Financial Operations

Nonprofit Fund Accounting: 2026 Guide to 990 & Restricted

Master nonprofit fund accounting. Our 2026 guide explains restricted/unrestricted funds, Form 990 compliance, & reporting for audit-ready organizations.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··19 min readThe most common advice on nonprofit accounting is also the most dangerous: “accounting is accounting.” If you come from SaaS, agencies, or professional services, that sounds reasonable. You already know accruals, close cycles, deferred revenue, board reporting, and cash forecasting.

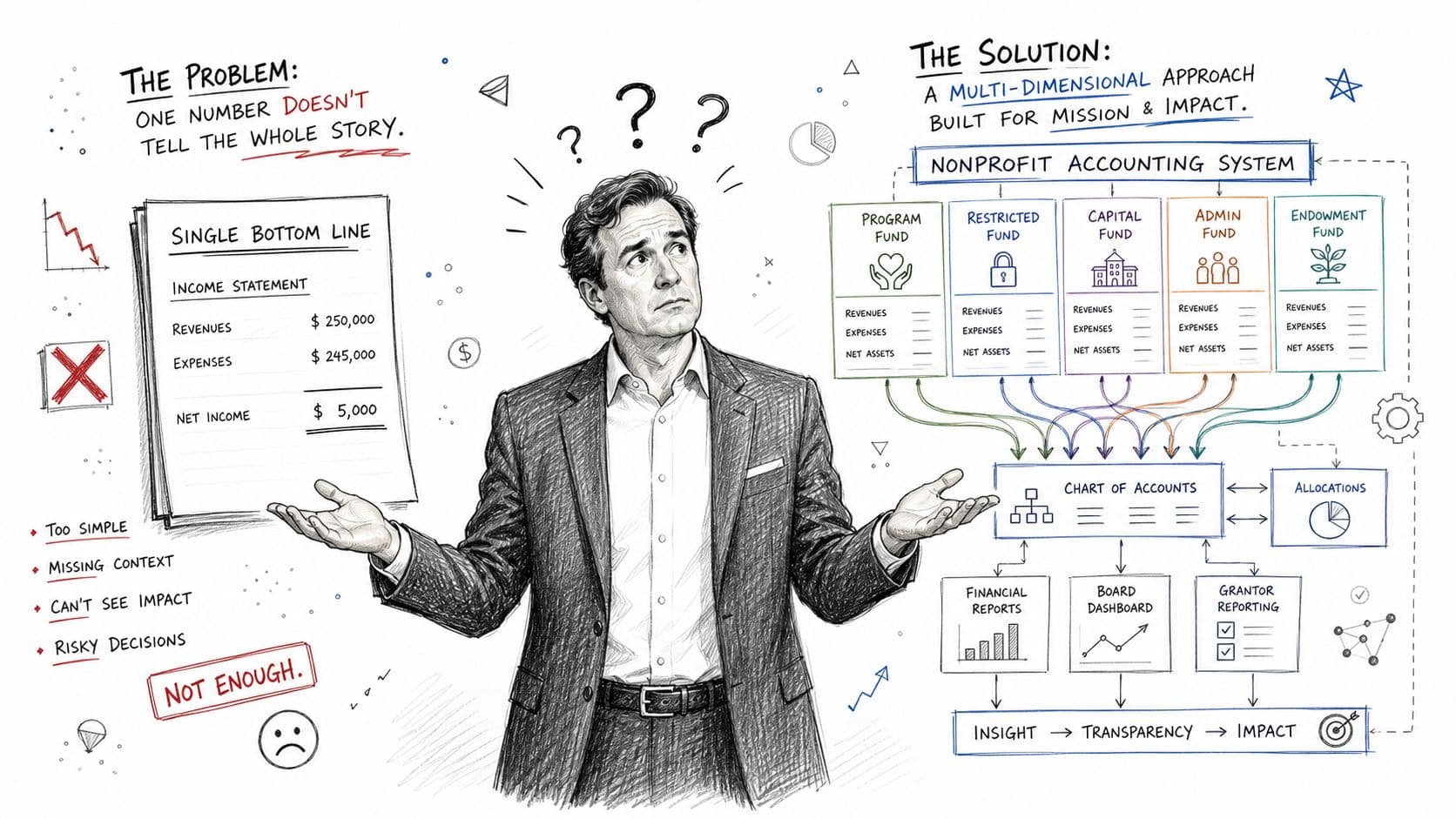

But nonprofit fund accounting breaks if you apply standard for-profit logic. In a company, you manage one economic engine and ask whether the business is profitable. In a nonprofit, you steward multiple pools of money with different legal and donor-imposed rules and ask whether each dollar was used the way it was promised. If your system can't prove that, your reports aren't just messy. They're risky.

That's why a generic setup in QuickBooks, a flat chart of accounts, or a spreadsheet-based restriction tracker creates real problems. You end up with a clean-looking P&L that tells the wrong story. If you're entering or advising a nonprofit board, this is the mindset shift that matters most.

Table of Contents

- Why Standard Accounting Fails Nonprofits

- Understanding Restricted vs Unrestricted Funds

- How to Structure Your Chart of Accounts

- Practical Journal Entries for Fund Accounting

- Essential Financial Reports and Compliance

- Red Flags and How to Avoid Common Mistakes

- Choosing the Right Tools or Expert Help

Why Standard Accounting Fails Nonprofits

If you run a business, your accounting system is built to answer one dominant question: are you creating value after expenses? Nonprofits use accounting to answer a different question: did you use each resource according to its intended purpose?

That difference changes everything.

Fund accounting is a specialized accounting system used by nonprofits, governments, and educational institutions. It separates finances into distinct funds with their own purposes, rules, and reporting requirements instead of treating cash as one shared pool, as explained in this overview of fund accounting basics for nonprofits. If you import for-profit habits into that environment, your instinct becomes a liability.

