent reporting breaks

Operators demonstrate their critical role. You don't want legal to finish on Friday and finance to “figure it out next week.”

Use this order of operations:

- Close the LLC books cleanly: Reconcile cash, AR, AP, debt, payroll liabilities, and owner accounts through the effective date.

- Stand up the new reporting structure: Corporate equity, retained earnings logic, board approvals, and stock issuances need separate records.

- Coordinate with payroll and HR: If you use providers like Gusto, Rippling, or BambooHR, get entity changes queued before the next payroll cycle. For companies that need broader people-ops support during transitions, tools and providers focused on small business HR solutions can help organize benefits, onboarding, and compliance updates.

- Update counterparties fast: Banks, large vendors, insurance carriers, and customers with formal procurement systems need revised entity information.

- Fix 1099 and vendor data immediately: Waiting until year-end creates reconciliation headaches.

If your AP team still pays bills from the LLC account after the corporation is effective, your “completed conversion” is only true on paper.

The operational fallout after state approval is often underexplained. Agreements may require third-party consent, and a conversion can force a new bank account, EIN change, or updated vendor reporting. That issue is highlighted in DWT's analysis of startup LLC-to-corporation conversion follow-through.

One more practical point. Time the conversion around a clean reporting boundary when you can. Finance teams usually prefer a month-end or quarter-start effective date because it reduces split-period confusion in revenue, payroll, tax reporting, and investor updates.

Your Investor-Ready Conversion Checklist and Next Steps

A founder usually feels “done” when the state accepts the filing. Finance is usually just getting started. The ultimate test is whether the company can close the next month correctly, run payroll under the right entity, issue stock from clean records, and answer investor diligence without a scramble.

Use this checklist to judge whether your conversion is investor-ready:

- Write down the business case in board-level terms: Fundraising, option grants, governance, and tax posture are common reasons. If the reason is vague, the execution usually is too.

- Confirm ownership maps cleanly from LLC interests to stock: Your cap table, stock purchase documents, board approvals, and founder vesting terms need to match. If they do not, diligence will find the mismatch.

- Check the tax structure before you celebrate: Nonrecognition treatment often turns on continuity and execution details. Treat the ownership threshold discussed earlier as a planning checkpoint, then have tax counsel confirm the actual structure used.

- Set a hard operational cutover date: Accounting, payroll, AP, AR, expense tools, banking, and tax registrations should all change on the same timeline. A legal conversion with a split finance process creates avoidable rework.

- Close the books around the conversion date: Reconcile cash, equity, loans, and member capital accounts before opening the new corporation ledger. If you skip this step, retained earnings and paid-in capital often end up wrong for months.

- Re-paper equity administration immediately: Option plan adoption, stock issuances, 83(b) tracking where relevant, and board consents should be organized in one place before you start talking to investors.

- Prepare a diligence file, not just a filing receipt: Investors want a coherent package. Formation documents, approvals, tax elections, stock records, payroll setup, and financial statements should tell the same story.

Security and controls tend to get reviewed at the same stage. If enterprise customers or larger investors are part of the plan, SOC2Auditors' guide to SOC 2 readiness is a useful reference for tightening the control environment alongside the entity change.

I have seen the expensive version of this cleanup many times. The conversion documents are signed, but payroll still runs under the old entity, vendor W-9s are stale, the cap table does not tie to signed consents, and the first institutional investor asks for a diligence folder that no one can assemble in one pass.

That is fixable, but it costs time, legal fees, and credibility. A disciplined review against an investor-facing financial due diligence checklist helps catch broken workflows before your next round, acquisition discussion, or audit request.

If you're planning an LLC conversion and want the finance side handled correctly, Jumpstart Partners helps growing companies manage the accounting transition, post-conversion cleanup, investor-ready reporting, and day-one operational cutover so the legal filing doesn't create months of downstream mess.