Financial Operations

Private Equity Accounting: Your 2026 Essential Guide

Navigate private equity accounting. Master waterfalls, fair value, ASC 606, & investor reporting to satisfy PE partners. Essential guide for CEOs & CFOs.

ByJumpstart Partners, CPA, QuickBooks ProAdvisor

··22 min readIn McKinsey's 2025 private equity report, buyout deals larger than $500 million increased 44% to over $1 trillion in value, and the median private equity purchase multiple rose to 11.8x EBITDA. If your company was acquired in that environment, your finance function now has one job above all others: produce numbers that can stand up to board scrutiny, lender scrutiny, and exit scrutiny.

That's why private equity accounting feels so different from the accounting you ran before the deal. Your old close process may have been good enough for managing cash and filing taxes. It isn't good enough when investors are measuring value through fair value marks, return metrics, and a timeline that pushes your team to close fast without breaking GAAP.

For SaaS companies, agencies, and professional services firms in the $500K to $20M revenue range, the hardest part isn't learning new acronyms. It's connecting your day-to-day accounting decisions, especially revenue recognition, accruals, and reporting quality, to the way your PE sponsor measures fund performance. That bridge is where most confusion lives, and it's where finance teams either gain credibility or lose it.

Table of Contents

- You Have a PE Partner Now What

- Fund vs Portfolio Company Accounting

- Key PE Fund Metrics That Now Drive Your Business

- Your New Accounting Mandates Under PE Ownership

- The Investor-Ready Reporting Package

- Common Pitfalls and How to Fix Them

- Building Your PE-Ready Finance Function

You Have a PE Partner Now What

After a private equity acquisition, the standards for your accounting function shift immediately.

Before the deal, many companies managed the business with a monthly P&L, cash on hand, and a few operating KPIs. After the deal, the same numbers are used for board decisions, lender reporting, purchase price support, and the sponsor's assessment of whether the investment thesis is tracking. From the CEO seat, that usually feels like the business changed. In practice, the business may be the same, but the tolerance for ambiguity is much lower.

That is the part management teams often underestimate.

The sponsor is not asking for cleaner reporting because it prefers prettier financials. It needs timely, supportable results because your operating performance now feeds fund-level reporting and valuation work. If revenue is booked inconsistently, if accruals move around without support, or if deferred revenue swings without a clear driver, the issue does not stay inside your monthly close. It shows up in board materials, lender questions, and fair value discussions above the company level.

What changes on day one

Your finance team now needs to close the books fast enough for decision-making and with enough support to stand up to audit and diligence review.

That usually means three immediate changes:

- The monthly close becomes a repeatable control process. The close now produces information used in board packages, covenant calculations, and sponsor reporting. A close that depends on memory, side schedules, and late manual entries will break under PE ownership.

- Revenue accounting gets tested early. SaaS terms, implementation work, variable consideration, retainers, and contract modifications need a documented accounting position that your team can apply consistently under ASC 606.

- Forecast accuracy starts with accounting accuracy. Sponsors do not separate weak actuals from weak forecasting. If the historical numbers need heavy cleanup every month, confidence in the forecast drops with them.

A simple test works well here. If a board member asks why EBITDA missed plan and your team cannot produce a reconciled answer the same day, the finance function needs work.

Newly acquired CEOs usually feel the first strain in reporting cadence. The sponsor wants monthly results faster, more detail by product or location, and fewer post-close revisions. At the same time, the company may still be running on a chart of accounts built for tax prep and lender reporting, not sponsor scrutiny. That mismatch creates friction fast.

I see the same pattern in newly acquired businesses. The company tries to meet PE expectations with the processes that got it through the sale process. Those processes were built for a transaction. PE ownership requires a finance function that can reproduce diligence-grade reporting every month. For a practical view of what gets reviewed before and after close, see this guide to private equity due diligence.

Fund vs Portfolio Company Accounting

Your sponsor and your company look at the same business through different lenses.