A founder usually sees cash and asks, “Can we use it to cover payroll?” A nonprofit finance leader has to ask two questions first: “What fund is this in?” and “What restriction applies?” That's not a semantic distinction. It's the difference between stewardship and misuse.

One pool of money is the wrong mental model

In for-profit accounting, one general ledger can tell a pretty complete story. In nonprofit fund accounting, the same setup often hides the very thing stakeholders need to see. A donor may fund a youth program, a foundation grant may cover a specific initiative, and board-designated reserves may support something else entirely. If you collapse those into one operating view, you lose control over compliance.

Practical rule: If your reporting can't show what came in, what was spent, and what remains by fund, your close process isn't finished.

That's why workaround-heavy systems fail. The issue isn't that a general ledger can't record debits and credits. It's that the structure doesn't naturally enforce restrictions, functional reporting, or grant-level accountability. Teams often try to patch that gap with classes, spreadsheets, and manual reconciliations. The result looks manageable until month-end, year-end, or audit prep.

If you want a clean contrast between oversimplified bookkeeping and a real accounting system, this explanation of single-entry accounting system limitations is useful background. Nonprofits don't need less structure. They need more dimensionality.

What actually breaks when you use for-profit logic

A standard setup usually creates four predictable failures:

- Restriction leakage: Money intended for one purpose gets used elsewhere because the ledger doesn't enforce fund boundaries.

- Bad management reporting: Your board sees totals, not fund-level reality.

- Grant compliance pain: Reporting becomes a manual reconstruction exercise.

- Credibility loss: Donors and auditors ask basic stewardship questions your reports can't answer cleanly.

Nonprofit fund accounting isn't “specialized” in the abstract. It's specialized because the underlying obligation is different.