The fund uses a telescope. It sees your company as one investment inside a portfolio. It cares about value, timing, and how your performance affects fund returns.

You use a microscope. You care about invoices, payroll, deferred revenue, utilization, churn, collections, and accruals. Those details are operational. But they're also what support the fund's big-picture view.

The telescope view

At the fund level, private equity accounting is governed by ASC 946, which allows investment companies to use fair value accounting for investments even when ownership percentage would otherwise point toward consolidation, as outlined in this ASC 946 private equity accounting guide. Most PE investments land in Level 3 of the fair value hierarchy, which means valuations rely on unobservable inputs and require extensive disclosure under ASC 820.

That matters to you because your operating results support those valuation judgments.

If your revenue recognition is inconsistent, your EBITDA bridge is sloppy, or your close leaves material accruals out, the sponsor's fair value mark gets harder to defend. Auditors notice that immediately.

The microscope view

At the company level, you still need clean GAAP financials. You still need receivables reconciled, payroll posted correctly, and revenue recognized under the contract terms.

But now your accounting has to do one additional thing. It has to translate into investor language.

Here's the practical difference:

| Perspective | Main question | Primary focus |

|---|---|---|

| Fund accounting | What is this investment worth now, and what return is the fund earning? | Fair value, NAV, IRR, distributions |

| Portfolio company accounting | What happened operationally this month, and is it reported correctly under GAAP? | Revenue, expenses, accruals, cash flow, controls |

Your sponsor doesn't need you to run fund accounting. They need you to produce company-level accounting that is reliable enough to feed fund-level reporting.

The mistake many CEOs make is assuming these are separate conversations. They aren't. If your controller misstates deferred revenue, your board deck is wrong. If your board deck is wrong, the sponsor's valuation discussion is weaker. If valuation support is weak, you'll feel it in audit friction, lender questions, and exit preparation.

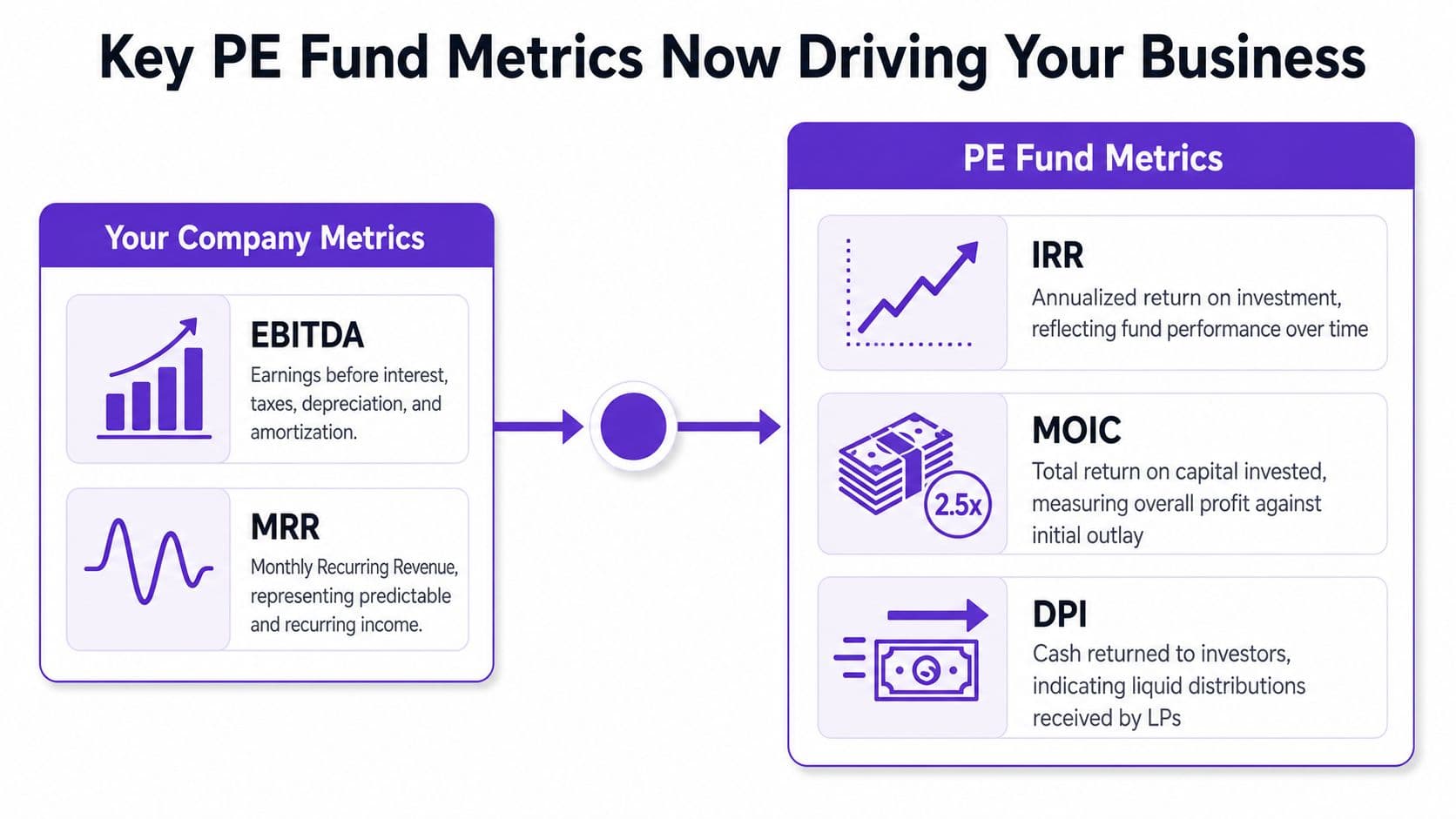

Key PE Fund Metrics That Now Drive Your Business

Your board may ask about MRR, utilization, and gross margin. Your sponsor is also tracking how your performance affects TVPI, DPI, RVPI, and IRR.

That's why your company's results now need to connect to the economics of the fund.

The metrics your sponsor cares about

Under the GIPS private equity standards, fund performance reporting commonly includes TVPI, DPI, RVPI, and Since Inception IRR. The same standards discussion also notes that the waterfall is one of the most scrutinized parts of private equity accounting, and that a typical hurdle rate is 8% with 20% carried interest for the GP.

For a portfolio company CEO, the practical translation is simple:

- TVPI tells investors the total value created relative to capital paid in.

- DPI tells them how much cash has been distributed back.

- RVPI tells them how much value remains unrealized.

- IRR tells them how quickly the investment is generating returns.

Your operating performance affects all four, even if you never calculate them inside your ERP.

A worked waterfall example

Most founders hear “waterfall” and tune out because it sounds like fund legalese. Don't. Incentives become real at this stage.

Use this simplified example:

| Step | Calculation | Result |

|---|---|---|

| Capital invested by LPs | Starting amount | $10,000,000 |

| Exit proceeds from sale of portfolio company | Cash available to distribute | $15,000,000 |

| Return of LP capital | First $10,000,000 goes back to LPs | $10,000,000 |

| Preferred return to LPs | 8% hurdle on $10,000,000 | $800,000 |

| Remaining profit pool after capital and hurdle | $15,000,000 - $10,800,000 | $4,200,000 |

| GP carried interest | 20% of $4,200,000 | $840,000 |

| LP share of remaining profit | 80% of $4,200,000 | $3,360,000 |

In this example, total distributions are:

- LPs receive $13,360,000

- GP receives $840,000

That's a simplified waterfall. Actual LP agreements often add catch-up provisions, holdbacks, reserves, and deal-specific terms. But the point is clear. Once your company creates value above invested capital and the hurdle, the sponsor participates directly through carry.