Understanding Restricted vs Unrestricted Funds

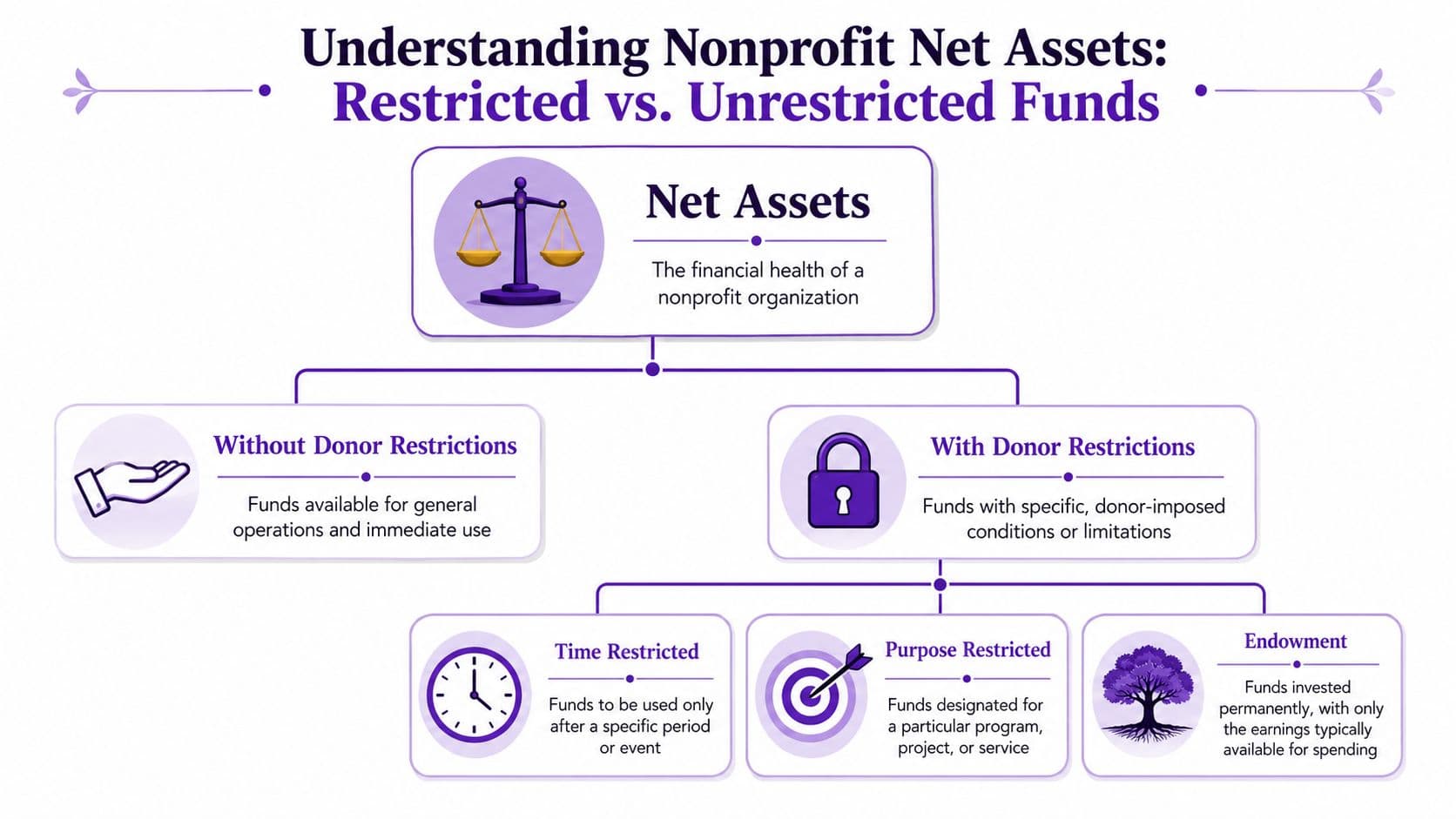

The first concept to get right is not grants, not Form 990, and not audit prep. It's net asset classification.

Under FASB ASC 958 as amended by ASU 2016-14, nonprofits report net assets in two classes: with donor restrictions and without donor restrictions. That simplified the old three-class presentation, but it did not relax stewardship. It sharpened it.

The classification that actually matters

If you're used to reading a balance sheet through the lens of liquidity and enterprise value, this can feel backwards. In nonprofit fund accounting, classification tells you whether the organization has the right to use resources freely.

Here's the plain-English version:

| Net asset class | What it means | Operational implication |

|---|---|---|

| Without donor restrictions | Funds available for general use | Can support payroll, rent, admin, fundraising, and mission delivery based on board and management decisions |

| With donor restrictions | Funds limited by donor-imposed purpose or timing | Can only be used when the specified purpose is met or the time restriction lapses |

That second category includes situations a for-profit operator would instinctively treat as available cash. The money may already be in the bank. It still isn't available for general operations if the donor restricted it.

A practical analogy for for-profit operators

Think of each fund as a client portfolio with its own investment mandate. If one client says “large-cap dividend stocks only,” you don't buy venture debt because another portfolio needs yield. The capital may sit on the same custodian platform, but fiduciary duty applies at the portfolio level.

Nonprofit funds work the same way. A gift for a building campaign doesn't become payroll money because the checking account balance is high. A grant for a literacy program doesn't cover IT unless the grant terms allow it. The accounting system has to preserve that discipline.

Restricted cash in a nonprofit behaves more like managed capital under a mandate than like general operating cash in a startup.

That's also why budgeting changes. You don't build one budget and fill the top line with “revenue.” You map funding sources to allowed uses, then determine what unrestricted support is still required. This guide to budgets for nonprofit organizations is helpful if you need to translate that into planning mechanics.

Midway through that learning curve, many leaders benefit from seeing how the same principles show up in adjacent sectors. A practical example is this explanation of fund accounting for churches, where designated gifts and general operating funds create the same stewardship challenge.

A short visual walkthrough helps if this still feels abstract:

The mistake to avoid is treating “restricted” as a note on a donation record. It's a ledger, reporting, and decision-making issue.