A CEO who understands the waterfall understands why sponsors care so much about timing, clean exits, and earnings quality.

If you want your operating dashboard to line up better with how investors interpret performance, this primer on SaaS financial metrics is a useful companion.

What management fees mean to you

Management company economics are different from fund returns, but they shape sponsor behavior. The ASC 946 discussion in the earlier source notes that management companies commonly collect 2% annual management fees on committed capital. You don't account for that fee in your operating books as fund carry, but you do feel the expectations it creates.

Sponsors need timely information. They need board materials that explain not just what happened, but whether value creation is tracking the investment case.

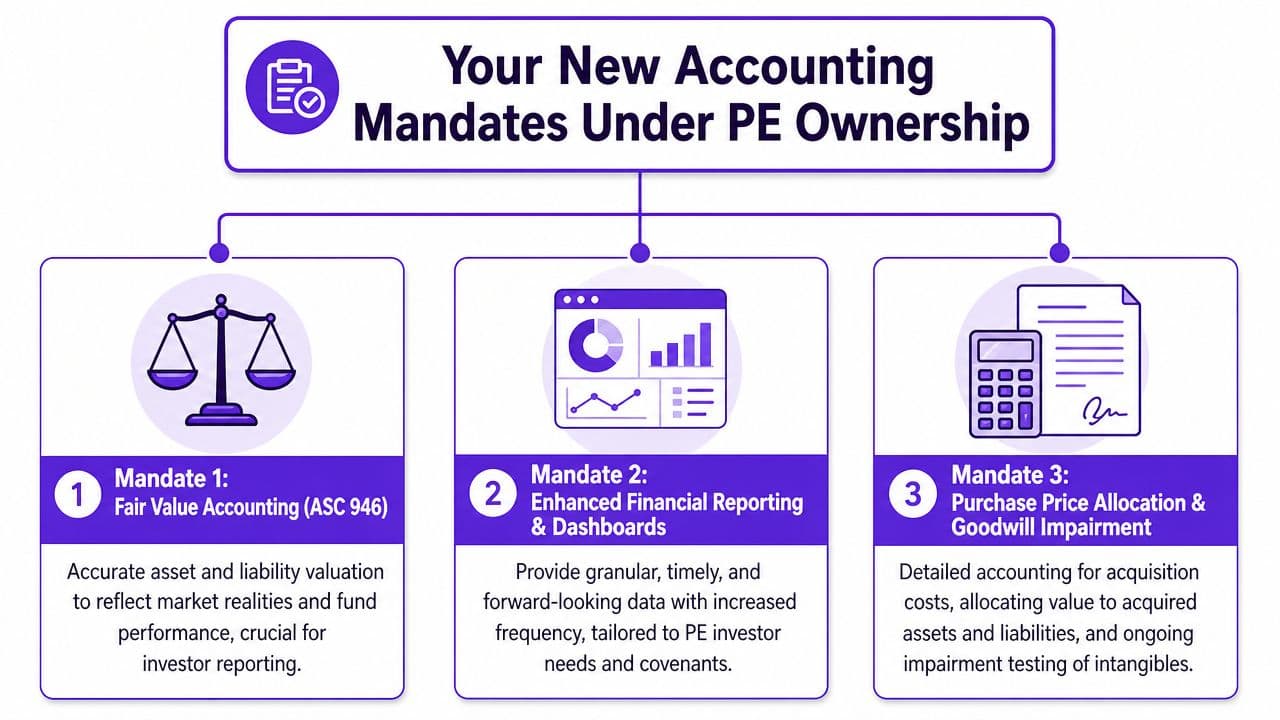

Your New Accounting Mandates Under PE Ownership

Your company doesn't become a fund after a PE deal. But your accounting does need to support fund-level valuation, investor reporting, and transaction readiness. In practice, that usually means three mandates rise to the top fast: fair value support, ASC 606 discipline, and purchase accounting around contingent terms.

Fair value support is no longer optional

Because PE funds operate under ASC 946 and rely heavily on Level 3 inputs under ASC 820, your reported results need to support valuation logic with more rigor than most founder-led businesses are used to.

That changes management behavior in a few ways:

- Forecasts need support. If revenue assumptions drive a mark, the sponsor will ask how those assumptions connect to pipeline, churn, backlog, and collections.

- Adjustments need documentation. One-off EBITDA add-backs don't count just because management says they're nonrecurring.

- Narrative matters. The valuation file needs a coherent explanation for changes in performance, not just a spreadsheet.

A weak close creates weak valuation evidence. Auditors push hardest where management relies on judgment, and Level 3 marks are full of judgment.

The video below gives a helpful overview of the accounting framework around these issues.

ASC 606 changes what counts as earned revenue

For private companies, ASC 606 became effective for annual reporting periods beginning after December 15, 2018, which made December 31, 2018 the first reporting date for many calendar-year private companies under the standard, according to EisnerAmper's ASC 606 effective date summary. If your sponsor acquires a services or software company today, they expect revenue policy to already be compliant.

The rule that often catches PE-backed companies is collectibility. Under the Certinia summary of ASC 606 and IFRS 15 differences, revenue under ASC 606 is recognized only when it is probable that collected consideration won't change, and the probable threshold is 75% to 80% under US GAAP, compared with 50% under IFRS 15.

Here's a simple worked example.

A SaaS company signs a $120,000 annual contract billed monthly. If management concludes collectibility isn't yet probable under ASC 606 because the customer has payment issues, the company can't recognize the first month's $10,000 as revenue just because service started. It may need to delay recognition until collectibility is sufficiently supported.

That changes reported EBITDA immediately.

| Scenario | Revenue recognized this month | Immediate EBITDA effect |

|---|---|---|

| Collectibility is probable | $10,000 | Higher reported EBITDA |

| Collectibility is not yet probable | $0 | Lower reported EBITDA until threshold is met |

At this point, operational accounting meets sponsor expectations. If your board is benchmarking performance to an acquisition model, delayed revenue recognition can make the business look weaker in the short term even when bookings are strong.

Transition choices still affect trend analysis

The MASource discussion of ASC 606 transition methods notes that companies adopted the standard using either full retrospective treatment or modified retrospective treatment. If your historical periods straddle that transition, comparing old growth rates to current results can be messy.

That's one reason PE-backed finance teams need a monthly memo on policy elections, unusual contract treatment, and changes in estimates. Without that discipline, board members end up comparing numbers that were prepared on different accounting bases.

Earnouts and contingent consideration need early attention

PE deals often include earnouts, rollover equity, or post-close adjustments tied to performance. The accounting answer depends on deal structure and purchase accounting analysis. The practical point for management is simpler: don't leave these items in legal documents and assume finance will “book it later.”

If a term in the purchase agreement changes who gets paid based on future performance, accounting needs to evaluate it immediately.

That review becomes much easier when your close process is documented and repeatable. For teams tightening that process, these month-end close best practices are worth implementing before the next board cycle.

The Investor-Ready Reporting Package

A PE sponsor doesn't just want financial statements. They want a reporting package that explains liquidity, operating performance, and whether the investment thesis is on track.

For most portfolio companies, the practical standard is a fast close paired with a board pack that management can defend. If your team can send statements but can't explain cash movement, deferred revenue changes, or variance drivers, you're still underbuilt.