How to Structure Your Chart of Accounts

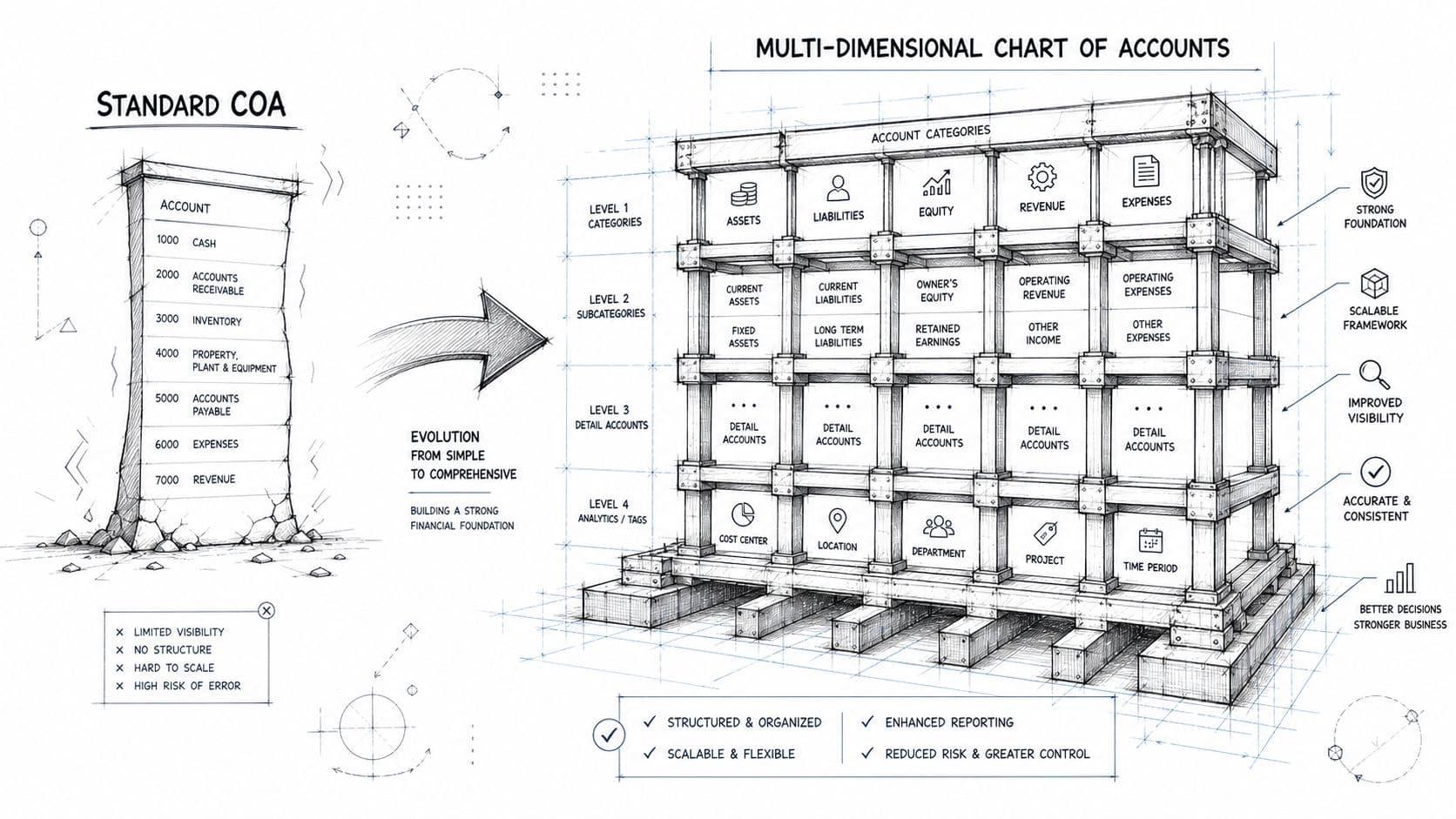

Most for-profit companies can survive with a flat chart of accounts plus departments or classes. Nonprofits usually can't. The structure has to support fund-level reporting from the first transaction entry, not after a spreadsheet cleanup.

A workable nonprofit fund accounting setup uses a multi-segment chart of accounts structured as Fund-Program-Grant-Account, which aligns with the Unified Chart of Accounts framework and can reduce IRS Form 990 filing errors by up to 30%. That's not cosmetic. It's the engine behind accurate board reporting, grant reporting, and audit prep.

Why a flat chart breaks reporting

A flat chart gives you entries like Salaries Expense, Rent Expense, Grant Revenue, and Donations. That may be enough for a small agency with one revenue stream. It's not enough when one salary line needs to answer four questions at once:

- Which fund paid it?

- Which program benefited?

- Which grant supports it?

- What kind of cost is it?

Without those dimensions, your month-end close turns into archaeology.

What works: encode reporting logic in the chart and transaction tags.

What fails: export the trial balance and rebuild fund views manually in Excel.

A chart structure that works in practice

Here's a simple example of a salary transaction coded in a nonprofit environment:

| Segment | Example value | Meaning |

|---|---|---|

| Fund | 220 | Youth Services Restricted Fund |

| Program | 410 | After-School Program |

| Grant | 115 | Foundation Grant A |

| Account | 6100 | Salaries Expense |

Full string: 220-410-115-6100

That single coded line gives you immediate visibility into whether salary costs hit the right restricted fund, the correct program, the correct grant, and the right expense category.

A flat for-profit string might just be 6100 Salaries Expense. Clean. Fast. Useless for nonprofit stewardship.

Here's how to build the structure:

- Start with funds first: unrestricted operating, donor-restricted purpose funds, time-restricted funds, and endowment-related funds as needed.

- Layer in programs: these reflect mission activities, not just departments.

- Add grant identifiers: use these only where reporting obligations exist.

- Keep the natural account list disciplined: don't create duplicate expense accounts to solve a tagging problem.

If you're drafting or cleaning this up, a nonprofit chart of accounts template can save time. For teams starting from scratch, a simple builder like the ReceiptsAI accounting tool can help map the account architecture before you implement it in QuickBooks, NetSuite, or another ledger.

The rule is simple. If your chart design can't produce reports by fund without manual manipulation, redesign it before volume grows.

Practical Journal Entries for Fund Accounting

Theory matters, but journal entries show whether your system really works. A good nonprofit ledger should tell the full story of a restricted grant from award to spending to release.

For a multi-year grant where the grantor commits to all payments upfront, nonprofits must record the present value of future payments as revenue in the award year. In the example outlined in this guide to accounting nonprofit fund accounting, a $100,000 three-year grant with a 5% discount rate is initially recorded at approximately $91,574, with the difference recognized as interest income over the pledge period.