What should be in the monthly package

Use a package that ties accounting, operating metrics, and forward visibility together.

| Report Component | Key Content | Purpose |

|---|---|---|

| Consolidated financial summary | P&L, balance sheet, cash flow summary, prior-month comparison | Gives the board a clean snapshot of financial position and recent movement |

| Budget vs actual variance analysis | Revenue, payroll, software spend, contractor costs, gross margin, EBITDA bridge | Shows where performance diverged from plan and whether issues are structural or timing-based |

| KPI dashboard | SaaS metrics such as MRR and churn, or agency metrics such as utilization, billable rates, and project margin | Connects accounting output to operating performance |

| 13-week cash flow forecast | Weekly cash receipts, payroll, debt service, vendor disbursements, expected shortfalls | Helps management and investors see liquidity pressure before it becomes a crisis |

| Revenue recognition memo | Material contracts, nonstandard terms, deferred revenue movement, ASC 606 judgments | Gives support for earnings quality and reduces audit and board questions |

| AR and collections report | Aging, disputed invoices, top overdue balances, collections actions | Tests whether booked revenue is converting to cash |

| Capex and debt schedule | Fixed asset additions, financing changes, covenant tracking | Supports lender conversations and board oversight |

| Executive narrative | Key wins, misses, hiring changes, customer concentration issues, forecast risks | Translates numbers into decisions |

Why the cash flow package matters more than most teams think

Many founder-led companies focus too heavily on the income statement after a deal. Sponsors don't. They care about liquidity, especially when growth, debt service, or integration costs are putting pressure on cash.

If your team needs a refresher on presenting a cash flow statement for loans, that walkthrough is useful because lenders and investors often want to see how earnings convert, or fail to convert, into actual cash.

Clean EBITDA with weak cash conversion creates board tension fast. The reporting package needs to show why cash moved, not just that it moved.

Who uses which report

Don't make the mistake of building one generic packet for everyone.

- Board members want concise interpretation and variance drivers.

- The PE operating team wants KPI-to-financial alignment and forecast credibility.

- Lenders care about liquidity, covenant support, and debt capacity.

- Auditors care about support, consistency, and documentation.

If you need a template to standardize this, review these financial reporting package examples and adapt them to your business model.

Common Pitfalls and How to Fix Them

Start with the close. That is where newly acquired portfolio companies usually feel the pressure first.

PE sponsors want speed because they are managing lender reporting, board materials, valuation support, and fund-level timelines. Your finance team still has to get the basics right at the company level, including revenue recognition, accruals, reconciliations, and cash reporting. The conflict is practical, not theoretical. If the team rushes through operational accounting, the sponsor gets numbers faster but trusts them less.

A 5-day close can work. It fails when recurring entries are still being booked as post-close cleanup, contract terms are reviewed after billing, or KPI reporting sits outside the general ledger with no monthly reconciliation.

I see the same pattern after acquisitions. The company keeps its pre-deal habits, then adds sponsor reporting on top of them. That creates two accounting systems in practice: one for running the business and another for explaining it to the PE firm. The fix is to build one process that supports both.

Red flags

Watch for these warning signs:

- Recurring entries show up as top-side adjustments. If payroll accruals, commissions, bonuses, or deferred revenue are still being cleaned up after close, your process is not stable.

- The KPI deck does not tie to the GL. Bookings, MRR, gross margin, and recognized revenue need a documented bridge every month.

- Valuation support lives in email and meeting notes. That creates problems for quarterly fair value support and year-end audit requests.

- Contract review starts after invoicing. By then, ASC 606 errors are already in the month, and reversing them creates avoidable noise.

- The board pack changes format every month. Trend analysis gets weaker, and management spends review time arguing about presentation instead of performance.