Entry one for a multi-year grant

Assume the nonprofit receives an unconditional three-year restricted grant for a program.

Initial entry at award:

| Transaction | Account Debited | Account Credited |

|---|---|---|

| Record present value of multi-year grant receivable | Grants Receivable $91,574 | Contribution Revenue with Donor Restrictions $91,574 |

If you're from a SaaS background, think of this as the opposite of your usual instinct. You're not spreading revenue because the work happens over time. You're recognizing the contribution based on the nature of the commitment.

A double-entry refresher can help if you're translating this from commercial accounting language into nonprofit logic. This overview of double-entry bookkeeping in accounting is a useful baseline.

Entry two for spending against the grant

Now assume the organization incurs a qualifying program salary expense funded by that grant.

| Transaction | Account Debited | Account Credited |

|---|---|---|

| Record eligible program salary expense paid from the restricted fund | Salaries Expense | Cash or Accounts Payable |

The critical detail is not the debit and credit alone. It's the coding. That salary should be tagged to the correct fund, program, and grant segment so the expense lands in the right reporting bucket.

Entry three for releasing the restriction

When the organization satisfies the donor restriction by incurring the allowed expense, it reclassifies net assets.

| Transaction | Account Debited | Account Credited |

|---|---|---|

| Release restriction after qualifying use | Net Assets with Donor Restrictions Released from Restriction | Net Assets without Donor Restrictions Released from Restriction |

That release entry is where many operators get tripped up. They record the revenue. They record the expense. Then they forget the reclassification that tells the financial statements the restriction was satisfied.

The release entry doesn't move cash. It updates the accountability story.

One more practical note. If the grant is conditional rather than unconditional, revenue is recognized only as the conditions are met. That distinction drives timing and often determines whether your board is looking at a reliable operating picture or a misleading one.