What fixes these issues

The answer is disciplined workflow design, clear owners, and a monthly reporting package that ties operating results to sponsor expectations.

| Pitfall | What actually works |

|---|---|

| Fast close produces weak accruals | Build a pre-close calendar, estimate recurring accruals with a documented method, and limit post-close entries to unusual items |

| KPI reporting conflicts with financials | Assign one source of truth for each metric and reconcile dashboard logic to the GL every month |

| Fair value support is thin | Keep a valuation file with forecasts, customer concentration, debt details, and documented management judgments |

| Revenue issues surface late | Route contract changes through finance before billing and document treatment for setup fees, implementation work, retainers, and variable consideration |

| Auditors find control gaps | Assign named owners for reconciliations, approvals, and review sign-offs, with due dates and evidence retained monthly |

One trade-off deserves attention. A sponsor may accept a reasonable estimate on day five if the methodology is consistent and the true-up is small. They will not accept a close that looks fast because the team skipped reconciliations or deferred obvious judgment calls. Speed helps only when the support holds up under audit, lender diligence, and quarterly valuation review.

This situation highlights the conflict between operational accounting and sponsor expectations. The portfolio company has to produce GAAP-ready numbers for the business while also giving the sponsor inputs that affect NAV, lender reporting, and ultimately IRR. If those two tracks are disconnected, every month-end turns into a debate.

That is one reason companies often bring in outsourced controller support for PE-backed reporting environments. The value is not extra hands alone. It is getting a close process, reporting package, and documentation standard that work for management, auditors, and the sponsor at the same time.

A common misconception

Some CEOs assume the sponsor only cares about headline EBITDA. In practice, sponsors care about EBITDA that survives scrutiny. They want earnings backed by clean revenue cutoffs, supportable add-backs, credible accruals, and cash conversion that makes sense.

If your team smooths results with aggressive reserves or deferred expenses, review the risks around "Kons Law helps recover investment losses" and similar accounting practices. PE ownership increases the scrutiny around those judgments, especially once lenders, auditors, and exit buyers start testing quality of earnings.

The finance team that performs well under PE ownership closes on time, ties KPIs to the ledger, and keeps support ready before anyone asks for it. That is what builds confidence with the board and reduces surprises during diligence.