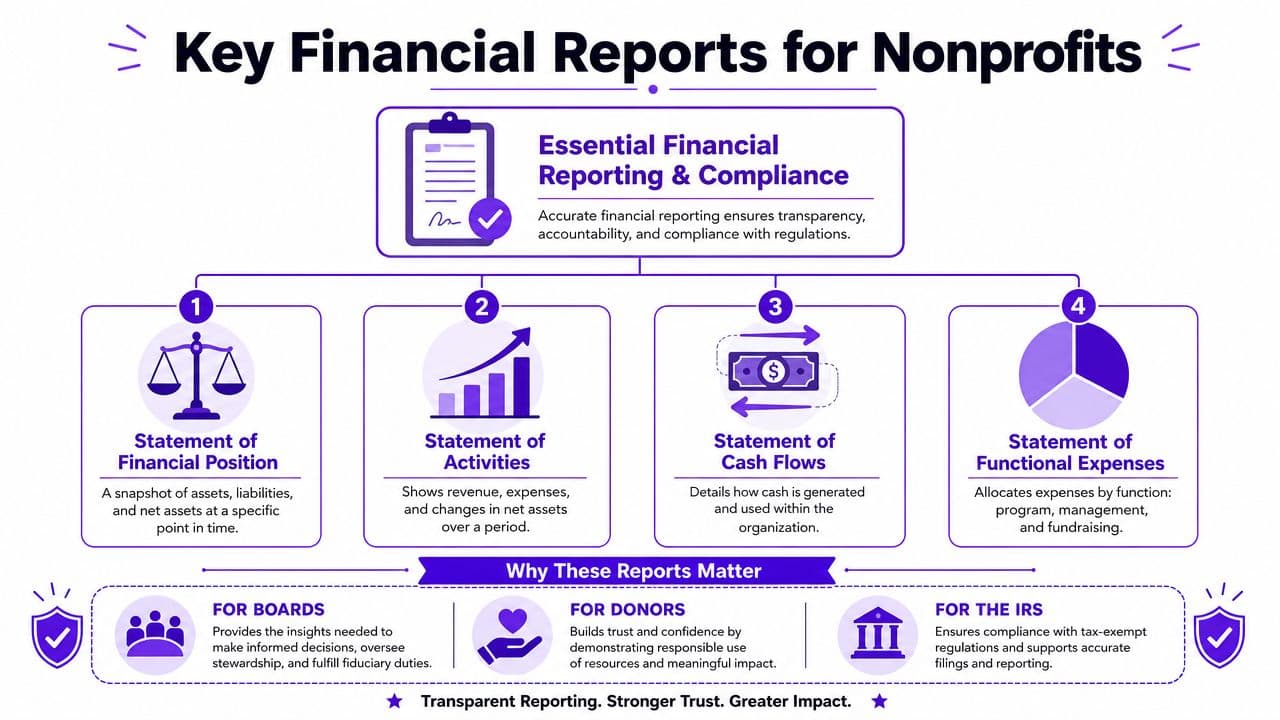

Essential Financial Reports and Compliance

A standard startup reporting pack will mislead you in a nonprofit if you read it the same way you read a SaaS dashboard. Revenue can look strong while cash is restricted. Cash can look healthy while it is already spoken for by grant terms. A clean month-end close still fails if the organization cannot show donors, auditors, and the IRS how money was used.

Nonprofits rely on four core statements: the Statement of Activities, Statement of Financial Position, Statement of Cash Flows, and the Statement of Functional Expenses. The first three will feel familiar to a for-profit operator. The fourth changes the conversation. It sorts spending by program, management and general, and fundraising, which means the accounting system has to support both natural classifications like salaries and rent, and functional classifications tied to mission delivery and overhead.

What each report is really for

| Report | What it answers | Who cares most |

|---|---|---|

| Statement of Financial Position | What does the organization own and owe, and how are net assets classified? | Board, lenders, auditors |

| Statement of Activities | What revenue came in, what expenses were incurred, and how did net assets change? | Board, management, donors |

| Statement of Cash Flows | Where did cash come from and where did it go? | Finance leaders, board |

| Statement of Functional Expenses | How were expenses allocated across program, management and general, and fundraising? | Board, donors, IRS |

The Statement of Functional Expenses is usually the report that trips up founders coming from venture-backed companies. In a startup, you can often manage off department spend and gross margin. In a nonprofit, leadership also has to defend why executive time, occupancy, software, and shared services were charged to program, administration, or fundraising. If those allocations are weak, the issue is not presentation. It is governance.

Boards should see these reports on a regular cadence, not only at audit time. Form 990 is annual, but management discipline is monthly. Quarterly board packets are the minimum I like to see for smaller organizations. Larger or grant-heavy nonprofits usually need monthly reporting because restriction releases, grant burn rates, and liquidity can shift faster than the board expects.

A worked benchmark calculation

Liquidity matters, but nonprofit liquidity needs a different lens than a for-profit current ratio. The practical question is how long the organization can keep operating with resources it can spend.

Formula: expendable net assets ÷ daily total expenses

Worked example:

- Expendable net assets: $600,000

- Annual total expenses: $1,200,000

- Daily total expenses: $1,200,000 ÷ 365 = about $3,288

- Reserve ratio: $600,000 ÷ $3,288 = about 182 days, or roughly 6 months

That result points to a solid operating cushion.

The catch is that reserve math can create false comfort. If a material share of net assets is donor-restricted, board-designated for another purpose, or tied up in illiquid assets, the organization may look stable on paper and still have very little room to make payroll. I tell boards to ask two questions at the same time: how much do we have, and how much is available for general operations?

Compliance follows from reporting quality. If the ledger is coded correctly, Form 990 prep is mostly a mapping exercise. If it is not, year-end turns into cleanup, reclassification, and uncomfortable board explanations. A structured year-end close checklist for nonprofit reporting and reconciliations helps keep close tasks, support schedules, and filing deadlines in order.

Red Flags and How to Avoid Common Mistakes

Most nonprofit accounting failures don't start with fraud. They start with shortcuts that seem harmless. A spreadsheet to track grant balances. A rough allocation for rent. An endowment draw approved without a written policy.

Then the audit starts.

A major blind spot is shared cost allocation. According to this guide to fund accounting for human services organizations, improper or undocumented indirect cost rates account for 40% of audit findings in human services organizations. That's a technical accounting issue, but it's also a leadership issue. If management can't explain how executive salaries, IT, occupancy, and other common costs are allocated, the system isn't under control.

Warning signs that show up fast

Here are the red flags I watch for first:

- One spreadsheet tracks all grant balances: that usually means the general ledger can't produce fund-level truth on its own.

- Shared costs are allocated using stale percentages: if program activity changed, old allocations become hard to defend.

- Restriction releases happen only at year-end: that delays visibility and distorts interim board reporting.

- Endowment draws are approved informally: boards often underestimate how quickly poor policy erodes restricted capital.

- Form 990 prep starts with trial-balance cleanup: that's a signal the ledger structure isn't doing its job.

The endowment point deserves special attention. It's easy to think of endowments as static assets on the balance sheet. They're not. They require board discipline, spending policy, and reporting discipline around what can be drawn and why.

Controls that actually prevent problems

You don't fix these issues with more heroic work at year-end. You fix them with controls.

| Red flag | Control to implement |

|---|---|

| Spreadsheet-only grant tracking | Require every restricted transaction to carry fund and grant coding in the ledger |

| Vague shared-cost allocations | Adopt a written cost allocation policy tied to actual program utilization and document the support monthly |

| Delayed release entries | Close restrictions monthly, not annually |

| Informal endowment decisions | Approve a documented board policy for endowment spending and reporting |

| Manual 990 mapping | Build reporting categories into the chart and review them before year-end |

Weak controls in nonprofit fund accounting usually look efficient right up until someone asks for proof.

One common objection is that this feels overly burdensome for a smaller nonprofit. It isn't. The burden comes from fixing weak accounting after the fact. A disciplined setup reduces work because the ledger produces usable answers all year.

Choosing the Right Tools or Expert Help

Many organizations waste time by asking, “Can QuickBooks handle nonprofit fund accounting?” The honest answer is: sometimes, but often with too many workarounds.

General accounting tools can post transactions. The critical question is whether your setup can reliably handle restricted funds, grant-level reporting, allocation logic, and nonprofit financial statements without a parallel spreadsheet system.

Software trade-offs in the real world

| Approach | Strengths | Trade-offs |

|---|---|---|

| QuickBooks with workarounds | Familiar, accessible, lower implementation burden | Heavy reliance on classes, custom reports, and manual controls |

| Cloud ERP or nonprofit-focused system | Better dimensional reporting, stronger controls, cleaner fund reporting | More setup work, stronger process discipline required |

| Expert-managed accounting stack | Better system design, fewer internal bottlenecks, stronger close discipline | Requires outsourcing comfort and clear ownership lines |

Sarah Johnson, CPA and lead nonprofit controller at Jumpstart Partners, puts it plainly:

“Many nonprofits try to force QuickBooks to do fund accounting with complex workarounds, but they spend more time fighting the software than analyzing their finances. True fund accounting software or an expert-managed system isn't a cost; it's an investment in compliance and donor trust.”

That's the right framing. Software isn't the strategy. The operating model is.

When DIY stops making sense

You should stop treating this as a DIY finance problem when any of these conditions are true:

- You have multiple active restricted grants: manual tracking starts breaking under volume.

- Your board wants cleaner fund-level reporting: leadership expectations have outgrown the setup.

- You're handling endowment activity or more complex donor restrictions: judgment and policy matter more.

- Your month-end close depends on one person's spreadsheet: that's operational risk, not efficiency.

- Your fundraising operation is scaling: for example, a church evaluating online giving for small churches still needs the back-office accounting structure to classify and report those funds correctly after the donation platform collects them.

The right move isn't always a new system. Sometimes it's a chart redesign, a better close process, or specialized controller support. But once complexity crosses a certain threshold, generic bookkeeping stops being cheap. It becomes expensive rework.

If your organization needs cleaner nonprofit fund accounting, better board reporting, or a finance setup that can support audits and donor restrictions without spreadsheet chaos, talk to Jumpstart Partners. Their team helps growing organizations build reliable accounting processes, close faster, and produce financials you can trust.