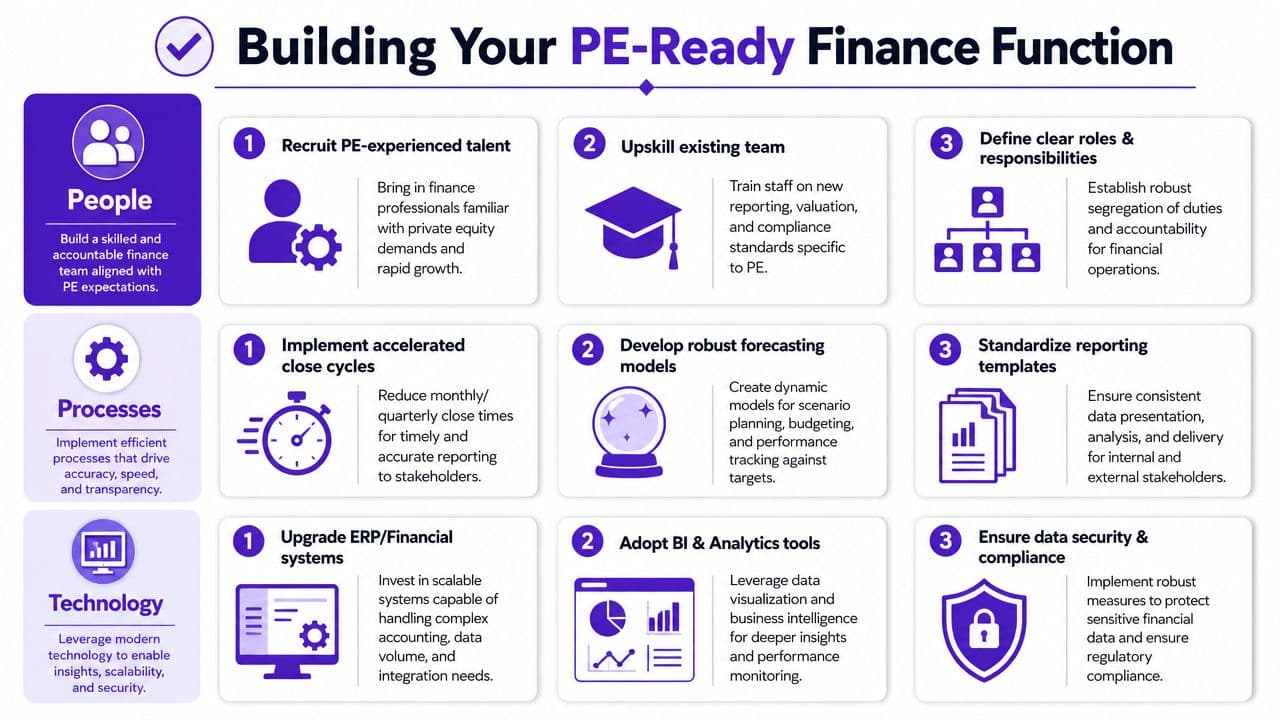

Building Your PE-Ready Finance Function

A PE-ready finance function rests on three things: people who understand the environment, processes that run on schedule, and systems that can produce defensible reporting without spreadsheet chaos.

If one of those three is weak, the rest of the structure wobbles.

Start with a practical checklist

For a newly acquired portfolio company, this is the prep list that matters most:

- Lock your accounting policies. Document revenue recognition, accrual thresholds, capitalization rules, and approval workflows.

- Clean the chart of accounts. Separate recurring operating activity from owner-era noise, personal expenses, and one-time deal costs.

- Create a month-end close calendar. Assign owners, due dates, and review points for reconciliations and board reporting inputs.

- Build a contract review lane. Finance needs visibility into customer terms before they hit billing.

- Stand up a cash forecast. Weekly cash visibility matters more under PE ownership than most founder-led teams expect.

- Prepare an audit file monthly. Don't wait for year-end to gather support.

- Organize your data room. Board decks, debt agreements, cap table data, major contracts, and policy memos should be easy to retrieve.

Checklist rule: If a reviewer needs to ask where support lives, the process still depends too much on individual memory.

Choose systems that can scale with scrutiny

You don't need a giant enterprise stack on day one. You do need tools that reduce manual work and produce consistent outputs.

For many companies in this revenue band, the core stack looks like this:

| Function | Common tools | What to look for |

|---|---|---|

| General ledger | QuickBooks Online Advanced, NetSuite, Xero | Strong close controls, class or location reporting, clean integrations |

| Billing and collections | Stripe, native invoicing tools, contract management workflows | Clear tie-out from bookings to billings to cash |

| Payroll and people data | Gusto, BambooHR | Reliable accrual support and headcount reporting |

| FP&A and dashboarding | Budget models, KPI dashboards, BI tools | Version control and one definition for each key metric |

A caution here matters. If your accounting gets sloppy under pressure, the legal and investor consequences can expand beyond a missed close deadline. For a plain-language discussion of how aggressive reporting practices can create deeper problems, this article on how Kons Law helps recover investment losses is a useful reminder of where weak financial discipline can lead.

Build internally or outsource intentionally

Many companies between $500K and $20M in revenue don't need a full in-house PE finance bench immediately. They do need controller-level discipline immediately.

That's why outsourced support often makes more sense than trying to hire a full team in a rush. The right partner can install the close process, reporting package, revenue workflows, and board support structure without forcing you to build the entire department from scratch.

If you're weighing that route, review what outsourced controller services typically include and compare it against your current internal gaps.

The test is simple. Your finance function is PE-ready when it can do three things consistently:

- Close on time

- Explain the numbers clearly

- Support the numbers with documentation

If your team can only do one or two, the next board cycle will expose it.

If you need help building that kind of finance function, Jumpstart Partners works with SaaS, agency, and services businesses that need a PE-ready close, investor-grade reporting, and stronger cash flow visibility without building the whole accounting department internally. A consultation is the fastest way to see where your current process will hold up, and where it won't.